Woody Allen closes “Annie Hall” with a joke: This guy goes to a psychiatrist and says, ‘Doc, my brother’s crazy; he thinks he’s a chicken.’ And the doctor says, ‘Well, why don’t you turn him in?’ The guy says, ‘I would, but I need the eggs.’

That pretty much sums up our relationship with the central banker ruling class. We know that they’re bizarrely out of touch with reality, and we’re terrified of what they might do next. But we go along with the magical thinking crew and smile at their courtiers. Why? Because we need the eggs.

It’s easy enough to rail at the Fed and the stultifying, excruciating, more-of-the-sameness that came out of Jackson Hole. But the larger problem is with us. The bigger problem is that we cannot imagine a solution for our current economic and political problems that does not rely on greater and greater government-directed spell casting. It’s time to wake up. It’s time to begin a new conversation.

Ben Hunt, “Magical Thinking”

Ben was inspired, ok – emotionally motivated by the post-Jackson Hole media parade:

What I’m saying is that we need to focus on empiricism and on what works in the real world, not theory and what “works” as an equation. What I’m saying is that usually the better course of state-directed action is to do less, not more, and the better course of individually-directed action is to do more, not less. (Emphasis mine.)

I smiled and whispered to myself, “What a creative and witty piece.” Amen Brother Hunt, amen. Ben concluded his missive saying, “The problem with magical thinking run amok and its perpetuation of a fantasy world is that sooner or later the dream of the delusional king becomes a real world nightmare for real world people. It’s time to wake up.”

I think we are waking up. Europe is waking up. Brexit moved the needle towards a better Euro solution. We don’t see that right now, but I think we will. Here too, “We the People,” are pissed off and tired of the good old boy fat cat cronyism. We are waking up. Maybe not in this election but perhaps in the next.

Maybe it is a crisis that kick starts fiscal policy action. Perhaps not, but I believe we are turning our lights on. There are solutions. We’ll collectively figure it out. But it will likely be bumpy.

We have a choice as to where we put our energies. My mom taught me years ago to hold joy in my heart and then focus my energies on what it is I want and then to see it as if it has already happened. Then go out and do the wind sprints, she advised — do the work, stay patient, focus on your end goal and you’ll succeed. Collectively, I believe, I mean I know… we can.

Yesterday morning, the August ISM Manufacturing Index fell to 49.4 from the prior high of 52.2. A drop below 50 suggests the economy is contracting. This morning, the odds for a September rate hike dropped after the jobs report missed expectations.

Here’s the rub: Our debt levels and entitlement promises are too large. We have crossed the debt-to-GDP thresholds at which point mucks up the growth engine — here, there and most everywhere. More debt and higher taxes is deflationary. Zero-bound interest rates are deflationary. The economic evidence we measure is deflationary. It’s not working.

We remain in the beginning of a debt deleveraging cycle. We have yet to tackle the big fiscal policy stuff (tax reform, debt restructure, infrastructure spend). For now, expect that we are going to get more eggs.

Ray Dalio sees the potential for a “beautiful deleveraging.” Mohamed El-Erian says we are coming to the T-Juncture. We’ve come to the end of the road and can only turn left or right. One turn finds monetary policy joining hands with fiscal policy. The other turn is not the good road to go down. The better turn sees tax reform and infrastructure spending driven by a bi-partisan effort that surprises us all. Can we believe it will happen? Collectively, I think we must.

Is it the answer? Not sure, but better than the path of higher taxes and over regulation.

Here’s an idea: How about reducing the federal tax rate to zero and funding the annual government budget with newly created currency; however, the annual budget stays fixed at 20% of GDP. Or 18% or 15%. I don’t know. But hold the government size in check to a proportion of our collective annual growth. And assign to pay down the national debt over say, 50 years. That would get us going.

OK – you say… Steve, “You’re nuts.” Maybe, but I much prefer the creative power of this vision versus the destructive power of negative thought. I believe that the good news coming out of the bad stuff is that it is forcing us to “wake up.”

But that’s enough of that. Today, let’s look at valuations and see what they are telling us about probable coming 10-year annualized returns. You’ll find that I also poke some fun at Wall Street consensus earnings estimates. I believe after you see my charts, you too will hold little faith in Wall Street’s “consensus earnings estimates.”

Grab a coffee, find your favorite chair and dig in. Enjoy the remaining few days of summer… You’ll find a number of charts but the read is quick.

