The rally in value stocks may have stalled, but Russ discusses why the trend still has further to go.

For much of the post-crisis period investors consistently craved growth stocks. They did so for the same reason they favored stocks with a healthy dividend: Both income and growth were scarce commodities for much of the past eight years. However, with yields rising and economic growth at least stabilizing, this began to change in the second half of 2016 when classic dividend plays stumbled while value started to come back into vogue. However, these trends stalled in January, raising the question of whether the recent preference for value has further to go. My view is that it does, primarily because value still appears cheap relative to growth.

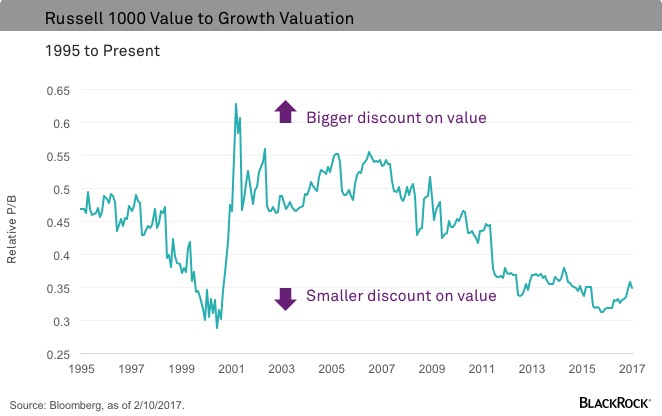

The notion of the “value of value” seems a bit redundant, but it is important when assessing style preferences. While value stocks, by definition, will trade at a lower valuation than growth stocks, the valuation spread moves over time. Based on the price-to-book (P/B) metric, since 1995, value stocks, as defined by the Russell 1000 Value Index, have typically traded at around a 55% discount to growth stocks.

During the tech bubble growth stocks became more expensive, pushing the value discount to more than 70% at the market peak in 2000. Conversely, prior to the bursting of the housing bubble, it was value that looked expensive. The rally in financial shares, which typically command a higher weight in value indexes, drove the value discount down to around 45% in 2006. The chart below illustrates this, showing the ratio of the value P/B to growth P/B. A relative ratio of 0.55, for example, translates into a value discount of 45%.

Do you prefer growth or value? Join in >

As financials started to come under pressure and the extent of the housing bubble became clear, investors started to demonstrate a strong preference for companies that could grow their earnings regardless of the economic environment. This preference for growth manifested in the outperformance of both stable growers, like defensive consumer staple companies, as well as technology firms benefiting from secular trends. As a result, value has gone from a 45% discount to growth in late 2006 to a 65% discount today.

While value was even cheaper in early 2016, today’s discount still places the growth/value spread more than one standard deviation below the long-term average. In other words, value stocks still look attractive relative to growth.

To be sure relative cheapness is not a guarantee of relative outperformance, but to the extent that value stocks are cheap and the economic outlook is improving, value has a reasonable chance of continuing its run.

For investors, the challenge is that the latter condition, i.e. better growth, is somewhat dependent on whether Washington can conjure up a reasonable and timely stimulus package, including tax reform. A stumble in such efforts is likely to revive old concerns over secular stagnation and push investors back toward old habits, namely a preference for yield and stable growth. However, even a modest package that raises growth expectations stands to benefit the cheapest segments of the market.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.

© BlackRock

Read more commentaries by BlackRock