Flowers Foods a High-Yield Risk Worth Taking

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIntroduction

There are certain times when being a value investor also implies taking a contrarian approach. However, the terms “value investor” and “contrarian investor” are not always synonymous. On the other hand, when faced with a significantly overvalued marketplace like we see today with blue-chip dividend growth stocks, value investing and contrarian investing tend to become one and the same.

The simple fact is that when faced with a strong bull market, true fairly valued dividend growth stocks become very hard to find. In a strong market, value typically comes about for a reason, and that reason is typically associated with problems. However, the key to long-term investing success is when you find fair value due to a temporary problem, and not a permanent impairment of the underlying business.

Flowers Foods, Inc (FLO): Once Highflying Investor Sentiment Has Recently Turned Negative

The fairly valued dividend growth stock research candidate I am featuring in this article is Flowers Foods, Inc. The company was founded in 1919, went public in 1968, and through organic growth coupled with a series of acquisitions and divestitures, it has grown into the second largest North American bakery. As a dividend growth stock, Flowers Foods is a member of David Fish’s Dividend Contenders as it has raised its dividend for 15 consecutive years.

Flowers Foods has historically commanded an above market P/E ratio in the marketplace. However, since the end of October 2015, the company’s stock price has fallen approximately 43% from its then overvalued high. This precipitous drop in stock price has brought the company into what appears to be attractive valuation levels based on earnings and/or cash flows, and has pushed its current yield above 4%. Clearly, the stock has become unpopular, and I see two primary reasons why this has occurred.

The most significant reason, in my opinion, has been a significant slowdown in earnings growth to a mere 1% average rate since the beginning of fiscal year 2014. Prior to that time, Flowers Foods had historically grown earnings at an average of more than 20% per annum. (I will cover both of these results in more detail later.) This previously high rate of growth essentially explains its historical normal P/E ratio of 22, and the recent significant slowdown of earnings growth partially explains the current reset in its valuation.

The second reason for the company’s current negative investor sentiment is based on the announcement that the Department of Labor is investigating whether or not the classification of its delivery drivers as independent contractors is legal and valid or not. This investigation has also resulted in a rash of additional lawsuits.

Flowers Foods has acknowledged the Department of Labor’s investigation without further comment at this time, and as expected, stated that they will cooperate with the investigation. However, management has indicated that they believe the additional lawsuits are without merit and plan to vigorously defend themselves against them. Also, Flowers Foods management indicated they see no reason to book a reserve for the DOL investigation. In an article on September 8, 2016 in baking business.com Flowers Foods Pres. and Chief Executive Officer Alan L. Schiver offered the following comments:

“Like many other companies operating independent contractor models, our model has come under recent scrutiny,” Mr. Shiver said. “To that end, we are cooperating with the Department of Labor in its review. Because that process is confidential, there is nothing more we can disclose.”

“Let me stress that we also consider our fiduciary duties and our financial reporting to be of the utmost importance,” Mr. Shiver said. “We have carefully evaluated the proper accounting treatment of our legal situation. Based on this review, we have determined that at this time booking a reserve is not appropriate, given the current facts and circumstances.”

“Additionally, as many of you are aware, there is pending litigation. We believe that the lawsuits have no merit, and we are vigorously defending ourselves against them.”

Personally, I am not overly concerned with the litigation issues which I consider as event risks. These are issues that management should be capable of dealing with, and I also believe that the DOL investigation will likely take years to resolve. Stated differently, I don’t see these events capable of instigating a permanent impairment in the company’s future business prospects.

However, I do believe the slowdown in earnings growth over the last few years represents a problem that requires more scrutiny and analysis. Consequently, the remainder of this article will deal with the current financial health and strength of the company, and most importantly, the future potential of the business over the longer run.

Why Get Interested in a Company Experiencing Problems?

I think most readers would agree that it’s getting very difficult to find quality and value in today’s long-running bull market - especially when looking for income opportunities available with blue-chip dividend growth stocks. As previously stated, there are usually reasons why a business (stock) is underperforming in a bull market.

On the other hand, low valuation on a good business offers the opportunity for extraordinary returns if the problems are temporary. Consequently, I approach these situations looking for the opportunity where others only see the risks. Legendary investor Warren Buffett taught me the benefits of this approach through his following quotes which I believe are full of investing wisdom:

“Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what’s popular and do well.”

