“President Trump may be able to temporarily hold off the sweep of automation and globalization

by cajoling companies to keep jobs at home, but bolstering inefficient and uncompetitive

enterprises is likely to only temporarily stave off market forces,” he continued…“While they might be popular, the reason the U.S. long ago abandoned protectionist trade policies

is because they not only don’t work, they actually leave society worse off.”– Seth Klarman, The Baupost Group

Andrew Ross Sorkin of CNBC and The New York Times wrote an article this week entitled, “A Quiet Giant of Investing Weighs In on Trump.” It’s about the recent investor letter penned by one of the all-time great investors, Seth Klarman. Many hedge fund managers write privately to their clients yet these letters often find a way on to the internet.

The article begins as follows:

He is the most successful and influential investor you have probably never heard of. His writings are so coveted and followed by Wall Street that a used copy of a book he wrote several decades ago about investing starts at $795 on Amazon and a new copy sells for as much as $3,500.

Perhaps that’s why a private letter he wrote to his investors a little over two weeks ago about investing during the age of President Trump — and offering his thoughts on the current state of the hedge fund industry — has quietly become the most sought-after reading material on Wall Street.

Several quotes from the Klarman letter:

- Exuberant investors have focused on the potential benefits of stimulative tax cuts, while mostly ignoring the risks from America-first protectionism and the erection of new trade barriers.

- The Trump tax cuts could drive government deficits considerably higher.

- The large 2001 Bush tax cuts, for example, fueled income inequality while triggering huge federal budget deficits.

- Rising interest rates alone would balloon the federal deficit, because interest payments on the massive outstanding government debt would skyrocket from today’s artificially low levels.

Sorkin concludes, “Much of Mr. Klarman’s anxiety seems to emanate from Mr. Trump’s leadership style. He described it this way: ‘The erratic tendencies and overconfidence in his own wisdom and judgment that Donald Trump has demonstrated to date are inconsistent with strong leadership and sound decision-making.’”

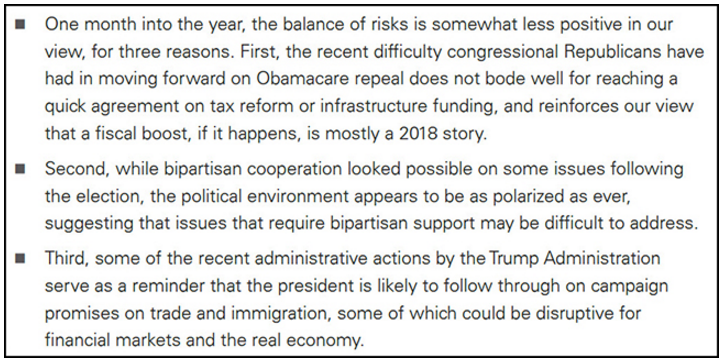

Also notable this week, to me, was Goldman Sachs reversing its earlier optimistic economic outlook tied to our new government. The firm cites three reasons:

- Obamacare struggle is a sign of things to come

- Polarization of political parties is getting worse

- There’s a real possibility of market disruption

Goldman concluded, “Some of the recent administrative actions by the Trump Administration serve as a reminder that the President is likely to follow through on campaign promises on trade and immigration, some of which could be disruptive for financial markets and the real economy.” Link to the Bloomberg post provided below.

Is this The Art of the Deal? Is Trump positioning for the greatest negotiation of all time? The stakes are high. With regard to protectionist trade policies, “… they not only don’t work, they actually leave society worse off.” Such policies are inflationary, lead to recession and raise the risk of war.

If you are feeling a bit unsettled, like me, perhaps our feelings are best captured in a piece called, “Nothing Feels Stable,” by Raymond James’ Jeffrey Saut.

OK Steve, pick your head up. Here are some positives: The equity markets are making new highs. My favorite recession indicators (economic data models) show low risk of U.S. recession and global recession. The equity market trend remains bullish (as you’ll find posted each week in Trade Signals) and our equity trend and momentum models remain risk on. Add in this from my friends at Ned Davis Research:

“Despite the numerous risks facing many of the world’s economies, including several elections in Europe, a possible rise of protectionism in the U.S. and a potential debt crisis in China, the outlook among the world’s largest economies remains favorable and suggests upside in the coming months.”

