Fresh concerns about Greece’s debts have prompted new worries across Europe. But another compromise looks likely—European leaders can ill afford a full-blown Greek crisis amid so much regional political uncertainty.

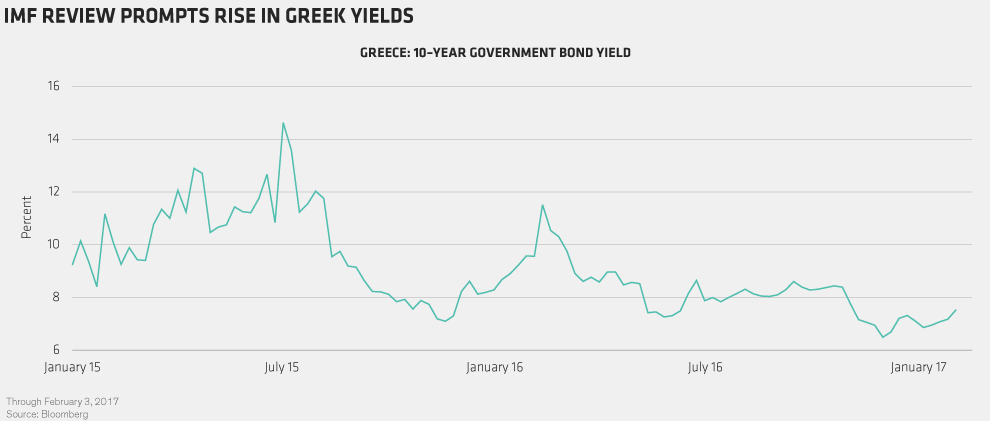

Yields on Greek debt surged this week as the International Monetary Fund (IMF) released a scathing review of the third Greek bailout agreed in the summer of 2015 (Display). In that deal, Greece’s European Union (EU) partners and the IMF realized that there was no way to reconcile their differences on debt sustainability and the associated need for debt relief. Instead, they agreed to “kick the can down the road” (again) in order to avoid Greece exiting the euro.

A FUDGED DEAL

The result is that the IMF still helps monitor the program to satisfy countries like Germany and the Netherlands. Yet it refuses to commit new funding until debt sustainability has been assured, via far deeper debt relief than the EU is willing to consider—particularly during a crucial electoral period.

But this fudge creates a recurring problem. Greek debt sustainability—and, ultimately, its place in the euro—comes into sharper focus every time we approach a program review, which normally precedes the release of fresh funding. That’s exactly what happened in the first review last spring and it’s happening again now during the second review.

ANOTHER COMPROMISE?

Last year, it ended with a compromise. This year, regional leaders know they must prevent things from coming to a head. With Dutch, French and German elections on the horizon, Brexit negotiations about to start and uncertainty from the Trump administration, the last thing EU leaders need is another full-blown Greek crisis.

Reaching a compromise won’t be easy. Greece wants the second review completed as soon as possible. However, the gaps between Greece, the EU and the IMF remain wide. Indeed, there’s still a fundamental disagreement between the EU and the IMF on debt sustainability, the need for debt relief and overall program design.

In the past, Greek bailout reviews have tended to rumble on until there’s a debt redemption and potential bankruptcy to focus the mind. The next crunch won’t come until April—when €1.4 billion of bonds are due to mature—or, more likely, July—when €7.8 billion of bonds are due. So Greek “noise” is likely to persist for a few months.