“The best thing that happens to us is when a great company gets into temporary trouble…We want to buy them when they’re on the operating table.”

“Be fearful when others are greedy and greedy only when others are fearful.”

“The most common cause of low prices is pessimism—some times pervasive, some times specific to a company or industry. We want to do business in such an environment, not because we like pessimism but because we like the prices it produces. It’s optimism that is the enemy of the rational buyer.”

Flowers Foods: Essential Fundamentals at a Glance

Next, I will utilize the F.A.S.T. Graphs™ fundamentals analyzer software tool in order to take the reader through a quick review of the important underlying fundamentals supporting this company. Additionally, I will be walking you through my personal analysis, and as previously promised, elaborate on the changes in the company’s growth rates. Through this process I will be analyzing and evaluating the company’s historical record and I will present a thesis regarding the company’s future growth potential.

Flowers Foods: Earnings Growth since 2002

As I have pointed out in previous articles, I prefer looking at the business behind the stock before I bring stock price into the equation. Stock prices can engender emotional responses, and I like to keep emotions out of my analysis - especially in the beginning. The following graph plots Flowers Foods’ earnings results since 2002.

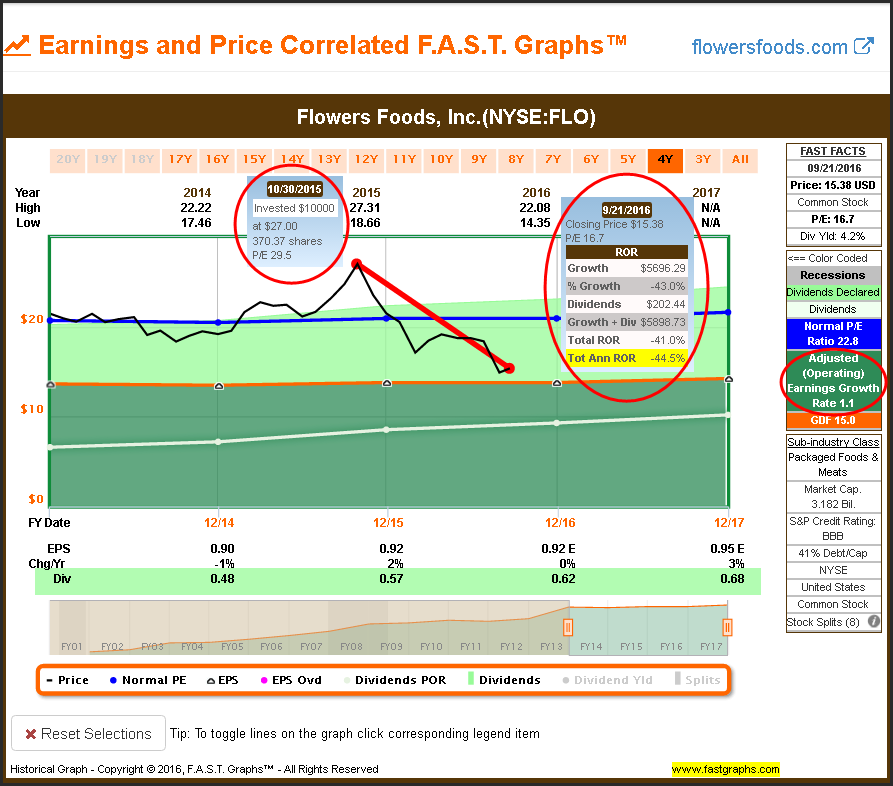

There are a couple of points I would initially like to bring to the reader’s attention by asking you to look to the FAST FACTS boxes to the right of the graph. The first is the average earnings growth rate of 18.8% shown in the green rectangle. The next is the reported normal P/E ratio of 22.5, which is not yet shown on the graph, but it will become important later.

With those numbers in mind, and keeping in mind that they are an average, the first thing that came to my attention visually was the flattening of the earnings growth as represented by the orange valuation reference line since 2014. Even though the average earnings growth over this timeframe was high, recent results have clearly flattened and slowed down.

