It is a big week for economic data and the first address to Congress from the new President. Most of the punditry is engaged in a collective head-shake about overbought conditions. Even if the data flow remains strong, pundits will be asking:

Have stock prices lost touch with reality?

Last Week

Last week the economic news was mostly positive, and stocks responded.

Theme Recap

In my last WTWA I predicted a discussion about Trump policies and the business cycle. This was partially correct, but the prevailing theme – by a widespread margin – emphasized the likely delays in key economic policies. That will be a transition point for the week ahead.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. She notes yet another record close based on the week’s gain of 0.7%.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read his entire post for several more charts providing long-term perspective.

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something very positive. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

This week’s news was mostly positive.

The Good

-

Chemical activity increases. Calculated Risk tracks the improvement in this leading indicator.

-

Business executive optimism is reflected in Deloitte’s annual survey.

-

Michigan sentiment remained strong at 96.3

-

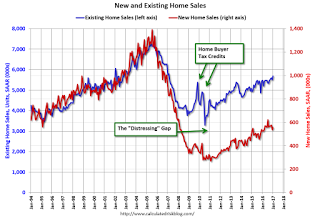

Existing home sales beat expectations, but are just 0.7% above a year ago. Inventory continues to decline.

-

Initial jobless claims rose slightly on the week, but dropped to the lowest level since 1973 on the widely-followed four-week moving average. (Calculated Risk).

The Bad

-

Hotel occupancy softened over the last few weeks (Calculated Risk).

-

New home sales missed expectations. The prior three months were all revised lower. While sales were up 5.5% year-over-year, the comparison months were among the weakest. Calculated Risk notes that these were the first months after mortgage rates moved higher and provides analysis and this key chart.

-

European tourism interest in America is down 12% after the travel ban. (Forbes).

The Ugly

Russia may have interfered with the Brexit vote say UK officials. Jake Kanter and Adam Bienkov have the story at Business Insider.

The Silver Bullet

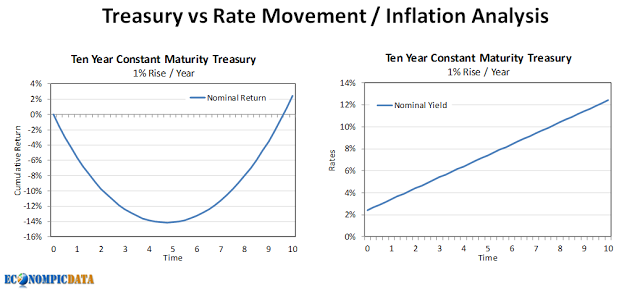

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. This week’s award goes to EconompicData, for an important and careful analysis of the effect of rising interest rates on bond investors.

The problem is that the debate over the Fed and interest rates became political. To maintain consistency, many argue that higher rates will be good for bond investors. Here is Jake’s summary of the problem:

I’ve read too many posts / articles that outline why a rise in rates is good for long-term bond investors (as that would allow reinvestment at higher rates). While this can be true depending on the duration of bonds owned and/or for nominal returns over an extended period of time, it is certainly not true over shorter periods of time and absolutely not true for an investor in most real return scenarios… even over very long periods of time.

There are a range of possible assumptions and consideration of each. Here is a key illustrative chart:

To summarize a great post – which bond investors should read carefully – higher rates will be great for future bond investors, but painful for those with current holdings.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

We have very big week for economic data, with all of the big reports except the employment situation.

The “A” List

- ISM index (W). Important for both concurrent and leading qualities. Strength continuing?

- Auto sales (W). More gains from a key sector or “peak auto?”

- Consumer confidence (T). Will the great strength continue?

- Personal income and spending (W). January data, but a very important business cycle series.

- Fed beige book (W). With the Fed resuming a role as a key worry, there will be extra attention.

- Initial jobless claims (Th). How long can the amazing strength continue?

The “B” List

President Trump’s first Address to Congress on Tuesday night will command attention in many ways. Most importantly for our purposes will be hints about legislative priorities and the Congressional reaction. Insider tip: Watch for things that get applause from both sides of the aisle.

Next Week’s Theme

The punditry, locked into a mindset about valuations, Trump policies, Fed significance, and daily preoccupation with what could go wrong is engaged in a collective head shake. Isn’t it obvious that many of the Trump policies will be delayed? Won’t this derail the “Trump Rally?”

The commentary increasingly expresses amazement, wondering:

Have Stock Prices Disconnected from Reality?

On one side, those who date the rally from the day of the election infer cause and effect. Anything that damages the prospects for tax and regulatory relief also damages the bullish story.

Another group notes that the market, after an extended period of strength is “overbought.”

An increasing number of observers is questioning whether Trump policies are actually the basis for the increase in stock prices.

If these policies are crucial, Tuesday night’s Presidential Address to Congress is definitely the key moment of the week – regardless of economic data.

What does this mean for investors? As usual, I’ll have a few ideas of my own in today’s “Final Thought”.

Quant Corner

We follow some regular great sources and the best insights from each week.

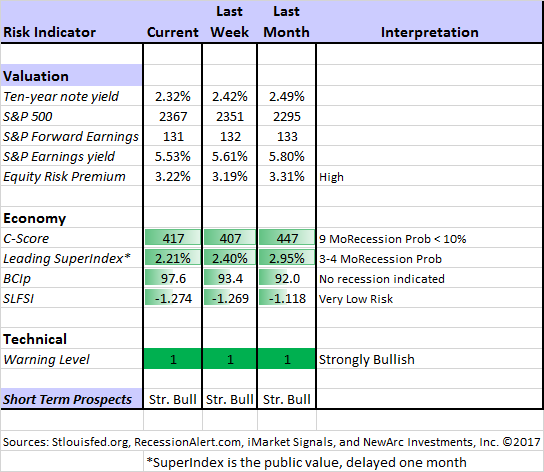

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment. (see below).

