Achieving long-term success as a dividend growth investor implies a long-term buy-and-hold strategy. The reasons why are simple and straightforward. The primary objective of a committed dividend growth investor is to achieve a growing dividend income stream. This primary objective further implies achieving an increasing level of income that can fight inflation while simultaneously being capable of raising their standard of living over time.

However, you cannot just buy-and-hold any stock; you must buy-and-hold a company that is capable of achieving the long-term results commensurate with meeting your objectives. As I stated many times, it is a market of stocks and not a stock market. Consequently, not every dividend paying stock is a keeper, and successful dividend growth investing implies investing in keepers. Stated more simply, this further implies investing in great businesses - not stocks. The most successful dividend growth investors position themselves as shareholder partners in excellent dividend paying businesses.

The ideal excellent dividend paying business is represented as a company that has consistently produced growing earnings and dividends over time, and the longer - the better. This clearly explains the attraction to premier blue-chip dividend paying stocks found in the Dividend Aristocrats or the Dividend Champions and Dividend Contenders found in David Fish’s CCC lists. To make these lists, these companies must have proven records of increasing their dividends for at least 10 consecutive years (Dividend Contenders), with the premier companies (Dividend Aristocrats and Champions) increasing their dividends for 25 consecutive years or longer.

This is important because it can be all too easy to become attracted to a dividend paying stock simply based on current statistics. Later I will present an example of a dividend paying stock with a very high current dividend yield and an extremely low current P/E ratio. Statistics like those can easily lure the unsuspecting dividend growth investor into investing in a stock that might not be capable of achieving the goals I’ve described above.

General Dynamics (GD): A Quintessential Example of a Keeper

In addition to the attributes of consistent earnings and dividend growth, I believe it is also critical to only invest in a keeper when it is attractively or fairly valued. To demonstrate my point, I offer the following long-term F.A.S.T. Graphs™ on General Dynamics. The orange and blue lines on the graph (both are there) illustrates that earnings growth has been very consistent notwithstanding a few down years. The light green line (it appears white) plots General Dynamics’ dividend since 1997. Although there have been a couple of down years of earnings, General Dynamics’ dividend record has been exemplary. And the reader should note this time period covers both of our most recent recessions (gray shaded areas).

I also chose this example in order to discuss what in some circles generates a controversial discussion. Dividend growth investors are often maligned for stating that they are not concerned with price movement. Clearly, over the timeframe covered on the long-term graph, the stock price (the black line) action of General Dynamics has been challenging. This is especially true during the Great Recession and the three or four years following. However, the primary objective of the dividend increasing each year was perfectly achieved. Therefore, the dividend growth investor who states they are not worrying about price action is simply pointing out that the growing dividend income stream is what matters most. On the other hand, as I will illustrate next, long-term performance through investing in a blue-chip dividend growth stock usually produces above-average capital appreciation as well - in the long run.

The long-term performance associated with the above General Dynamics’ graph illustrates the benefit of buying a great dividend growth stock at value and holding for the long run. For illustration purposes, the calculations are based on a one-time $10,000 investment on December 31, 1996 and held through yesterday’s closing price. This would have purchased 565.37 shares, which would have produced $231.80 of dividend income in 1997.

However, the dividend increased to $248.76 in 1998, and continued growing at a compound average growth rate (CAGR) of 10.6% going forward. In 2015 that original $231.80 of dividend income would have grown to $1560.44. This took the original yield on cost of approximately 2.3% up to over 15.6% by 2015, and is expected to grow again in 2016. Buying and holding General Dynamics over this timeframe clearly met the primary objective of an increasing dividend income stream.

On the other hand, in spite of a few trying years post the Great Recession, the stock price eventually (I contend it was an inevitability) moved into a more rational alignment with the company’s earnings achievement. Consequently, that original $10,000 investment grew to $86,563.80, producing a total annualized capital appreciation rate of return of 11.6%. Add in the more than $14,000 of cumulative dividend income and the total annualized rate of return is 12.4%. Both the dividend income and the capital appreciation trounced the S&P 500 over this timeframe.

Investing in a great business like General Dynamics at fair value is precisely the kind of dividend growth stock I do want. However, as the title of this article indicates, I think it’s just as important for dividend growth investors to recognize and be aware of what they don’t want to invest in. I consider this both important and interesting, because I have always tended to only present companies that I felt were worthy of investment consideration.

