1. Why This Economic Recovery Has Been So Disappointing

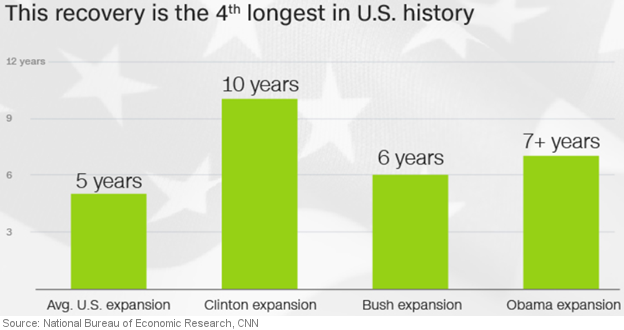

2. The Fourth Longest Economic Expansion on Record

3. One Chart Shows Why So Many Americans Feel Poor

Overview

Forecasters who were predicting a surge in the economy in the second half of this year have revised those estimates much lower in recent weeks. It now looks like the economy may not achieve even 2% growth this year. Today, we’ll look at some of the reasons why.

While economic growth has been anemic, the recovery since mid-2009 has been the fourth longest in history. Since World War II, the American economy has typically grown for about five years on average, as shown below, and then had a contraction. This expansion, which officially began in June 2009, is already over seven years old.

Increasing numbers of Americans feel “poor.” I will provide one particular chart today which illustrates why so many people feel that way today. I think you’ll find it very interesting. Let’s get started.

Why This Economic Recovery Has Been So Disappointing

The US economy grew at an annual rate of only 1.1% in the first half of this year. That was well below predictions late last year of 3+% growth for all of 2016. Likewise, many forecasters suggested that GDP growth would surge in the second half of this year. But as I wrote last week, most predictions of 3-4% growth in the second half have been pared back to around 2%.

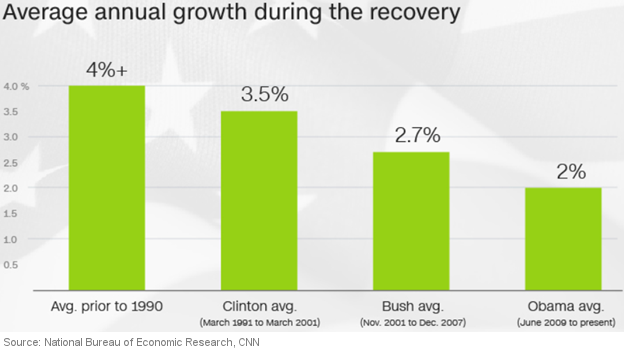

This has been a distressingly consistent pattern in recent years. With the exception of a strong quarter here and there, economic growth has been stubbornly disappointing ever since the Great Recession ended in mid-2009. Growth in US gross domestic product has averaged only about 2% since then, compared with4.6% on average during the recovery following the recession of the early 1980s.

The problem goes beyond the current recovery and beyond the US. For most of the 21st century, the developed world – the US, Western Europe and Japan – has been stuck in a pattern of slow economic growth. In the US, the boom of the late 1990s ended with the bursting of the dot-com bubble; the recession that followed was relatively mild, but the recovery was weak. It took another bubble, that time in housing, to get the economy moving again. And as we all know, that bubble ended with the Great Recession and a financial crisis.

Economists aren’t exactly sure what’s behind the prolonged global slowdown. Aging populations certainly play a significant role – more retirees means fewer people working, which, all else being equal, means less economic growth.

But that isn’t the full story. Even setting aside retirees, fewer adults are working, especially men. As I wrote on September 6, some 8-10 million working-age (25-54) US males have disappeared from the workforce and many, if not most, have given up looking for work.

And among those who are working, productivity has been growing more slowly. Productivity is measured by how much value people produce for each hour they work. Some economists, most prominently Northwestern University economist Robert Gordon, argue that the Internet and other recent technological advancements haven’t boosted the economy as much as past innovations such as electricity and air travel.

Yet whatever the explanation, more and more economists are convinced the trend is here to stay. In a 2013 speech at the International Monetary Fund, former Treasury Secretary Larry Summers became perhaps the first prominent economist to talk about “secular stagnation,” a wonky term for the idea that low-growth is a long-term trend, not a short-term effect of the recession.

Since then, the idea has gone mainstream. In August, John Williams, the president of the Federal Reserve Bank of San Francisco, wrote an essay looking at what policymakers can do in a world of sustained low interest rates. His conclusion was, not much.

Later in August, Fed leaders dedicated much of their annual retreat in Jackson Hole, Wyoming to similar discussions. One conclusion was that the Fed is playing catch-up, since economic growth has consistently fallen short of policymakers’ expectations throughout the recovery.