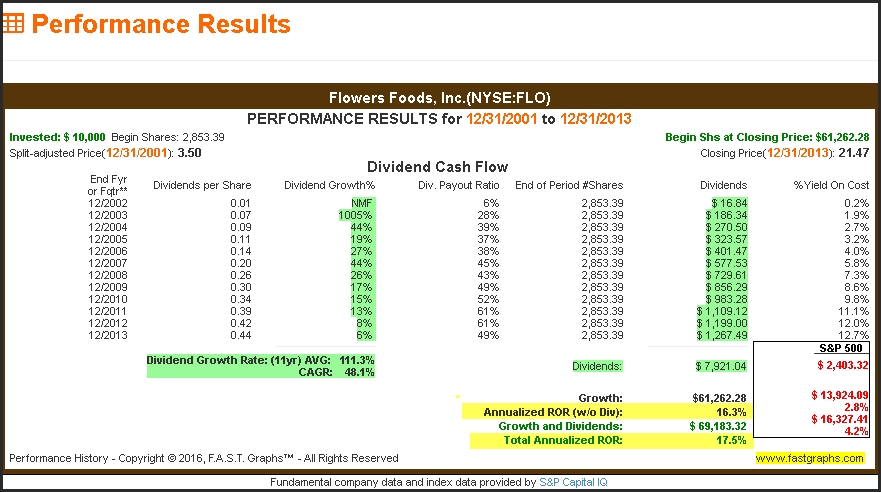

With my next graph, I present a complete F.A.S.T. Graphs™ including dividends, but I have scrolled the timeframe back to 2013 and discovered that earnings growth from 2002 to 2013 averaged 25.4%.

With everything including the monthly closing stock prices, the normal P/E ratio line (the dark blue line) and the dividends, I discovered a very rational and logical picture of Flowers Foods since 2002 through 2013. The stock price (the black line) clearly tracked and correlated to earnings (the orange line) and generated interesting looking capital appreciation. Therefore, the high historical normal P/E ratio of 22.6 makes perfect sense, and could even be looked at as a low valuation when viewed over this timeframe and relative to its earnings growth achievement.

The light green shaded area stacked on top of the earnings line vividly illustrates the significant amount of additional dividend income received representing the second component of total return - dividend income. The light green line (it appears white) in the dark green shaded area illustrates those same dividends prior to being paid out. The dark green shaded area below the light green line represents the earnings paid out as dividends (dividend payout ratio). This clearly shows that Flowers Foods has been very generous by sharing their profits with shareholders in the form of dividends.

When you put the performance associated with the above graph into numbers, we discover an excellent long-term dividend growth stock and superior total return investment. A $10,000 investment made on December 31, 2001 would have grown to over $61,000 by December 31, 2013 representing a 16.3% annual rate of capital appreciation. Add in the $7,921 of dividends and our total annual rate of return calculates to 17.5% over this timeframe, which is more than four times higher than the S&P 500. Over that timeframe, Flowers Foods was clearly an exceptional dividend growth stock and total return investment.

However, when we examine the company’s performance more recently, we get an entirely different picture. Earnings growth rates since 2014 and 2015 to include estimates for 2016 in 2017 are only 1.1% on average. That’s a far cry from the company’s previously shown historical earnings growth rate achievements.

Moreover, this explains the 44.5% drop in stock price since October 2015 that I alluded to earlier. This to me is of much greater concern; it’s not the drop in stock price, but the slowdown in earnings growth that troubles me the most. On the other hand, the dividend has continued to grow at double-digit rates in spite of the slowdown in earnings and the drop in stock price. That at least is encouraging at this point.

When you put these recent years’ performance into numbers, they paint a completely different picture of Flowers Foods as an investment. What was previously an excellent long-term investment has turned into a real dog in recent years, except of course for those dividends.

When I am researching a stock, I always start out by looking at earnings, but I never stop there. After I have reviewed earnings, I next turn to an evaluation of cash flows, especially when I am reviewing a potential dividend growth investment.