Not All Stocks Are the Same: Here Are Examples of What I Don’t Want

My motivation for writing this article is inspired by many comments and even caveats that I have come across regarding the dangers of being a dividend growth investor. For example, I’ve seen admonitions about what happens if the dividend is cut or what if the price drops - to cite just a few. Although it can happen, and has occasionally happened, even within Dividend Aristocrats, I believe it is rarer than some would like to lead us to believe. For example, General Electric is a past Dividend Aristocrat that fell from grace. Nevertheless, I believe a properly diversified portfolio of carefully-selected blue-chip dividend growth stocks provides more than adequate protection.

On the other hand, I do believe that careful selection is key. In this regard, another common warning that is often bandied about is past performance is not a guarantee of future results. Additionally, this is often followed with a statement suggesting that the examination and analysis of historical performance is not valuable. Although I partially agree with that position, we must also understand that in matters of investing, there are no guarantees. Nevertheless, I believe that examining the past operating history of a business is an extremely valuable exercise. Although we cannot invest in the past, we can certainly learn a lot from it.

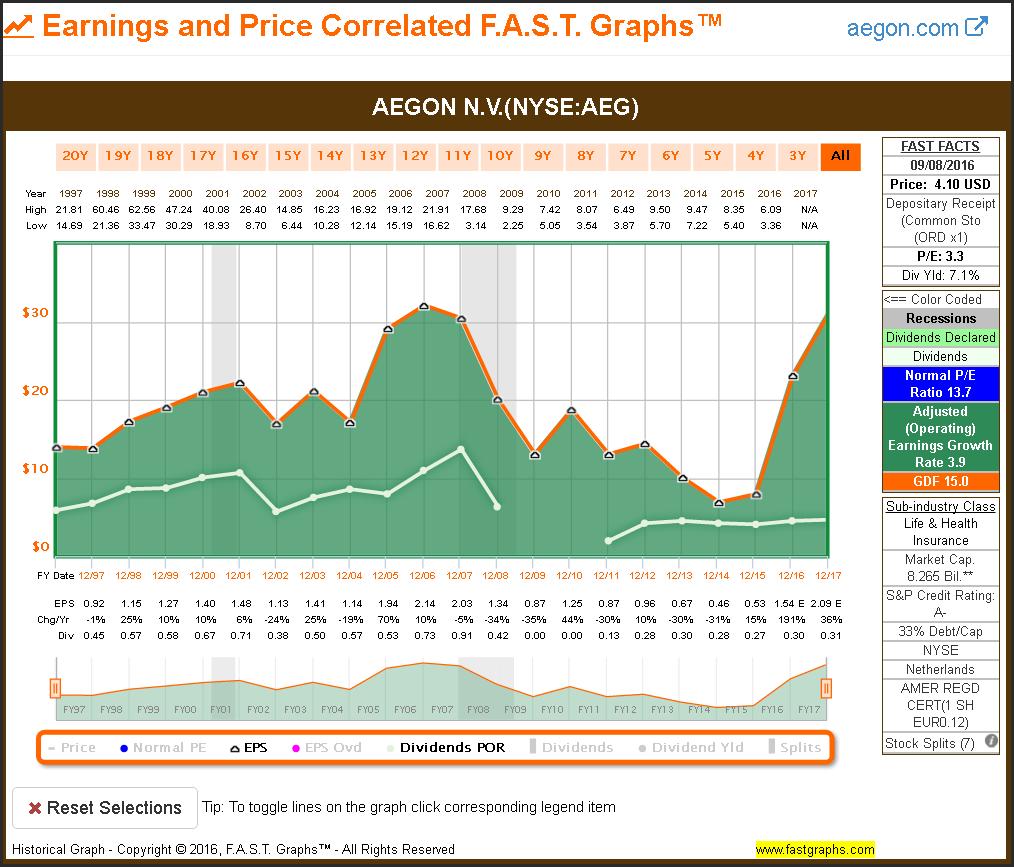

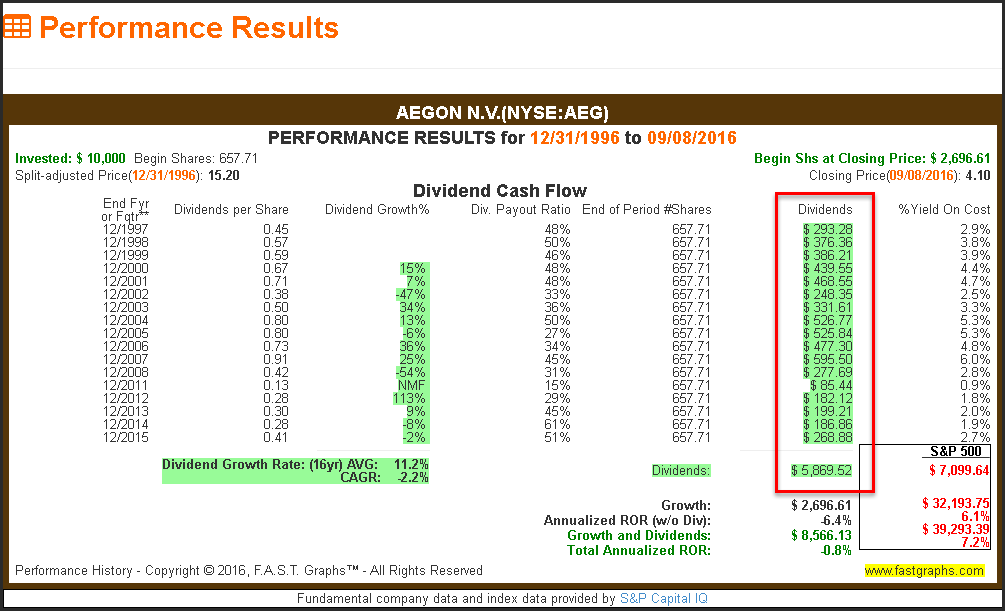

