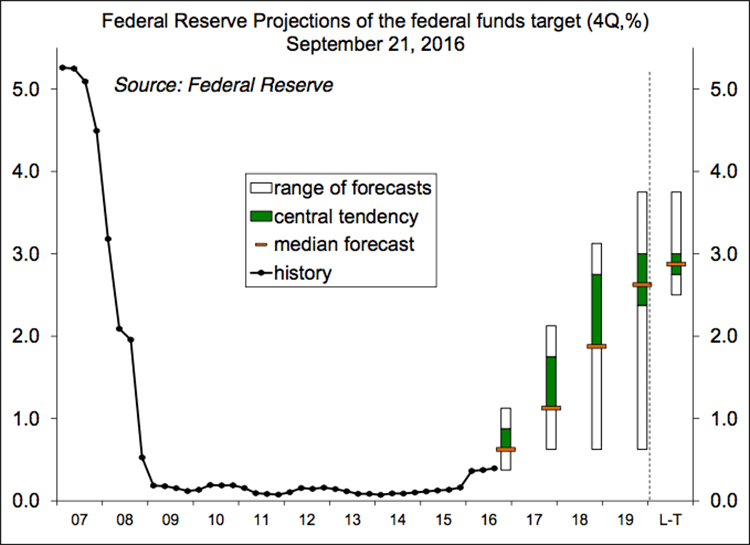

Recent data reports have added little color to the economic outlook, but that may change soon enough. The advance GDP report should show the economy advancing at a moderate pace, but results are likely to remain mixed across sectors. Fed officials were close to raising rates in September, but recent figures probably haven’t been compelling enough to force action at the November 1-2 policy meeting. The employment report will be subject to the usual uncertainties, but job growth has slowed, if only reflecting tighter job market conditions.

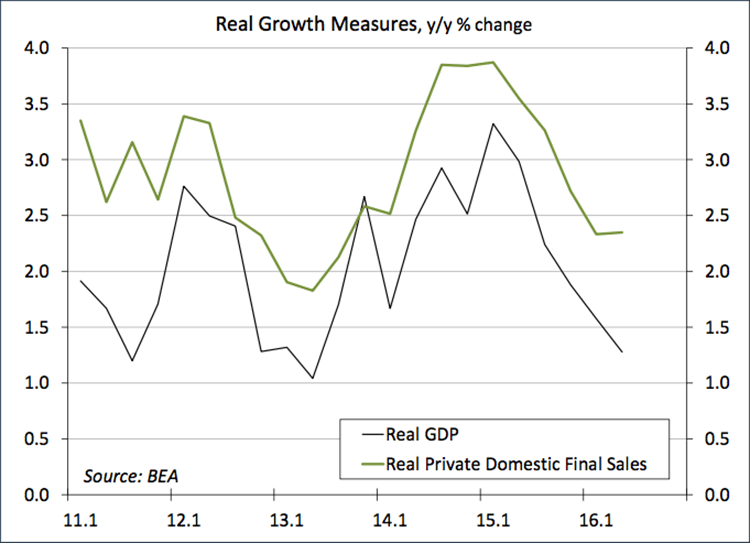

Investors place far too much significance in the headline GDP growth figure. This is the advance estimate (arriving Thursday) and will be subject to large revisions. However, the story ought not to change much. Consumer spending growth (roughly 70% of GDP) was likely moderate – slower than the second quarter’s blistering 4.4% pace, but better than the first quarter’s 1.6%. Business fixed investment and residential homebuilding are likely to have been soft. A slowing trend in inventory growth subtracted significantly from headline GDP growth in recent quarters, making the economy appear weaker than it really is. An inventory rebuild was expected to fuel stronger GDP growth in 3Q16, but now that contribution appears likely to have been much more modest. Foreign trade ought to add, largely reflecting a surge in agricultural exports.

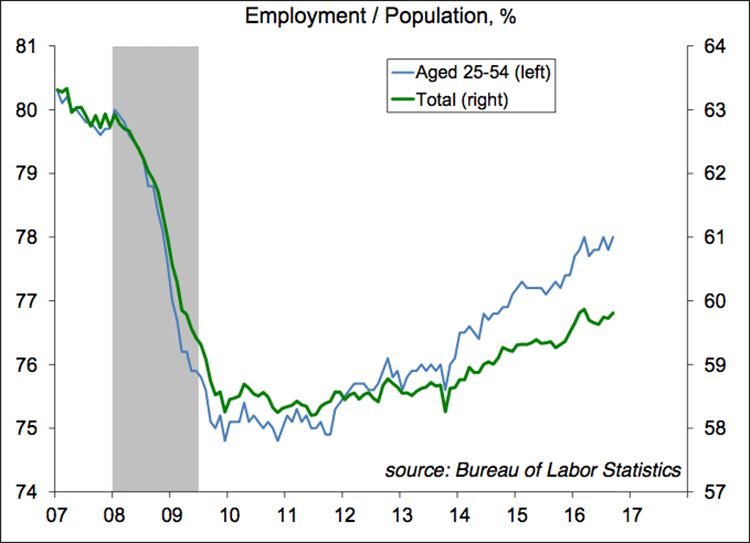

Job growth was especially strong in 2014 and 2015, recovering more of the slack generated in the financial crisis. However, the trend appears to have slowed this year. That likely reflects tighter labor market conditions. Late in the job market recovery, tight conditions typically lead to higher wages and many of those on the sidelines (out of work, but not officially counted as “unemployed”) will return to the workforce. Wage growth is still moderate, but higher than in recent years, and labor force participation has begun to rise.