(Ned Davis Research, “Global Indicators So Far Point to Little Risk in the Outlook,” February 9, 2017.)

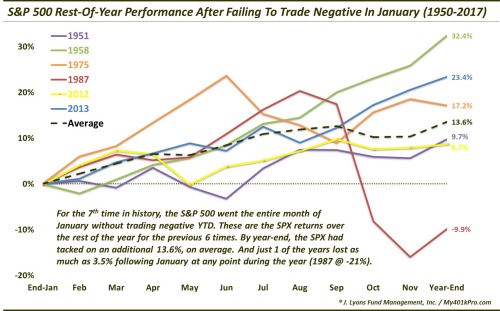

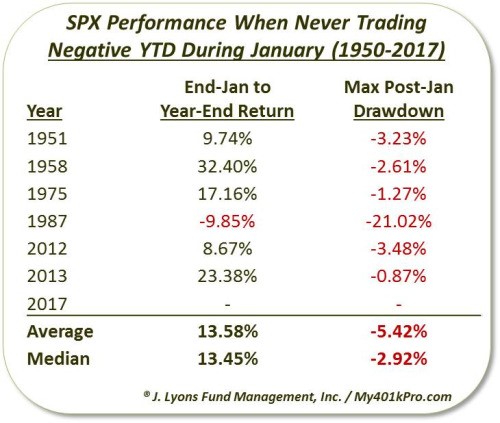

And this piece of potential good news from an old friend, Dana Lyons:

Here is the data:

We are approaching the point in the game of musical chairs when one by one the chairs are removed from the circle. When the music stops, fewer chairs remain. I’m concerned that valuations are at the second highest level in history. I’m concerned that the Fed has raised rates twice with a few more likely on the way (historically bad for stocks). I’m concerned that it’s been eight years since the last recession. I’m concerned that we are in the second longest cyclical bull rally. I’m concerned that we are at the end of a long-term secular debt cycle and the beginning of a deleveraging cycle (barely begun).

We are at the end of a long-term debt cycle. They happen maybe once in a generation and we are working towards resolve. The global debt mess will be addressed one way or another.

“The exodus of investors from flexible investment disciplines to passive investing and indexing, at valuations that are among the most obscene in history, is a symptom of a performance-chasing mentality dressed in the clothing of prudence.” – John Hussman

So let’s step forward and pray for a beautiful deleveraging, knowing the high probability of an ugly deleveraging.

This week you’ll find a great chart on debt showing deleveraging has just barely begun, an explanation with historical data on the 200-day moving average rule and a link to John Hussman’s latest missive. I would not dismiss what he has to say.

I really hope that I leave you with a sense of optimism. Protectionism, inflation, recession, aged, overbought, over-believed… Let’s not get emotional. Just see it as data and follow the trend. Set your game plan to paper and prepare your clients. The next great dislocation, when it presents, will create another outstanding buying opportunity. Let’s not get run over on the way to that opportunity.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Goldman Sachs Starting to Worry About Trump

- 200-Day Moving Average Rule

- A Look at U.S. Domestic Debt

- Hussman – Portfolio Strategy and The Iron Laws

- Trade Signals – Majority of Equity Indicators Bullish, Trend Positive, Sentiment Remains Excessively Optimistic

Goldman Sachs Economists are Starting to Worry about President Trump

From Bloomberg:

A rethink, if not an outright reversal?

Just a few weeks ago, Wall Street analysts were busy boosting their economic forecasts on the expectation that President Trump would implement sweeping corporate-tax reform, a rollback of regulations and new fiscal stimulus. Two weeks into his term and the President has been focused primarily on immigration and trade, causing a reevaluation among analysts at some banks that hark back to pre-election concerns about Trump’s uncertain effect on markets and U.S. economic growth.

Goldman Sachs Group Inc. economists led by Alec Phillips wrote a note published late last week. Phillips cites three key reasons for the more cautious tone:

Sources: Bloomberg and 361Capital.