Included in this week’s On My Radar:

- U.S. Equity Market Valuations

- The Dirty Harry Jobs Report

- Trade Signals – Overvalued, Sentiment Remains in Bullish Extreme (S/T Bearish for Stocks), Cyclical Bull Uptrend

U.S. Equity Market Valuations

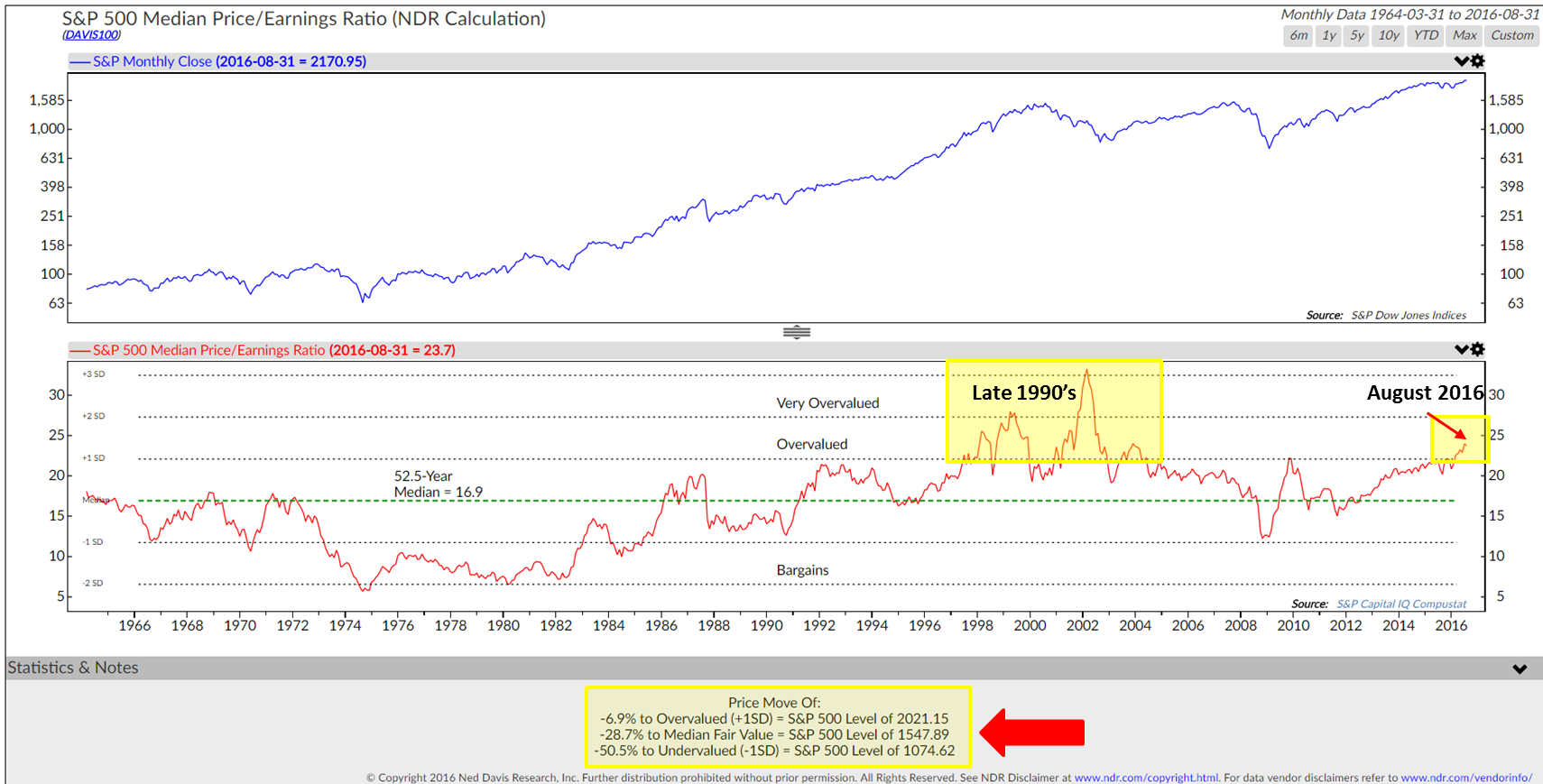

The S&P 500 median price-to-earnings (P/E) ratio was 23.7 on August 31, 2016. Think of “median P/E” (which is based on actual, reported earnings and current price) as the middle P/E (250 stocks have a lower P/E and 250 have a higher P/E).

I like it because it tends to take out the one-off accounting gimmicks. From there we can look at each month-end median P/E number and compare it to other points in time to get a sense if the market is overvalued or offering investors bargains. Further below we’ll sort median P/E into five categories that range from inexpensive to expensive. We are in the most expensive quintile today.

Note the date and small red arrow in the next chart.

Source: Ned Davis Research, Inc. (NDR)

The large red arrow at the bottom of the chart identifies price targets for the S&P 500 Index based on the median fair value since 1964. With the S&P 500 at 2170 at August month-end, the market is 28.7% above its 52-year median fair value. Rarely does a market move more than one standard deviation move above its fair value. It is 6.9% above the overvalued level of 2021.15. OK – it’s expensive but it could grow to be more expensive.

