If you are like us and try to read as much economic research and market commentary as you can, you have probably noticed several stories regarding currency hedged government bonds. If you haven’t, then the gist is that even though nominal government bond yields are much higher in the US relative to the other major bond markets in the world (Japan, Europe, and the UK), on a currency hedged basis global government bonds are now trading at a yield parity with one another. The conclusion in many articles is that because of this fact the marginal foreign buyer of US treasuries no longer has any incentive to invest in US treasuries; thus, US government yields could be set to rise. It is unclear how sustainable it is that global government bond yields will remain at currency hedged parity and of course if it is not sustainable then the incentive for foreign bond investors to buy US treasuries could return.

As we noted back in July, the developed market government bond market is dominated by the US, Japan and Europe. Approximately 37% of total debt outstanding comes from the US, 28% from Japan, 25% from Europe and 7% from the UK. So for large international bond buyers, the yield differential between the various regions is huge factor in deciding where to invest. Currently, 10-year US treasuries yield 168 bps compared to 77 bps in the UK, 3 bps in Germany, and -2 bps in Japan. So it would seem that for bond investors investing in the US would be a no brainier, right? Well, not so fast. For investors that want to immunize their portfolios from currency movements currency hedged US treasuries aren’t the slam dunk that have been over the past decade. For European investors, the currency hedged yield of a 10-year US treasury is now actually negative at -2 bps. This is a far cry from the 400 bps currency hedged yield in 2011. The same is true for Japanese investors. In 2010, the currency hedged yield of a 10-year US treasury for a Japanese investor was over 350 bps. It has subsequently fallen to just 1 bps as of yesterday. For a UK investor, and remember nominal government bond yields in the UK are about 75 bps higher than in Japan and Germany, currency hedged US government bonds still offer a higher yield than gilts. The currency hedged yield of a US 10-year government bond is 106 bps or 29 bps higher than the current yield on 10-year UK government bonds.

As the charts above illustrate, it is not the norm (at least since 2009 which is as far back as our cross-currency basis swap data goes) for the currency hedged yields to be at parity. We think it is instructive to breakdown the cost of the hedge into the components to understand how sustainable the current situation is.

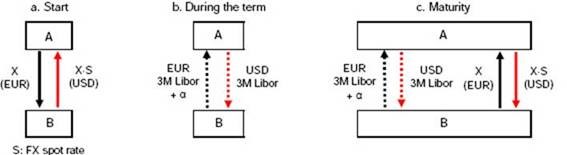

So there are two key components if an investor wants to hedge against currency movements: the price of the basis swap and the spread differential between LIBOR in the two countries.

Basic Mechanics of a Cross-Currency Basis Swap Agreement

source: BIS (link)

Let’s begin with the hedging breakdown from the perspective of a European investor. We will then show the same breakdown for a Japanese and UK investor. The cross-currency basis swap rate between euros and dollars is currently -50 bps. Said differently, this means that it is very expensive to convert euro payments into dollars at the moment. As you can tell by the first chart below, the price of this swap is at a relative extreme level. The second component of the hedging cost is the spread differential between USD 3-month LIBOR and EUR 3-month LIBOR. There tends to be a high correlation between these two series over time. However, right now they are moving in opposite directions. USD 3-month LIBOR has increased from 25 bps in January 2015 to 86 bps as of yesterday. EUR 3-month LIBOR has gone from 5 bps in January 2015 to -32 bps as of yesterday. This means the spread differential is currently at 118 bps. This is the highest such differential since 2007 but you can see that from a longer term perspective that the spread differential tends to oscillate between 200 bps and -200 bps. The current level is squarely in that range. If you take the LIBOR spread differential and subtract the basis swap rate (since the basis swap rate is negative you are actually adding these series together) you can see that the overall cost to hedge euros is the most expensive it has been since 2009.

Here is the same breakdown for Japanese investors. The cross-currency basis swap rate has actually come in a bit and is now -76 bps which is an improvement from -103 bps earlier this year. So it is expensive to convert yen payments into dollars but not as expensive as it was earlier this year. Once again, USD 3-Month LIBOR is moving higher while JPY 3-month LIBOR is moving negative. This means that the LIBOR differential is increasing. It is currently 89 bps which is the widest level since 2008.

Lastly, let’s analyze the hedging cost from a UK investor’s perspective. The cost to convert pound payments into dollars is much cheaper than to convert from euros or yen. It currently is just -13 bps. However, once again the movements in LIBOR rates have gone in completely different directions. Since 1985, USD 3-month LIBOR and GBP 3-month LIBOR have had an 89% correlation. This relationship has completely diverged in 2016 as GBP 3-month LIBOR rates have gone from 57 bps to 38 bps as USD 3-month LIBOR rates have increased from 23 bps to 86 bps. This means that the LIBOR differential has increased to 48 bps which is the highest level 2006. As the third chart below illustrates it is pretty rare for USD LIBOR rates to be higher than GBP LIBOR rates. The currency hedging costs are still high relative to history in the short data series that we have but it is not high enough to completely wash away the fact that yields in the US are higher than they are in the UK on a currency hedged basis.

So just how sustainable is this current market configuration? By far the biggest input in the cost of the hedge right now is the relatively high level of USD LIBOR rates. USD 3-month LIBOR rates are 49 bps higher than 3-month t-bill yields. This is the largest spread since 2011 but it is at a level that was regularly seen in the 1990s. If this spread reverts back to levels seen for the majority of the post-Financial Crisis period, USD 3-month LIBOR rates could shed 20-30 bps which would then once again make it favorable for foreign investors to buy currency hedged positions in the US treasuries. In addition, as we stated above, LIBOR rates tend to move in a highly positive correlated fashion. So if USD LIBOR rates don’t fall back than it would be reasonable to assume that the other LIBOR rates will begin to increase and if this relationship begins to normalize it would lower the cost of the currency hedge. The other component of course is the currency basis swap cost. This is more difficult to make a broader statement about. However, specifically for European investors, it seems that the cost to get dollars is going to remain high and could actually become more expensive. The basis swap cost has shown a remarkably strong relationship to changes in Chinese Forex reserves and changes in the value of the yuan. If Forex reserves continue to decline and the yuan continues to depreciate (which we would view as more likely than not) than the cost of getting dollars will probably get more expensive.

© GaveKal Capital