“We are not enemies, but friends. We must not be enemies. Though passion may have strained it must not break our bonds of affection. The mystic chords of memory, stretching from every battlefield and patriot grave to every living heart and hearthstone all over this broad land will yet swell the chorus of the Union, when again touched, as surely they will be, by the better angels of our nature.”

- Abraham Lincoln, 1809-1865 16th President of the United States

There was a lot of drama behind the scenes of the S&P 500 Index’s solid 12% return in 2016. The year began with a sharp 14% market drop into mid-February, on worries of a China crisis and a U.S. recession, then everything reversed in a great “pain trade” whereby 2015’s losers mostly become 2016’s winners. The surprise election victories by President Elect Trump and congressional Republican’s kicked these trends into overdrive with a year-end stock market flurry.

We mostly spared our readers political commentary during the exhausting and demoralizing 2016 race, but we can refrain no longer given the incredible gyrations in financial markets since the election. As a Trump victory appeared increasingly likely, stock futures were down some three percent in the middle of election night (a massive move)... but the collective market quickly changed its perception of the implications of a GOP victory. Stock market futures ended about flat by the time the market opened and the stock market finished its first full day of trading strongly up (a massive four percent reversal).

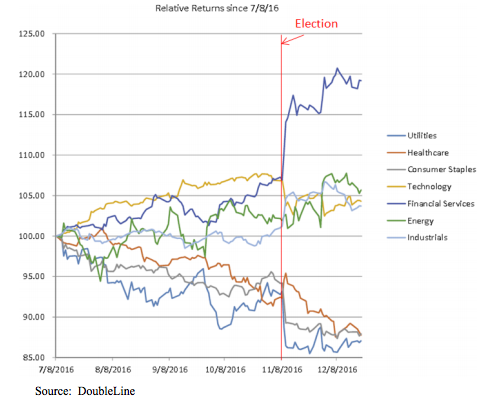

However, movement in the overall stock market doesn’t even begin to match the drastic movements in other financial markets and the “under the hood” divergence of the individual stocks that make up the broader market. Inflation expectations and interest rates both soared amid anticipation of lower taxes and increased military and infrastructure spending. Expectations of a robust economy due to lower taxes and a rollback of business regulations resulted in soaring consumer confidence and economically-sensitive stocks taking off while previously sought-after defensive stocks were jettisoned in the rush to jump aboard the Trump Train. The chart below shows the extremely sharp divergence of different stock sectors in the days following the election.

Stock Market S&P 500) by Sector Performance

July 8, 2016 – December 31, 2016

The markets, anticipating the effects of new government policy, have been pricing in a sea change. We are not ready to fully accept the market’s preliminary conclusion, and expect many of these trends to stall or reverse.

Consider what we refer to as the “Trump Enigma”: what exactly Trump wants to do is unknown; what exactly Trump will attempt to do is unknown; what exactly Trump is able to do is unknown... and only a future unraveling of that enigma will determine how much governmental change we actually get (to say nothing of the effect such change will have on markets). Meanwhile, many industries seem to be expecting regulatory changes which will consist of... whatever changes they have been wanting. Many are likely to be disappointed, as we simply cannot all have it all. Hope is abundant and we fear it exceeds available realities.

Perspective here is important, as political promise is not always reality. A few years ago, expectations soared on the election of Japanese Prime Minister Abe with his positive “can-do” attitude and promise of stimulative “Abenomics”. Many of the proposed policy changes were not realized and economic performance has been underwhelming.

Or consider the case of our very own Governator, ironically the new replacement host of Celebrity Apprentice. He was elected on the similar premise that if we could just elect a smart guy with good intentions who wasn’t beholden to outside money and lobbyists, he or she could then clean up the mess in government. His experience showed it is a lot easier to get elected riding a wave of populism than it is to push legislation across the finish line. Not beholden to anyone, he went toe to toe with the public unions and their lobbyists… and lost, leaving office looking exhausted. Time will tell with the new commander in chief, but in American politics, it is often the swamp that drains you.

The Republican Party is not monolithic (anybody remember the Tea Party and budget sequestration?) and does not have the 60 votes required to pass most legislation in the Senate. Yesterday we picked up the newspaper and read the headline “Rand Paul Defects on Proposed Health Law Repeal” (because of budget concerns) and then today “Republican Skepticism Grows over Strategy on Health-Law Repeal”.

One of the big drivers of the market rally has been the promise of the lower taxes and increased military and infrastructure spending that Trump has endorsed; economic types would call this “fiscal stimulus”. However, given that many Republicans are disposed to be fiscally conservative and government debt is already very high, anything which resembles fiscal stimulus may be very difficult to pass, given it could increase the deficit. We do expect that Trump will have more success rolling back regulations.

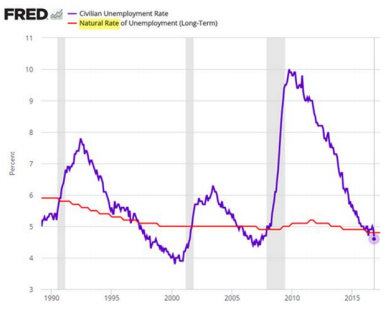

In addition to the difficulty of passing fiscal stimulus, we also question its desirability at this point in the economic cycle. Standard economic policy calls for stimulus in and around recessions to restore employment, but the implementation of fiscal stimulus during periods near full employment mostly only creates inflation. Aren’t we currently seven years into economic recovery? U.S. wage growth just clocked in at its quickest pace since the 2008 financial crisis and we have reached “full employment” (i.e. the rate of unemployment is now below its “natural rate” - red line at right).