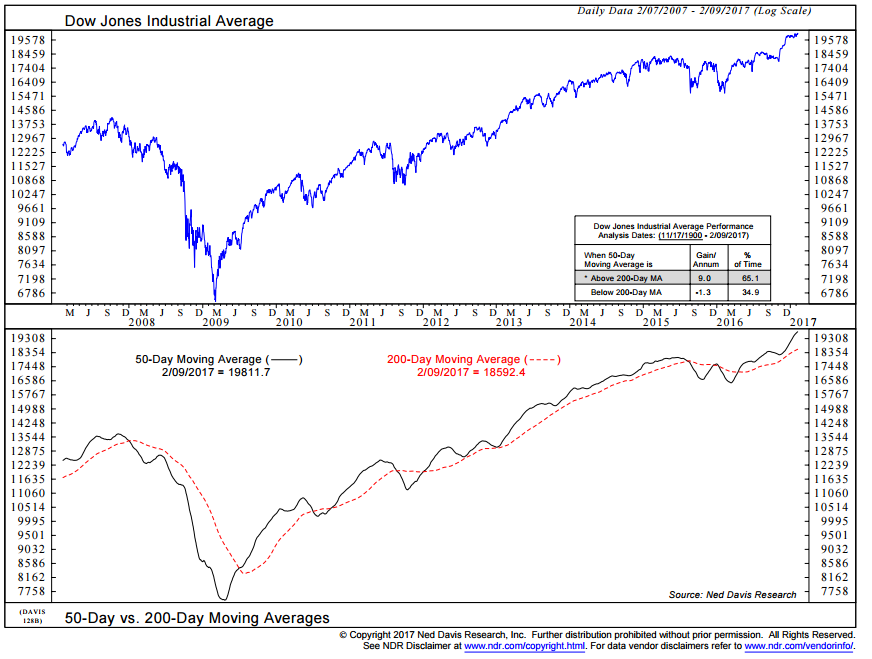

200-Day Moving Average Rule

Source: Ned Davis Research

In this chart, focus in on the red line (bottom section of chart):

- Top section is the rule – You exit when the Dow Jones Index (total return) or blue line drops below the red dotted 200-day MA line.

- You trade back in when it rises above.

- Red line bottom section is the 200-day MA cross strategy gain of $100 dollars over time vs. the gain of the same $100 buying and holding DJIA.

“My metric for everything I look at is the 200-day moving average of closing prices. I’ve seen too many things go to zero, stocks and commodities. The whole trick in investing is: “How do I keep from losing everything?” If you use the 200-day moving average rule, then you get out. You play defense, and you get out.”

– Paul Tudor Jones (source)

The idea here is to simply point out that there are many ways to risk protect your hard- earned capital. Find a process that works best for you.

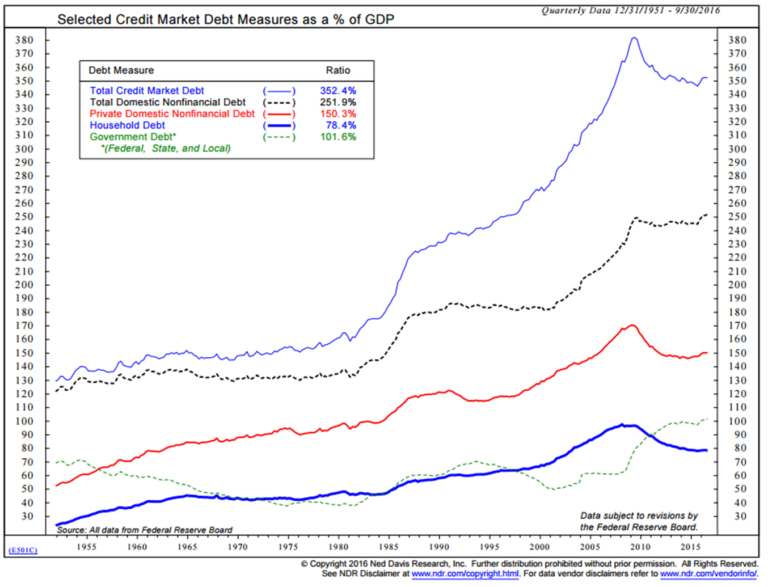

A Look at U.S. Domestic Debt

Source: Ned Davis Research

Total Credit Market Debt in the U.S. is 352.4% of GDP. Post the peak in 2008 at north of 380%, this chart shows deleveraging has begun.

