The October job market data were not far from expectations, consistent with a further tightening in labor market conditions. While the average hourly earnings figures can be quirky (the data are often revised in the following month), wage growth appears to be picking up. That should keep Fed policymakers on track to raise short-term interest rates in December.

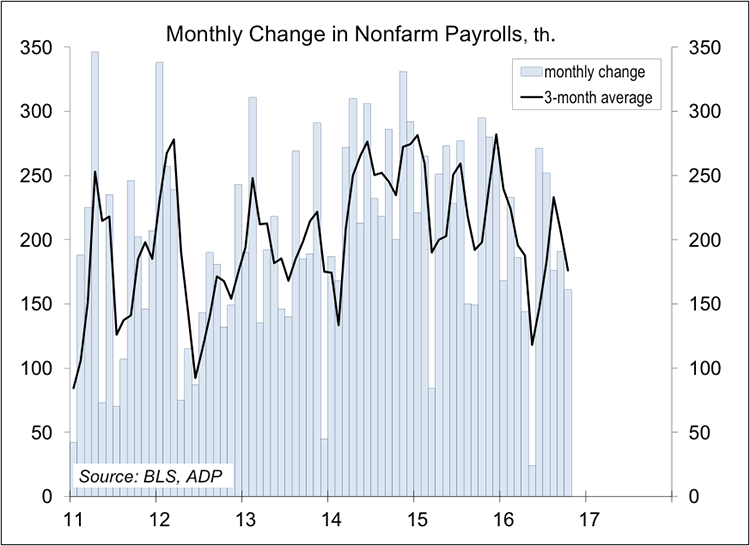

Nonfarm payrolls rose by 161,000 in the initial estimate for October, a bit lower than expected, but previous figures were revised higher. While there is a fair amount of noise from month to month, the pace appears to have slowed this year. However, job growth remains relatively strong given the demographics (slower growth in the working-age population). Remember, we need a bit less than 100,000 jobs per month to remain consistent with population growth.

Nonfarm payrolls have now risen for 72 consecutive months, the longest string ever (the previous record was 48 months). Private-sector payrolls have risen by 15.5 million.

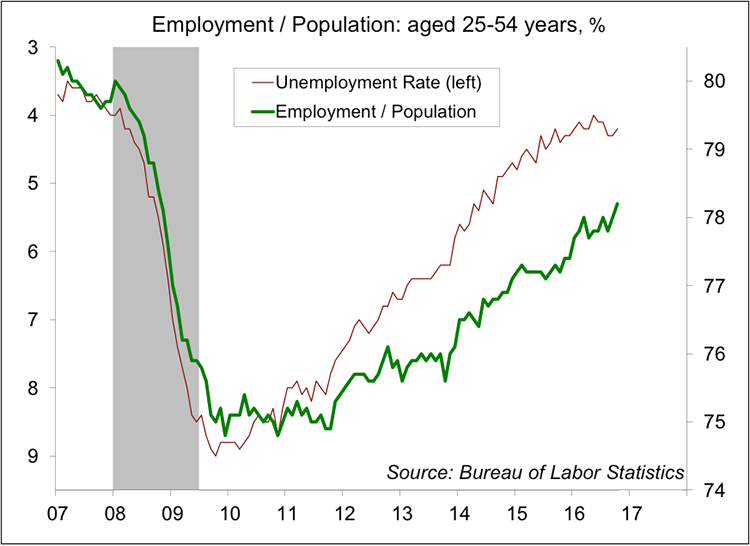

The unemployment rate edged down, partly reflecting a drop in labor force participation. Do not read much into that – it is consistent with the usual noise in the Household Survey. The employment/population rate also edged down, but the trend for the key age cohort, those aged 25-54, has continued to improve. As this key cohort moves up to better jobs, space will be created for teenagers and young adults to get experience (the typical late-cycle pattern in a job market recovery).

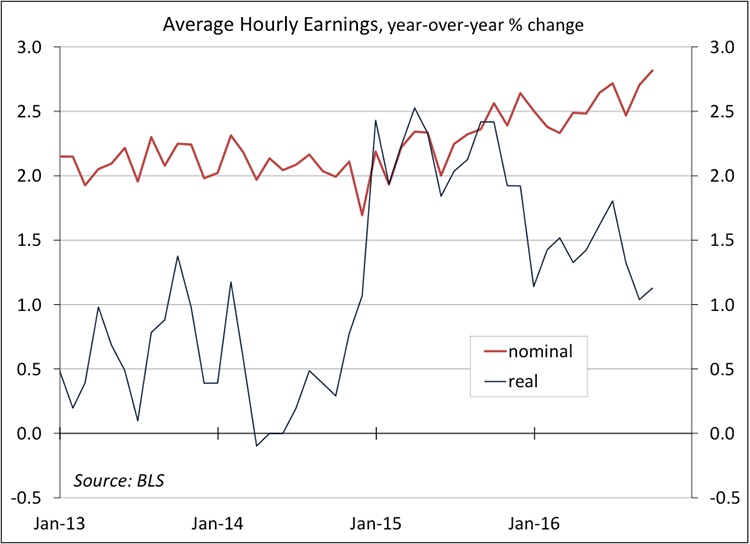

As the job market tightens, one should see some upward pressure on wages. Average hourly earnings, as reported, are often quirky. Large gains may be revised away in the next month’s report or may be followed by more modest gains. Average hourly earnings rose 0.4% in October, up 2.8% y/y.

While nominal wage growth has picked up over the last year, real wage growth has slowed. That moderation reflects the stabilization and initial rise in gasoline prices. The recent increase in gasoline prices has come at a time of year when they usually fall – hence, the increase is magnified by the seasonal adjustment. The benefit to consumer spending growth of lower gasoline prices was expected to fade over time. The pickup in nominal wages helps to offset some of that impact.

Where does this leave the Fed? The Federal Open Market Committee’s November 2 policy statement made it clear that officials are getting closer to raising rates. However, the FOMC did not completely lock down a December 14 move. Policy action will remain data dependent, driven by the job market and the inflation outlook. We’ll get another employment report ahead of the mid-December FOMC meeting. While the Fed isn’t going to react to any one piece of data, the November job market figures should play a critical part in the Fed decision. At the same time, Fed officials are not expected to raise rates aggressively in 2017. However, that may depend on the pace of wage growth and the ability of firms to pass higher costs along.

© Raymond James

© Raymond James

Read more commentaries by Raymond James