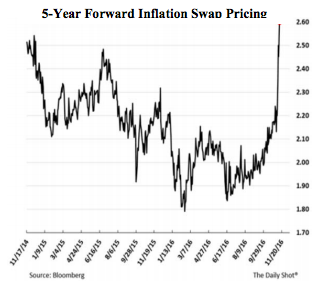

The aforementioned explains a large part of the post-electoral observed jump in market inflation expectations1 and interest rates.

There is a final reason to doubt that all the extreme market movements since the election are justified: the importance of politics to the economy is usually overstated. Since 1928 the median gain during a Democratic Presidential term was 27.7%, vs. a 27.3% gain for Republican terms. A very similar pattern is observed in GDP growth.

Even if Trump is able to push through a legislative agenda along the lines of his campaign rhetoric, we at Knightsbridge maintain a somewhat contrarian view that the jury is still very much out on interest rates. We have written for some time that interest rates could very well remain relatively low for quite some time... and we submit we remain mostly correct so far. It was only last summer that rates were hovering at century low levels and they remain negative in various countries. Last year the Fed raised rates fewer times (once) than was expected at the beginning of last year. Remember the 2013 “taper tantrum” when the Fed first mentioned taking a step back from QE? Rates jumped up sharply, but then shortly fell back. Could the jump in rates since the election be a similarly temporary move? We speculate there may be global structural forces stronger than Trump at work here. Perhaps it is a surfeit of savings arising from increasingly concentrated wealth due to globalization? Whatever the cause, there seems to be some mysterious global force holding interest rates down globally, and since it not well understood, we would be cautious in proclaiming it vanquished.

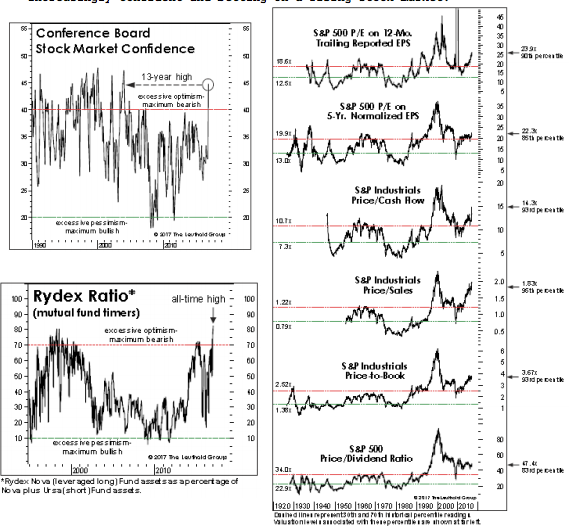

Why are we raising a number of questions and challenges around what is widely presumed to be a propitious economic backdrop and a stock market hovering at all-time highs? We are seven years into economic expansion and we no longer hear anyone talk of the threat of a potential recession. We want to be fearful when others are greedy. The environment is starting to feel greedy, with investors increasingly confident and betting on a rising stock market.

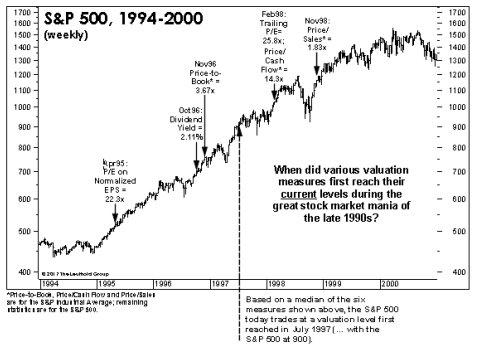

Additionally, the stock market is rather expensive, as the chart to the above-right illustrates. However, as we have written for some time, the stock market deserves to be expensive given the low 7 competing interest rates. Valuation also is not a great timing tool and trends have a tendency to progress further than one expects. As the chart below shows, during the 1990s we reached current valuation levels and blasted right past them. Still, on balance, we view valuation as a cautionary sign.

Lastly, we remind readers of the other risk we have written about: the fragile state of China. The country still has the ingredients of a massive financial crisis. While such an outcome has been, and can continue to be, forestalled, cracks in the Chinese credit and currency markets have recently reemerged, with the Yuan falling further and short-term borrowing rates spiking in a liquidity crunch. Might a potential trade war with America be the needle that pricks the bubble? Trump’s promise to put tariffs on Chinese goods is one of the few the market seems not to be taking very seriously... for now.

Putting all this together, we see: 1) potential for disappointment in what actually comes out of government policy, 2) an already lengthy economic expansion, 3) substantial enthusiasm toward the stock market, 4) a very full (if not quite overdone) valuation environment and 5) risks of a financial crisis in China.

These five factors imbue us with caution and leave us looking for undervalued, potentially left-behind, more “defensive” investments. Healthcare is one out-of-favor example. Our most recent stock purchase, beaten down drug distributor McKesson, is a member of this relatively cheap sector.

It has been tough to sell some of the positions that helped us double the market return last year, especially in taxable accounts, where gains may be realized earlier than we anticipated. For this reason, we have sold fewer positions in our taxable accounts than in our taxfree accounts, but we did feel that at least some cautionary action was warranted. We recognize we may well be early in guiding our investment portfolios toward preparation for stormier times. This recognition and necessity means our defensive turn will be slow and measured. Such a cautious turn will be validated (and reversed!) should we experience significant market weakness.

We thank you for the trust you place in us and wish you all a very prosperous and healthy new year.

Sincerely,

John G. Prichard

Miles E. Yourman

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

1 To be fair, there also have been strong readings of measured inflation around the globe since the election.

© Knightsbridge Asset Management, LLC

Read more commentaries by Knightsbridge Asset Management