Earlier I stated that I would present an example of a company with a high current dividend yield and low valuation. However, I also warned that current statistics do not always tell the whole story. AEGON N.V. is the example I was referencing. The company currently offers a dividend yield of 7.2% and is available at a blended P/E ratio of only 3.3. Furthermore, the company is A rated and its debt to capital ratio of 33% is reasonable. Based on these statistics, that many investors might rely on, we could assume that this is a very attractive dividend growth stock option.

To be fair, that could very well be the case going forward based on rather enticing-looking estimates of growth over the next few years. Therefore, I want to be clear that I am not suggesting that this is a bad investment choice for certain investors. On the other hand, I do not consider it suitable for the conservative and prudent dividend growth investor whose primary objective is an increasing dividend income stream. I base that position on the company’s historical results, or lack thereof, regarding earnings growth and dividends.

In order to clearly illustrate why this is the kind of company I do not want, I will turn to F.A.S.T. Graphs™ and look at the company’s historical operating history and eventually price and dividend performance since 1997. I will produce several graphs as I build towards a complete illustration of this company’s historical operating record. The first graph looks only at the company’s historical record of earnings (the orange line). Instantly we see that the company’s record has been quite inconsistent - to put it mildly.

AEGON N.V. (AEG)

With this next graph, I add a plotting of the dividends (the white looking line on the graph), and once again, we see a high level of inconsistency. Not only has the dividend been cut more than once, it was totally eliminated for fiscal years 2009 and 2010.

