1. Over Two-Thirds of Americans Retire Too Early

2. The Main Sources of Income in Retirement

3. Most Retirees Spend Less Than They Can Afford

4. How Retirees Can Avoid Under-Spending in Retirement

Overview

We all know that there is a savings crisis in America. According to the National Institute on Retirement Security (NIRS), the median savings balance of near-retirement households is only around $12,000, while the median saving balance for all working-age households is only around $3,000.

NIRS states that some 45%, or 38 million working-age households, have no retirement savings. Based on 401(k)-type accounts and IRA balances alone, NIRS says some 92% of working households do not meet conservative retirement savings targets for their age and income. Even when counting their entire net worth, 65% still fall short.

While saving trends have started to improve over the last couple of years, we’re still facing a huge shortfall, especially among Baby Boomers of all races who are retiring in droves. No one knows the solution to this dilemma. The obvious answer is that most Americans will need to work longer before they retire.

Yet just the opposite is happening. Americans are retiring earlier and earlier. Recent data show that over half of working Americans are retiring between the ages of 61 and 65, despite their lack of savings. This doesn’t make sense.

Even more surprising is another study which found that most retirees in recent years are spending even less each year than they can afford to in retirement. Here again, the reasons are not entirely clear. I’ll try to make sense of them as we go along today.

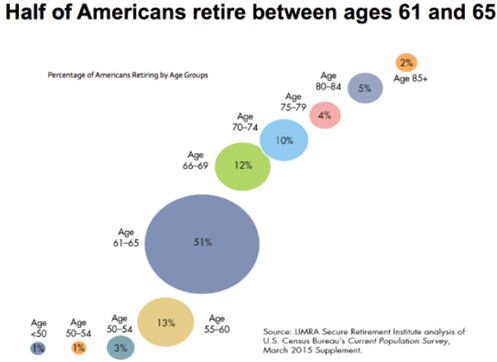

Over Two-Thirds of Americans Retire Too Early

You’ve heard the horror stories about many Americans retiring with puny nest eggs and little income to live on. Still, data show that more than two-thirds of Americans are out of the full-time workforce by age 66.

Over half of Americans quit working between the ages of 61 and 65, while 18% retire even earlier, according to the data shown below from the LIMRA Secure Retirement Institute. By age 75, almost 90% of Americans have left the labor force, LIMRA says, despite the savings crisis.

The retirement statistics no doubt include some people who can’t find work or who can’t work because of health problems. Still, early retirement usually means an income squeeze. So what gives?

Along with stopping work early, most Americans begin collecting Social Security before their full retirement age, which is 66 for many and rises to 67 for those born after 1960. That’s a bad idea since it reduces the total amount they’ll receive from the government over their lifetimes.

Fortunately, the percentage of those claiming Social Security early has declined in the last few years. That’s good news because monthly benefits rise by roughly 6.5% to 8% a year between ages 62 and 70. Still, in 2014, 57% of men and 64% of women took Social Security early.

Half of leading-edge Baby Boomers, those ages 61 to 69, have fully retired and about 15% of the total US population is now finished with work. Among this group, the presence of a traditional pension or retirement plan is often what separates those considered income-rich from those who are not, according to the latest LIMRA report.

The Main Sources of Income in Retirement

Retired Americans receive over $1.3 trillion in income annually. The vast majority of this income comes from two sources: Social Security (42%) and traditional pension and retirement plans (30%), with the remainder coming from other sources. The traditional pensions remain fairly common for those over 75, but are virtually nonexistent for those under 35, LIMRA found.

Some 41% of retirees have annual income of less than $25,000, and of those, only 21% receive income from a pension or retirement plan. Meanwhile, of retirees with income over $50,000 a year, about 80% draw from a pension or retirement plan.

To get a picture of how severe the retirement income crisis is -- and why more Americans should consider working longer and delaying Social Security -- LIMRA looked at total household savings.

US households own $31 trillion of investable assets. That’s an average of $253,200 per household. But most of that is owned by the wealthy. The median holding of investable assets is just $17,500, and three in four American households have saved less than $100,000.

Most Retirees Spend Less Than They Can Afford

Much of the advice on managing your finances in retirement focuses on controlling spending to ensure that assets last a lifetime. And that certainly makes sense, especially for people who are short on savings.