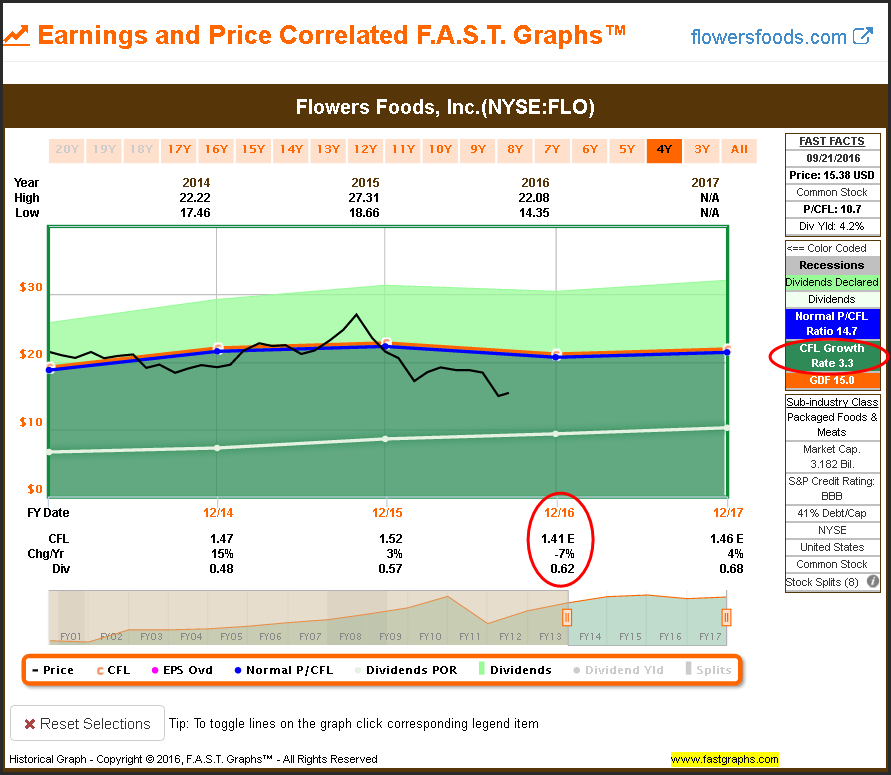

This next graph looks at Flowers Foods’ operating cash flow record since 2003 (Note: I shortened the timeframe by one year to exclude an aberrant growth of cash flow from 2002 to 2003 that skewed the growth rate). When looking at this company via cash flows, I get a similar picture of what I saw with earnings. However, on the basis of cash flows, the company appears more undervalued than it did when looking at earnings.

On the other hand, average cash flow growth was only 8%, and the company’s normal price to cash flow 12.6. Nevertheless, the cash flow view suggests to me that the company’s dividends are well covered. I consider this very important.

To keep my comparison of cash flow to earnings consistent, Flowers Foods’ cash flow record since 2014 is moderately better than what we saw with earnings. Cash flow growth has averaged 3.3%, including an estimate for 2017. However, cash flow growth for this year is expected to be down 7%. Nevertheless, this would still indicate that Flowers Foods is undervalued based on cash flow analysis.

Cash Flow and Profitability

Next I start looking a little deeper under the hood by turning to FUN Graphs (financial underlying numbers) and start out by looking at cash flow per share (cflps) and free cash flow per share (fcflps) relative to dividends paid per share (dvpps). I shortened the timeframe for just the past 10 years just so the numbers were easier to see, however, I wanted to include the Great Recession (grey shaded area). Once again, the dividend appears very well covered by cash flows, and I was pleased to see that Flowers Foods generated free cash flow even during the recession, however, only by a little.