Recall the Reinhart / Rogoff study that debt greater than 90% of GDP slows growth. We’ve certainly witnessed slow growth in the 2% range for the last 16 years. Debt’s a drag on growth.

As you may know by now, I’m a big Ned Davis Research fan. I’ve been a subscriber and happy client since the mid 1990s. They kindly let me share certain charts with you, but I story them in a way to share with you how I’ve been using many of the charts for many years. I love the data and I think NDR is one of the best independent research shops in the business.

If you’d like to learn more about their subscription services, contact Dan Dortona. Please know I don’t get paid a penny from NDR nor a reduction in my research fee. Just a happy client.

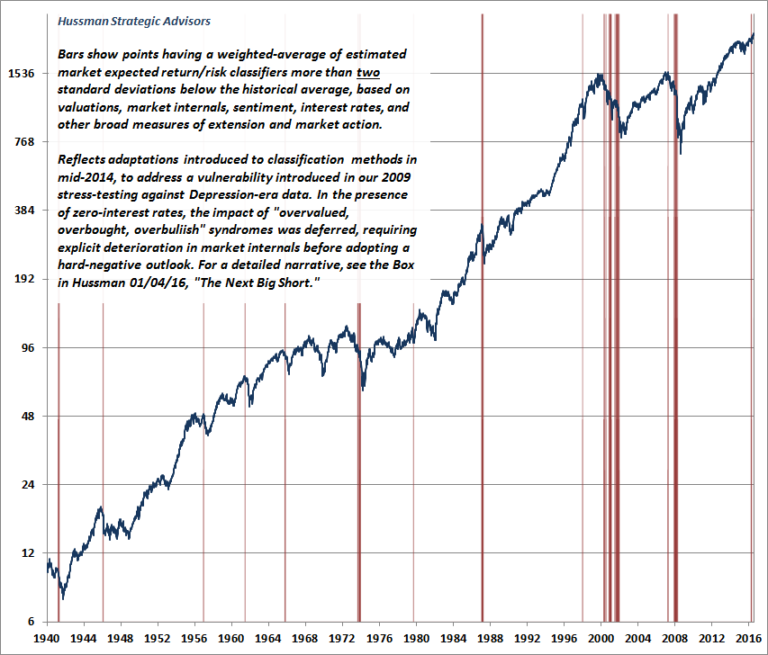

John Hussman – Portfolio Strategy and the Iron Laws

A few weeks ago, we observed the single most extreme syndrome of “overvalued, overbought, overbullish” conditions we identify (see Speculative Extremes and Historically Informed Optimism) at a level on the S&P 500 4% higher than the syndrome we observed in July. The S&P 500 has climbed about 1.5% further since then, and all of the features of this syndrome remain in place.

As I noted in December, except for a set of signals in late-2013 and early-2014 (when market internals remained uniformly favorable as a result of Fed-induced yield-seeking speculation), an overextended syndrome this extreme has only emerged at the market peaks preceding the worst collapses in the past century. Prior to the advance of recent years, the list of these instances was: August 1929, the week of the bull market peak; August 1972, after which the S&P 500 would advance about 7% by year-end, and then drop by half; August 1987, the week of the bull market peak; July 1999, just before an abrupt 12% market correction, with a secondary signal in March 2000, the week of the final market peak; and July 2007, within a few points of the final peak in the S&P 500, with a secondary signal in October 2007, the week of that bull final market peak.

Two weeks ago, we observed a fairly rare set of “crash signatures” that we associate with the risk of market losses in excess of -25%, generally over a period of about 6 months. No single variable drives these signatures. Rather, they capture infrequent combinations of market conditions that may include offensive valuations, dispersion across market internals, credit market weakness, lopsided bullish sentiment, Federal Reserve tightening, or other features which, in combination, have historically preceded steep and compressed plunges in the market. These signatures are designed to identify the most hostile points in a market cycle. The last three times these features were in place to the same extent were: Apr-Oct 2008, Mar-May 2002, and Aug-Sep 1987.

