“I can’t change the direction of the wind, but I can adjust my sails to always reach my destination.”

Jimmy Dean, American Country Music Singer

Today Donald J. Trump was sworn in as the 45th President of the United States. President Trump steps to center stage. Bring us jobs, bring us tax reform and bring us a grand fiscal infrastructure spend. That would be positive.

Trump’s speech today hit hard on the subject of protectionism. “We are going to follow two simple rules, buy American and hire American.” He was also direct in saying, “I’m giving you back your government.” It’s broken. Let’s hope that happens.

Tax cuts and the repatriation of $2 trillion sitting on the offshore books of U.S. corporations are in the economic plus column. Thumbs up too on deregulation and fiscal infrastructure spend. Trade wars and protectionism go in the negative column. As former Dallas Fed President Richard Fisher advised today on CNBC, “Be very careful on these issues of protectionism. It could lead to a global depression.”

There are reasons for hope and reasons for concern. There will be disruption and that I believe may be a good thing. We’ll soon find out exactly what we are going to get.

Today, let’s take a look at the investment landscape through the lens of risk and reward. To that end, you’ll find two great charts immediately below.

Return and Risk. Following are two charts that paint the picture.

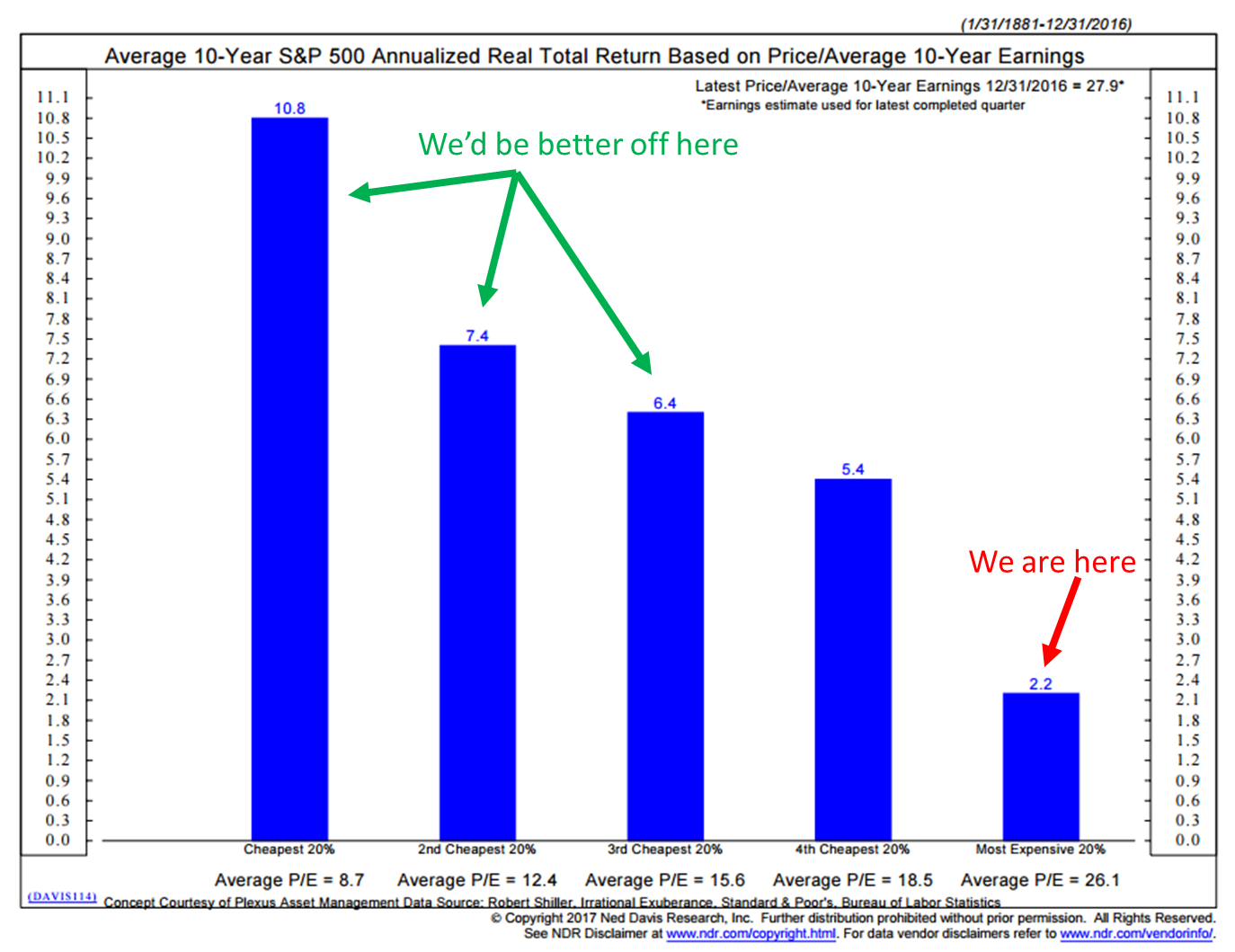

1. Return Potential – P/E is calculated by smoothing 10-year earnings. Monthly P/Es (1881 to 12-31-16) are then sorted into five quintiles, lowest P/E to highest P/E (as you read the chart left to right). A high P/E means that the market is expensively priced. The blue bars then show the subsequent 10-year average annualized real total returns that were achieved sorted by quintile. Note the number at the top of each blue bar. That’s the average subsequent return in each valuation quintile. See the red “We are here” projecting 2.2% annualized real returns over the next 10 years. Past history is no guarantee to what the next 10 years will look like, but I wouldn’t stray too far from that bet. I think it is best to play defense and be in a position to play offense when we get to the “We’d be better off here.”