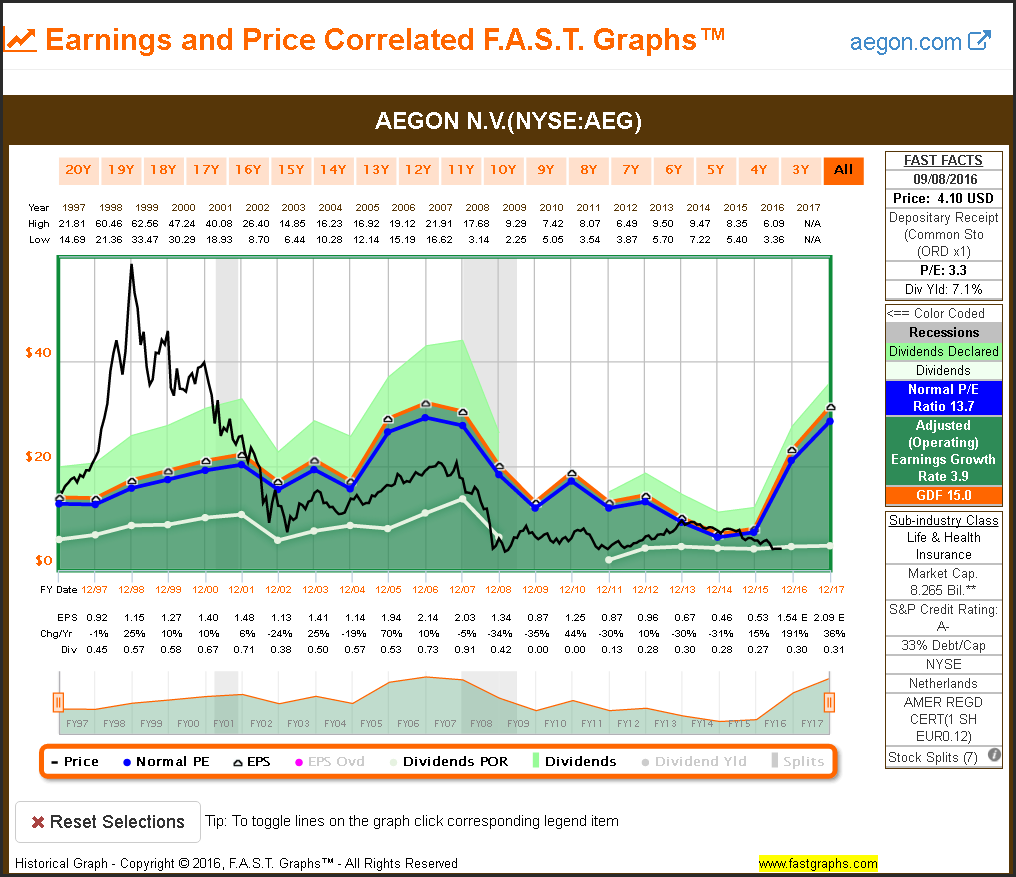

With my final graph, I offer a complete F.A.S.T. Graphs™ to include the company’s historical price action. In my way of thinking, this is clearly not an attractive buy-and-hold candidate for the prudent dividend growth investor. Not all dividend paying stocks are the same. The contrast between this company and General Dynamics is night and day. Maybe past performance is no guarantee, but I for one, would rather bet on General Dynamics’ record than I would this example. It seems like a no-brainer to me.

When comparing the past performance of AEGON N.V. to what we saw earlier with General Dynamics, should crystallize my thesis. I am simply not interested in buying and holding a business that would destroy my capital and interrupt my dividend income stream many times.

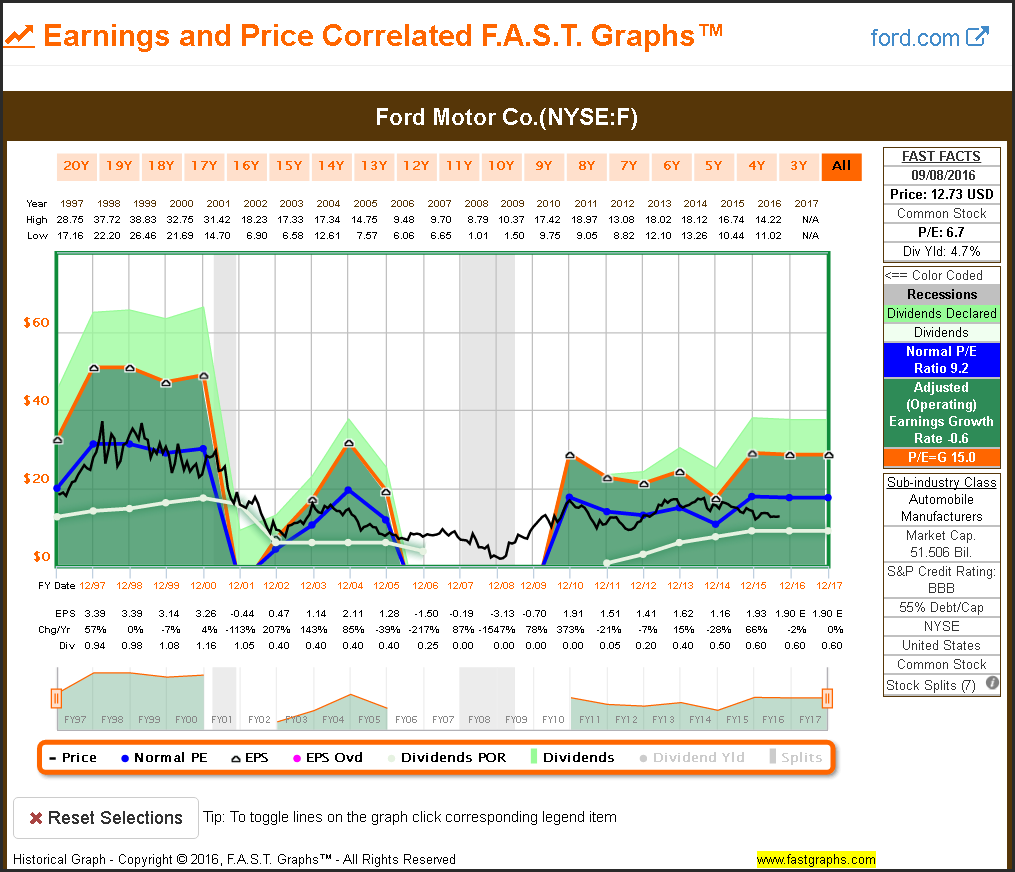

Ford Motor Company (F)

My second example of a company that I do not consider appropriate as a buy-and-hold dividend paying stock is the high profile Ford Motor Company. Once again, the dividend yield is high and the valuation is low. Since a picture is worth a 1000 words, a quick glance at the company’s historical earnings, price and dividend record tells the story.

