Introduction

Financial metrics such as P/E ratios, price to cash flow ratios, PEG ratios, price to sales ratios, price to book value, and many others, should be thought of as tools in the investor’s toolbox. They can all be useful when appropriately utilized towards putting together a successful stock portfolio. However, just as you wouldn’t be able to build a house with only a hammer or a saw, this same logic applies to building a portfolio. Any task is made easier when you have the proper tools at your disposal and when you use them appropriately. You wouldn’t try to pound a nail with a saw or try to beat a board in half with a hammer. You would use the hammer for the nail and a saw to cut the board.

PEG Ratio: Definitions

Proponents of the PEG ratio allege that it is superior to the P/E ratio as a valuation metric because the P/E ratio does not take the company’s earnings growth into consideration. To an extent, I tend to agree with that assertion. On the other hand, I personally never utilize the P/E ratio without simultaneously considering a company’s earnings growth past, present and future potential. But most importantly, not all proponents of the PEG ratio define it exactly alike. Here are several definitions that illustrate my point:

Courtesy of INVESTOPEDIA here is one definition of the price/earnings to growth ratio or PEG ratio:

“What is the 'Price/Earnings To Growth - PEG Ratio'

The price/earnings to growth ratio (PEG ratio) is a stock's price-to-earnings (P/E) ratio divided by the growth rate of its earnings for a specified time period. The PEG ratio is used to determine a stock's value while taking the company's earnings growth into account, and is considered to provide a more complete picture than the P/E ratio.

According to this definition a lower ratio indicates a cheaper stock and a higher ratio indicates a more expensive stock. The equilibrium PEG ratio would be one where earnings growth and the current P/E ratio are equal.”

Although this is a reasonable definition of the PEG ratio, I find it somewhat vague regarding the specified time period. Are they talking about past earnings growth or future earnings growth? And if they are talking about future earnings growth, what timeframe are they utilizing?

Wikipedia offers a similar but perhaps slightly more precise definition because it specifies expected earnings growth over historical growth. Nevertheless, this definition still does not speak directly to how far into the future forecasting growth should be calculated.

“The PEG ratio (price-earnings to growth ratio) is a valuation metric for determining the relative trade-off between the price of a stock, the earnings generated per share (EPS), and the company's expected growth.

In general, the P/E ratio is higher for a company with a higher growth rate. Thus using just the P/E ratio would make high-growth companies appear overvalued relative to others. It is assumed that by dividing the P/E ratio by the earnings growth rate, the resulting ratio is better for comparing companies with different growth rates.”

The website Nasdaq provides a definition that is slightly more specific alleging that the PEG ratio is based on consensus estimates for earnings over the next 12 months as follows:

“PEG Ratio

The PEG ratio is the Price Earnings ratio divided by the growth rate. The forecasted growth rate (based on the consensus of professional analysts) and the forecasted earnings over the next 12 months are used to calculate the PEG.”

The blog “Inside Investing” produced by the CFA Institute produced an interesting read on August 16, 2012 titled “Is It Overvalued? Look at the PEG Ratio. Here is a link to the full blog and a short excerpt with a second link that is appropriate to this series of articles:

“We discussed the P/E and why it is a good measure of the relative valuation of two companies in a previous post here. One of the major drawbacks of this valuation measure, however, is the static nature of the analysis it provides. If you’re thinking that sounds a bit wonky, you’re right, it does. OK, it sounds really wonky! Geez.

What I mean by “static nature” is that the P/E really just looks at valuation at one point in time, like a snapshot of the two companies at that moment. One of the things that comparing the P/Es of two companies fails to take into account is the respective growth rates of each of the companies—in other words, how much each company will earn next year compared with what it earned this year.”

What I’m suggesting by sharing these various definitions is that the PEG ratio is not universally calculated. Consequently, when you are seeing the PEG ratio reported on various financial websites, it’s important to know precisely what timeframe is used to estimate the earnings growth rate. Sometimes it will be 1 year forward, sometimes it will be 5 years forward (this timeframe might be the most common) and sometimes historical earnings growth will be utilized. Therefore, I caution the reader that utilizes the PEG ratio to be sure they understand what earnings growth rate is being utilized.

The Origin of the PEG Ratio

The origin of the PEG ratio was originally attributed to the author Mario Farina who wrote about it in his 1969 book, “A Beginner’s Guide To Successful Investing In The Stock Market.” However, the popularity of the PEG ratio is primarily credited to Peter Lynch based on his 1989 best-selling book “One Up On Wall Street.” However, Peter Lynch did not specifically talk about the PEG ratio as it is widely used today. On the other hand, he did essentially describe and establish a ratio based on P/Es and growth rates. Here are a few excerpts of what Peter actually said on pages 198 and 199:

“The P/E ratio of any company that’s fairly priced will equal its growth rate. I’m talking about growth rate of earnings here.”

Then a few paragraphs down he introduced the concept and described it as a ratio of sorts as follows:

“In general, a P/E ratio that’s half the growth rate is very positive, and one that’s twice the growth rate is very negative. We use this measure all the time in analyzing stocks for the mutual funds.”

However, and here is the interesting part. Most practitioners and devotees of the PEG ratio today base their calculation on an estimate of a company’s future 5-year earnings growth rate. But, Peter Lynch was not recommending that the ratio be based on forward earnings growth. Instead, he suggested utilizing historical earnings growth. Here are his exact words from the next paragraph in the book:

“If your broker can’t give you a company’s growth rate, you can figure it out for yourself by taking the annual earnings from Value Line or an S&P report and calculating the percent increase in earnings from one year to the next. That way, you’ll end up with another measure of whether a stock is or is not too pricey. As to the all-important future growth rate, your guess is as good as mine.”

As I will discuss in more detail later, the PEG ratio is most appropriate for valuing high-growth stocks. Additionally, there are those that suggest that the PEG ratio is best applied to stocks that do not pay dividends because it does not incorporate income received in its valuation calculation. Consequently, there are those that suggest using a modified version of the PEG ratio through adding the dividend yield to the estimated growth rate (PEGY ratio).

The reason I bring this up is because Peter Lynch also had a view on utilizing a modified version of the PEG ratio (PEGY ratio) for dividend paying stocks. However, he actually suggested a calculation that turns the current PEG ratio calculation upside down.

As described above, the standard PEG ratio formula is expressed as the price earnings ratio divided by the annual earnings growth rate (P/E divided by EPS Growth). Peter Lynch suggested adding the dividend yield to the earnings growth rate and dividing that by the P/E ratio. With Peter’s version a higher ratio is better than a lower ratio, which is the exact opposite of how the PEG ratio is used today. Here are his exact words:

“A slightly more complicated formula enables us to compare growth rates to earnings, while also taking the dividends into account. Find the long-term growth rate (say, company X’s is 12%), add the dividend yield (company X pays 3%), and divide by the P/E ratio (company X’s is 10). 12+ 3÷10 is 1.5.

