As Liquidity Tightens Fade DM Americas and Look to DM Asia for Outperformance

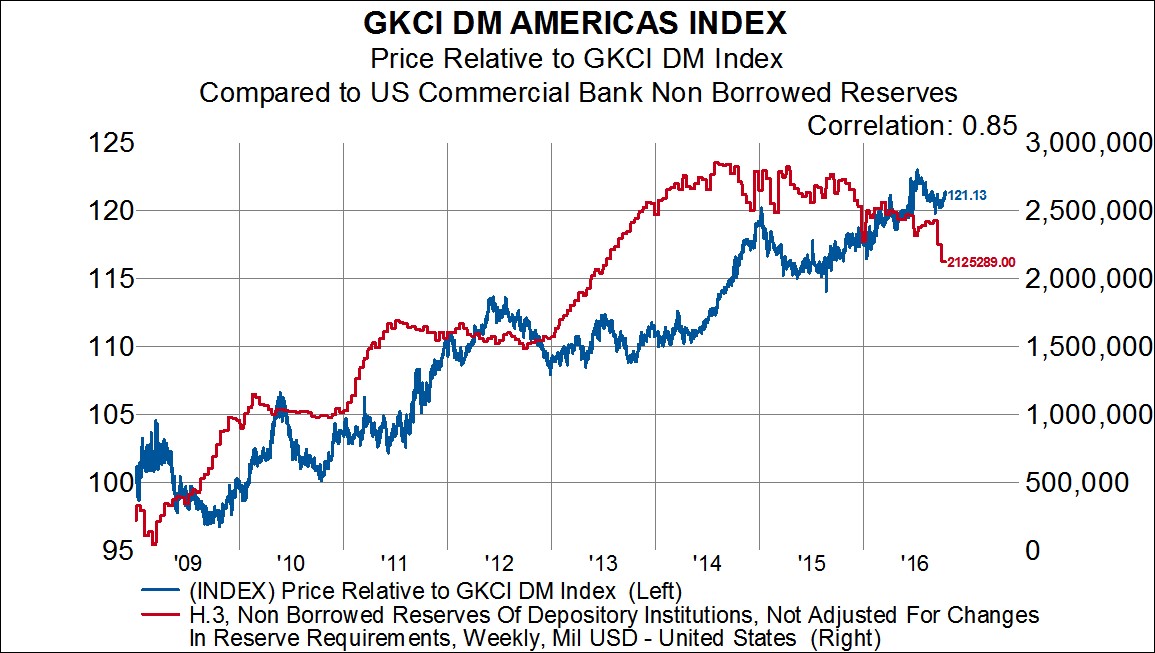

We all know that the Fed has committed to keeping its balance sheet extraordinary large for as long as they feel the weak economy justifies this accommodating position. And so far as the first chart below shows, the Fed has held to its word. Total assets at the Fed have remained around $4.5 trillion since the end of 2015. However, while total assets have held steady there has been a not so suitable decline in US commercial bank non borrowed reserves. Non borrowed reserves have declined by over $717 billion from the high in August 2014 and this has impacted relative equity performance around the world.

As non borrowed reserves were accumulating it paid to be exposed to North America relative to the rest of the developed world. In particular, DM Americas consumer discretionary, industrials and health care stocks all have very strong positive correlations to the level of non borrowed reserves in the US banking system. So as non borrowed reserves have declined over the past 24 months or so, we have started to see what looks like some relative performance tops for many DM Americas sectors.

If we assume that this declining trend in non borrowed reserves continues, then it would make sense to look at relative equity performance that has a negative relationship to this series. And when we look for that, DM Asia looks like the most interesting region. On a relative performance basis DM Asia is only 8.5% above its low that was put in place right as the Fed begin to hold the size of its balance sheet steady. However, as this next chart suggests, DM Asia is ripe to outperform if non borrowed reserves continue to decline. Specifically, cyclical sectors of the economy such as industrials, information technology and materials look poised to outperform the rest of the developed market.