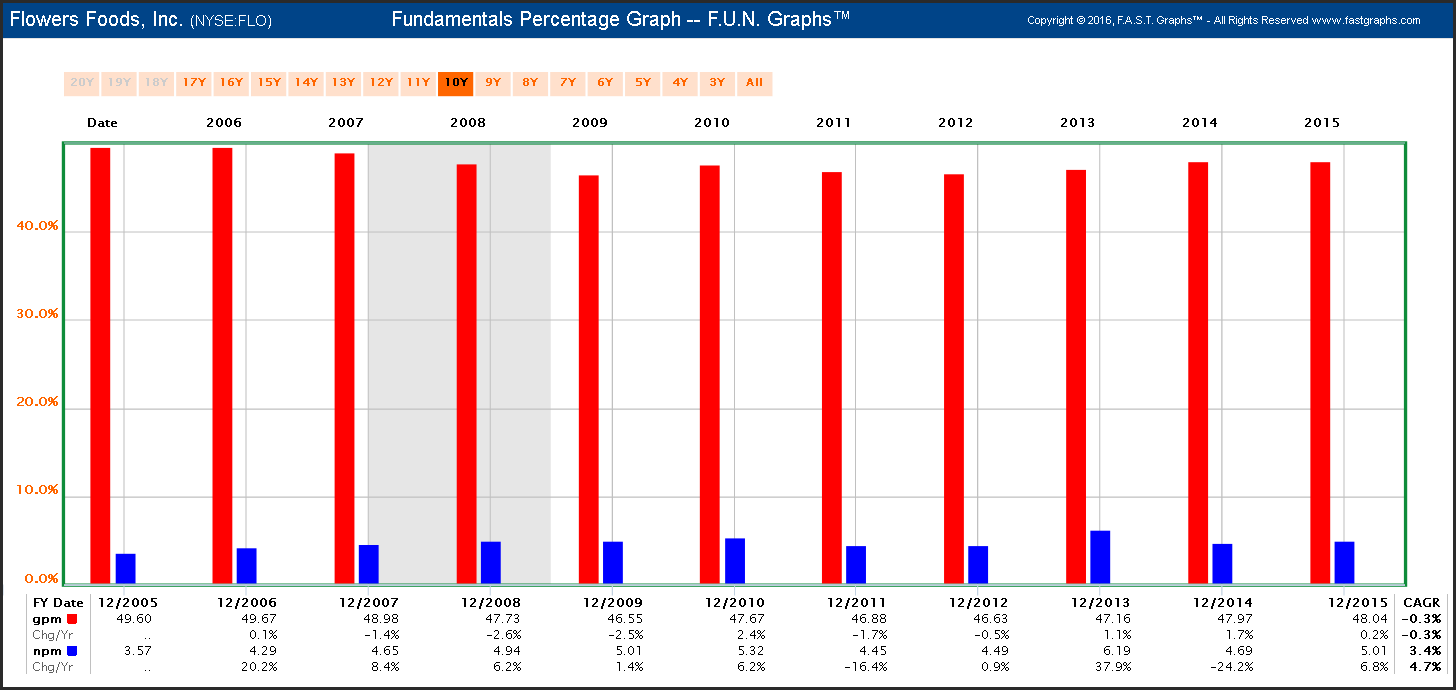

When I evaluated gross profit margin (gpm) and net profit margin (npm), I was pleased to see consistency in both over the past 10 years. Net profit margins in this kind of business are typically low, but Flowers Foods has consistently produced net profit margins in the 5% range.