Less than a 1 is poor, and 1.5 is okay, but what you’re really looking for is a 2 or better. A company with a 15% growth rate, a 3% dividend, and a P/E of 6 would have a fabulous 3.”

In conclusion, if the PEG ratio was truly attributed to Peter Lynch as many suggest, then the way it is commonly used today is an upside down version of what Peter Lynch was actually suggesting. Peter Lynch’s version of the PEG ratio would be Annual EPS growth divided by the P/E ratio.

The Risk of Estimating Future Earnings

One benefit of the P/E ratio over the PEG ratio is that the P/E ratio is a more precise calculation. It is more precise because it is typically calculated based on specific reported earnings. However, it is not perfectly precise either. Some P/E ratio calculations are based on trailing 12 month data (ttm), however, that level of earnings is not perfectly precise. In other words, every company is continuing to generate earnings at some level after the last quarter has been reported. Companies only report earnings quarterly, and the earnings report doesn’t typically come out until approximately 45 days after the actual quarter has closed.

At other times, the P/E ratio is calculated utilizing forward earnings. This calculation of the P/E ratio relates more closely to the PEG ratio because forward earnings growth is built into the calculation. Nevertheless, calculations based on a forward estimate of earnings might hopefully be close, but again, not precise. The F.A.S.T. Graphs™ research tool that I will be showing later in this article utilizes a blended P/E ratio calculation. This calculation is based on past, current and the closest forward forecast. Again, it is not perfectly precise, but does tend to average out the difference between past and forecast earnings.

The bottom line is that all calculations based on earnings (or any other metric for that matter) are never perfectly accurate for the reasons stated above. On the other hand, these types of calculations should all be thought of as guidelines within reasonable ranges of accuracy and/or probability.

With these thoughts in mind, one of the biggest criticisms of the utilization of the PEG ratio is the reality that the forecast earnings growth utilized in the calculation could be wrong, and sometimes significantly so. For example, I received the following comment from a reader on part 1 of this series that sums it up nicely:

“Basically this. I can't even count the number of people I've seen cutting down Wall Street analysts as idiots, but then are perfectly happy to cite PEG ratios on their holdings as a reason to keep owning.”

My own view on the matter is that all investing in stocks is done in future time. Consequently, the accuracy of earnings forecasts is an unavoidable risk no matter if they are done by analysts or the individual investor themselves. Nevertheless, since we can only invest in the future, earnings estimates are an unavoidable part of a rational investment decision. My college professor and original mentor put it so eloquently as follows:

“As investors we cannot escape the obligation to forecast- our results depend on it. Our forecasts are not prophecy. We should not merely guess or play hunches. We should calculate reasonable probabilities based on all the factual information that we can assemble. We should then apply analytical methods that are employed based on our underlying earnings driven rationale, providing us reasons to believe that the relationships producing earnings growth will persist in the future.”

Therefore, I contend that criticizing the PEG ratio because it incorporates earnings estimates is a two-edged sword. On the one hand, those utilizing this metric should be consciously aware that the denominator (earnings growth rate) might be completely off the mark. On the other hand, since we can only invest in the future, we are obligated to incorporate forecasting within our decision making process.

In part 1 of this two-part series found here a reader and advocate of the PEG ratio provided some interesting insights and reasons supporting its use. The whole comment is over 600 words long, therefore, I have simply listed the 5 major points he offered followed by his concluding remarks. His whole comment can be found by following the above link.

“BeatlesRockerTom

Juzt,

Critical point, and easily overlooked, re trend of the PEG.

1) I see PE as kind of like a given day's temp. Ex. In August it may be 95 and in late Jan it may be 5 degrees. (Northern hemisphere, for readers south of the equator).

2) a PEG ratio depends on a future growth estimate. A PE alone is incomplete info because it does not provide sufficient information regarding where the company's earnings are headed.

3) Using the PEG ratio provides info that a PE alone does not.

4) G, growth, is an estimate of the future, hence cannot be precisely known.

5) The PEG for a company can change over time by changes in the growth estimate and the PE. The relative change in growth over time matters.

I respect those who dismiss the PEG. We each have the right to choose what we feel is best for us. I prefer to use PEG to compare investments, accepting its imprecision, than to not. Investing in stocks inherently accepts the risk of investing for but not being able to predict future growth of returns exactly, in return for the potential to earn more than a CD. PEG gives some information you don't have in its absence, accepting its imprecision. Assessing the growth trends- the PEG trend- over time provides even more info.”

In my response to the above comment, I promised that I would address his points more fully in this article. Here is my exact response:

“Tom,

Thanks for sharing your perspectives. I will be addressing many of the points you bring up more fully in part 2 where I cover the PEG ratio specifically. Although I do not specifically disagree with most of your points, I do approach the implementation of growth differently. I do agree that it is an important consideration. However, I do not feel that the PEG ratio specifically addresses those considerations. I will try to explain that more fully in part 2.

Regards,

Chuck”

Growth stocks: Best use of the Peg Ratio

Personally, I do consider the PEG ratio a very valuable valuation metric - but only for growth stocks. As indicated in part 1, I like the P/E ratio of 15 as a standard baseline valuation reference on most companies. However, very fast-growing companies (earnings growth above 15%) are clearly worth more than their slower-growing counterparts due to the power of compounding.

As I suggested earlier, as investors in common stocks we can only invest in the future. Simply stated, this implies that we are truly buying future earnings.

The Power and Protection of High Compounding Earnings Growth

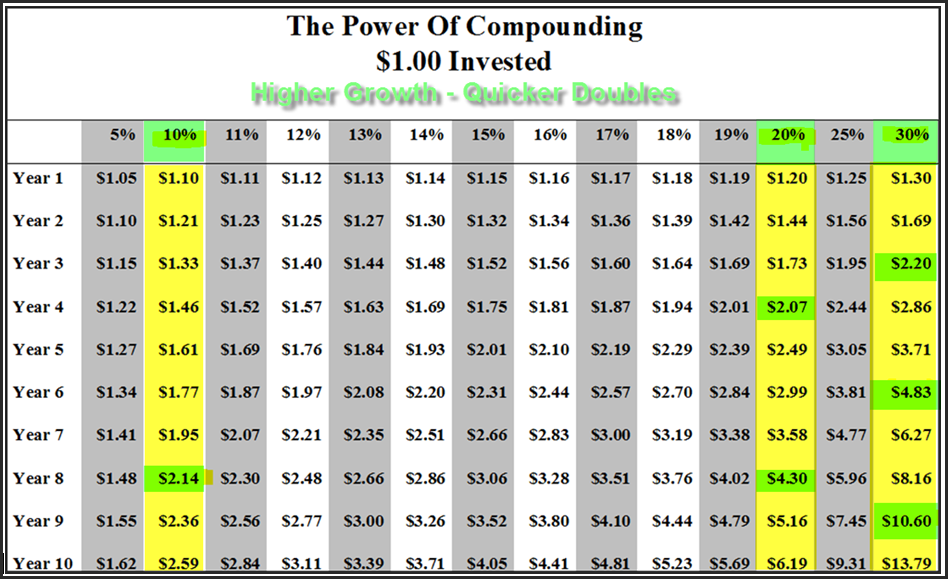

The review of a simple compounding table illustrates my points better than words. What actually happens as a result of faster earnings growth is that it shortens the time it takes to double earnings. Therefore, the following compounding table illustrates how an original $1.00 worth of earnings that are purchased today will double more often over a 10-year timeframe when earnings growth is higher. The tipping point becomes rather dramatic at 15% per annum or better.

People that do not understand the powerful force of compounding will often mistakenly assume that a 20% growth rate will produce twice as much future earnings as a 10% growth rate. However, compounding is more about geometry than it is simple mathematics. From the table below, note that $1.00 invested today that grows by 10% per annum does not double until the 8th year. In contrast, $1.00 invested at 20% doubles in the 4th year, and then again in the 8th year. Therefore, doubling the growth rate from 10% to 20% doubles the number of doubles on your earnings in 10 years. This compounding effect is even more dramatic when you look at what happens with various growth rates by the 10th year.

Increase the growth rate to 30%, and that first dollar will double 3 times instead of only once. Consequently, it is easy to understand why Albert Einstein said: "Compound interest is the eighth wonder of the world. He who understands it, earns it ... he who doesn't ... pays it." Compounding is the power; and the higher level of earnings it produces is the protection that high-growth stocks can provide. However, earning high rates of earnings growth over an extended period of time is quite difficult. Few companies are capable of achieving high earnings growth, and therein resides the risk of growth stock investing.

Growth Stocks and the PEG Ratio

When I originally designed the F.A.S.T. Graphs™ fundamentals analyzer software tool, the first formula I implemented was Peter Lynch’s P/E ratio equal to earnings growth rate. As it relates to the commonly utilized PEG ratio, this formula produces a valuation reference line (the orange line) as a PEG ratio of 1. In other words, when I’m looking at growth stocks, I draw a PEG ratio of 1 across the entire graph. So although I in essence utilize the PEG ratio, I use it differently than simply viewing it as a statistic.

I am not a fan of statistics per se; instead, I prefer dynamic models that allow me to evaluate valuation ratios over numerous timeframes. Furthermore, I implement and analyze my version (P/E = EPS growth rate) based on historical earnings growth as Peter Lynch did, and I apply it to future earnings growth as it is commonly utilized today. In my opinion, I consider this a more comprehensive utilization of the metric.

The PEG Ratio-Real-Life Examples

The primary reason that I use any valuation metric is to help me make reasonable and sound buy, sell or hold decisions for my stock portfolios. In this respect, my application of valuation methodologies is practical rather than philosophical. In short, I am not interested in debating what valuation metric is the best. Rather, I am interested in any valuation metric that can assist me towards making intelligent decisions under real-world applications.

For fast-growing companies (true growth stocks) I have found that the PEG ratio - when used appropriately - works quite well. Below are just a few examples to corroborate my thesis. On each historical graph the orange valuation reference line represents a PEG ratio of 1. A PEG ratio of 1 indicates that the P/E ratio of the orange line is equal to the company’s historical earnings growth rate.

As the reader reviews each of these graphs, take special notice of how the orange line represents a practical and sound valuation reference. However, the reader should also note that when growth is as fast as found in the following examples, you cannot really overpay to invest in any of them if you hold it long enough. The power of compounding at high rates of growth is truly powerful.

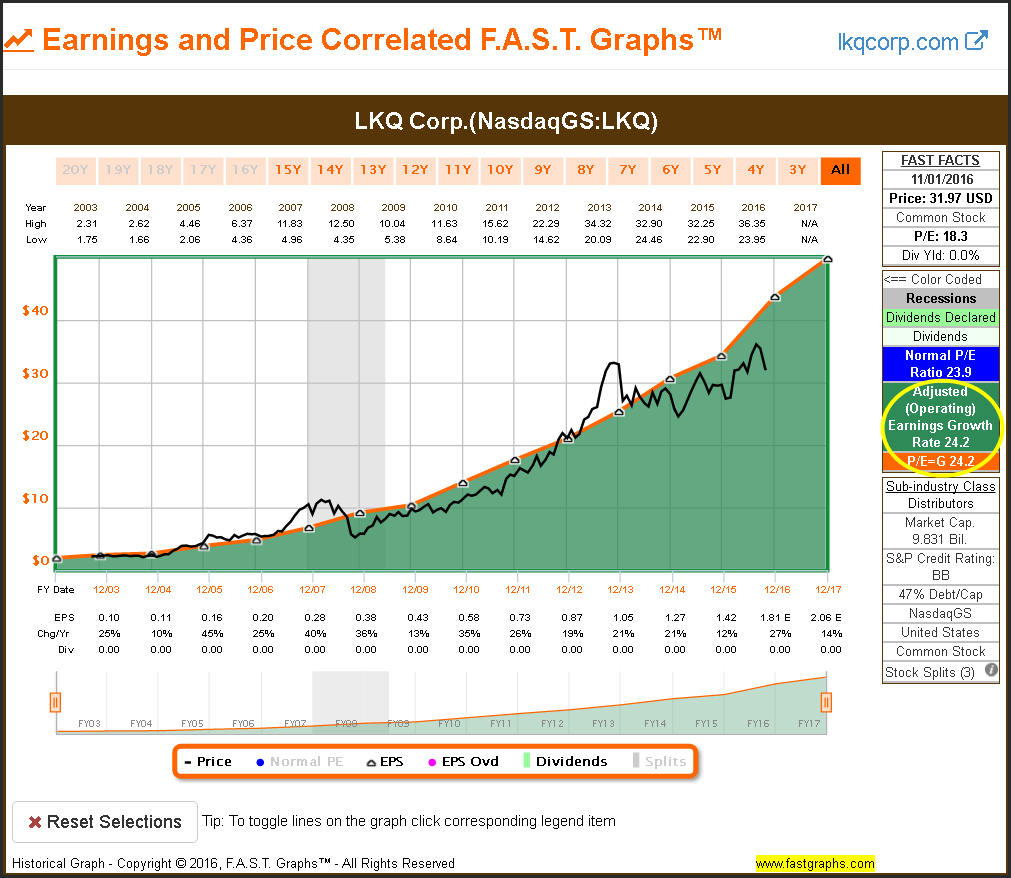

LKQ Corp. (LKQ)

LKQ has achieved an earnings growth rate of 24.2% per annum since it went public. It is clear that a PEG ratio of 1 or a P/E ratio of 24.2 represented sound valuation. More importantly, stock price has tracked that valuation reference about as perfectly as you could expect.

However, when you view LKQ since the beginning of 2009, you discover that its earnings growth rate has somewhat slowed down to 20.7% per annum. This indicated a reset of the PEG of 1 to 20.7 from its previous 24.2 level on the longer-term graph. But most importantly, this represented a highly correlated valuation reference over this timeframe.

When evaluating LKQ based on forward estimates for the next 3 to 5 years, we still apply the P/E equal to earnings growth rate or PEG ratio of 1. However, future expectations have reset the PEG ratio of 1 to a P/E ratio of 17.67 based on expected earnings growth. Consequently, the current PEG ratio is 1.12 calculated by dividing the current indicated blended P/E ratio of 19.6 by the forecast growth rate of 17.67%. I like the visual better than I do the statistic.

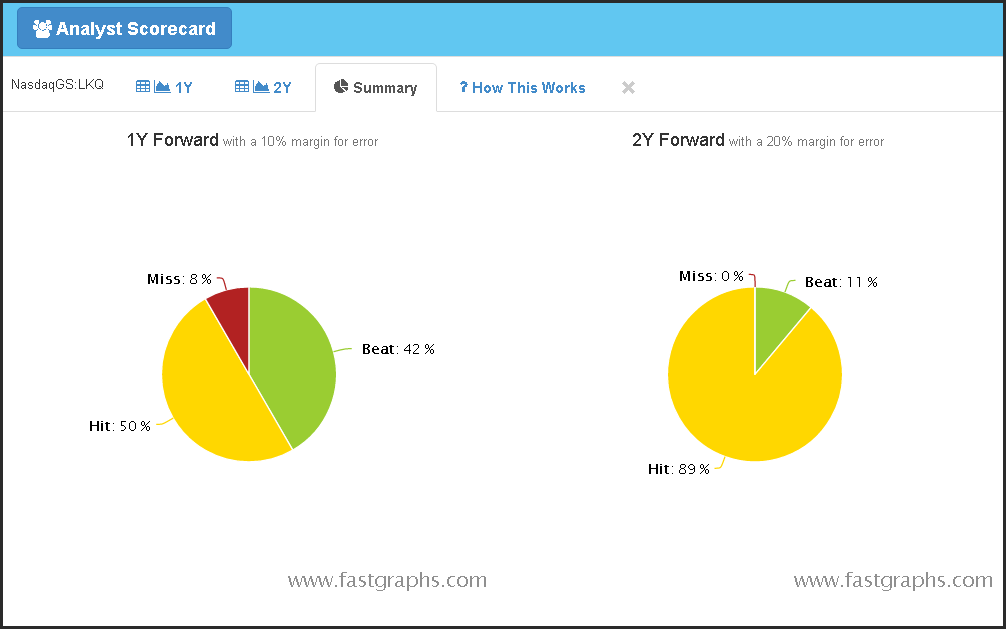

As previously stated, one of the biggest criticisms of the PEG ratio is that it is based on estimates of future growth. However, in the case of LKQ, analysts have amassed an excellent record of forecasting this company’s earnings within a reasonable range of error. Consequently, I have a high level of confidence that those forecasts could be within a reasonable range of accuracy. Therefore, I would consider this growth stock reasonably valued based on its attractive PEG ratio.