The long-term performance results of this cyclical company further validate why it’s inappropriate as a long-term buy-and-hold selection. As with the example before, Ford might actually be a good short to intermediate term investment at these levels. However, I find it hard to garner the confidence to believe I can own it for many years to come.

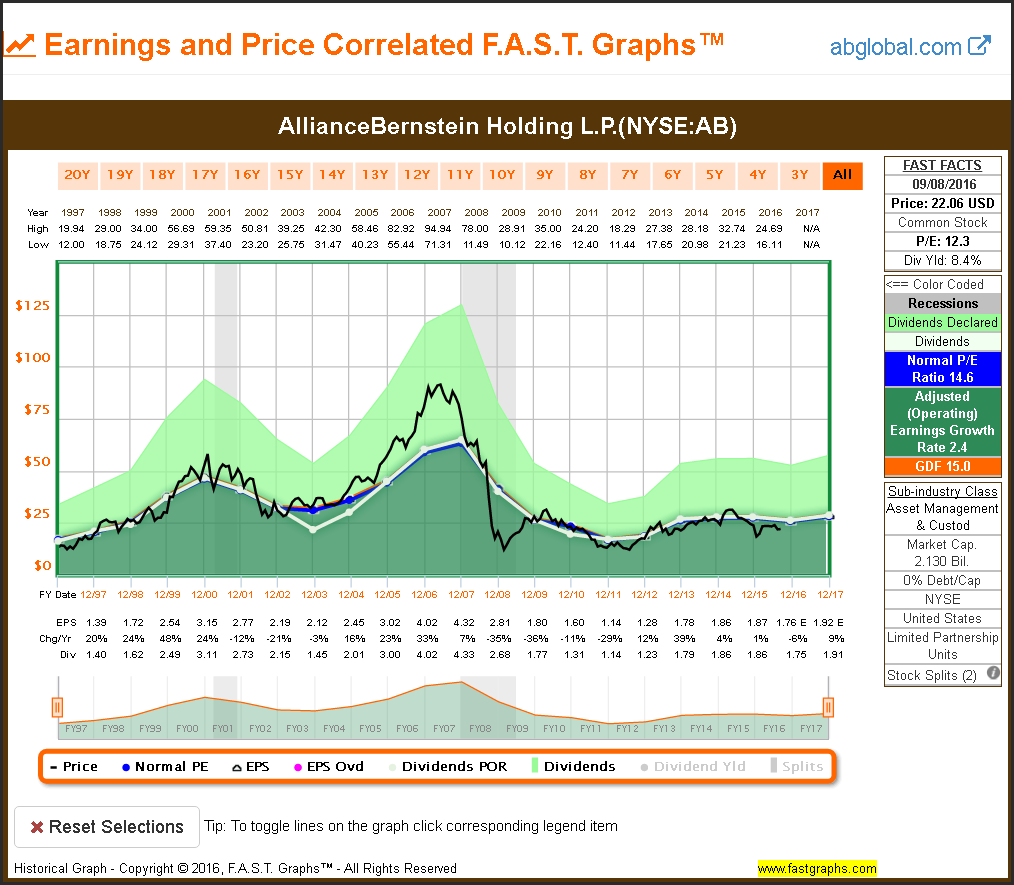

AllianceBernstein Holding LP (AB)

With my third example I throw the reader a ringer - so to speak. AllianceBernstein also offers a very high current yield of 8.4% and an attractive valuation with a blended P/E ratio of only 12.3. The reason I consider this company a ringer is because even though its historical operating history has been inconsistent, it has produced a very enticing cumulative dividend income stream. However, there have been numerous dividend cuts over the years. Furthermore, capital appreciation has not been so hot.

When you examine AllianceBernstein’s historical performance associated with the above graph, there are a couple of things that stand out. This limited partnership has produced an extraordinarily high level of cumulative dividend income since 1997. Long-term investors would have received more than three times the original investment in dividends alone since 1997. On the other hand, there were several dividend cuts along the way.