Last week, an additional class of risk signatures, typically active in only a small percentage of historical data, shifted to warning mode. To offer some idea of the risk profile we are estimating here, the chart below reflects a blend of several types of classifiers we’ve developed over the years. These include estimates of the expected market return/risk profile on horizons ranging from 2 weeks to 18 months, as well as signatures we associate with specific “events,” such as air-pockets, panics and crashes. The bars show points where a blended composite of these estimates was at least two standard deviations below average, as it is presently. There’s no assurance that future outcomes will be similar, but most of these instances were rather challenging for investors.

Full link here.

Trade Signals – Majority of Equity Indicators Bullish, Trend Positive, Sentiment Remains Excessively Optimistic

S&P 500 Index — 2,293 (2-8-2017)

Click here for the charts and explanations.

Personal Note

I’m writing you from Snowbird, Utah and thought I’d share two quick stories. It was nearly six years ago and I received a call from my friend, John Mauldin. I had just stepped off the tram (pictured above). It was a perfect fresh powder ski day and my kids were with me. John was going to fly in and join me and my family for my 50th birthday celebration but had to pass. He was invited to have dinner with then House Speaker John Boehner.

My phone rang and I took the call. Skiers often joke that there are “no friends on a powder day” and for good reason. But this was different, remember the post-crisis world that existed in 2011, I was eager to hear what John learned at his dinner.

John shared with Speaker Boehner and several other high ranking Republicans his views on the economic path forward. The room remained quiet to which John leaned forward and said, “Well, boys, what are you going to do?” Boehner leaned forward and said, “I’ll tell you exactly what we are going to do, we are going to print, and print and keep on printing.”

I thanked John for the birthday present and took off down the hill. I thought I really was given a gift. In my wildest dreams I couldn’t have imagined the extent to which we (Fed) and the ECB and the Japanese Central Banks have embraced this plan. We just don’t know how it is going to play out. Global QE has inflated asset prices and enabled zombie companies to stay in business. We’ve brought forward returns from future years to today. I remain concerned.

What I do know is the next recession will hurt portfolios. I know that most of the hurt will be on those that can least afford to lose – pre-retirees and retirees. I know that people behave irrationally (buy when they should be selling and sell when they should be buying) and that this time 75% or so of the investable money is sitting in the self-directed hands of the individuals who don’t have the years it will take to come back from the loss. So, we watch the data, we watch the trends and we step forward with a disciplined game plan. We stay patient and mentally prepared to act.

The other story is a personal one. I lost my wonderful father a handful of years ago. He brought me to Snowbird when I was 18 and I’ve come every year since. Many of those years I spent raising my children on the mountain. We are a family of skiers and it is all thanks to my old man.

I walked off the tram early yesterday morning and smiled as I gave thanks to my dad. Grateful… and what a great day it was.

I’ll be presenting at a meeting in Kansas City on February 23. We are co-hosting a conference in the NY metro area on March 14 and 15. Details next week. I’ll be in Dallas March 28 and 29 for a private advisor gathering.

Have a great weekend. Here’s a hat tip and toast to those in your life who lift you the most.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts via Twitter that I feel may be worth your time. You can follow me @SBlumenthalCMG.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

The CMG Tactical Fixed Income Index, CMG Tactical All Asset Index, CMG Tactical Equity Index and CMG Beta Rotation Index are rules-based indexes that reflect the theoretical performance an investor would have obtained had it invested in the manner shown and do not represent actual returns, as investors cannot invest directly in the Indexes. The CMG Tactical Fixed Income Index, CMG Tactical All Asset Index, CMG Tactical Equity Index and CMG Beta Rotation Index returns represented do not reflect the actual trading of any client account. No representation is being made that any client will or is likely to achieve results similar to those presented herein. Unless noted, performance results are presented net of a 2.50% maximum annual fee deducted from the account balance quarterly, in arrears.

Any financial product based on the CMG Tactical Fixed Income Index, CMG Tactical All Asset Index, CMG Tactical Equity Index and CMG Beta Rotation Index or any index derived therefrom that is offered by CMG Capital Management Group, Inc. is not sponsored, endorsed, sold or promoted by Solactive AG and Solactive AG makes no representation regarding the advisability of investing in the product.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group