But many retirees face a different problem. They have sufficient resources to support themselves, but are so reluctant to draw on their nest egg that it continues to grow throughout retirement. In other words, they spend less than they can afford to in retirement.

That may be good for their heirs, but it can prevent them from enjoying their retirement life as much as they could. Here’s how to stop “spendaphobia” from undermining the retirement Americans have worked and saved so hard to attain.

Researchers including the American College of Financial Services chief academic officer Michael Finke found a “retirement consumption gap” when they examined retiree spending habits between 2000 and 2012 for a study published earlier this year.

Specifically, except for households of low to modest means, the retirees they tracked were spending less on average than the amount available to them from Social Security, pensions and income from retirement accounts. In the case of wealthy retirees, the researchers calculated that they were spending less than half the annual amount they could actually afford to spend.

Vanguard, one of the world’s largest investment companies, discovered a similar reluctance to spend when it surveyed retirees with at least $100,000 in financial assets. For example, when Vanguard looked at what it called “cornerstone accounts” -- workplace savings plans, IRAs, brokerage and mutual fund accounts -- it estimated that retirees spent only 60% of the money they withdrew, and reinvested the remaining 40% in other accounts.

There are any number of reasons that explain why many retirees are so hesitant to spend down their savings. The combination of longer lifespans and the inherent difficulty of estimating a sustainable withdrawal rate can make retirees overly cautious about spending for fear of outliving their assets.

Likewise, the threat of high medical expenses or a medical emergency late in life may also lead many people to be especially conservative about tapping their nest egg. And undoubtedly some retirees may limit spending because they wish to pass on a legacy to heirs.

But Finke believes there’s also a psychological or emotional factor that contributes to this aversion to spend. “A lot of retirees have formed a habit of thrift over the years. And they’ve developed a decision-making rule that you don’t spend more than your income,” he explains.

What they consider income can include interest, dividends and other distributions from investments, Finke says, but not the capital growth of their portfolios -- which makes them reluctant to dip into principal.

Indeed, when Finke and another researcher asked retirees as part of a yet-to-be-published study whether they would feel uncomfortable spending down assets in order to maintain their retirement lifestyle, three-quarters answered YES.

How Retirees Can Avoid Under-Spending in Retirement

So how can you prevent such fears -- financial or emotional, rational or not -- from in effect cheating you out of the retirement happiness you deserve by relegating you to a more frugal lifestyle than is necessary given the resources at your disposal?

On the financial front, the single most important thing you can do is start with a reasonable idea of how much you can afford to spend each year from your nest egg, without subjecting yourself to an undue risk of running out of money too soon. You can’t know that number exactly. There are too many uncertainties involved -- the market’s ups and downs, unanticipated expenses, medical costs and how long you might live, just to name a few.

By going to a retirement income calculator that uses Monte Carlo simulations to make its projections, you can see how the chances of your nest egg lasting the rest of your life vary based on different withdrawal rates and different estimates of how many years you’ll spend in retirement.

By running several scenarios with different withdrawal rates and time horizons, you should be able to come away with a decent sense of how much spending your nest egg can reasonably support over your lifetime.

If you plan to leave assets for heirs or want to factor in the possibility of large health care expenses in the future, you can set aside money for those purposes and then estimate your sustainable level of spending net of those amounts. You can do this sort of analysis using T. Rowe Price’s Retirement Income Calculator, which you’ll find in the Tools & Calculators section of RealDealRetirement.com.

Of course, this exercise may not overcome the various psychological or emotional impediments to spending. But a way to deal with those issues is to find ways to spend that tend to make for a happier retirement -- and thus may make retirees more amenable to parting with their money.

On that score, Finke says, you’ll get the biggest bang for your buck from “social spending” -- that is, outlays for activities that take you outside of yourself and keep you engaged with other people, such as traveling, dining out, and taking vacations with friends and family.

That’s hardly surprising, as research shows that retirees who are more socially connected and enjoy active relationships with friends and relatives tend to be happier in retirement. This makes sense.

In conclusion, you definitely don’t want to loosen your purse strings so much that you end up depleting your savings too soon. Yet the research shows just the opposite, that most retirees are spending less than they can afford. It would be a shame to work and save your entire career for retirement and not fully enjoy the fruits of all that planning.

Just something to think about.

Wishing you the very best in 2017,

Gary D. Halbert

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

|

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management