Therefore, although the income has been significant, it does not meet the objective of a steadily increasing dividend income stream. On the other hand, this could be an interesting selection to include in a well-diversified dividend growth portfolio of mostly blue chips. However, the investor should consider the trauma that would have been associated with the various dividend cuts that happened over time. In other words, it might have been very hard to buy and hold the stock in spite of its results. And finally, capital appreciation, as previously stated, has been rather weak.

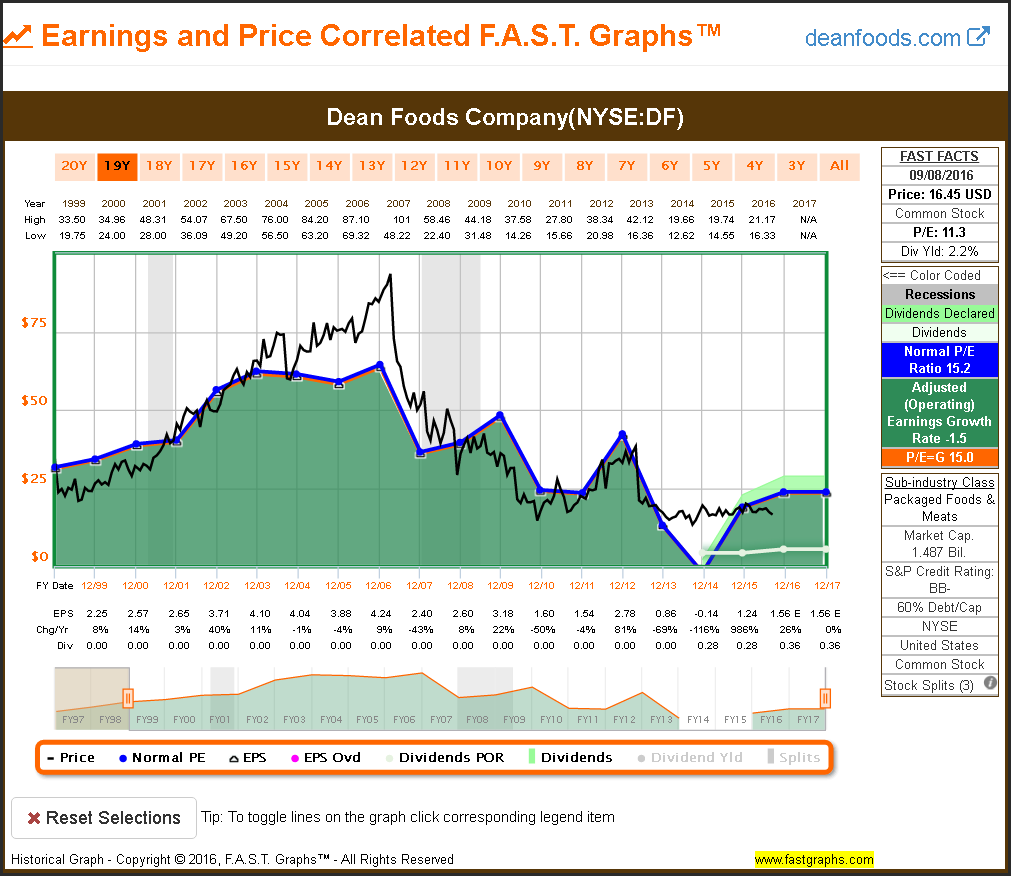

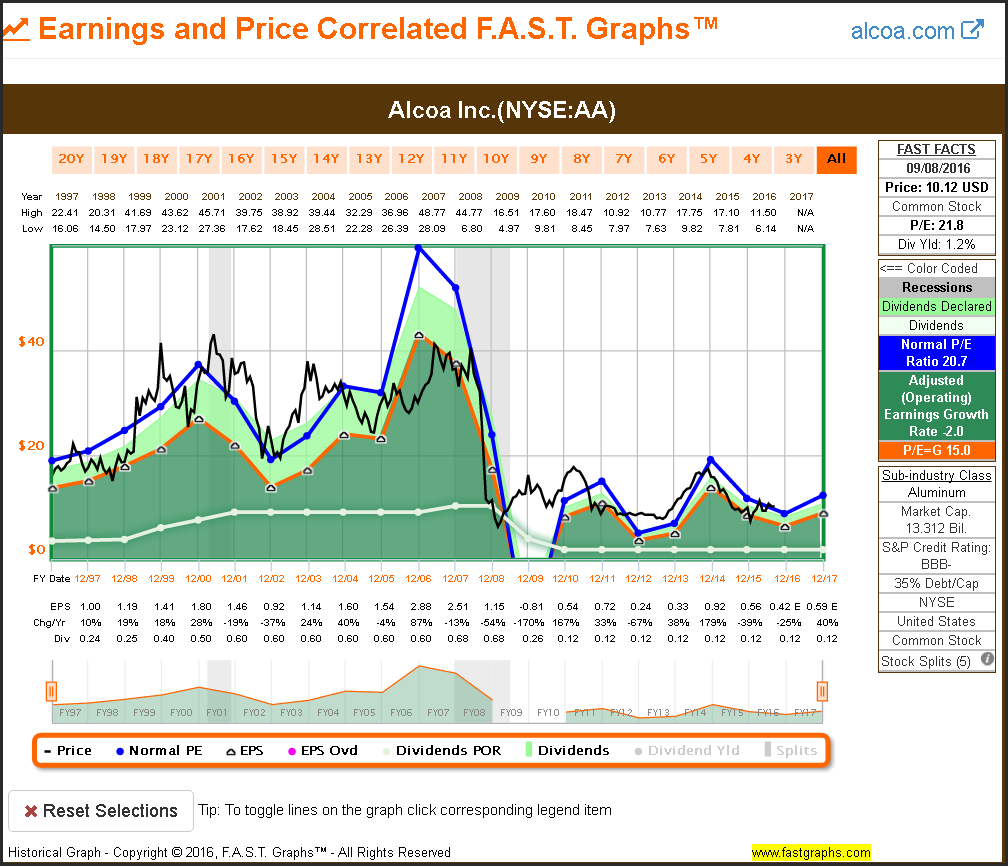

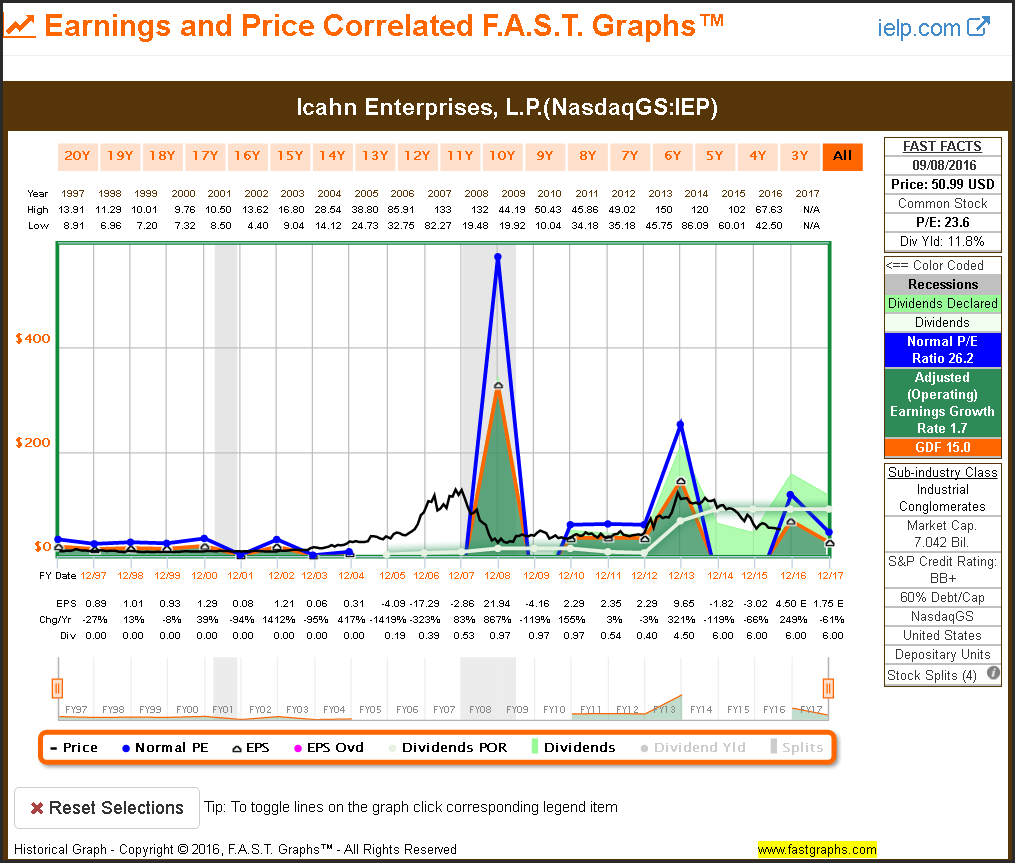

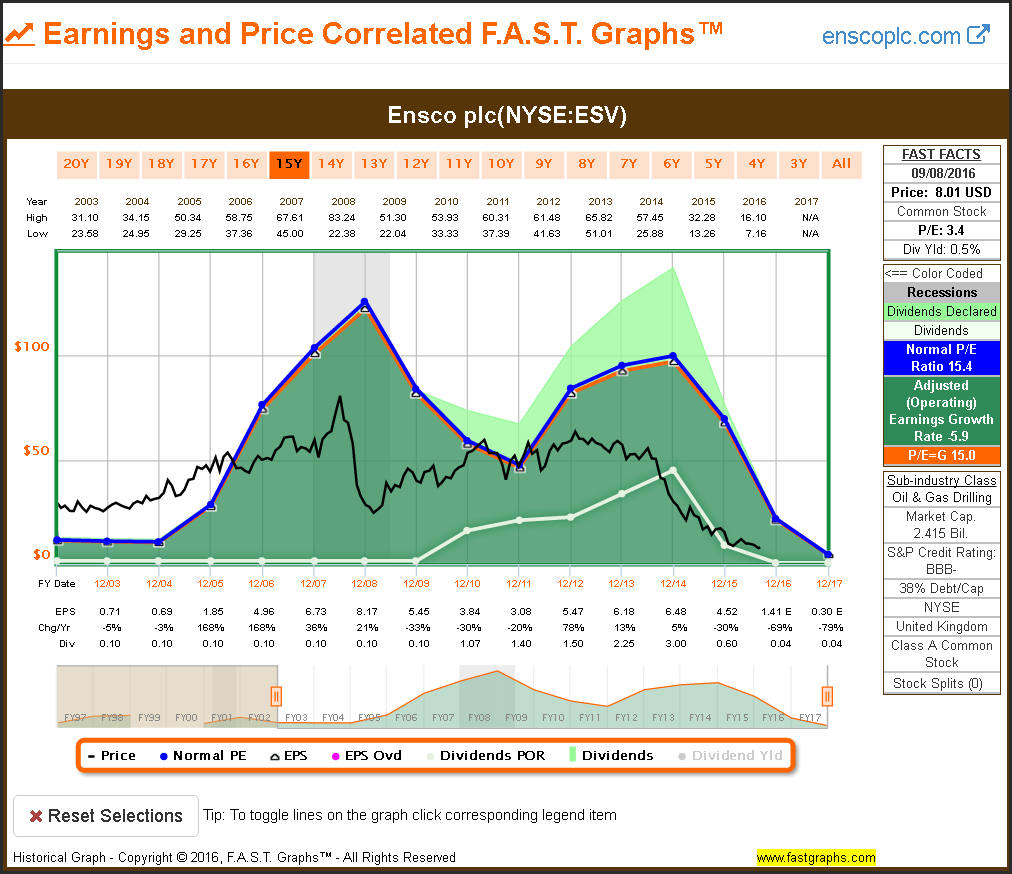

A Graphical Review of What I Don’t Want As a Dividend Growth Investor

One of my primary inspirations for presenting this article was simply to illustrate the undeniable reality that it is a market of stocks and not a stock market. The North American stock market is huge and comprised of more than 19,000 