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

Doug Short: The World Markets Weekend Update (and much more).

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has several interesting approaches to asset allocation. Try out his new public Twitter Feed.

Georg Vrba: The Business Cycle Indicator and much more.Check out his site for an array of interesting methods. Georg regularly analyzes Bob Dieli’s enhanced aggregate spread, considering when it might first give a recession signal. His interpretation suggests the probability creeping higher, but still after nine months.

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies. His most recent post notes that the expected growth rate in S&P earnings is now 8.41% — the highest level since October, 2014.

The legal Marijuana business will create nearly 300,000 jobs by 2020.

How to Use WTWA (especially important for new readers)

In this series, I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. Most readers can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have eight different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

Most of my readers are not clients. While I write as if I were speaking personally to one of them, my objective is to help everyone. I provide several free resources. Just write to info at newarc dot com for our current report package. We never share your email address with others, and send only what you seek. (Like you, we hate spam!)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and the top sources we follow.

Felix and Holmes

We continue with a strongly bullish market forecast. All our models are now fully invested. The group meets weekly for a discussion they call the “Stock Exchange.” In each post I include a trading theme, ideas from each of our four technical experts, and some rebuttal from a fundamental analyst (usually me). We try to have fun, but there are always fresh ideas. Last week the focus was on sector rotation strategies, with a recent example from Oscar.

Top Trading Advice

Brett Steenbarger explains how knowledge is part of trading. He makes a powerful analogy between traders that can see both the macro and micro pictures and a quarterback who sees the entire field. His work always helps traders discover both what they should know, and how to learn it. While this was my favorite for the week, the daily posts should all be on the trader’s must-read list.

The early T-Wops (a negative Presidential tweet) had a negative impact on stocks. Traders learned this, of course, and the high-frequency algorithms did automated tracking. As often happens, once everyone catches on, things change. The WSJ shows that a Negative Tweet may not crush a stock

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Warren Buffett’s annual letter to his investors. It is full of wit and humor – and plenty of great insights. You can learn about tax policy, accounting issues, stock buybacks, and Mr. Buffett’s ten-year bet where he took the overall market versus hedge funds.

Stock Ideas

Mr. Buffett’s dividend stocks versus the “dogs of the dow.” Jon C. Ogg crunches the numbers.

Big biotech? Battered down, but with good earnings and cash flow. Some of the companies also have a pipeline. Check out some large cap choices.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. If you are a serious investor managing your own account, this is a must-read. Even the more casual long-term investor should make time for a weekly trip on Wednesday. Tadas always has first-rate links for investors in his weekly special edition. As usual, investors will find value in several of them, but my favorite is the post from Dan Danford. He explains the difference between excellent but general advice from experts and advice specific to your circumstances. Keep this in mind when reading the Warren Buffett letter. Here is a key quote:

Those experts don’t know a thing about you or your situation. They don’t know your age, health, marital status or personality quirks. They don’t know where you live or how much your house cost. They don’t know how much you spend on groceries or hobbies, or that you were forced into early retirement by an ungrateful employer. They know none of this. Nada.

Seeking Alpha Editor Gil Weinreich’s strong series is ostensibly aimed at financial advisors – a must-read for them. It also attracts many DIY investors. The zesty topic of the week started with an explanation from a noted writer and advisor, David Merkel, on why investors need good advice. I strongly agree with David, but I realize that some investors enjoy doing the work to maintain a successful program. (Is that you? My (free) short paper on the top investor pitfalls is a good test of whether you can successfully fly solo. Send a request to main at newarc dot com).

Watch out for…

Rising interest rates. In a riff on this week’s Silver Bullet analysis, Davidson (via Todd Sullivan) explains some key fundamentals about rates, the yield curve and the Fed. It is another myth-busting analysis.

Final Thoughts

How the punditry interprets the current market depends on how one defines base valuations and expectancy.

The result?

Most people choose the over-valued path. It is the conventional wisdom in the media. Even the bullish pundits choke out a statement that stocks are “reasonably valued.” This world view requires some explanation of why the stock rally continues. The explanation has changed over time —

- Stocks are overvalued and a crash is likely.

- A crash might not happen, but returns over the next five, ten, twelve years will be lower.

- Valuation is not a good method of market timing, and who knows when the “half-cycle” will end?

- Stock strength is due to extraordinary Fed policy, providing liquidity that banks or the plunge protection team use to buy stocks. It will end with the end of QE, which probably will never happen.

- The end of QE merely shifted focus to Europe, where the ECB has taken over the money printing.

- The current rally is based upon Trump promises, which will never come to pass and might not even work.

Investment Conclusion

I hope most will notice that the forward valuation approach and the recession data I report weekly is a simple explanation. The current market is what we would expect. The Republican victory had increased small business confidence, but is not the main driver of stock prices.

The prevailing explanation was wrong-footed at the start and has remained so. Like bad science, it has not explained anything, so it must be continually re-invented.

It is really not complicated. There will be a time to become cautious. Meanwhile, mid to late- stage cyclical stocks, financials, homebuilders, and technology remain attractive.

© NewArc Investments, Inc.

Read more commentaries by NewArc Investments, Inc.