I believe, as fiduciaries, advisors are paid to understand potential risks and rewards for their clients. The above chart quantifies various levels of valuation. Are we going to get a better or worse return on our money? In this way, valuations are very telling in terms of the probable returns investors are likely to receive over a coming period in time.

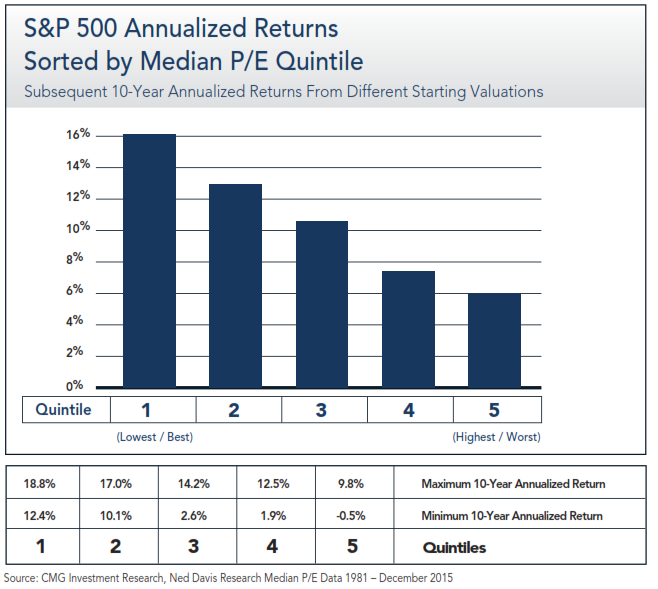

The next chart is something I’ve shared in the past. Note that returns are highest when the market is most favorably priced (low median P/Es) and lowest when the market is least favorable priced (high median P/Es). We are in Quintile 5 today.

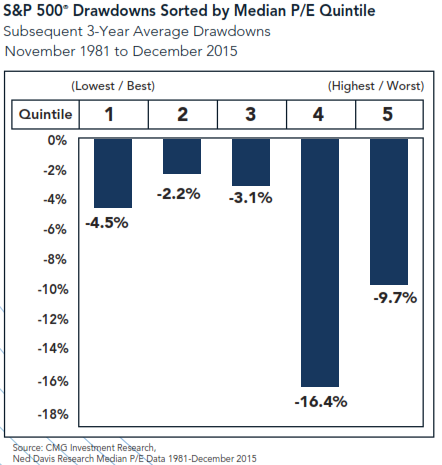

The next chart shows that not only were returns lowest when P/Es are high, like they are today, the risk is actually the highest.

You can find more on this in The Total Portfolio Solution white paper. It suggests an investment plan that is rules-based and limits exposure to assets that are viewed as overpriced and increases exposure to assets when they are considered underpriced. Simple logic, but it takes discipline along with a long-term investment mindset.

