When I last wrote about gold, I discussed the argument for gold as a potential hedge against volatility. Now, in recent weeks political uncertainty has returned, and with it, volatility. The VIX Index recently traded to its highest level since early September. As risky assets like equities and high yield bonds have come under pressure, gold has rallied roughly 4% (source: Bloomberg).Still, many investors remain concerned that gold will falter in an environment of rising rates. Although this is a reasonable concern, it is important to note that gold’s prospects are highly dependent on not only the direction of interest rates, but also why they are rising.

Historically, gold typically comes under pressure when real, or inflation adjusted, interest rates are advancing. Since 1972, the level and change in real 10-year Treasury rates, along with changes in the dollar index, have explained roughly 30% of the change in the price of gold. This makes it easier to see why gold sold off in the late summer and early fall: Real 10-year yields rose roughly 15 basis points (bps, or 0.15%) between late July and early September (source: Bloomberg).

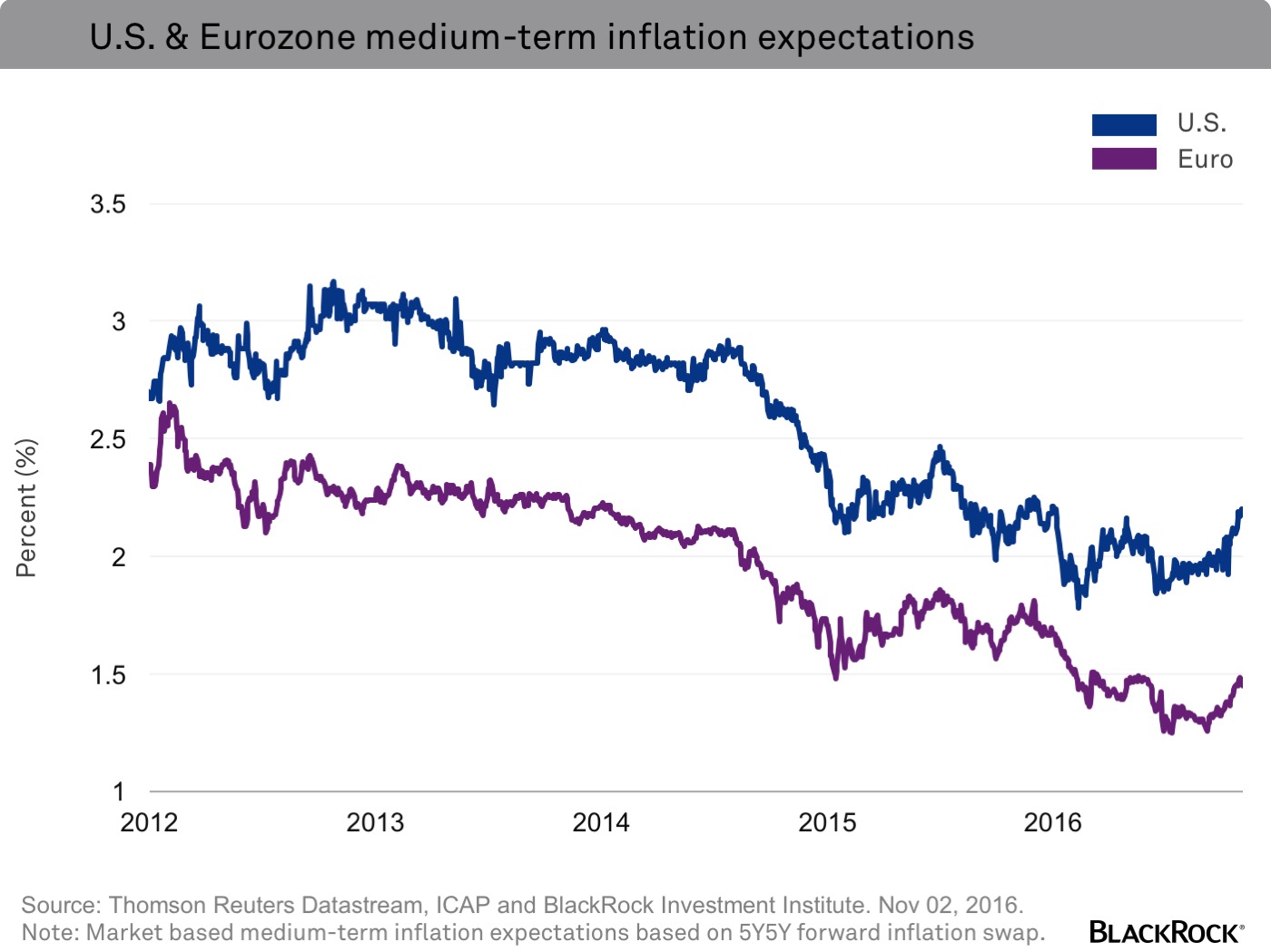

Higher inflation expectations

However, more recently real yields are no longer driving rates. While nominal 10-year yields are roughly 10 bps higher than their September peak, real yields have slipped. Instead, higher rates have been driven by higher expectations for inflation. Based on the 10-year Treasury Inflation Protected Securities (TIPS) market, inflation expectations recently hit 1.75%, the highest level since the summer of 2015. See the chart below. To the extent that rates are being driven by changing perceptions of inflation and not real rates, higher interest rates may not be an impediment for gold.

This raises the question: Can inflation expectations continue to rise? Probably. Despite the sharp rise in inflation expectations, 10-year breakevens (the difference between the yield on a nominal fixed-rate bond and the real yield on TIPS) remain depressed relative to their long-term history. As recently as two years ago, inflation expectations were roughly 2.25%.