Source: Ned Davis Research

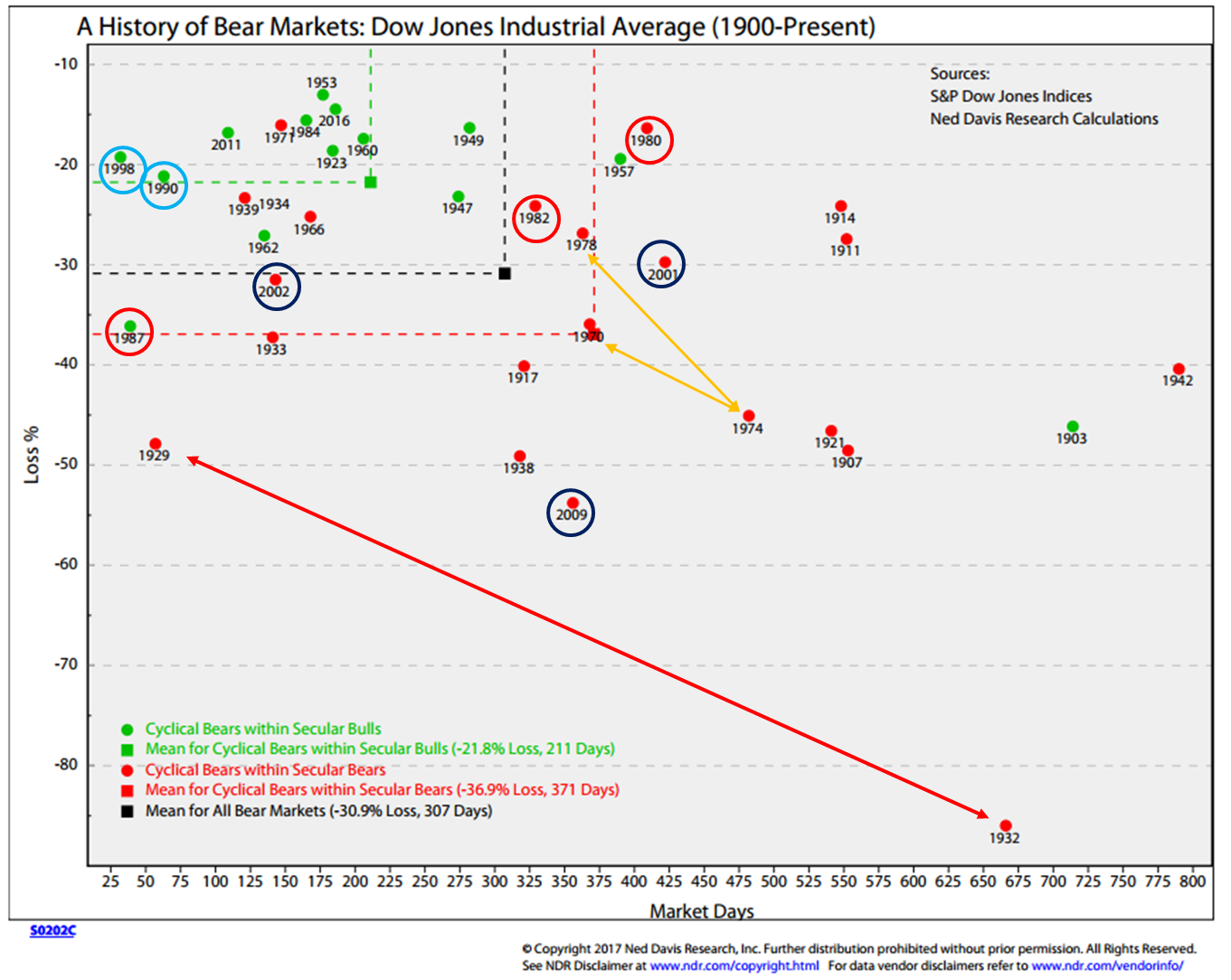

2. Risk – Show this chart to your client. It shows the corrections and the length of days the corrections lasted. Circled in blue are the corrections by percent that occurred in the decade between 2000 and 2010 (left-hand side “Loss %”). For example, the 2001 correction was -30% and lasted 435 days. The 2002 correction took the market down another -32% and lasted about 140 days. Collectively, that compounded to about -50%. The 2009 correction was -55% and lasted about 355 days.

Also, take a look at the corrections in the 1980s (red circles) and the 1990s (light blue circles).

Source: Ned Davis Research

Note that the mean correction for a cyclical bear market that exists within a larger secular bull market cycle is a -21.8% loss that took 211 days. Note too that the mean correction for a cyclical bear within a secular bear market cycle is a loss of -36.9% that took 371 days. For what it’s worth, I believe we sit in a secular bull market cycle.

As you may know by now, I’m a big Ned Davis Research fan. I’ve been a subscriber and happy client since the mid 1990’s. They kindly let me share certain charts with you, but I story them in a way to share with you how I’ve been using many of the charts for many years. I love the data and I think NDR is one of the best independent research shops in the business.

If you’d like to learn more about their subscription services, contact Dan Dortona. Please know I don’t get paid a penny from NDR nor a reduction in my research fee. Just a happy client.

My friend, John Mauldin, wrote many years ago that he expects three recessions before the deck is reset. We’ve had the first two. My point is to stay vigilant as the largest declines tend to occur from points of extreme overvaluation, which is where we are today. You can find a detailed summary of various assessments of most recent valuation measurements here.

My other point is that a better opportunity awaits. Stay patient and be prepared to act when we get to the “We’d be better off here” valuation area (quintiles 1, 2 and 3 in chart 1 above).