companies that I am aware of. But more to the point, these companies come in all shapes and sizes. With this article, I looked only at stocks that pay dividends; however, there are many companies that do not pay a dividend. Nevertheless, even though all these companies had paying a dividend in common, to a great extent the similarities stop there.

Hopefully, the reader is now somewhat familiar with the graphing tool utilized in this article. Therefore, I offer the following additional examples utilizing only the historical earnings and price correlated graphs. Some of the following names are high profile and likely recognizable, and some are not. But the main point behind this exercise is to illustrate just how different companies and stocks can be even when they share a common trait such as paying a dividend. Most importantly, none of the examples presented below are companies that I would consider appropriate long-term buy-and-hold candidates. A quick glance of each graph and the reader should instantly understand why I take that position. It is a market of stocks, not a stock market.

Summary and Conclusions

Achieving success as a dividend growth investor implies a long-term buy-and-hold strategy. Only then can a rising dividend income stream be achieved. However, it’s imperative that you also carefully select the best possible companies that you can identify. Although there are a lot of companies that pay a dividend, only a select few have proven themselves capable of generating a consistent increasing dividend income stream.

Therefore, I suggest that a careful examination of the company’s long-term operating history is imperative. And finally, it is equally important to conduct a comprehensive research and due diligence effort in order to ascertain whether or not you believe the company will continue to possess the characteristics that attracted you to it in the first place. And always pay attention to current valuation, because it is also a fact that you make your money on the buy side.

Disclosure: Long AB,GD,F

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs