Introduction

Recently, I have been engaged in rather intense discussions regarding the validity of P/E ratios versus PEG ratios as proper or appropriate valuation metrics. I generally find these types of debates befuddling for a couple of reasons. One, they are often a result of a failure to communicate. Either party or sometimes both parties assume that their adversary holds or supports a specific position which may or may not be a fact.

From my perspective, this was precisely the case regarding the discussion cited in my opening sentence. Assumptions were made regarding my positions on P/E ratios and the PEG ratio that were not positions that I actually hold. Consequently, it is hard to argue or debate an issue when you are essentially being required to defend a position that you do not hold.

The second reason I find these types of discussions puzzling is because they are often over generalized. Financial metrics such as the P/E ratio or the PEG ratio, like most financial metrics, have their place and their value in financial analysis. Consider that a P/E ratio is a statistical metric referencing a single point in time.

However, in the real world, the P/E ratio is a dynamic measurement that is constantly changing over time. Moreover, just as it is with all financial metrics, I don’t believe any metric is supremely valuable in a vacuum. In my experience and opinion, all financial metrics will only bring investors value and insight when utilized relative to other metrics.

Therefore, with this series of articles I will share my perspectives, opinions and insights into how both the P/E ratio and the PEG ratio can be appropriately utilized by investors towards making better informed investment decisions on common stocks. Additionally, I will discuss how both of these commonly used financial metrics are for all intents and purposes joined at the hip. In other words, they are more interrelated metrics than they are separate or distinct valuation tools.

The P/E Ratio: Definitions and Insights

The P/E ratio is one of the most commonly utilized tools for the serious common stock investor. It is, however, one of the most misunderstood and misused tools. Learning how to use it properly and understanding its significance can significantly increase returns and lower risk.

The P/E Ratio - Definitions:

The P/E Ratio can be defined in several ways, with each definition adding insight to its significance. The simplest definition is simply the price of the common stock divided by its earnings per share. This is a basic mathematical definition expressed as follows: PRICE/Earnings = P/E Ratio.

A second commonly used definition is: The P/E Ratio is the price you pay to buy $1.00 worth of a company's earnings or profits. For example, if a company's stock has a P/E Ratio of 10, then you must pay $10 for every dollar's worth of that company's earnings or profits you buy. If its P/E Ratio is 20, then you pay $20 for every dollar's worth of that company's earnings or profits, and so on.

It is important to note, however, that a higher P/E Ratio does not necessarily mean that the company has a higher valuation or that it is more expensive than a company with a lower P/E Ratio. This fact is not understood by many investors and is the key reason that the P/E Ratio has little value by itself or if used in a vacuum. It is theoretically possible, depending on each company's future prospects, that a company with a P/E Ratio of 10, for example, can be significantly more expensive than a company with a P/E Ratio of 40. I will elaborate on this important point later.

A third definition would be: How many years in advance you are paying for this year's earnings. For example, if a company has a P/E Ratio of 20, then you are paying 20 times this year's earnings. If the P/E Ratio is 10, you are paying 10 times this year's earnings, and so on. This definition illustrates a simple premise of what an operating business is worth.

What is a Fair Value P/E Ratio?

As an example to illustrate this important point, I offer the following analogy based on the earnings of a private business. If you had a private business that was netting you $100,000 net, net, net after all expenses and taxes, it is unlikely that you would sell it to me for $100,000, or a P/E Ratio of 1.

A business that generates an annual revenue stream for its owner has a value greater than one year's profits. This is true even if the company is not growing or not growing very fast. For example, let’s assume that the above private company does not grow, but that it does pay a consistent $100,000 per year of net income. If the owner sold it for one times earnings ($100,000) he or she would essentially have no money coming in after the end of the first year.

So this raises the question, what value should an owner place on a business they are desirous of selling? The optimum value would be to sell the business for a price where the net proceeds could be invested in order to generate a comparable income stream.

Note: since this is being offered as a theoretical mathematical exercise, I will assume no taxes or other costs associated with a sale. Therefore, for illustration purposes, let’s assume the owner was confident that he or she could earn a reasonable 6.67% return on their proceeds from the sale of the business. If this were true, the owner would need approximately $1,500,000 net after taxes earning 6.67% ($1,500,000 x 6.67% equals $100,050) in order to replace the $100,000 per year they were receiving from their business. In other words, this valuation represents a P/E ratio of 15.

From the purchaser’s perspective, if they paid $1,500,000 for the example business (the P/E ratio of 15), he or she in turn would be receiving a current earnings yield of 6.67%. Earnings yield (E/P) is the inverse of the P/E ratio. Since the average rate of return from common stocks has ranged between 6% - 8% historically, a 6.67% expected current return might be considered reasonable by both the seller and buyer. If this were true, then this transaction theoretically benefits both buyer and seller and could be consummated.

This exercise establishes the P/E ratio of 15 as a baseline or rational valuation level from both a buyer’s and a seller’s perspective. This does not suggest that it is a perfect calculation of fair value, intrinsic value or true worth. Instead, a P/E ratio of 15 represents a sound valuation level that a business generating an income stream is worth, even if the business isn’t growing. However, this valuation level is only relevant if the business is generating a positive level of earnings. Therefore, I suggest that the reader might consider a P/E ratio of 15 as a benchmark for a sound valuation reference for average growing companies.

Moreover, a P/E ratio of 15 as a sound valuation reference is useful for most companies when their earnings growth is 15% or less. There are many investors that find this last statement either illogical or hard to accept. However, in my experience analyzing thousands of companies over many decades, the 15 P/E ratio as a valuation reference is fully supported in real-world circumstances. In my opinion, this speaks loudly to my earlier point that the P/E ratio cannot be utilized in a vacuum. Furthermore, a sound valuation does not in itself guarantee a high level of future returns.

In order to ascertain future return potential, I believe the P/E ratio needs to be evaluated in relation to the earnings growth potential of the company in question. A 15 P/E ratio represents soundness as illustrated in my private company example above. However, it is the P/E ratio in relation to the company’s earnings growth rate that will produce future capital appreciation and dividend income growth, if a company pays a dividend.

Sound valuation is primarily a measurement of risk associated with making a purchase of a common stock. However, from a total return point of view, it is a relative metric that is best evaluated in conjunction with earnings growth. Nevertheless, the proof is in the pudding as they say. Therefore, I offer the following F.A.S.T. Graphs™ where I review several prominent well-known stocks in relation to the 15 P/E ratio as a standard valuation reference. I will start out with the S&P 500, followed by several companies with various earnings growth rates. The company examples are offered in order of lowest earnings growth rates to highest.

The 15 P/E Ratio As A Standard Valuation Reference

In order to illustrate the validity of a 15 P/E ratio as a benchmark valuation reference, even over different earnings growth rates, I offer the following simplified graphs. There are only three lines on each graph. The bright pink line represents a P/E ratio of 15 across the entire graph. The dark blue line represents a calculated normal P/E ratio for each example. There is no dividend information included in these graphs because the exercise is designed to evaluate valuation based on earnings as represented by the price-to-earnings ratio. Finally, the black line plots monthly closing stock prices over the timeframe graphed.

What I am asking the reader to notice is how the price line relates to the 15 P/E ratio benchmark over time. There are times when the price will be above the 15 P/E ratio benchmark, and times when the price will be below it. However, a close examination of each graph should clearly illustrate the validity of the 15 P/E ratio benchmark. It is obviously not a perfect relationship; however, it should be clear that the 15 P/E ratio represents a valid valuation benchmark on each example.

There is another important takeaway that I would like to focus the reader’s attention on. The 15 P/E ratio benchmark clearly illustrates sound valuation. However, the slope of each line is equal to the respective growth rate of each example. Therefore, even though sound valuation is indicated by the same 15 P/E ratio, long-term price action is determined by the growth rate of each company (the slope of the line).

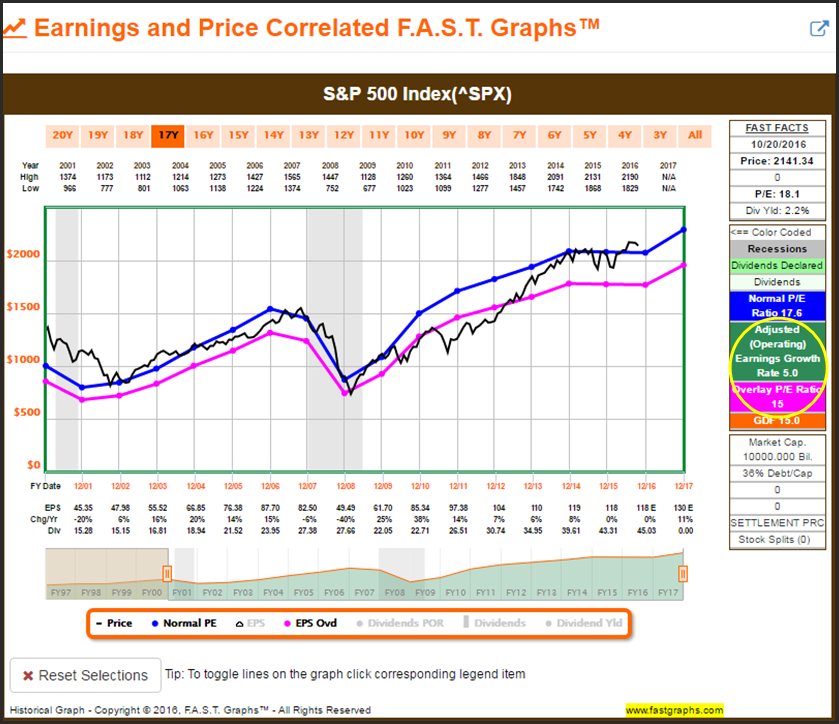

S&P 500 Index

When reviewing the overall stock market as represented by the S&P 500 index, we discover a valuation range between a P/E ratio of 15, and the normal P/E ratio of 17.6. Additionally, we see that the average earnings growth rate of the S&P 500 since 2001 has been 5% per annum. Nevertheless, the monthly closing stock prices of the S&P 500 correlate very closely to where earnings have gone. More importantly, we see that having the discipline to invest in the S&P 500 when its P/E ratio was at or below the 15 P/E ratio benchmark represented optimum investment opportunities in the index.

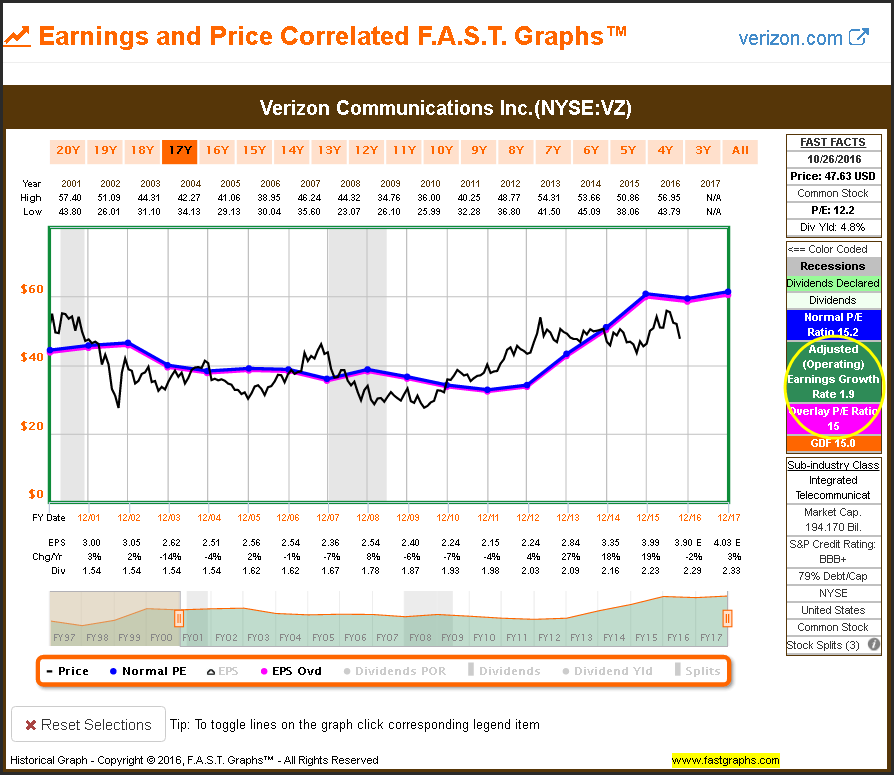

Verizon communications Inc. (VZ)

Verizon has the lowest earnings growth rate of any of the samples I will be presenting. Since 2001 Verizon’s average earnings growth rate has been 1.9%. Nevertheless, the validity of the 15 P/E ratio as a fair valuation reference is clear. Whenever price gets above that valuation reference it moves back into alignment and vice versa.

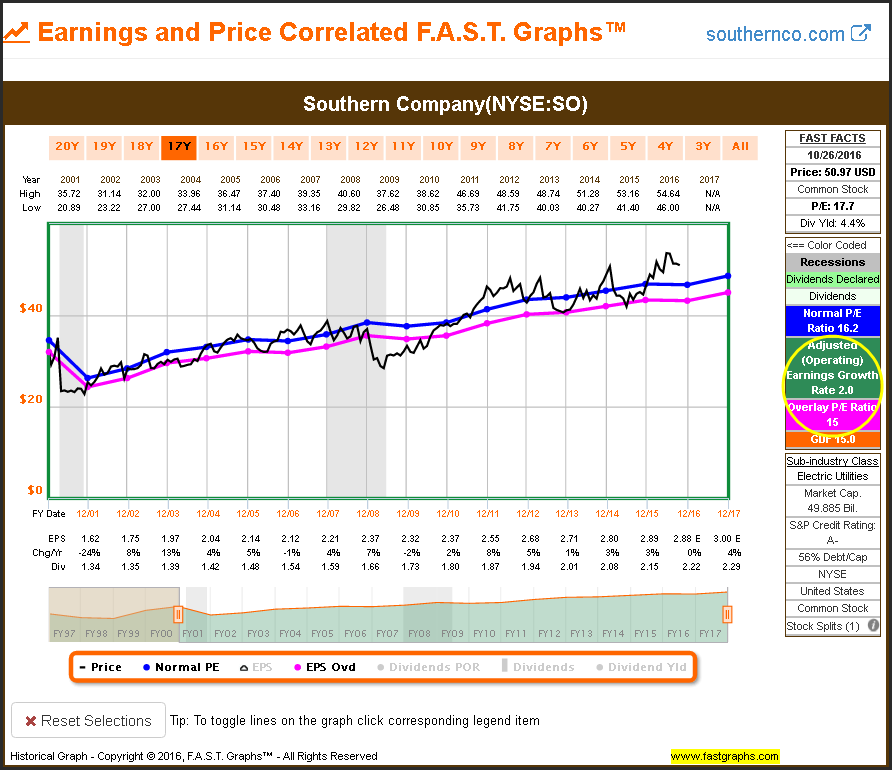

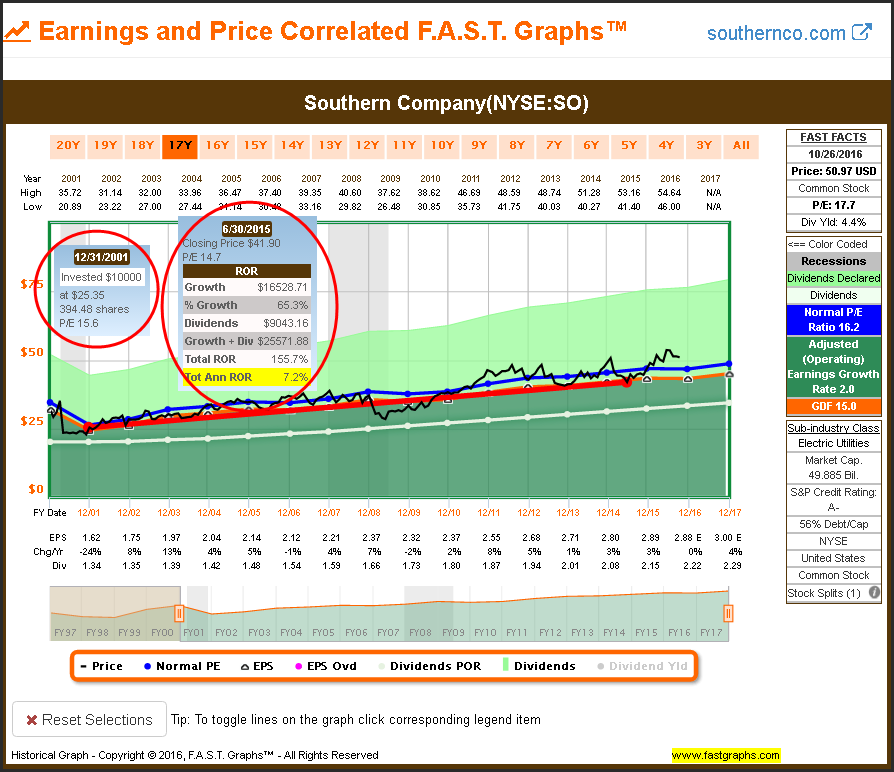

Southern Company (SO)

My second example looks at Southern Company, which also has a very low earnings growth rate of only 2%. However, with this example, earnings growth has been more consistent. Once again, we see how the stock price wants to gravitate to the 15 P/E ratio fair valuation reference.

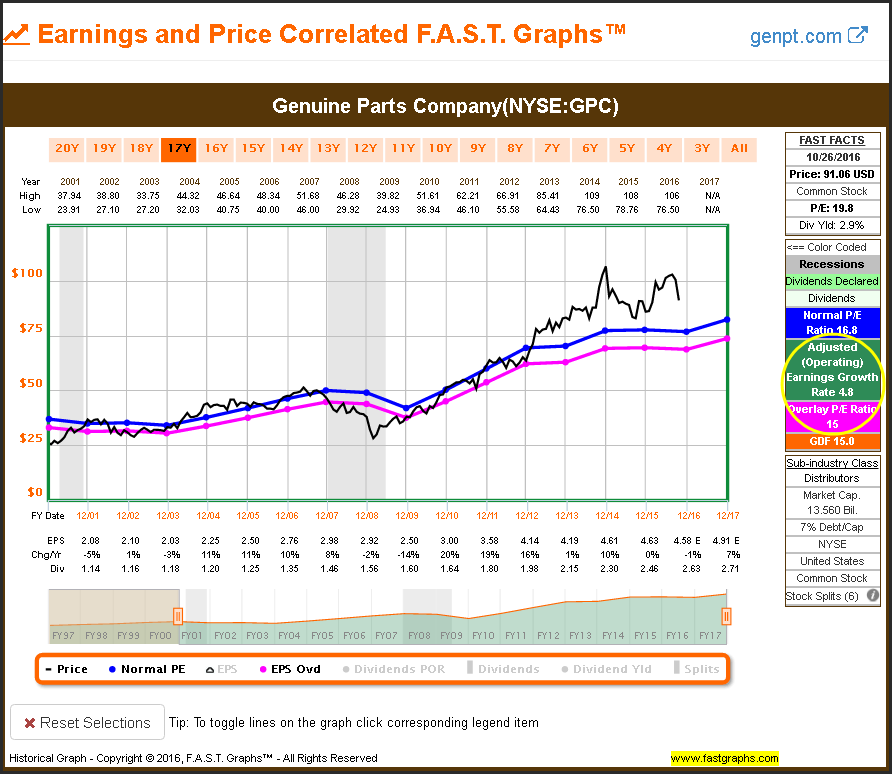

Genuine Parts Company (GPC)

With my Genuine Parts example I present a company with a similar earnings growth rate of 4.8% similar to the S&P 500 earnings growth rate of 5%. Once again we see the validity of the 15 P/E ratio as a standard valuation reference. The reader should note how relevant the pink 15 P/E ratio line is as a valuation standard over this long time frame.

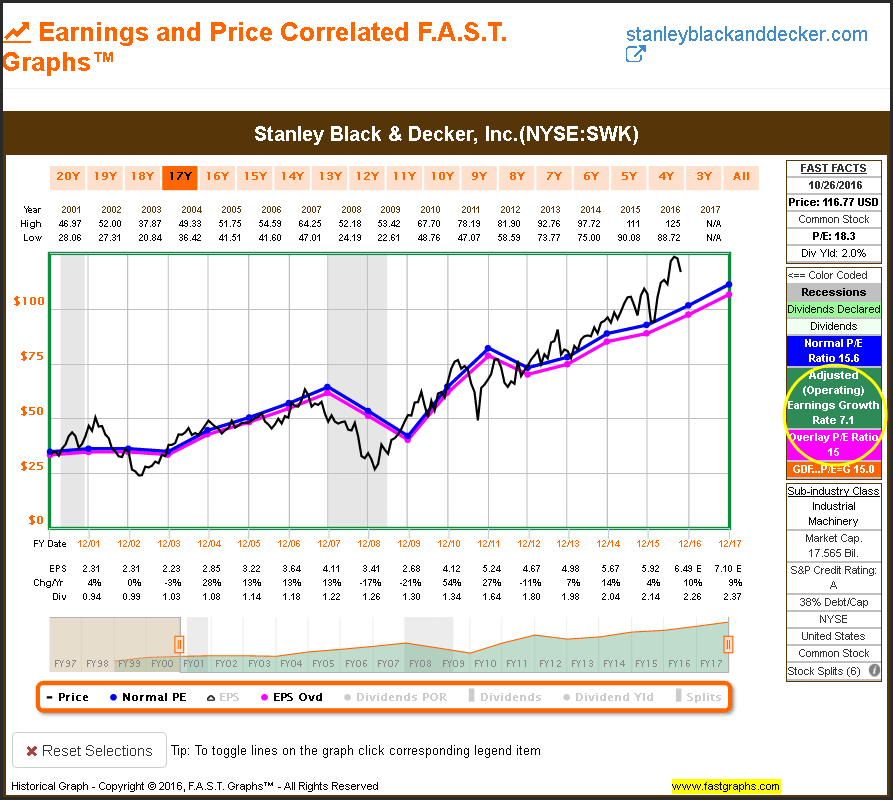

Stanley Black & Decker, Inc. (SWK)

Stanley Black & Decker is my first example where earnings growth is above the average earnings growth of the S&P 500. Once again we see the value of utilizing the 15 P/E ratio as a standard valuation reference. In this case, the normal P/E ratio of 15.6 and the fair valuation reference P/E ratio of 15 are closely aligned. The correlation between price and these valuation references are undeniable.

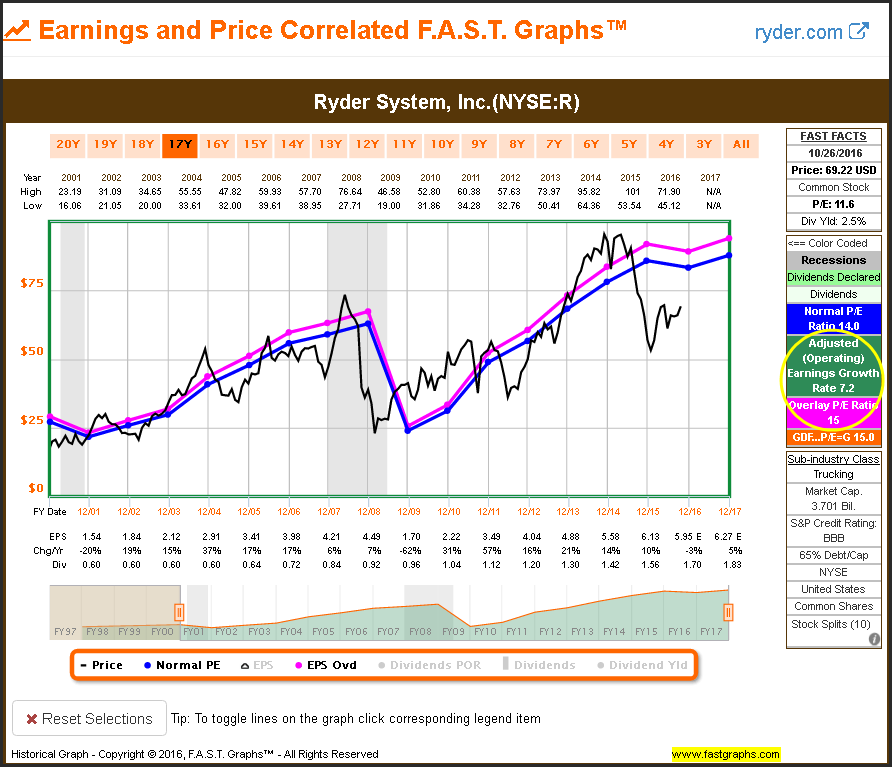

Ryder System, Inc. (R)

Ryder System has also generated an above-average earnings growth rate of 7.2%. However, in this example we see a significant earnings drop during the Great Recession. This example provides the opportunity to illustrate why the P/E ratio must always be looked at relative to other metrics. In other words, even though the 15 P/E ratio is a valid valuation reference, it doesn’t tell the whole story. This example clearly shows that the P/E ratio is a relative metric.

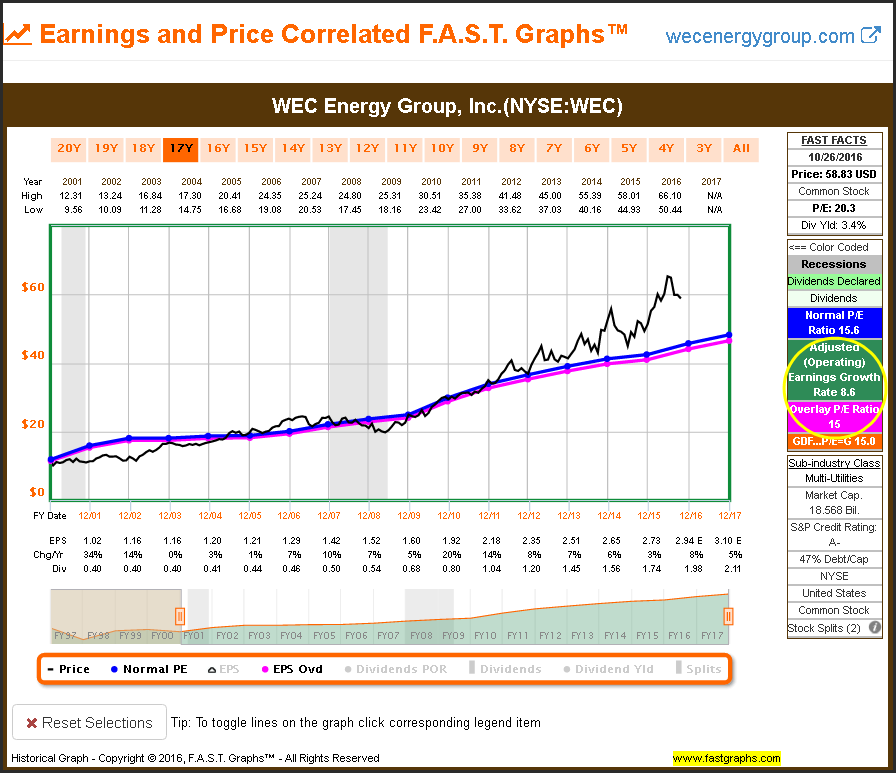

WEC Energy Group, Inc. (WEC)

WEC Energy Group (formerly Wisconsin Energy Corporation) is one of the fastest-growing utilities in America. Since 2001 earnings growth has averaged 8.6% per annum. However, once again we clearly see the validity of the 15 P/E ratio valuation reference. Even though this company has grown at an above-average rate, the P/E ratio of 15 represents a sound valuation level to consider investing in it.

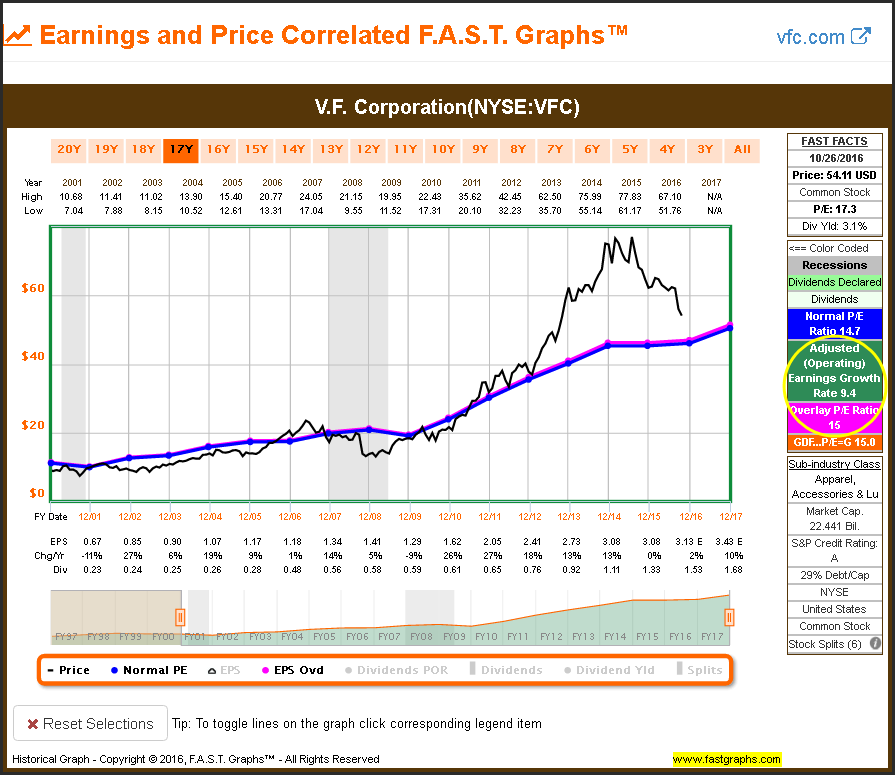

V.F. Corporation (VFC)

With V.F. Corporation we see an example where earnings growth is approaching double-digit levels at 9.4% per annum. Nevertheless, we see how valuable and insightful the 15 P/E ratio as a valuation reference has been over this historical timeframe. Additionally, since 2013 the stock price had become significantly disconnected from that fair valuation reference level. But price is clearly gravitating back towards that level over the last two years.

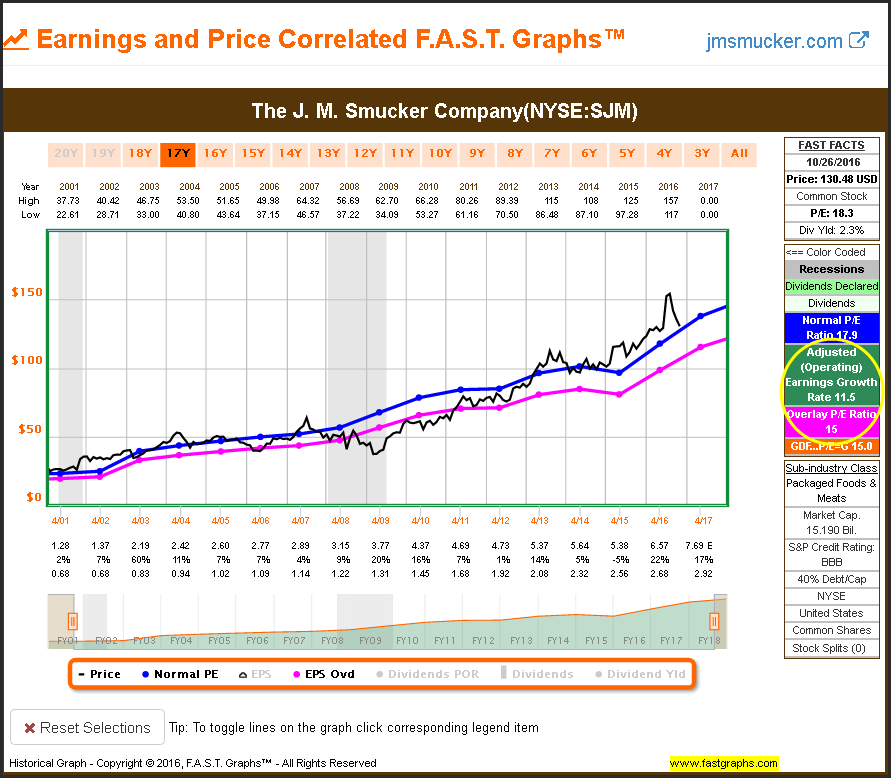

The JM Smucker Company (SJM)

With JM Smucker earnings growth of 11.5% is more than double the average earnings growth of 5% as represented by the S&P 500. As we have now entered double digit earnings growth, we see an example where the normal P/E ratio of 17.9 might be considered a better valuation reference than the P/E ratio 15 standard.

However, even with this faster growing company, the 15 P/E ratio valuation reference has still manifested many times since 2001. The point is that the 15 P/E ratio valuation reference should not be thought of as an absolute. Instead, it should be thought of as a rational valuation reference even when growth is double digits.

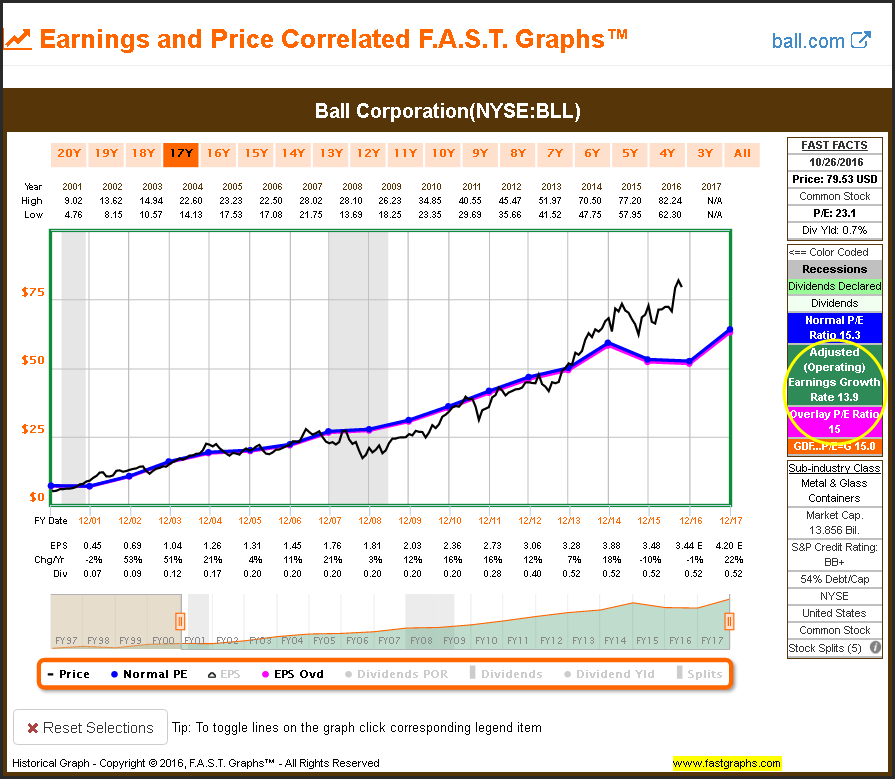

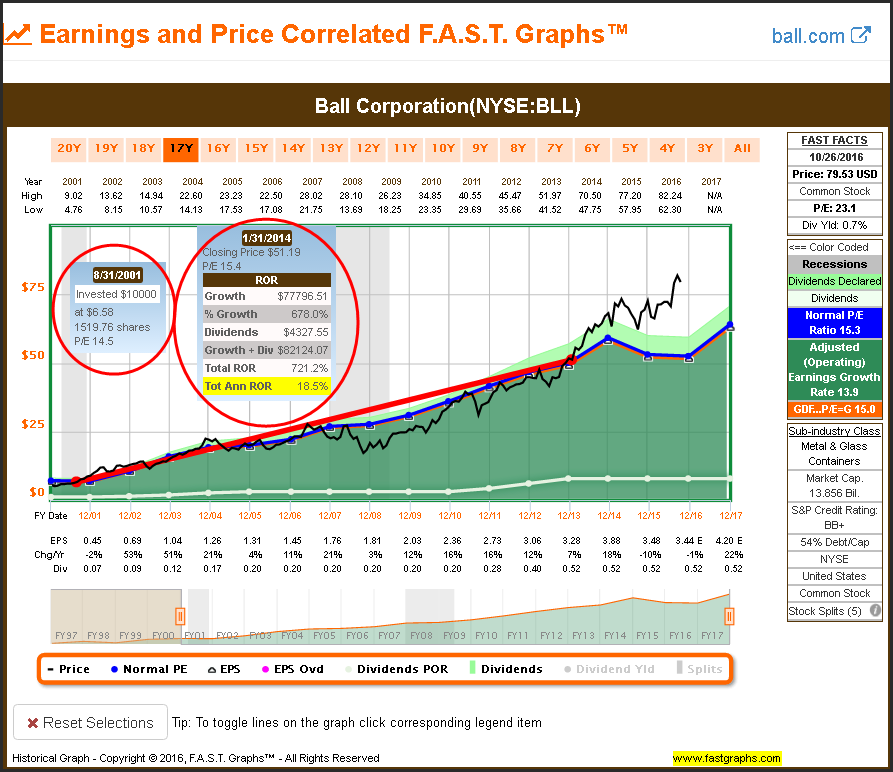

Ball Corporation (BLL)

Even though we saw a tendency for a higher normal P/E ratio with JM Smucker above, the 15 P/E ratio valuation reference on faster growing Ball Corporation is quite profound. Ball Corporation has grown earnings at 13.9% since 2001, but in this example both the normal P/E ratio of 15.3 and the fair valuation standard P/E ratio of 15 are almost identical. I will utilize this same example with a complete F.A.S.T. Graphs™ later in this article to illustrate the relative nature of the P/E ratio to a company’s earnings growth rate towards generating total returns.

With the above examples I demonstrated how the 15 P/E ratio represents a rational standard of valuation across various earnings growth rates from low to mid double digits. Moreover, from this perspective the P/E ratio of 15 as a standard valuation reference is not an indicator of future returns. Instead, it simply represents a rational level of soundness and/or prudence.

The P/E Ratio A Relative Metric When Utilized To Calculate Future Returns

Perhaps the most important thing to realize when using P/E ratios as an investment tool is that the P/E ratio by itself tells you very little about the return potential a stock might offer. As previously discussed, the P/E ratio represents a level of soundness based on the earnings yield it represents. Therefore, the P/E ratio's true value is as a barometer or tool best utilized to measure soundness. Unfortunately, many investors fail to realize this, and therefore, miss the long-term benefits that an understanding of the relevance of the P/E ratio at various levels offers.

The P/E ratio, used properly, can assist the investor in the rational evaluation of the realistic probabilities of achieving a certain long-term rate of return and the amount of risk taken to get there. However, this can only be accomplished when the P/E ratio is evaluated in relation to a stock’s past, present and future capacity for growth. The primary metrics available to measure a company’s growth potential are earnings, cash flows and revenues. However, when utilizing the P/E ratio, it is solely based on earnings.

When a stock is purchased at a sound valuation, it represents prudence on the part of the buyer. However, from that point forward, future returns will be a function of how fast the underlying company can grow its business. Therefore, you can pay a sound valuation represented by the same P/E ratio of 15, for example, for two companies, one of which is growing faster than the other. However, even though your purchase might be prudent in both cases, the faster growing company will generate a higher long-term total return.

With the following examples I present a complete F.A.S.T. Graphs™ to include dividends on the slow-growing Southern Company versus the faster-growing but lower-yielding Ball Corporation. I have run calculations on historical returns on both companies based on investing as close as I could to a P/E ratio of 15 at the beginning and at the end. In both cases, the 15 P/E ratio valuation reference represents soundness. However, a faster-growing Ball Corporation produced significantly higher total returns.

Summary and Conclusions

With this part 1 of a two-part series I demonstrated the value and the validity of the P/E ratio as a valuation tool for companies growing earnings at 15% or less. I pointed out that a P/E ratio of 15 represents an earnings yield of 6.67% which I consider a minimum threshold for low to moderate growing businesses. When the P/E ratio of companies that fall within this growth rate is higher than 15, the investor should realize that it represents an earnings yield that does not compensate them for the risk they are taking.

But more importantly, as it relates to the promise in the title of this article, the P/E ratio is more relevant than the PEG ratio for companies falling into these earnings growth rate capabilities. However, in part 2, I will discuss the superiority of the PEG ratio as a valuation metric when examining growth stocks. As a clue, a PEG ratio of 1 is considered attractive and PEG ratios above 1 are considered less attractive.

However, when examining companies with earnings growth rates lower than 15%, the PEG ratio will always be above 1, and sometimes significantly. In the case of a low growth stock such as Southern Company presented in this article, even at a fair valuation P/E ratio of 15 its PEG ratio would be 7.5 (15÷2). Such a high PEG ratio would suggest that the company was significantly overvalued when its P/E ratio was 15 even though it is not.

With that said, I am a major advocate of the PEG ratio as an important valuation tool when evaluating fast-growing companies. For companies growing earnings at 15% or greater, I consider the PEG superior to the P/E ratio as a valuation measurement. In part 2, I will state my case as to why.

Disclosure: Long VZ,SO,GPC,SWK

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs

© F.A.S.T. Graphs

Read more commentaries by F.A.S.T. Graphs