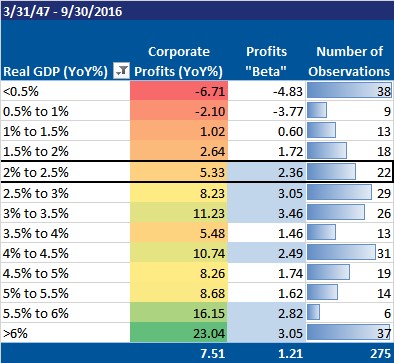

While the myth that stock market returns are highly correlated to a country’s GDP growth rate has largely been debunked, there remains a strong, and intuitive, relationship between corporate profits and GDP. GDP measures the output of an economy and corporate profits are simply the income to capital owners derived from that output (with some accounting adjustments made along the way). In the long-run, equity investors need to see growth in corporate profits in order to justify equity prices.

In the table below, we summarize the YoY change in before tax corporate profits (with IVA and CC adjustments) by various real GDP growth rates. We are using quarterly data from the NIPA accounts from 3/31/1947-9/30/2016. Let us explain what the table is illustrating by looking at an example. For instance, when the YoY change in real GDP growth is between 1% and 1.5% for any given quarter (we have had 13 such occurrences since 1947), corporate profits on average have increased by a little more than 1% on a YoY basis. Additionally, we have calculated a profits “beta” by taking the growth rate of corporate profits divided by the growth rate of real GDP and highlighted every instance where the beta is above 2x. The point of this calculation is to show how important real GDP growth is to corporate profits. When the profit beta is higher it means that the business community is able to squeeze more profits out of every dollar of GDP growth. This is why 2% real GDP growth is a key point for the US economy. When real GDP growth is between 0.5%-2%, the average profit beta is just 0.12x and the YoY change in corporate profits is just 1.05%. However, when real GDP growth is between 2%-2.5%, the beta jumps up to 2.36x and the YoY change in corporate profits increases to 5.33%. This is more than double the YoY% change in corporate profits when the economy is growing at just a bit slower growth rate between 1.5%-2%. When the economy is growing by over 2% and profits are growing by at least double that rate, the market should feel much more comfortable with the future and will most likely apply a higher multiple to current profits. That is a configuration that all equity investors should like.