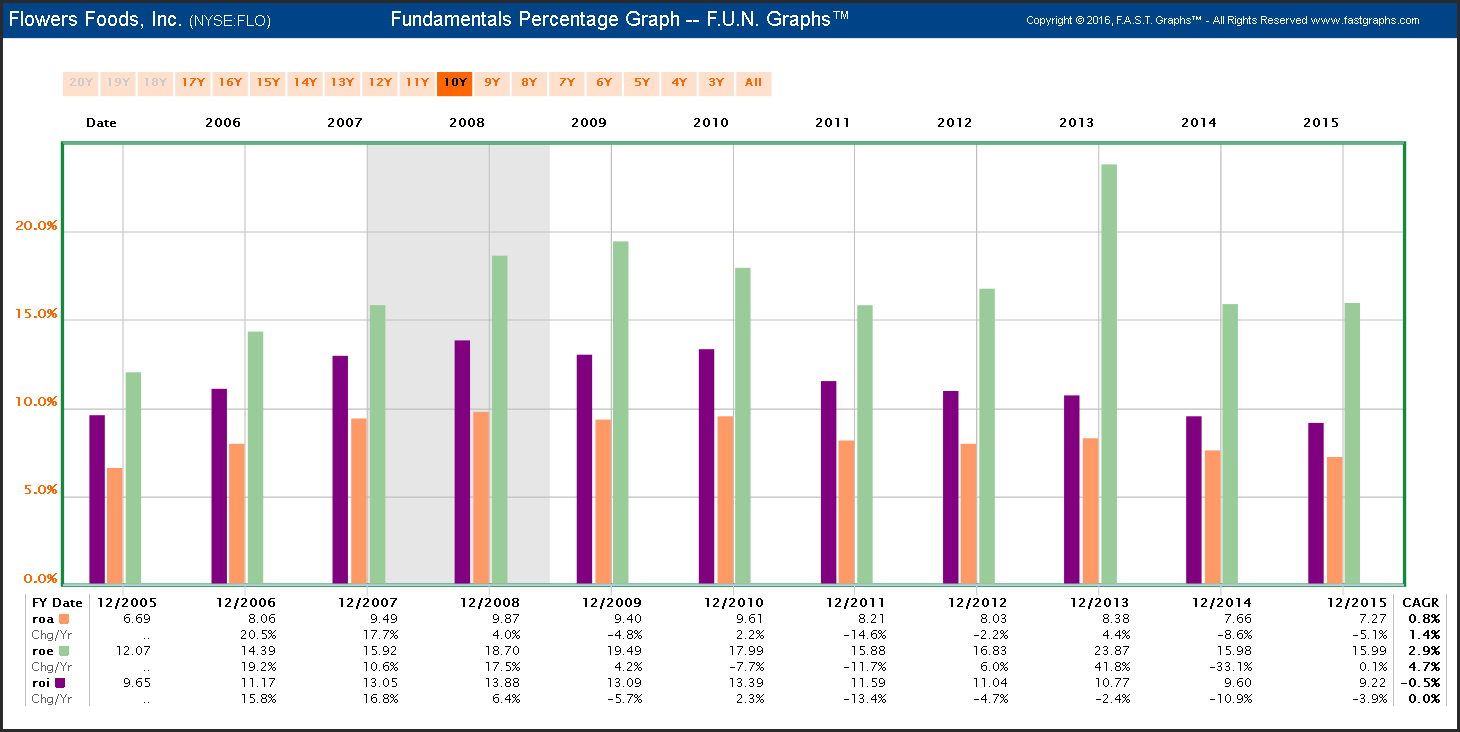

Flowers Foods’ returns on assets (roa), returns on equity (roe) and returns on invested capital (roi) are all acceptable levels, in my opinion. But more importantly, they all appear to be holding up quite well during the period of slow growth since 2014.

Since the above metrics look good, it seems logical that the issue might be with revenue growth. The following revenues per share (revps) clearly illustrate that revenue growth has slowed over the timeframe 2013 to 2015. However, the revenues are also high based on historical norms, even though they are not growing. This leads me to surmise that if the company can get their revenue growth back on track, then future operating results might improve.

The Balance Sheet

This next series of graphs looks at some key balance sheet metrics. The company’s assets (at) have grown nicely over time, including fiscal year 2015.

