On My Radar: The Bond Market is Facing the “Perfect Storm” plus Latest Equity Market Valuation C

Learn more about this firm“Promise yourself to be so strong that nothing can disturb your peace of mind. Look at the sunny side of everything and make your optimism come true.

Think only of the best, work only for the best, and expect only the best.

Forget the mistakes of the past and press on to the greater achievements of the future.

Give so much time to the improvement of yourself that you have no time to criticize others.

Live in the faith that the whole world is on your side so long as you are true to the best that is in you!”

– Christian D. Larson

Brianna, sent me a text message over the holiday, “I just read your OMR piece – very interesting.”

I responded, “Here’s the bottom line:

- We’ve saddled my generation and worse yours with too much debt.

- Because of the debt mess, governments around the world are trying to print, buy and sweep it under the carpet.

- Think “how the economic machine works.” The most important thing to understand is that we are at the end of a long-term credit expansion cycle and at the beginning of a deleveraging cycle.

- Many people can’t get credit anymore. Tapped out.

- We need to get out of this debt mess and reset the system somehow.

- It will take a dozen or so years. It has to break (default in some form) before it can reset.

- The question is whether governments soften the blow or not. A beautiful or ugly deleveraging?

- The U.S. has a better shot. Europe has bigger structural challenges. Japan and China?

- Can one do it? Can they all do it?

- We need to reset or the greater power of economic reality will do it for us.

- We’ll get through it but not without consequences. It will be bumpy.”

I concluded my text reply to Brie saying, “Maybe I need to take a happy pill, but I’m almost certain I’m right. No guarantees. We’ll see.”

And her text back to me made me smile, “Well, on the positive side — this too shall pass and we are fortunate to understand what is happening and can better prepare for it… AND it’s Christmas so let’s not worry and drink some of Rory’s yummy wine .”

How about that! “Promise – peace – optimism – think – best – future – faith – true – you.” Amen!

Brianna works in New York with a team of people lead by her boss Rory Riggs. Google him. He’s sharp and probably the brightest business mind I know. Rory sent Brie home with an outstanding bottle of red wine and, oh yes, we did drink it. Their firm, Syntax, has created a better way to index. Think owning the same stocks in the S&P 500 Index but weighted across the same constituents in a way that diversifies you better. Same with small caps, sectors, etc. The result is an improvement in returns and the numbers are compelling. You’ll want to learn more. Stay tuned.

Today, let’s take a look at the most current equity market valuations for they can tell us a great deal about future 7-year and 10-year annualized returns. We’ll also look at the bond market. Total U.S. credit market debt-to-GDP is nearly 355%. Global debt-to-GDP is 325%.

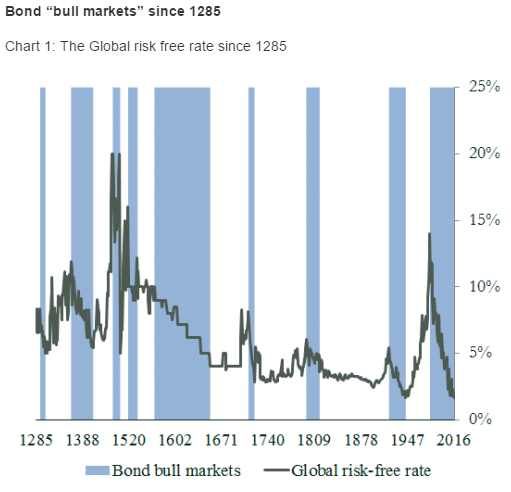

I hope you find the messaging in such a way that your retail client can better understand. I believe that the biggest bubble of all bubbles is in the bond market. If not tactical last quarter, that bond portion of a portfolio took a beating. What can you do? I share a few ideas. You’ll also find a great chart showing bond yields dating all the way back to the year 1285 (not a typo). It is a reminder that we sit at a very unusual period in time. The great bond bull market is behind us… not ahead of us. But let’s see opportunity… not despair.

Included in this week’s On My Radar:

- Year-End Valuations and Forward Equity Market Returns

- The Bond Market is Facing the “Perfect Storm”

Year-End Valuations and Forward Equity Market Returns

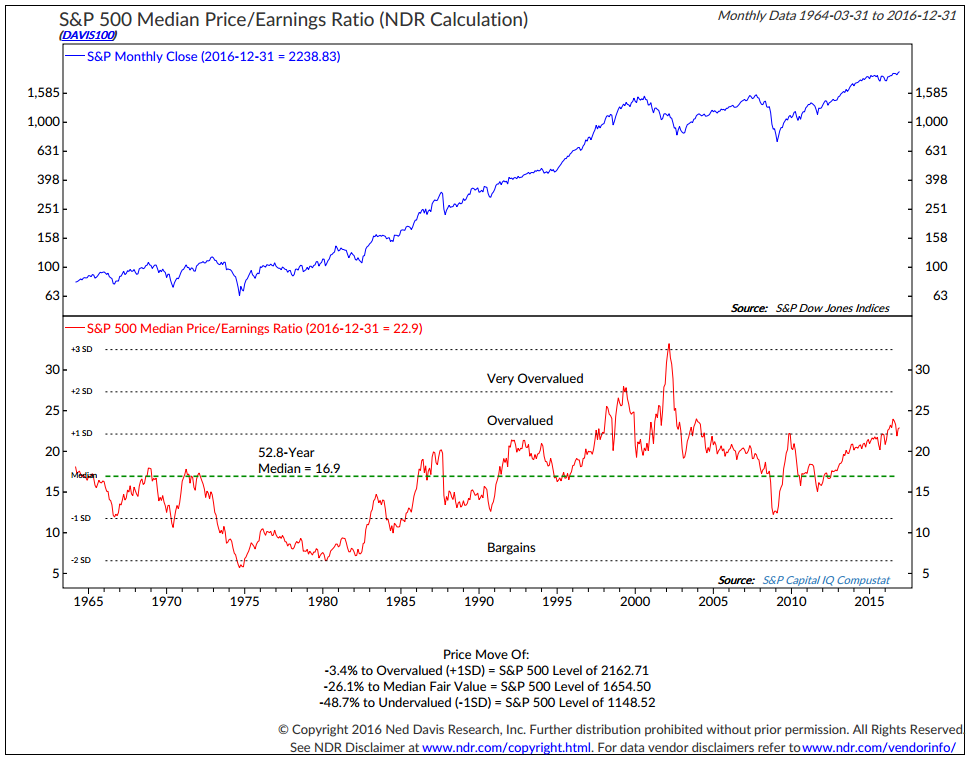

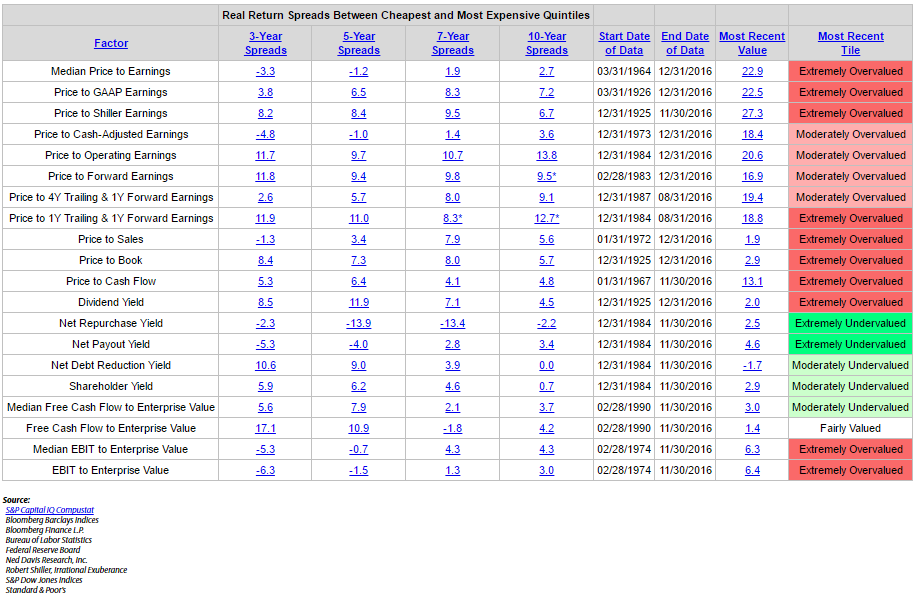

Chart 1: My favorite – Median P/E. At 22.9 the market remains “Overvalued”

Here is how you read the chart:

- Median P/E is the P/E in the middle, meaning there are 250 companies out of 500 that have a higher P/E and 250 that have a lower P/E.

- The red line in the middle section shows you how P/Es have moved over time (updated monthly).

- The green dotted line is the 52.8 year median. So a Median P/E of 16.9 is the historical “fair value.” Simply a point of reference.

- You can see that over time the red line moves above and below the dotted green line.

- The future returns come when you buy at “bargains.” It also happens to be when risk is least.

- As you’ll see in Chart 2, the worst returns come when Median P/E is in the highest 20% of all readings. That is where it sits today. Expensive!

One last comment on the above chart. At the very bottom of the chart, NDR calculates just how far the market is from “Overvalued,” “Median Fair Value” and “Undervalued”. For example, Median Fair Value is determined by taking 16.9 (Median P/E) x 97.90 (Most recent 12-months earnings) or 1654.50. The S&P 500 Index closed the year at 2238.83 which is 26.1% above fair value. A correction of -26.1% would mark a point in time where you would get better bang for your money.

A correction to “Undervalued” would make for a great buying opportunity. Unless one is run over by the 48.7% decline it will take to get there. Such declines come in recession so we’ll keep close watch on the recession indicators (more on that next week). No sign of U.S. recession for now. I am on record predicting 2017 to be the year. I’m not so sure. We’ll watch the data and I have some pretty good recession indicators that have done a good job at calling them in advance. Again, no recession signs today.

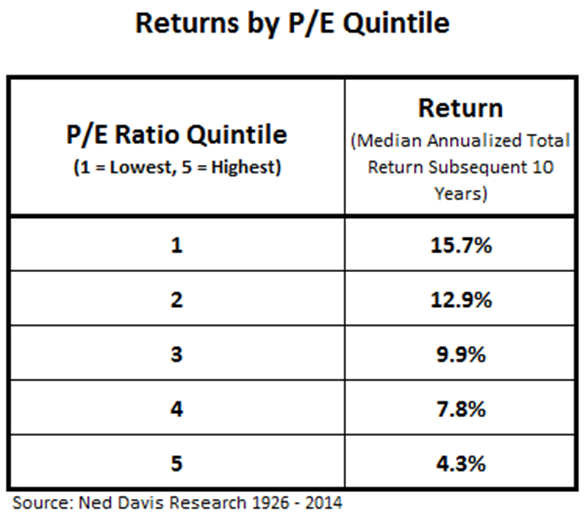

Chart 2: Median P/E and Forward 10-Year Returns

Median P/E can help us predict what is likely to be the coming 10-year annualized returns for the S&P 500 Index. Not perfect but a pretty good guide.

Here is how you read the data:

- A Median P/E of 22.9 puts us in the highest quintile.

- The overall idea is to determine if buying at bargains is better than paying up.

- In this way, looking at actual reported Median P/E every month back to 1921 we can then measure what the subsequent 10-year returns turned out to be.

- Then look at each month and see what the returns were 10 years later. Step forward a month, what were the returns 10 years later. And so on…

- Then group all of the month-end actual reported Median P/Es into five quintiles (not Wall Street’s future guesstimates… actual real numbers) and then evaluate what the subsequent 10-year average returns were by quintile and you get the following chart:

We sit today firmly in quintile 5. It is telling us to expect the low returns over the coming 10 years. We want to be aggressive buyers of equities when we get to quintile 3, 2 and 1. That’s how measuring valuations can help us. For now, patience.

As a forward guide, when I share the Median P/E with you at the beginning of each month, use this next chart as a guide to see which quintile we are in:

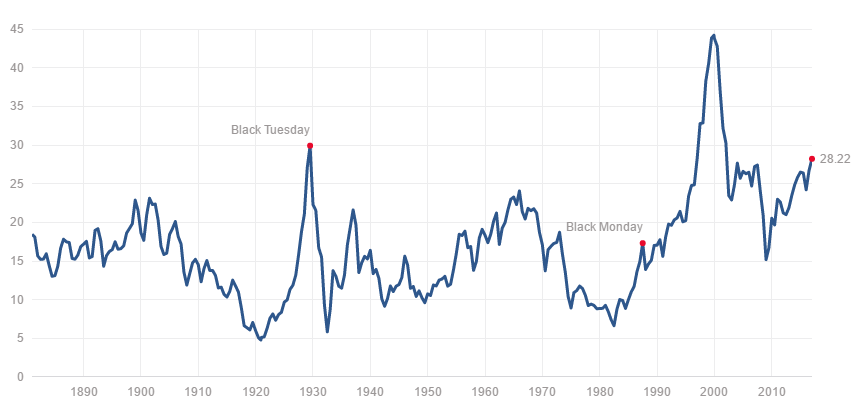

Chart 4: Shiller’s CAPE or Cyclically Adjusted P/E (a measurement process that smooths P/E over the last 10 years).