This is far more than an academic debate. If the underlying growth rate of the economy has slowed, that means it will take less to push the US into a recession, and it will be harder for policymakers to pull it out.

Likewise, there are consequences in addition to recessions. Slow economic growth generally means weak wage growth, which is why many Americans saw little benefit from the recovery until only recently. Wages grew by 2.6% in the 12 months ended in September.

Japan and Western Europe have fared even worse. Japan has been locked in a generation-long slump, and Europe has never seen a meaningful recovery after the global financial crisis. In Europe especially, the prolonged downturn has created a generation of young people who can’t find work and of older workers who can’t afford to retire.

Despite unprecedented quantitative easing by central banks around the world, and near zero (or even negative) interest rates, the economies of the US, Western Europe and Japan continue to grow well below their post-recession averages, with no end in sight.

The Fourth Longest Economic Expansion on Record

As noted above, the US economy has grown by only 2% per year on average since the Great Recession ended in mid-2009, making it the slowest recovery since records have been kept. Yet while growth has been disappointing, this is the fourth longest recovery in history going back to 1850.

Since World War II, the American economy has typically grown for about five years on average, as shown below, and then had a contraction. This expansion, which officially began in June 2009, is already over seven years old.

September marked the 86th month of this economic recovery. If it continues into February, it will become the third longest recovery on record. It would have to continue for another three years to break the all-time record of 120 months.

So far, this recovery has occurred entirely during President Obama‘s time in the Oval Office, making it the longest expansion under a single president. The growth streak would need to extend just a little more than halfway through the next president’s term to achieve a modern record.

The bright spot in this seven-year recovery is jobs. While the rate of economic growth has been disappointing, the average pace of job growth in this recovery has already topped what happened during the 2001 to 2007 expansion under President George W. Bush.

Over 14 million jobs have been added since the low point from the financial crisis. Job growth is as important – if not more important – than overall growth, many economists argue. “We are experiencing the longest string of consecutive monthly jobs gains in economic history,” says Mark Zandi, chief economist at Moody's Analytics.

The unemployment rate has gone down by half and now stands at 5.0%, down from a high of 10% in 2009. About 245,000 people applied for unemployment insurance last week, down from 595,000 during the second week of June in 2009. Job openings have more than doubled.

Yet even the improving unemployment rate doesn’t tell the whole picture. The country’s Labor Participation Rate – the share of the workforce that is employed or looking for a job – is woefully low. Currently it stands below 63%, the lowest level since the 1970s.

Meanwhile, many American families are living paycheck to paycheck. According to a survey earlier this year by the Federal Reserve, nearly half of all American adults couldn’t scrape together $400 to cover a financial emergency such as a health problem or a car in need of repair.

In summary, while this may be one of the longest economic recoveries on record, it certainly feels to many Americans that we never fully emerged from the Great Recession.

One Chart Shows Why So Many Americans Feel Poor

Why do so many Americans feel dissatisfied about the economic state of our nation? One simple chart offers a lot of insight.

Economists measure standards of living in many ways. Among the most common is to look at the change in the value of goods and services produced by a country, adjusted for inflation and for population growth. This measure, known as “per capita real gross domestic product,” essentially shows how much income the average person is generating.

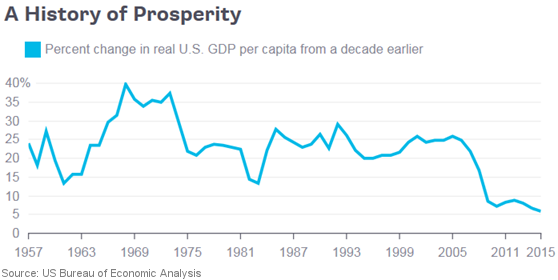

The chart below shows the cumulative growth in per capita real GDP in the US over the preceding 10 years, for each year from 1957 to 2015. It does a great job of depicting the country’s post-World War II macroeconomic experience.

There are several takeaways from this chart. Economic growth was very strong in the late 1960s and early 1970s. In every year from 1966 through 1973, per-capita income was up between 30% and 40% from a decade earlier.

In every year from 1984 to 2007 – a period that economists call the Great Moderation, because of the way both growth and interest rates stabilized – per-person income was up between 20% and 30% from a decade earlier.

To the contrary, cumulative per-person growth from 2005 to 2015 was lower than in any prior decade in the sample. That certainly helps explain why many Americans are unhappy with the nation’s recent economic performance.

While the US economy has recovered from such slumps in the past, more and more Americans believe we will be stuck with slow growth for the foreseeable future. If Hillary Clinton is elected president, with her tax increases and even more big government regulations, they may be correct.

Wishing you profits,

Gary Halbert

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

|