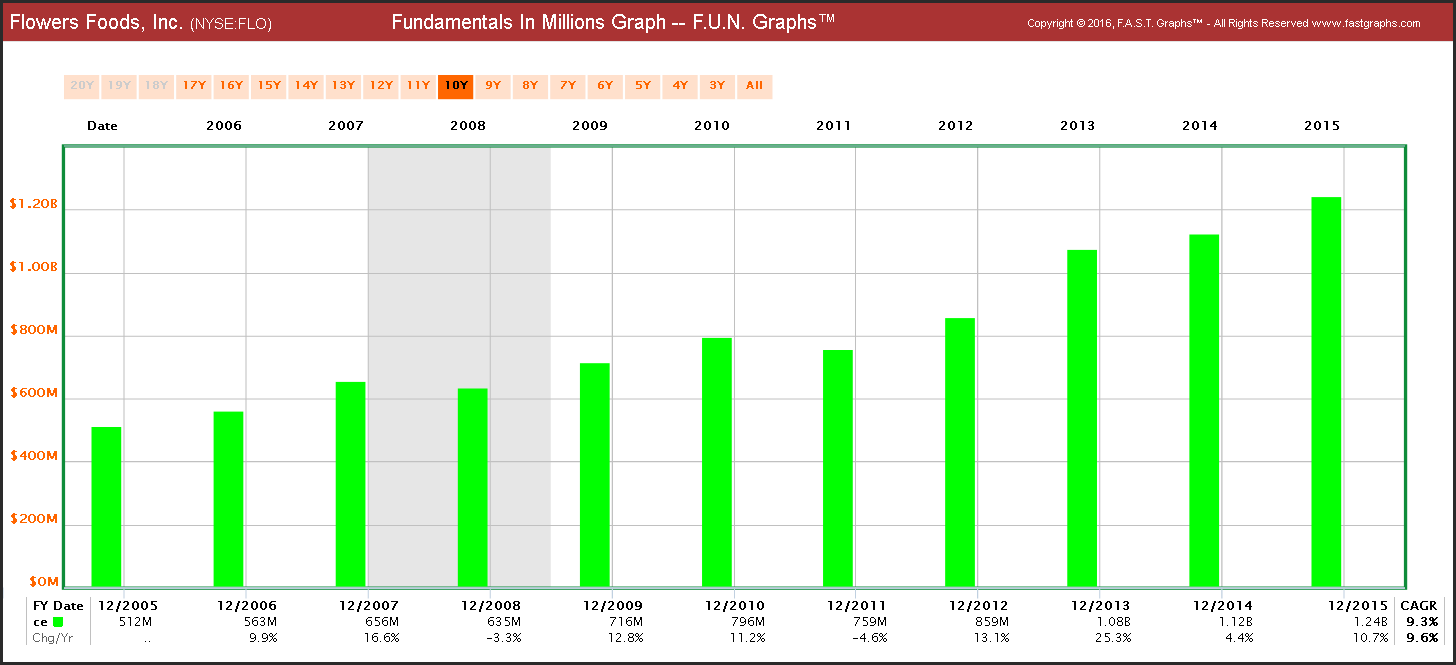

In conjunction with asset growth, the company’s book value or common equity (ce) has also steadily increased.

When I look at book value from a valuation perspective, I discovered that Flowers Foods’ price-to-book value is within normal historical norms. However, the company’s price-to-book (pb) is also currently on the low side of those historical norms.

When examining Flowers Foods’ debt situation, I see that both total debt (dt) and long-term debt (dlt) have increased in recent years. However, the company made strategic acquisitions, most notably Dave’s Killer Bread and Alpine Valley Bread Company. Both of these acquisitions fall into the healthier and popular organic and whole grains categories.

The Income Statement

Flowers Foods’ management has indicated that they are closely examining their cost structure. The company’s cost of goods sold (cogs) have stabilized in recent years and management believes there is room for continued improvement.

The Future: Focus on Cash Flows and Dividends

Since Flowers Foods’ current high yield and dividend growth record are my primary incentives for considering this company, I consider cash flow growth potential of paramount importance. The following Forecasting Calculator includes specific near-term consensus analyst estimates of cash flow growth, followed by the consensus 3 to 5 year trend line cash flow growth. Assuming those cash flow estimates are reasonably correct, the longer term total return potential based on a conservative price to cash flow of 12 looks appealing.

Analyst Scorecard

Although forecasting the future of anything is always a challenge, a review of the analysts historical record of forecasting cash flows provides some encouragement. The following Analyst Scorecard indicates that forward estimates have been reasonably accurate. However, there have been a few surprises.

Management Initiatives and Objectives

In a recent presentation, Flowers Foods’ Pres. and Chief Executive Officer Alan L. Schiver discussed the company’s views about the company’s vast market opportunity and their position. In that discussion he pointed out that Dave’s Killer Bread positions them for promising growth in the organic bread category and is now available at 9000 new store locations nationwide.

Additionally, he discussed the company’s Project Centennial, an operations review and potential restructuring program aimed at improving profit margins. He also talked about how the company is conducting a comprehensive review of their brand portfolio in order to identify additional growth drivers. It’s impossible to know that they will be successful, but it is encouraging to know that management is addressing their current slowing growth issues.

Summary and Conclusions

Flowers Foods is a major force in baked goods throughout the United States. The company has a prudent management team that has a legacy of transforming their business to remain current and relevant. For example, in 2001 they sold their investments in Keebler to the Kellogg Company and spun their bakeries and Mrs. Smith’s bakeries into the company now known as Flowers Foods. In January 2002 they sold their Smith’s frozen food desert business to the Schwan Food Company. I point this out only to illustrate that management is capable and willing to transform their company in order to remain current in the marketplace.

In conclusion, I believe that Flowers Foods represents a reasonably valued high yielding dividend growth stock in today’s overvalued market. However, I think it’s important to recognize that investing in out-of-favor companies requires patience and constant due diligence in order to reap the potential long-term rewards. Personally, I am not too concerned about downside from here. To me the real question is can the company reinvigorate their growth going forward. But even more importantly, will they remain committed to growing their dividend over time. Caveat emptor.

Disclosure: Long FLO

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits