1. Fourth Quarter GDP Report Was a Big Disappointment

2. The Emerging Markets Face Looming US Dollar Crisis

3. Mr. Trump Says Dollar “Too Strong” – Hurts US Economy

Overview

Over the last eight years, with US interest rates at rock bottom thanks to the Fed, the rest of the world has borrowed a huge amount of dollars – about $4 trillion according to the Bank for International Settlements. During that same time, the US dollar has soared against a basket of foreign currencies.

The majority of this borrowing has been by so-called “emerging nations” that now look to have serious trouble paying back their US dollar-denominated debt, given that the greenback has gone up so much in the last few years. It’s complicated but I’ll break it down for you today.

But before we get to that discussion, let’s take a look at Friday’s initial estimate of 4Q GDP from the government. It received scant attention in the media given the non-stop coverage of President Trump and his flurry of executive actions in his first week in office.

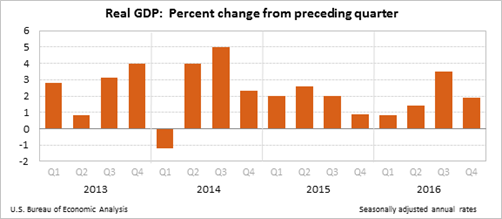

Fourth Quarter GDP Report Was a Big Disappointment

The US economy’s expansion slowed in the 4Q, and annual growth failed to reach 3% for an 11th straight year, reflecting the huge hurdles the Trump administration faces in trying to speed up a nearly eight year-old weak expansion.

The Commerce Department reported Friday that 4Q GDP expanded by a disappointing 1.9% (annual rate) in its first of three estimates. This was below the pre-report consensus of 2.2%, and was well below the 3.5% pace in the 3Q.

If the advance 4Q report of 1.9% holds up, that will mean the US economy expanded at an unimpressive annual rate of only 1.6% for all of 2016, compared to 2.6% in 2015. That was also well below the average annual rate of 2.1% since the Great Recession ended in mid-2009.

In the 4Q, the biggest factor contributing to the slowdown was a widening in the trade deficit. Exports, which had been temporarily bolstered in the 3Q by a surge in sales of soybeans to Latin America, retreated in the 4Q. Meanwhile, imports which are a drag on GDP, surged in the final three months of last year.

In light of the much weaker than expected GDP growth in the 4Q, the question now is whether the much stronger than expected growth of 3.5% in the 3Q was an aberration? The answer is probably so. It will be interesting to see if the Commerce Department revises the 3Q GDP estimate lower in subsequent reports.

Consumer spending, which accounts for 70% of economic growth, slowed to 2.5% in the 4Q from a 3% gain in the 3Q. Trade cut 1.7% from GDP growth in the 4Q after adding 0.9% to growth in the 3Q. A higher trade deficit subtracts from economic growth because it means more production is being supplied from abroad.

On the bright side, business investment spending accelerated in the 4Q, rising at a 2.4% rate, the best showing in more than a year. That’s a hopeful sign that the prolonged slowdown in investment spending, reflecting in part big cuts by energy companies, is coming to an end.

President Trump has set a goal of doubling GDP growth to at least 4% through an ambitious stimulus program featuring tax cuts, deregulation and higher infrastructure spending. Yet private economists believe sustained annual growth rates of 4% will be a tough goal to achieve for a variety of reasons.

It will be interesting to see how economists react to Friday’s weaker than expected GDP report. Many had increased their forecasts in light of the strong 3Q estimate. In fact, just last week – before last Friday’s weak GDP report – economists at the International Monetary Fund (IMF) boosted their outlook for US GDP to 2.3% this year and 2.5% in 2018.

IMF economists said the upward revisions were due to strong growth in the 3Q and the expectations that Trump’s economic program of tax cuts, regulatory relief and higher infrastructure spending had boosted growth prospects. It remains to be seen how those same economists and others feel now in light of Friday’s disappointing 4Q GDP report.

The Emerging Markets Face Looming US Dollar Crisis

The US dollar has risen significantly in the last few years. Most currency analysts expect the dollar to continue to rise, especially if the Fed continues to hike short-term interest rates. Generally speaking a strong dollar means weak commodities (like oil), and weak commodity prices tend to be bad for emerging markets.

A strong dollar and higher interest rates could cause money to exit emerging markets and flow into US assets, further exacerbating the problem for emerging countries. Add to this the fact that many emerging nations also hold significant dollar-denominated currency reserves, which can be a double whammy when those stronger dollar reserves are eventually converted to their home currency.

Further complicating the currency conundrum for emerging markets is the uncertainty about the Trump administration and the policies it will pursue. For example, will Trump’s team of economic nationalists, who want to impose import tariffs and increase infrastructure spending, get their way?

Or will it be his gang of economic conservatives, who want to cut income taxes for individuals and corporations and deregulate significantly? Actually, it could well be some of both. It’s clear Trump is going to try to do what he said he would do on the campaign trail, even if some of those things aren’t entirely consistent. But I digress.

For purposes of this discussion, let’s focus on the fact that the rest of the world has borrowed a lot of dollars the last eight years – about $4 trillion according to the Bank for International Settlements (BIS). The BIS says that since 2008, dollar loans to non-bank borrowers outside the United States have gone from $6 trillion to almost $10 trillion, with emerging markets making up the majority of that increase. Their dollar debts, according to the BIS, have actually more than doubled during this time from $1.7 trillion to $4.5 trillion.

That makes these emerging nations particularly vulnerable to the uncertainties in the currency markets. Think about it like this. If you borrow in dollars but earn most of your money in something other than the dollar, then your debts will get harder to pay back anytime the dollar increases in value – which it really has in the last two and a half years.

Indeed, on a trade-weighted basis, the dollar has shot up over 25% against a broad basket of currencies just since the middle of 2014, as you can see in the chart above.

As noted above, most analysts expect the dollar will continue to appreciate under President Trump. Why? For one, the Federal Reserve’s latest minutes show that it thinks Trump’s tax cuts, if they happen, will force it to raise rates faster than it thought it would just a few months ago.

Otherwise, the Fed worries, the economy could start to overheat and inflation might rise significantly. If the Fed raises rates more than previously expected, that means our interest rates will be even higher compared to the rest of the world’s than they already are. That, in turn, should push the dollar up even higher than it already is.

At some point emerging market borrowers are going to have trouble paying back their US dollar debts if the greenback keeps going up – especially if Trump puts in import tariffs that make it harder for them to earn dollars in the first place.

Take Brazil for example, which is currently mired in its worst recession since the 1930s and has borrowed the second-most dollars of any emerging nation. If the dollar continues to strengthen, Brazil might have to choose between an even worse economic crisis or a financial crisis. That is, it could keep propping up its currency at the cost of growth, or it could let it fall against the dollar and see its US dollar borrowers default.

Even China might not be immune. It has the ugly combination of the highest level of dollar debt in the developing world and a currency that has been sliding against the greenback for over a year now. In the worst case, it might have to bail out a bunch of borrowers who can't handle the combination of a stronger dollar, a slightly weaker economy and possible Trump tariffs that could take away some of their export markets.

It might not be that different from the Latin American debt crisis in the early 1980s. Then, like now, poorer countries had gone on a dollar borrowing binge. And then, like now, a surging dollar made those debts harder to pay off – until they couldn’t be – and then some defaulted. That not only sent those countries into a lost decade, but also almost brought down the American banks that had lent them so much money.

President Trump Says Dollar is “Too Strong” – Hurts US Economy

It is, of course, impossible to predict when a currency crisis might erupt in the emerging markets. It is also not a given that the US dollar will continue to rise. As we all know, the Fed has not made good on its intentions to raise interest rates several times in each of the past two years, which would have made the dollar even stronger.

Add to that the recent comments by then President-elect Trump. On January 18, Mr. Trump told the Wall Street Journal that “Our currency is too strong, and it is killing us.” Nobody, it seems, wants a stronger currency. I should add that American presidents in the Modern Era have had only limited success in “talking” the US dollar up or down (as it should be).

Trump’s comments stand as a reminder of the sensitivity of the dollar to the US economy. A stronger dollar hurts American exporters trying to compete in overseas markets with similar product makers in countries with lower cost structures.

In the past 12-18 months, the Fed has alerted investors to the adverse impact of a stronger dollar on exports and economic growth. Yet they’ve tended to play down any negative spill-over effects from the Fed’s own monetary policy and what a strong dollar has done to emerging markets.

As you can see in the graph above, the dollar has been weakening since the first of the year. At the end of last year, the dollar was at a 14-year high and overdue for a downward correction which it’s now in the midst of.

The current downward correction in the dollar has reached levels where it should find support and rebound higher, if the uptrend is intact. We will see what happens in the next few weeks.

All the best,

Gary D. Halbert

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

|

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management