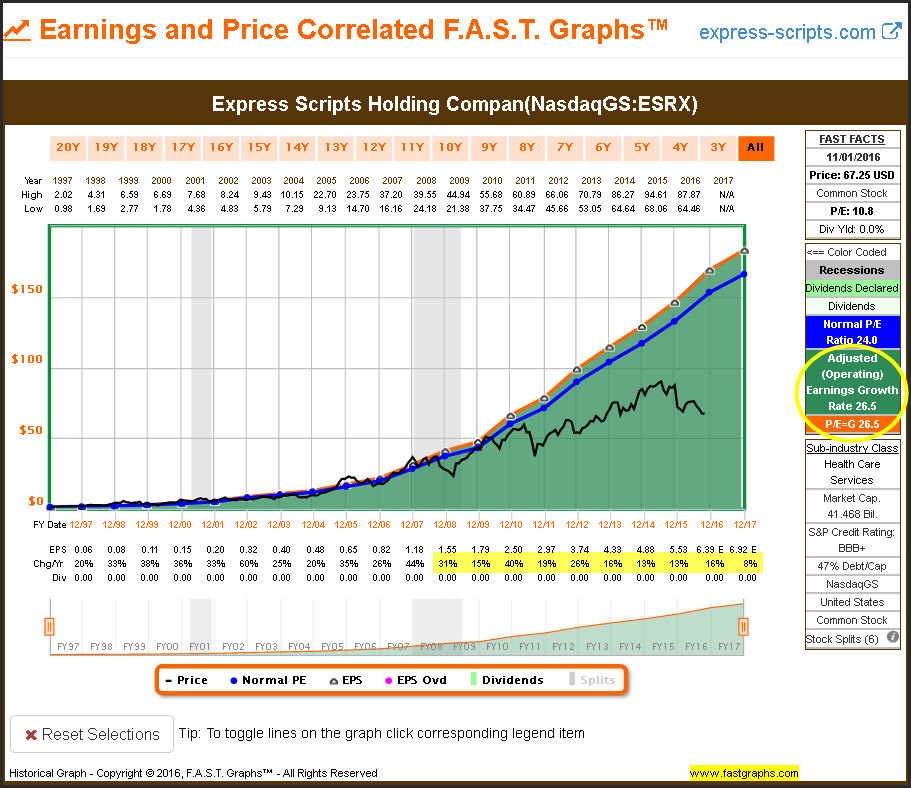

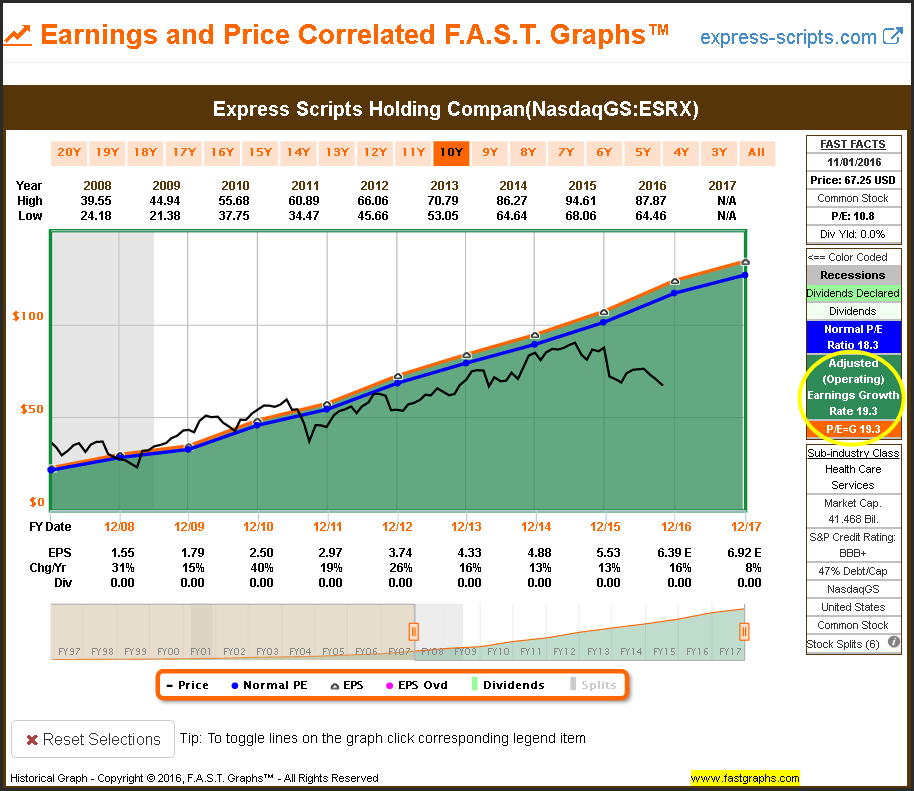

Express Scripts Holding Company (ESRX)

As I did with my first example, I will present Express Scripts over different historical timeframes in order to address the important point that a reader expressed in part 1 of this series as follows:

“5) The PEG for a company can change over time by changes in the growth estimate and the PE. The relative change in growth over time matters.”

Since 1997, Express Scripts produced an average annual growth rate of earnings of 26.5%. Up through the Great Recession this P/E ratio of 26.5 (PEG ratio of 1) represented a highly correlated valuation reference. However, since 2011 the market has clearly implied a lower valuation to the shares of Express Scripts.

Nevertheless, when we review the historical graph of Express Scripts since the Great Recession, we once again see a reset of the PEG ratio based on earnings growth slowing down to 19.3%. For the shorter timeframe, a PEG ratio of 1 (P/E ratio 19.3) produces a rational valuation reference for this timeframe.

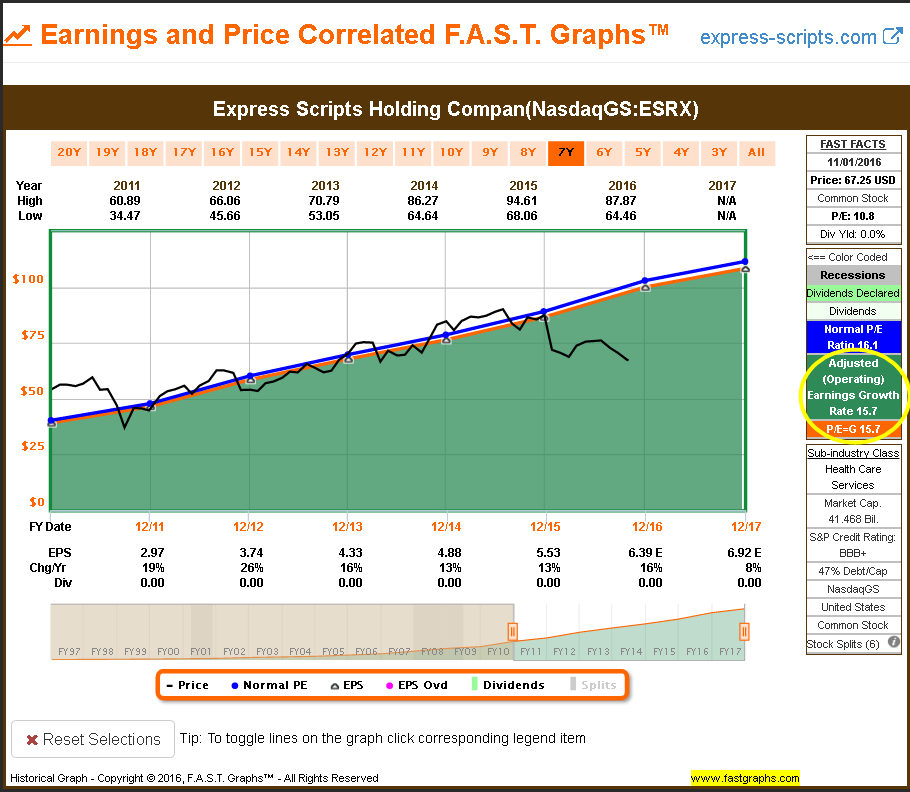

However, shortening the timeframe even more from 2011 to current we discover that average annual earnings growth has fallen to 15.7%. Since this is above 15%, we still utilize the formula P/E equal to earnings growth rate and draw the valuation reference line and a P/E of 15.7. Once again, the valuation reference is highly correlated to stock price over this even shorter timeframe.

I specifically chose this example because a reader mentioned it in the comment thread of part 1 of this series as follows: “Maybe, now, we should talk about Express Scripts!”

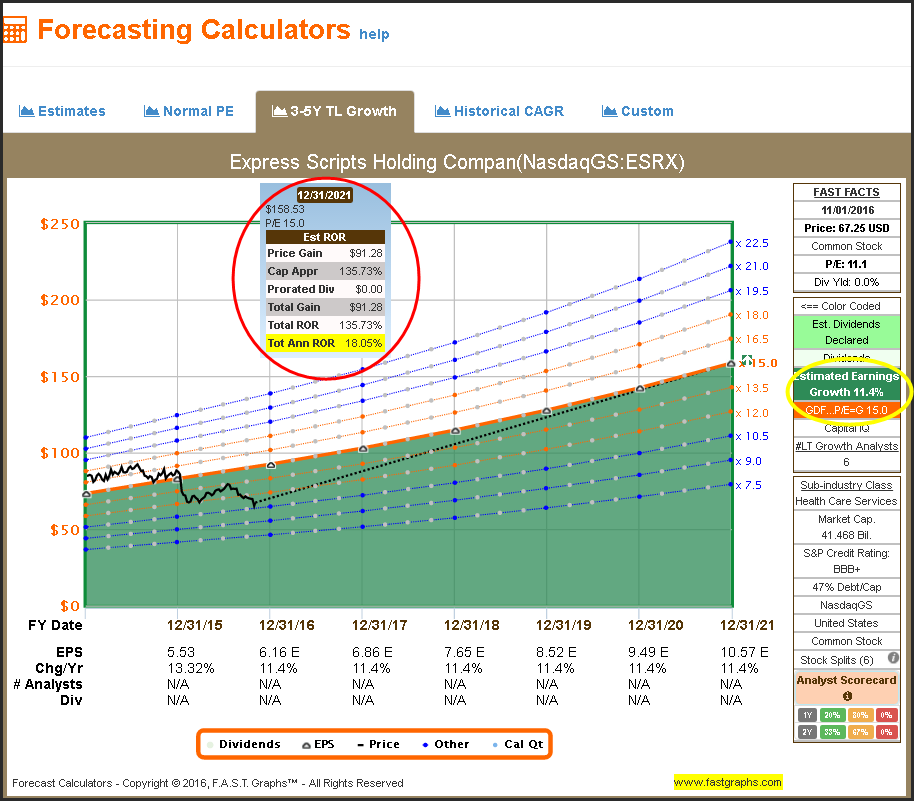

As earnings growth has clearly slowed down over time, it is even more relevant that it is expected to continue slowing down over the next 5 years to an estimated 3 to five-year earnings growth rate of 11.4%.

Since forecast earnings growth is now below 15%, I no longer utilize the P/E ratio equal to earnings growth rate is my valuation reference. Instead, the “Forecasting Calculator” is utilizing the traditional formula that more realistically applies to companies growing earnings at rates below 15%. However, as an interesting aside, Express Scripts is currently trading at a PEG ratio of approximately 1. The current blended P/E ratio is 11.1 and the forecast long-term earnings growth rate is forecast at 11.4%.

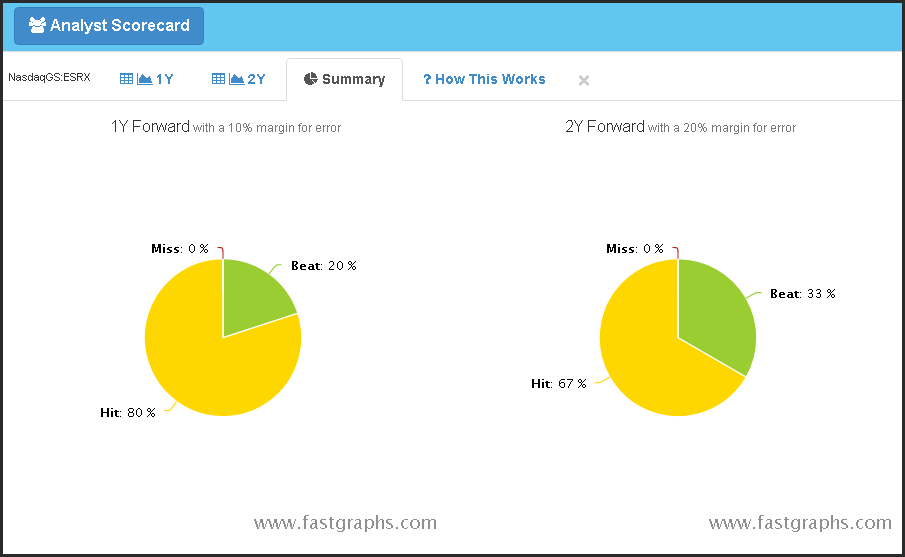

The following summary of the analysts’ record on accurately estimating earnings for Express Scripts has been extremely accurate. Although this doesn’t guarantee that the record will continue, it does engender a high level of confidence that they might be reasonably accurate.

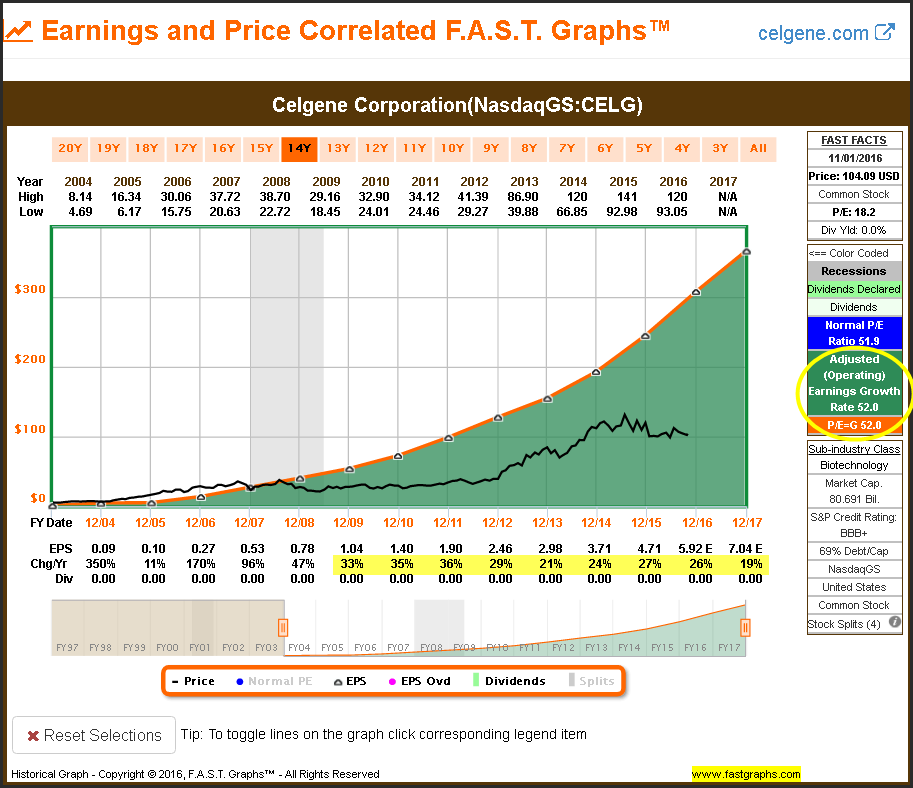

Celgene Corporation (CELG)

Celgene represents a second example of how the PEG ratio, just as it is with all ratios, should be thought of and recognized as a dynamic calculation. Just as I did with Express Scripts above, notice how the PEG changes and adjusts as a valuation reference when different timeframes are drawn.

The long-term graph on Celgene would present the illusion that the stock had become significantly undervalued since the Great Recession based on its long-term historical earnings growth rate of 52% per annum.

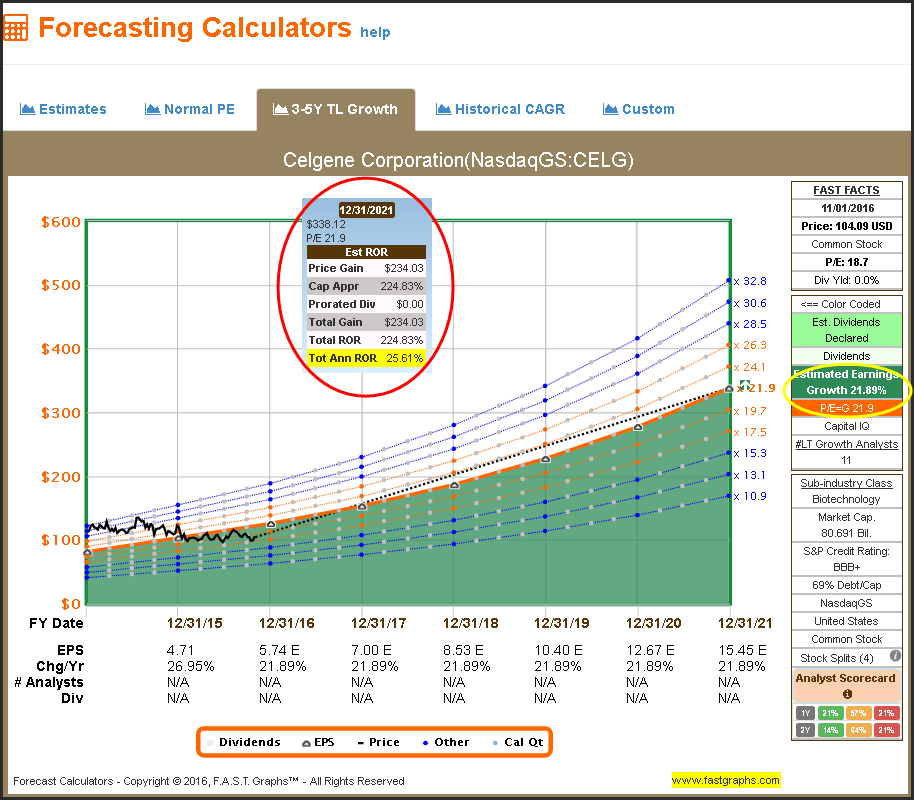

However, when we shorten the timeframe, we discover that earnings growth since the Great Recession is almost half as fast as it was in the long-term graph. When looked at from this perspective, valuation based on earnings growth of 27.7% per annum makes more sense.

When looking to the future as the PEG ratio is most commonly used, the earnings growth rate utilized to calculate a forward PEG ratio has been reduced to 21.89%. Using this number, the PEG ratio for Celgene would be considered attractive with a PEG ratio of .84 (less than one).

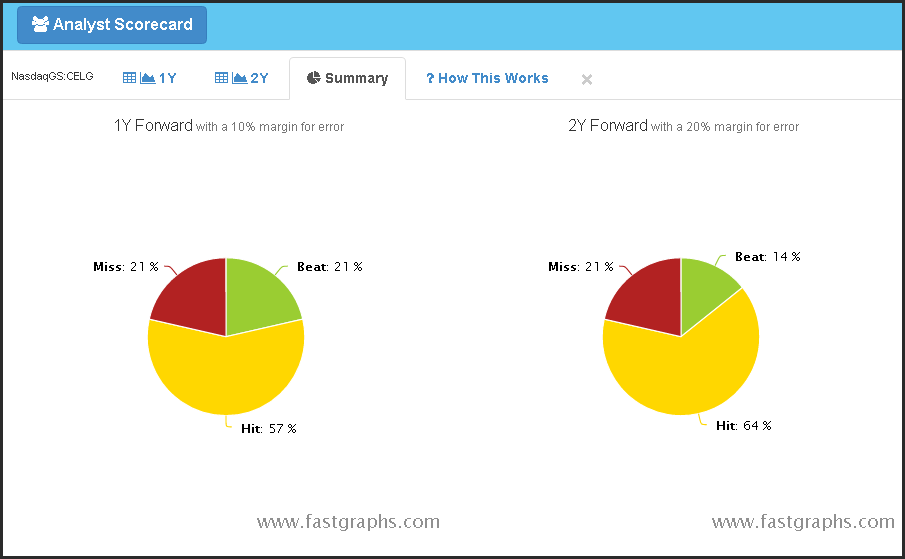

Although analyst estimates for this company have been reasonably accurate historically, they have been wrong approximately 21% of the time.

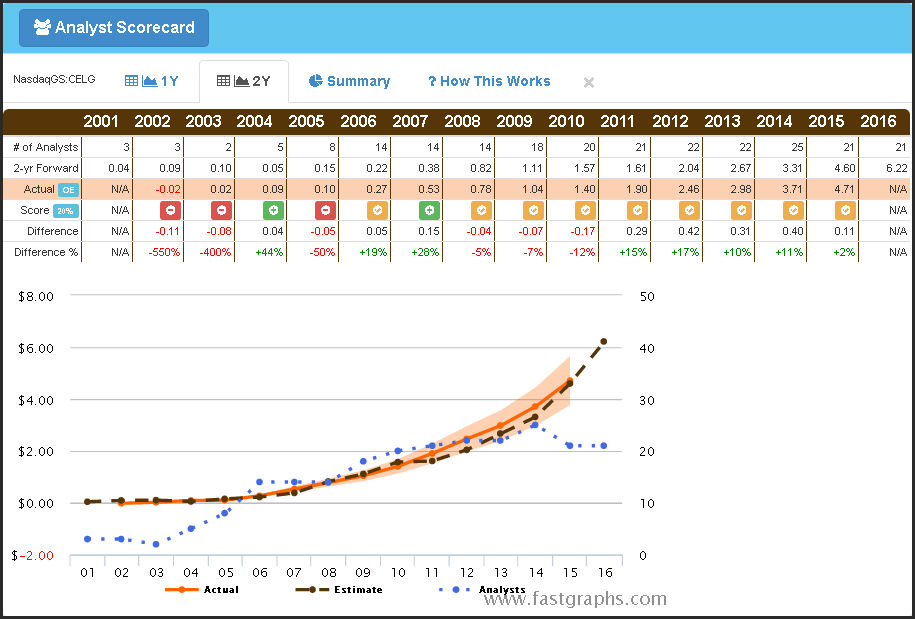

On the other hand, a more detailed look at the analysts’ record shows that analysts’ forecasts since 2006 have been extremely accurate. It is also interesting to note that the number of analysts providing estimates to S&P Capital IQ have increased over this timeframe.