Current level is 28.26.

In simple terms… historically very high!

Chart 5: Shiller P/E 28.22 as of 1-5-17

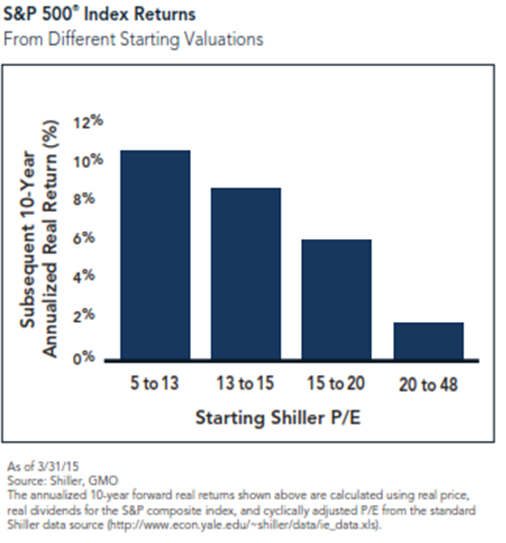

John Hussman shared this next chart — it is similar in thinking to Chart #2 above except it looks at P/E by quartile not quintile. Same conclusions. Expect low coming returns.

Here’s how you read it:

- With a CAPE of 28.26 we sit firmly in the CAPE 20 to 48 quartile. Real returns (nominal returns less inflation) of less than 2% annualized are probable over the coming 10 years.

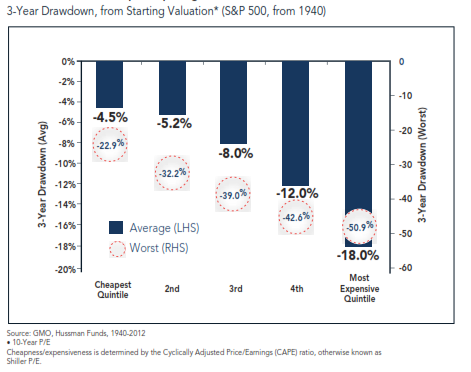

Chart 6: What about Drawdowns?

Here is a look at the downside risk by quintile. Remember, we sit in the most expensive quintile. The simple point is that risk is highest when valuations are highest.

