1. Interest Rates Spike on Fears of Rising Debt & Inflation

2. Global Investors Dumping Bonds & Reaching For Stocks

3. Concerns Over Bonds & Inflation May be Early & Overblown

Interest Rates Spike on Fears of Rising Debt & Inflation

Bond investors have had a rough ride in November. The Barclays Global Aggregate Bond Index plunged by 5% during the last two weeks just before and after the election – its worst such drop since March 2003, according to Dow Jones data. When yields rise, bond prices fall, and vice-versa.

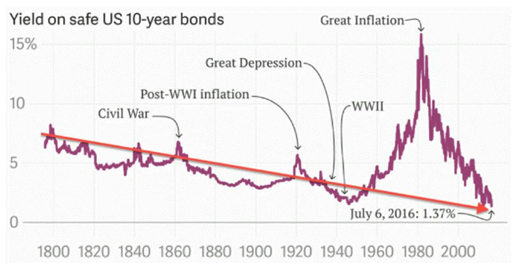

As you know, interest rates have been falling for over 35 years since peaking in 1980. It has been a spectacular bull market for bond investors, that is until just recently. To say that the reversal over the last few weeks came as a surprise to bondholders around the world is an understatement.

More than $77 billion in assets are benchmarked to the Barclays Global Aggregate Bond Index, according to Morningstar, making it one of the most widely followed in the fixed-income world. It incorporates investment-grade debt denominated in 24 different currencies. Sovereign bonds have historically been the Index’s most heavily-weighted constituent, followed by asset-backed securities, corporate bonds and government-related debt.

Global bond yields have been edging up since falling to historic lows in late June/July following the UK’s vote to leave the European Union. But the selloff accelerated aggressively after Donald Trump won the US presidential election – an outcome that took most bond market participants around the world by surprise.

The sharp selloff was predicated on the notion that Donald Trump’s campaign promises to rebuild America’s infrastructure, cut taxes and raise trade barriers, would – if they become reality – drive up inflation, and possibly force the Federal Reserve to raise interest rates much more aggressively than had been expected.

In just the two days following Trump’s election, global bonds shed an estimated $1.1 trillion in value, the worst rout in a year and a half as investors sold bonds and bought stocks in many cases. The stampede out of bonds propelled US Treasury yields to their highest levels since January.

The 10-year Treasury Note yield soared from a record low of 1.36% in late July to near 2.4% yesterday. While 2.4% might still seem low, that is a huge increase since late July. The spike up at the end has happened since the election.

The 30-year Treasury bond yield has seen a similar spike in the last two weeks. After hitting an all-time record low near 2.1% in late July, the bellwether long-bond soared to just over 3% last week, another huge move in percentage terms.

The question is, have we finally seen the lows in interest rates? I’ll come back to that below.

Global Investors Dumping Bonds & Reaching For Stocks

Global investors have rendered their verdict on Donald Trump as president: Sell government bonds and pile into stocks that should benefit the most from a resurgent United States economy.

From Indonesia to the United States, government bonds are undergoing a sharp selloff as investors – including large sovereign wealth funds and hedge funds, as well as the accounts of American retirees – restructure investment portfolios to try to capture the fruits of what they expect will be a free-spending Trump presidency.

Across the board, the yields of these bonds, which move up as their prices decline, are pushing higher. The yield on the 10-year United States Treasury note – a benchmark for mortgages and many other lending rates – has risen to above 2.2% from 1.5% in less than two months. For such a widely-held and traded security, that is an unusually abrupt move.

Other safe-haven bonds have had similar reactions. The yield on Germany’s 10-year government notes has gone to positive. In just over a week, it has gone from negative 0.15% to positive 0.35%. And the Swiss 10-year note is now on the cusp of paying investors to borrow money after close to two years of trading in negative interest rate territory.

If this trend continues, it will signify a jarring philosophical shift from the view put forward by many prominent economists, like former Treasury Secretary Lawrence Summers. He has predicted for several years that the global economy is destined to stagnate for some time under a regime of low growth, zero interest rates and maybe even deflation. But that view is changing in the wake of the US election.

In just the last few weeks, millions of risk-averse investors who have been camping out in government bonds for years now have become concerned with Trump’s economic plans. Trump promises to have the federal government take responsibility for stimulating the economy – in the form of big infrastructure investments and significant tax cuts – rather than relying on the Fed and global central banks.

After the financial crisis unleashed an unprecedented wave of activism on the part of global central banks, investors the world over followed the lead of central bankers and loaded up on long-term government bonds. Until recently, that has been a no-risk trade, with global growth stagnant and interest rates expected to remain “zero-bound” indefinitely.

Again, that view is changing rapidly. The numbers tell the story.

Concerns Over Bonds & Inflation May be Too Early & Overblown

According to J. P. Morgan Chase, central banks and financial institutions in developed countries are sitting on $26 trillion in bonds, or 49% of the entire tradable market for these securities. That figure is staggering, up from 40% in 2002. It highlights the extent to which worries about deflation and stagnation (political and economic) have resulted in a non-stop bull market for government bonds – that is until recently.

Making matters worse still, of the $50+ trillion in bonds outstanding, almost $11 trillion is in debt securities with a negative yield – meaning that investors have to pay to own them. Since central banks in Europe and Japan pushed sovereign yields into negative territory, the US dollar level of bonds with sub-zero yields grew at one point to nearly $12 trillion.

The point is, the bond market is the largest market in the world and apprx. 20% of it is made up of negative yielding securities.

The question is, will the wave of bond selling/stock buying that we’ve seen over the last few weeks continue?

Most analysts agree that the bond market is severely oversold at this point and thus overdue for a bounce. Along that same line, the bond markets may have reacted too severely to Donald Trump’s election. He won’t even take office until late January, and then it will likely be at least several more months before we know exactly what priorities he will actually pursue – much less how successful he will be in getting his programs passed and funded.

Put differently, it is likely too early to be making investment decisions based on a fast-growing economy and higher inflation. In that context, I would not expect interest rates to continue to shoot higher as they have done over the last several weeks.

And let’s not forget that the Federal Reserve is likely to raise the Fed Funds rate on December 14. The odds of a rate hike on that date are now north of 90% according to the futures market. This could well cause a downward correction in equity prices, so I would not be a seller of bonds/buyer of stocks at this point.

Yet the longer-term implications for bonds and interest rates are much less certain. It is true that Trump plans to increase federal spending significantly, including a massive infrastructure program which could potentially create a million new jobs or more and boost the economy over time.

Mr. Trump’s unfunded pledge to spend $550 billion or more on infrastructure would boost federal borrowing and, by creating jobs at a time of near-full employment, could cause inflation to rise over time. But I would think that would be late next year at the earliest.

In addition, Trump has proposed significant tax cuts for corporations and individuals. Even if he is successful in getting those passed next year, their effects on the economy won’t be felt until sometime after they go into effect – perhaps not until 2018. Yet many investors seem to think that just the thought of large tax cuts means three decades of falling bond yields may be over.

Perhaps the greatest concern about Trump’s plans is that his big spending and tax cuts will balloon the federal budget deficits. Yet if these plans are successful in goosing the economy, the budget deficits should be manageable. I will have much more to say in this just ahead.

Next, Trump proposes rolling back significant government regulations across the board, with the idea that such rollbacks will stimulate the economy. I agree, but I would caution that such deregulation will be less than Mr. Trump envisions, will take longer than expected to enact and does not automatically mean that inflation will rise significantly anytime soon.

My point today is that the bond and stock markets may be getting ahead of themselves. It remains to be seen what will happen after Donald Trump takes office, how much of his pro-growth agenda he will get through Congress and how long it will be for those policies to result in stronger economic growth and higher inflation.

In conclusion, I would caution investors against making snap decisions on bonds or stocks in response to the election, as so many seem to be doing. We need to wait awhile until we have more information.

HAPPY THANKSGIVING EVERYONE!!

Wishing you thanks,

Gary D. Halbert

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

|

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management