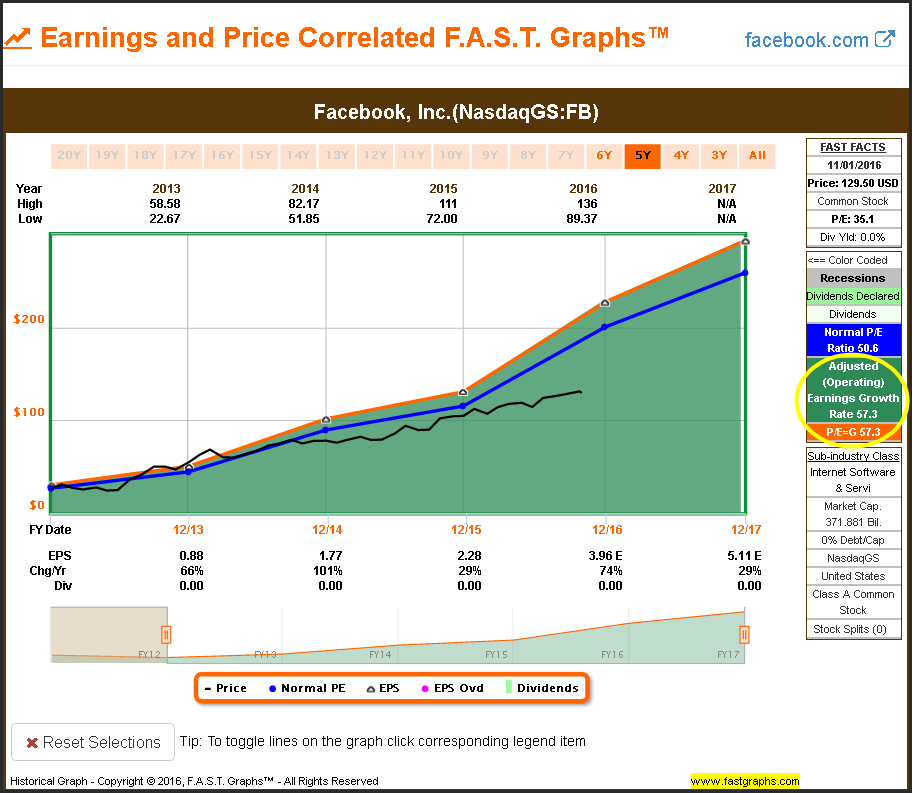

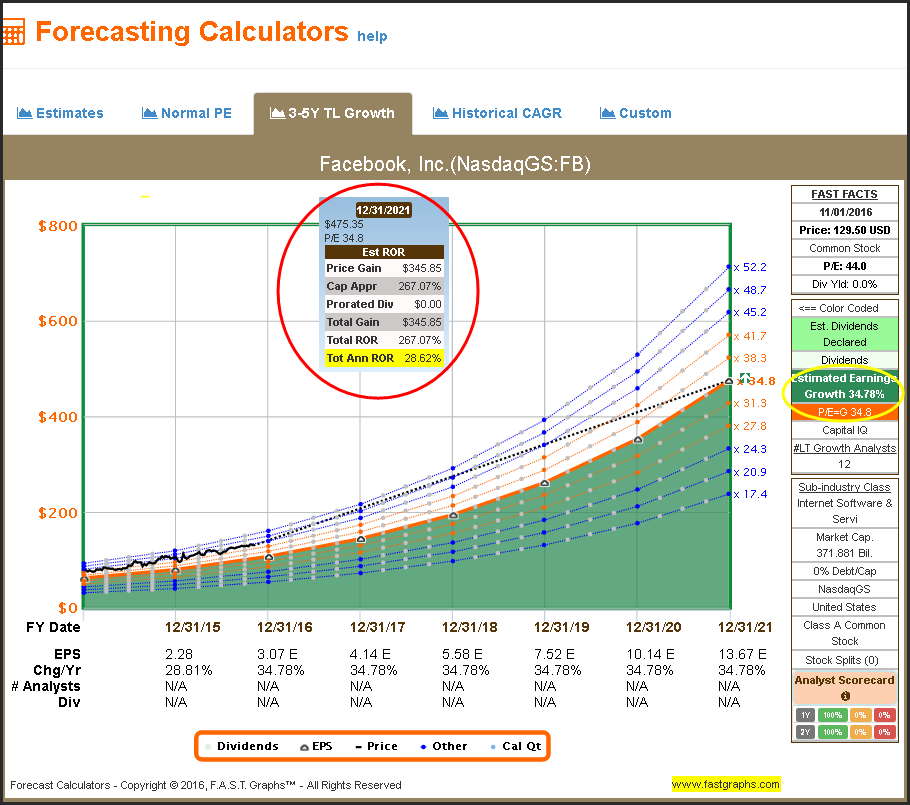

Facebook, Inc. (FB)

My final example looks at Facebook from the perspective of the PEG ratio as a valuation metric. Historical earnings growth has been remarkably high averaging 57.3% per annum.

However, Facebook is already a company with a market cap in excess of $376 billion. Consequently, it seems logical that forecast growth going forward has been reduced to 34.78%. On the other hand, that is still an exceptionally high forecast growth rate for such a large company. Nevertheless, based on the current blended P/E ratio of 44 and forecast earnings growth of 34.78%, Facebook’s PEG ratio would be considered reasonable at approximately 1.28.

Summary and Conclusions

Financial ratios such as P/E ratios, PEG ratios, price to cash flow ratios, price to sales ratios, price to book ratios and all other ratios should be thought of as tools in the investor’s toolbox. However, I believe that none of them should be viewed in a vacuum, nor do I believe they should be thought of as a simple statistic. Instead, investors should understand that these ratios are dynamic and can - and do - change over time. Consequently, I like to utilize all of these metrics in a relative manner. This implies examining each metric past, present and future.

Finally, I don’t believe there is one best valuation metric to utilize. Instead, I believe more insights are gained by examining as many valuation ratios as you can. At the end of the day, the objective is to try to ascertain whether or not a current investment in a given stock is rational and/or sound. Investors are best served by utilizing all of the available tools at their disposal. However, the tools must be practically and appropriately applied to be of true value. Most importantly, financial ratios and metrics should only be the precursor to a more comprehensive research and due diligence effort before your money is invested.

Disclosure: Long FB,LKQ,ESRX

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs

© F.A.S.T. Graphs

Read more commentaries by F.A.S.T. Graphs