Active money management is not dead. The herding into traditional buy-and-hold equity market investing today is in full bloom. I believe it will prove no different than the money that raced into tech in the late 1990s or housing (and equities) in 2007/08.

Sometime over the next several years, we’ll have a recession. They happen. They’re normal. They’re healthy. Recessions have occurred on average about once every five years or so since World War II.

I will continue to share my favorite recession probability charts with you in this piece and in Trade Signals from time to time -especially when the risk is rising. As I shared with you in recession charts last week, there is currently no sign of recession. Data dependent, as they say.

Grab a coffee and click through below. You’ll find a link to a Bloomberg video interview that includes Ray Dalio, Christine Lagarde and Larry Summers.

Dalio offered, “Populism scares me. I want to be loud and clear — populism scares me. It is the extremes.” The video interview is about 50 minutes long. It is worth the time. Amen, brother Ray. Be prepared to adjust your sails to reach your destination.

Lastly, if you are going to attend the Inside ETFs Conference in Florida, please tap me on the shoulder and say hello.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Ray Dalio on Populism — The world today looks very much the way it did in the 1930s and Ray Dalio doesn’t like it one bit

- A Look at Volatility (For Quant Geeks Like Me)

- Trade Signals – Flat Tape Related to Extreme Optimism (S/T Bearish for Equities), Zweig Remains in Sell, Equity Trend Bullish (published 01-18-2017)

Ray Dalio on Populism — The world today looks very much the way it did in the 1930s and Ray Dalio doesn’t like it one bit

International Monetary Fund Managing Director Christine Lagarde, Italian Finance Minister Pier Carlo Padoan and Founder, Chairman and Co-CIO of Bridgewater Associates, Ray Dalio, discuss what’s needed to restore growth in the middle class and confidence in the future.

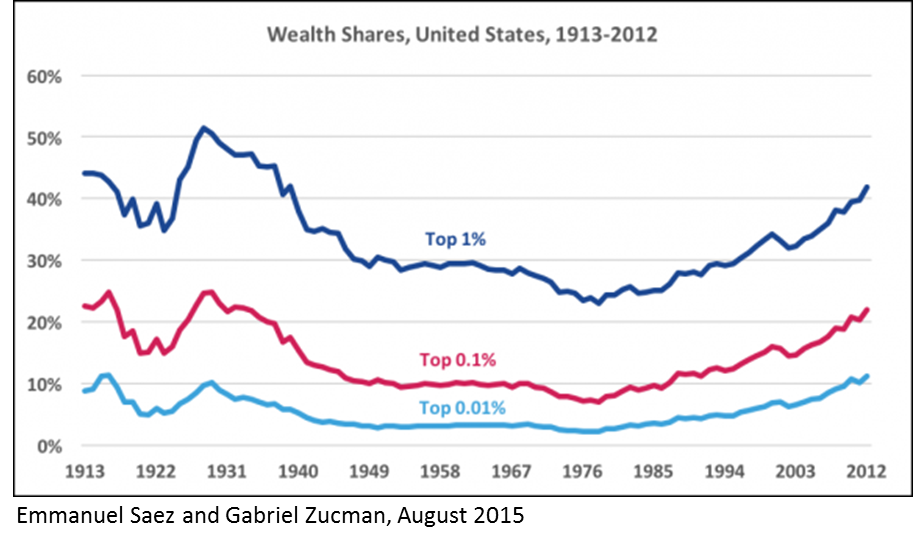

Jump forward to the eight minute mark for Ray’s beginning comments. He likens today to the 1930s. Concerning is the wealth gap that is similar today to what it was in the 30s.

There’s one other similarity to put on your radar. The 1930s was the last time we reached the end of a long-term debt cycle. We don’t get them often. I believe it is the greatest issue we face today. How we navigate out of it remains to be seen.

Recall the bear market data chart at the top of this week’s piece. There is a red arrow that shows the two big declines in the 30s. I’m not saying that’s going to happen. Just pointing out the similarities with an eye toward risk.

A Look at Volatility (For Quant Geeks Like Me)

Last year, nearly 100% of trading returns were made between November 8 and December 15. The dollar gained nearly 13% versus the yen, the 10-year Treasury yield moved 80 basis points higher, the 10-year Treasury dropped approximately 7%, 30-year Treasury bonds dropped nearly 14%, the Russell 2000 rallied 18% and equities jumped higher most everywhere.

There has been little progress since. The market turns and waits. Tax cuts? Tax amnesty on the $2 trillion in offshore corporate cash? Fiscal infrastructure spend, Obamacare repeal? Walls and trade wars? Government deregulation. It begins today or well, maybe Monday… The big boss man says he wants to take the weekend off.

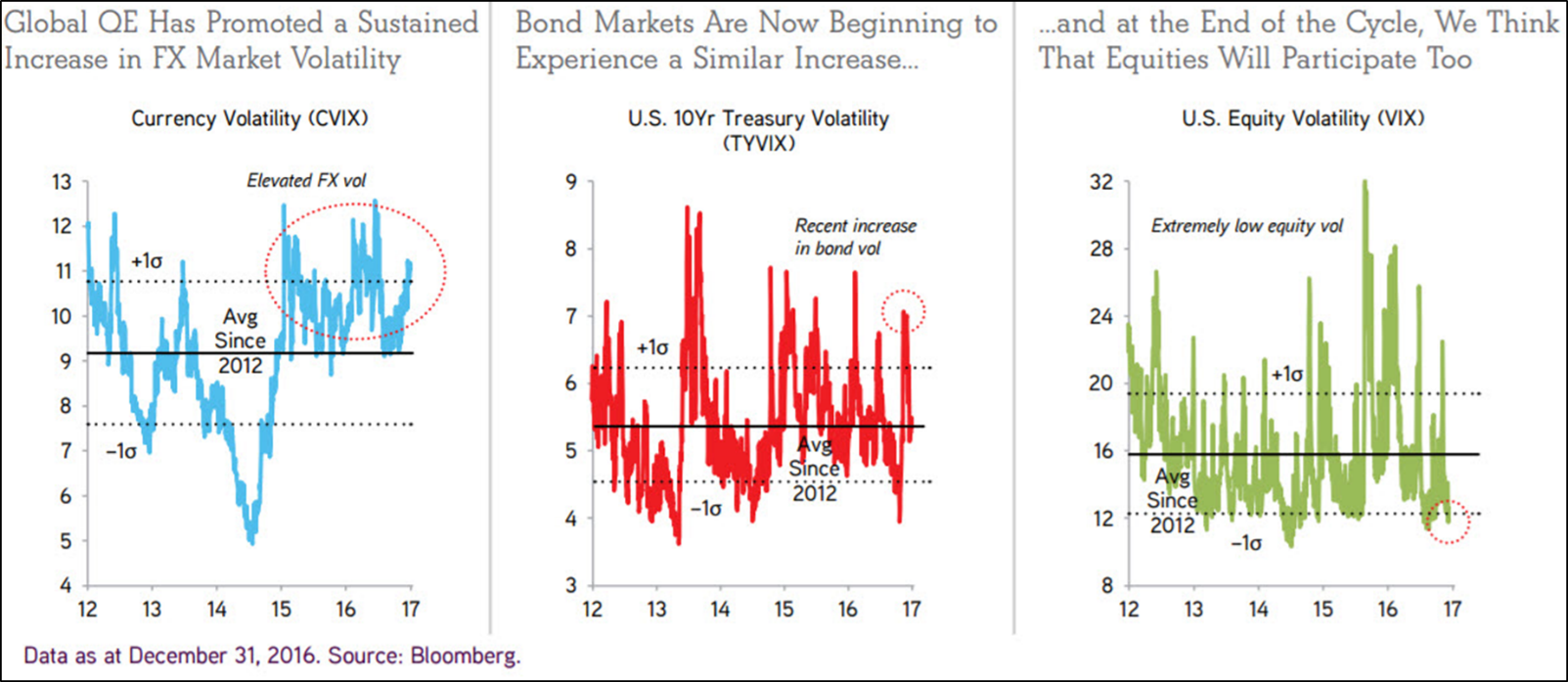

One last and final chart pretty much sums up recent market behavior. It looks at the high volatility in currencies and in bonds and it looks at the low volatility in stocks. Interesting…

Here is how you read the chart:

- Volatility refers to the amount of uncertainty or risk about the size of changes in a security’s value. A higher volatility means that a security’s value can potentially be spread out over a larger range of values. This means that the price of the security can change dramatically over a short time period in either direction. A lower volatility means that a security’s value does not fluctuate dramatically, but changes in value at a steady pace over a period of time. (Source: Investopedia)

- The dotted horizontal lines show 1 standard deviation moves. They are plotted both above and below the dark horizontal lines. Low volatility is the dark line.

- Periods of extremely low vol are rare (points below -1σ) and are often followed by periods of high vol (points above 1σ)

Source: KKRinsights (with a hat tip to 361 Capital)

Trade Signals – Flat Tape Related to Extreme Optimism (S/T Bearish for Equities), Zweig Remains in Sell, Equity Trend Bullish

S&P 500 Index — 2,269 (1-18-2017)

You’ll find “Trade Signals” to be organized into three sections:

- Trade Signals – Dashboard

- Executive Summary (What I am seeing this week)

- Detailed review of the Trade Signals with charts (how it works)

I hope you find the information helpful in your work. For informational purposes only… Not a recommendation to buy or sell any security. The weight of equity trend evidence remains bullish. The trend in interest rate trend, as measured by the Zweig Bond Model, remains bearish for high quality bonds. High yield bonds and gold remain in short-term trend buy signals. The CMG Tactical All Asset Index remains largely invested in equities (risk on). Keep a close eye on Don’t Fight the Tape or the Fed chart below. Especially the Fed.

Here is a summary:

Trade Signals — Dashboard

Equity Trade Signals (Green is Bullish, Orange is Neutral and Red is Bearish):

- CMG Ned Davis Research (NDR) Large Cap Momentum Index-Active Trend: Buy Signal – Bullish for Equities

- Long-term Trend (13/34-Week EMA) on the S&P 500 Index: Buy Signal – Bullish Cyclical Trend for Equities

- Volume Demand (buyers) vs. Volume Supply (sellers): Buy Signal – S/T Bullish for Equities

- NDR Big Mo: See note below (active signal: Buy Signal on March 4, 2016 at 1999.99)

- Don’t Fight the Tape or the Fed: Indicator Reading = -1 (Neutral for Equities)

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Extreme Optimism (S/T Bearish for Equities)

- Daily Trading Sentiment Composite: Extreme Optimism (S/T Bearish for Equities)

Fixed Income Trade Signals:

- Zweig Bond Model: Sell Signal

- CMG Managed High Yield Bond Program: Buy Signal

- CMG Tactical Fixed Income Index: JNK & BIL (HY Bonds and Treasury Bills)

Economic Indicators:

- Global Recession Watch Indicator – Low Global Recession Risk

- Recession Watch Indicator – Low U.S. Recession Risk

- Inflation Watch – High Inflation Risk. The focus has shifted from deflation to inflation.

Gold:

- 13-week vs. 34-week exponential moving average: Sell Signal

- Daily Gold Diffusion Model: Buy Signal

- Daily Gold Model: Buy Signal

- Gold Technical Composite Model: Buy Signal

Click here for the most recent Trade Signals blog. You’ll also find the current CMG Opportunistic All Asset allocation pie chart. Mostly long equities.

Personal Note

See Opportunity and Create Great Things. Maybe it is Trump’s “Think big and dream even bigger” quote today that got me thinking. Like him or not, I really do believe there is some wisdom in that advice. I know my kids read this weekly piece from time to time so I thought I’d share with them some advice from Dad.

Thought – word – and action:

Be mindful of the words that you speak. They set a pattern for the reality of who you are and what you are likely to create. Envision a grand machine inside of you listening to your every spoken word. Imagine that machine will deliver what you are asking for. Think and be patient as you speak to yourself and others. What you say matters. Speak with great integrity. Be compassionate with yourself and with others.

When you put your thoughts to word, your thoughts become clearer. Think about and put what you feel is most important to you to paper. Who you wish to be, what you wish to create. Be clear, be crystal clear. Then read what you wrote and speak out loud what you wish for yourself. Let your body hear your words. See yourself healthy, see yourself happy and see unending abundance in your life. Of course, if that is what you wish most.

Then do the wind sprints. Your thoughts are powerful, your word sets to motion the goals and your action gets it done. 10,000 hours, consistency, thought-word-action. Think big, dream big… trust the process. Say and do great things. See yourself celebrating in your outcome.

Perhaps our great journey together is to create harmony here on earth. Envision peace. Stay balanced in the face of drama. Create great things for you. Be mindful that you’ll lift others and while you’re at it, send your light to those who might need it most. It sure makes the journey exciting and I can’t imagine a better way to live.

Hope they read this one with a smile on their faces. You know how hard it can be to share your advice with your teenager.

The Inside ETFs Conference in Hollywood is up next. I’ll be in sunny and warm southeast Florida January 22-25. I present on Monday, January 23, at 2:00 pm. Here’s the agenda. Let me know if you’ll be attending. Would love to grab a coffee with you.

I’ll be taking notes with plans to share what I believe are the most important insights with you next week. My daughter, Brianna, is attending the conference with teammates from the company she works for.

I know I often write about high valuations and low probable 10-year returns and I believe it is important for clients to know how highly predictive those historical forecasts have turned out to be; however, there are ways to improve on that low 2.2% annualized real return outlook and her firm and other ETF providers are a good place to look. I’m looking forward to learning more at this year’s Inside ETFs Conference.

I head back to Dallas on February 1 for the S&P Index Conference. If you are in the Dallas area, the agenda for the S&P Conference is here. The Salt Lake City area follows February 8-10 and I’m speaking at an advisor event in Kansas City on February 23.

The weather app is showing sunny and 82 in Miami. I’m packing the golf clubs. Business really does get done on the golf course… and the ski slopes. Lucky man…

Susan’s birthday is today so I better get moving. A big dinner out is planned (sushi) and gifts need to be wrapped. The boys and I so love when we all slow down and come together.

Here is a toast to you and your family. May we all create great things!

Have a wonderful weekend!

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts via Twitter that I feel may be worth your time. You can follow me @SBlumenthalCMG.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

The CMG Tactical Fixed Income Index and CMG Tactical All Asset Index are rules-based indexes that reflect the theoretical performance an investor would have obtained had it invested in the manner shown and do not represent actual returns, as investors cannot invest directly in the Indexes. The CMG Tactical Fixed Income Index and CMG Tactical All Asset Index returns represented do not reflect the actual trading of any client account. No representation is being made that any client will or is likely to achieve results similar to those presented herein. The CMG Tactical Fixed Income Index performance results are presented net of a 2.50% maximum annual fee deducted from the account balance quarterly, in arrears.

Any financial product based on the CMG Tactical Fixed Income Index, CMG Tactical All Asset Index or any index derived therefrom that is offered by CMG Capital Management Group, Inc. is not sponsored, endorsed, sold or promoted by Solactive AG and Solactive AG makes no representation regarding the advisability of investing in the product.

Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group