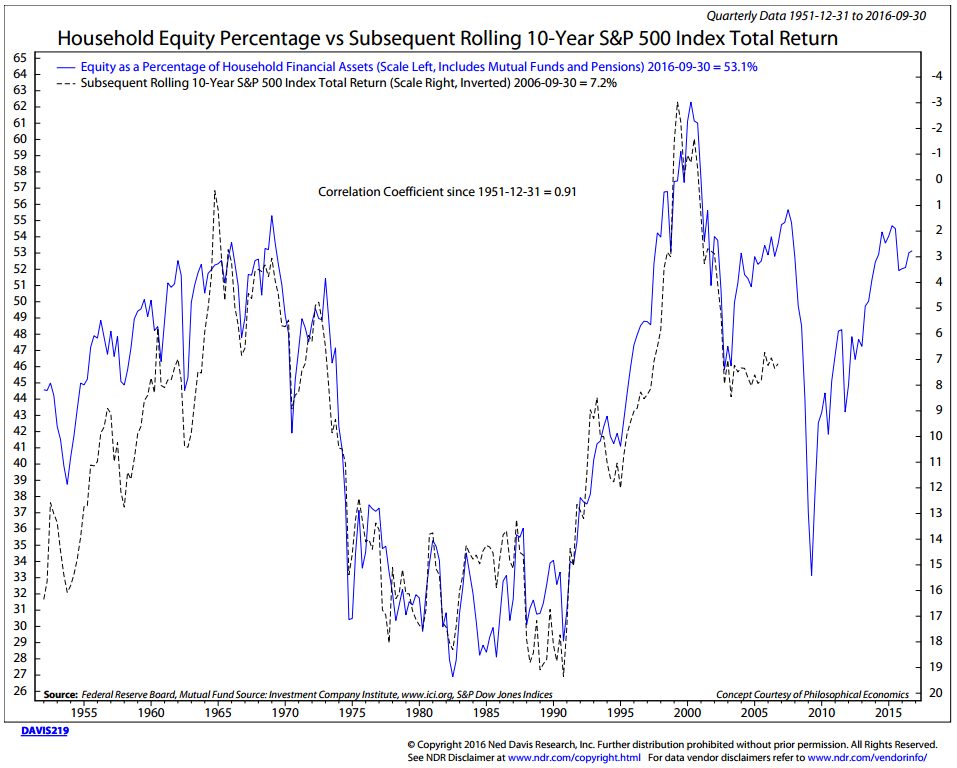

Chart 7: Household Equity Percentage vs. Subsequent Rolling 10-Year Returns

This next chart is one of my all-time favorite charts. Here’s how you read it:

- The blue line tracks just how much households own in equities as a percentage of their total liquid net worth.

- The dotted black line is a plot of what the annualized 10-year return turned out to be.

- What it shows is that at points in time when households had a large percentage invested in stocks, the subsequent 10-year returns were lowest.

- Note late 1999 – early 2000. The blue line was at 62% (left hand column). It predicted a subsequent return of approximately -3% per year.

- The black line shows what actually happened.

- Also note how investors raced out of equities in 2008 and 2009. At the market low in early March 2009, the most recent household equity percentage ownership was at 33%. At that level, the data is projecting a 15% annualized return from 2009 to 2019.

- We don’t yet know the 10-year numbers but pretty safe to say that so far returns for equities since March 2009 have been good. Problem is, and I’m pretty sure you’ll agree, that most people were in a state of pure panic. They were selling when they should have been buying.

- Finally, where are we today? The blue line is at 53.1% as of September 2016 quarter-end suggesting a 2.75% coming 10-year annualized return (before inflation).

We can use this chart as a guide. I’ll share it with you from time to time. Point is that we want to get our clients prepared to overweight stocks when the getting gets good. The hard part is they’ll need to be a buyer when everyone around them is panicking. That’s when opportunity is always best.

Chart 8 – Price to Sales, Price to Operating Earnings, Etc.

Here’s how you read the chart:

Look to the far right – most valuation metrics are “Extremely Overvalued”

The Bond Market is Facing the “Perfect Storm”

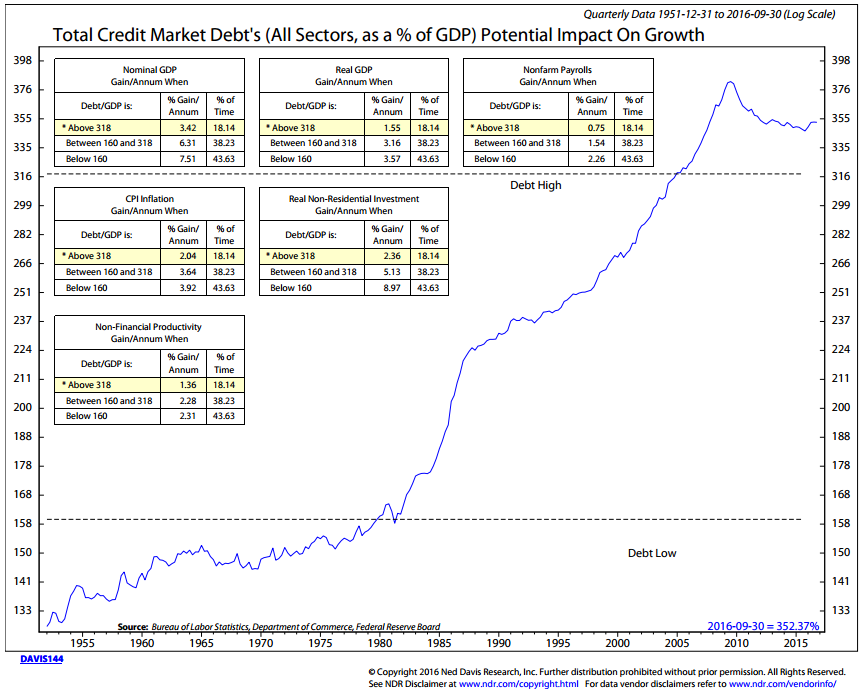

I’ve been saying for some time that the biggest bubble of all bubbles is in the bond market. European sovereign debt might just be the first to crisis. Further, global debt has reached 325% of GDP. Academic studies show that economies get into trouble when debt-to-GDP exceeds 90%.

OK, in English for your clients who have other important things to focus their time on: If you earn $100k per year and borrow $10k per year, your spending power was $110,000 (before taxes, of course). That leveraging up fuels the economy. Another year passes, you earn more, your credit rating improves, and you can borrow more. Economies expand on income and credit (spend today is good for growth – pay off tomorrow is bad for growth). But how do we know when we’ve reached tomorrow?

Academic research shows that number to be about 90% debt-to-GDP. Think of GDP as a country’s gross income. So what if you earn $100k and borrowed and now owe $90k? Can you see it is now getting harder to borrow from a bank and that more of your income is required to pay the interest on the $90k debt? Your economy slows.

Expand that to the U.S. and you find a 105% debt-to-GDP number. Well, the number is actually much higher than that if you include Social Security and Medicare debts and several others government has creatively reworded, but they are debts to be paid and the total number is north of 250%.

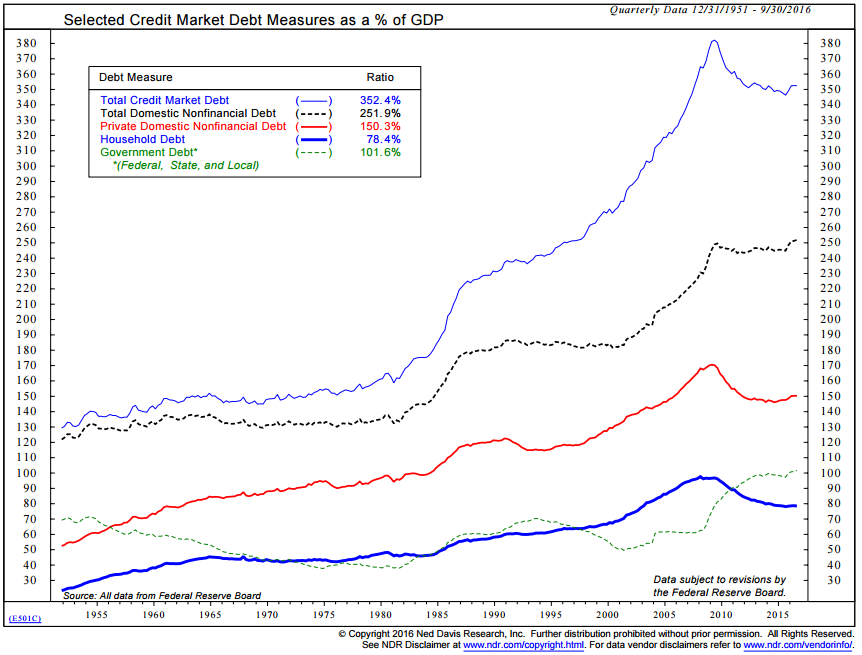

The next chart shows the breakdown of that debt.

Global debt-to-GDP is now 325% of world GDP, rises to record $217 trillion. Europe and China are a mess. When I say “debt” is our single biggest global issue, debt here, there and everywhere, it is like you are earning $100k and owe $325k to the banks and credit card companies. Is it any wonder that global growth has slowed and limps along?

Every country is competing for growth. How? Lower currency in a way that puts your goods on sale. It gets dicey. All this leads to currency and trade wars. We are seeing this in China, Europe and in Trump tweets today.

As Hardy said to Laurel, “Well, here’s another fine mess you’ve gotten me into!”

Harvard Academic Sees Debt Rout Worse Than 1994 ‘Bond Massacre’

The current bond market is facing the “perfect storm” of potential steepening of the bond yield curve, monetary policy tightening and a multi-year period of sustained losses due to a “structural” return of inflation resembling that of 1967. (Source: Bloomberg)

If you thought you had already read the gloomiest possible prognosis for bonds, wait until you read this one.

Paul Schmelzing, a Ph.D. candidate at Harvard University and a visiting scholar at the Bank of England, said if the latest bond market bubble bursts, it will be worse than in 1994 when global government bonds suffered the biggest annual loss on record.

“Looking back over eight centuries of data, I find that the 2016 bull market was indeed one of the largest ever recorded,” wrote Schmelzing in an article posted on Bank Underground, which is a blog run by Bank of England staff. “History suggests this reversal will be driven by inflation fundamentals and leave investors worse off than the 1994 ‘bond massacre’”.

The gist of his message is this:

- Schmelzing research focuses on the history of international financial systems.

- He divided modern-day bond bear markets into three major types:

- inflation reversal of 1967-1971,

- the sharp reversal of 1994 and

- the value at risk shock in Japan in 2003.

- The Bank of America Merrill Lynch Global Government Index of bonds fell 3.1 percent in its worst-ever annual loss in 1994 as then-Fed Chairman Alan Greenspan surprised investors by almost doubling the benchmark rate.

- Treasury 10-year yields surged from 5.6 percent in January to 8 percent in November.

- Schmelzing said, “The current bond market is facing the “perfect storm” of potential steepening of the bond yield curve, monetary policy tightening and a multi-year period of sustained losses due to a “structural” return of inflation resembling that of 1967.”

- Last quarter was the worst for government bonds since 1987, according to data compiled by Bloomberg.

I bet you’re sitting there wondering what bond yields look like today vs. the year 1285. Here you go:

Not your father’s bond market. Interest rates move higher and the squeeze gets tighter.

But, fear not! Just think about your bond allocations differently.

Here’s what you can do:

Diversify the bond portion of your portfolio to several tactical bond trading strategies. If we are heading for a reset, which I believe may take several years, then you’ll want to find ways that gets you to that higher interest rate opportunity with capital intact. It won’t be straight up; it will be bumpy. Protect and grow, protect and grow.

Trend following trading strategies can help:

- Tactically trade the trends in high yield. Non-emotional. Easy to implement but requires an ability to religiously stick to the process. A high percentage of profitable trades with downside risk protection.

- Take a look at the Zweig Bond Model signal… I post the chart each week in Trade Signals.

- Tactical Fixed Income – take a look at our Tactical Fixed Income Index. It looks at nine fixed income ETFs and allocates to the top two showing the strongest positive price trends. It lost 1.08% last quarter vs. a decline of 7% in the Barclays Global Bond Index. A 6% beat. It gained 11% for the full year 2016 vs. a gain of just 2% in the Barclays Index.

- Diversify to several tactical fixed income trading strategies. No guarantees — all investments involve risk; however, each of the above three processes came through the recent spike in interest rates (loss in bonds) quite well.

The point is that now is not the time to buy-and-hold bond funds and ETFs; however, bonds can still play an important role in your portfolio(s).

Concluding Thought

Put this next chart in the “food for thought” category. Look at those bond returns from 1950 up to 1980. Just saying…

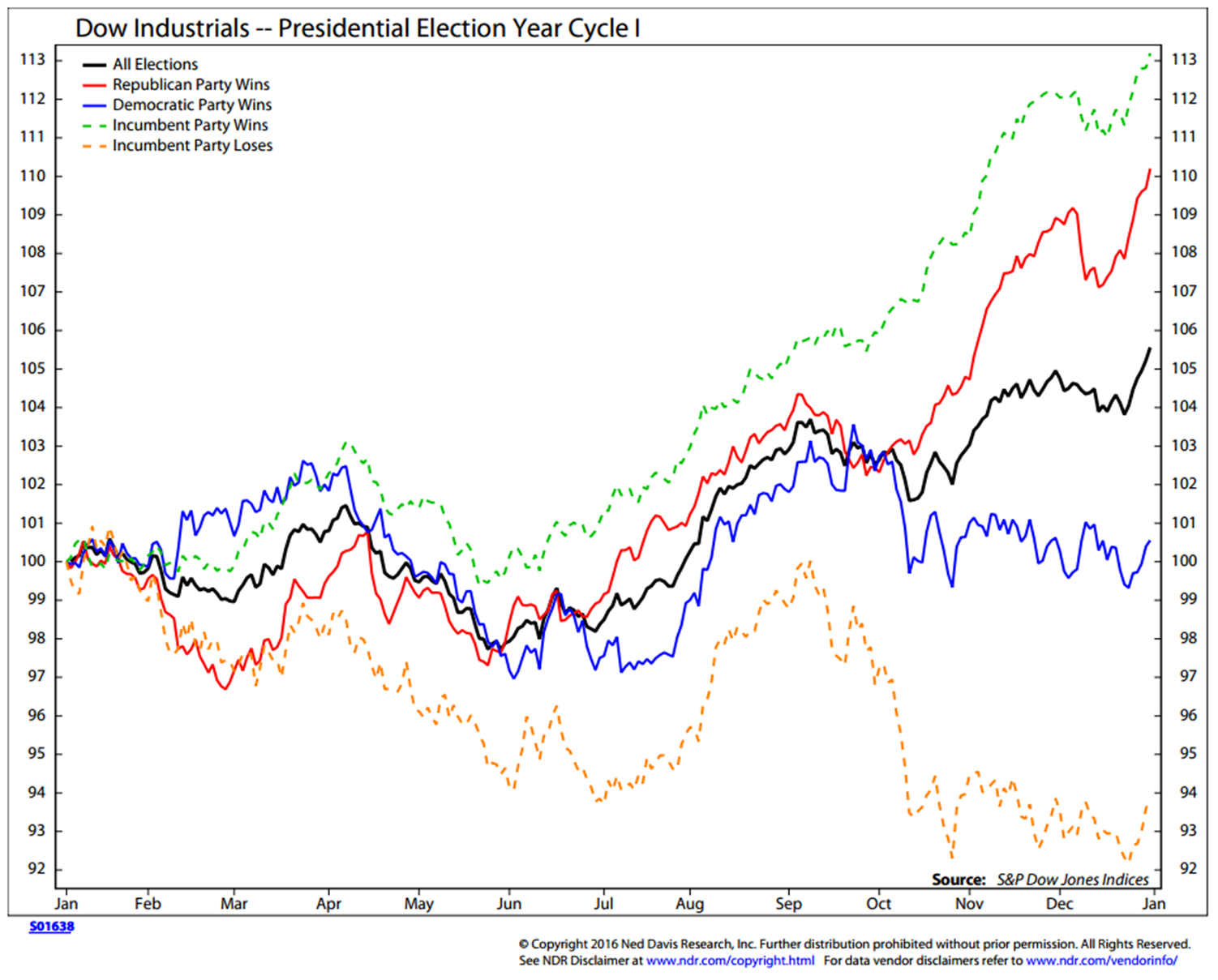

Put this last and final chart in the “fun” category:

- This chart shows what the Dow Industrial average did in prior election cycles – year one.

- The orange dotted line shows what the market did the first year when the incumbent party lost.

If this chart is to be any guide to 2017 (and there is most certainly no guarantee), then expect a market top in January followed by a retest of the high in September and a sell-off into year end. It suggests a negative return year for equities. Of course, no guarantees and data set is fairly small.

Keep in mind that if you gained 1% in 2015 and 10% in 2016 and the market corrects 6% to 10% in 2017, then your equity gains for the full three years will be close to 0%. Overall, high valuations and high debt and low growth are the culprits. We remain in a low coming 10-year return world.

The S&P was up just 3% going into the election. The prior two years of gains stood near that same number — up 3% over 24 months. Frustrating. To the surprise of all of us (certainly me), the market gained 7% from the election into year-end. So far, 2017 is off to a pretty good start.

Wishing you a wonderful weekend!

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

The CMG Tactical Fixed Income Index and CMG Tactical All Asset Index are rules-based indexes that reflect the theoretical performance an investor would have obtained had it invested in the manner shown and do not represent actual returns, as investors cannot invest directly in the Indexes. The CMG Tactical Fixed Income Index and CMG Tactical All Asset Index returns represented do not reflect the actual trading of any client account. No representation is being made that any client will or is likely to achieve results similar to those presented herein. The CMG Tactical Fixed Income Index performance results are presented net of a 2.50% maximum annual fee deducted from the account balance quarterly, in arrears.

Any financial product based on the CMG Tactical Fixed Income Index, CMG Tactical All Asset Index or any index derived therefrom that is offered by CMG Capital Management Group, Inc. is not sponsored, endorsed, sold or promoted by Solactive AG and Solactive AG makes no representation regarding the advisability of investing in the product.

Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group

© CMG Capital Management Group