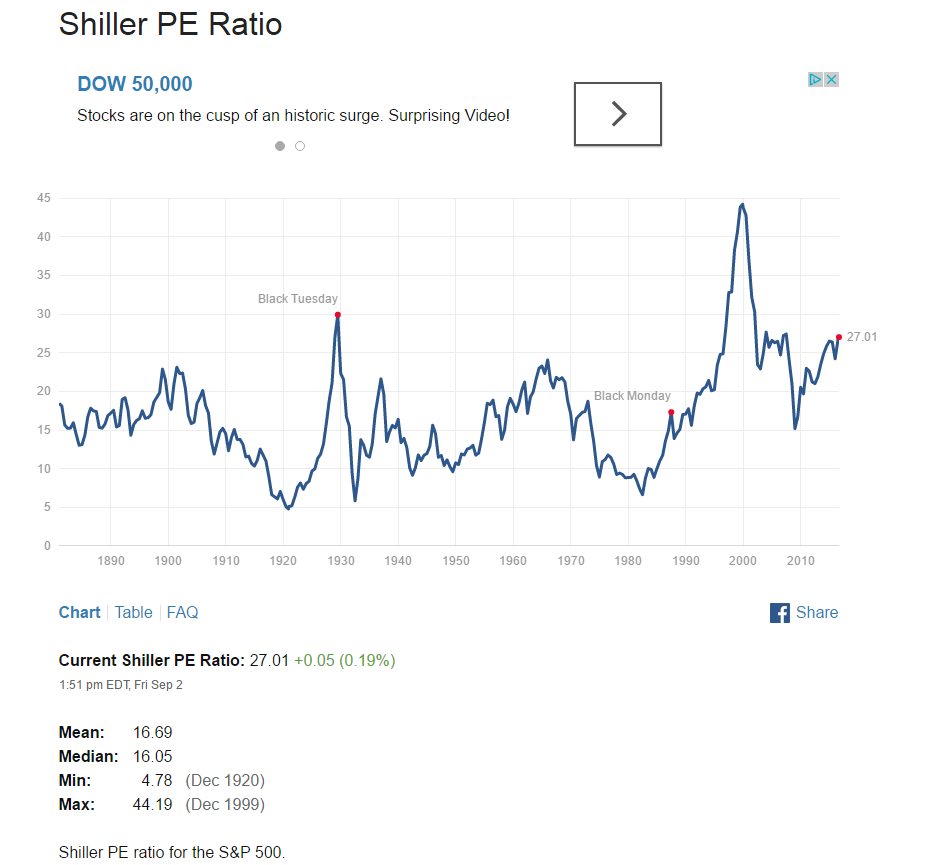

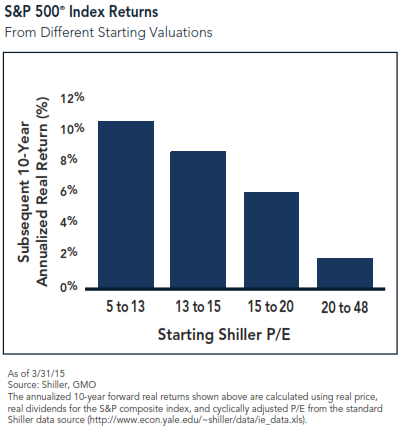

The next chart looks at subsequent 10-year annualized returns based on Shiller P/E. You’ll see five quintiles that range from cheapest 10% of P/E readings (going back to 1881) to the most expensive. It shows what actually happened 10 years following where Shiller P/E was at that time. For example, today Shiller P/E is 27.01.

Next is a look at returns by quartile:

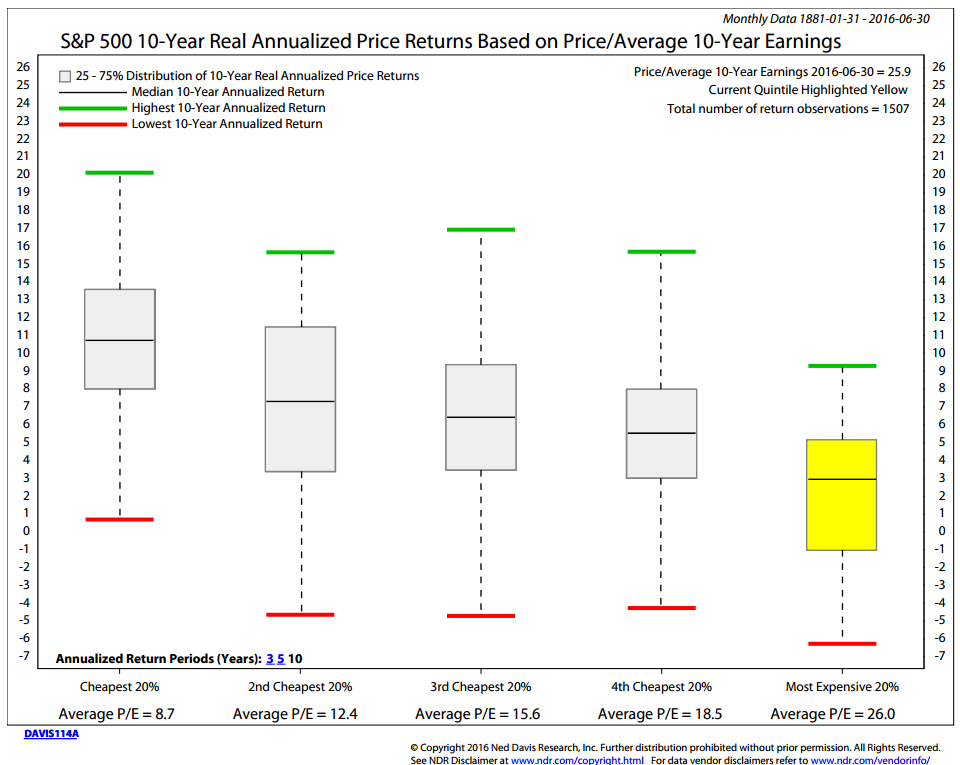

And think of this next chart from a probability perspective. Meaning, what is the likelihood of return based on Shiller P/E valuation. It looks at each month-end P/E and charts the high, low and median 10-year annualized returns based on what actually happened and sorts the returns into five categories. Think of it as real life proof that, when you buy low, you get more for your money. The reverse is true if you buy high.

Take a look at the yellow highlight in the next chart. The median return line of all the 10-year performance incidences that were measured is predicting real 10-year annualized returns of 3%. But there certainly could be outliers as shown. For example, there was one 10-year period out of all the occurrences over more than 135 years where the annualized return was 9.5% when in the most expensive P/E category.

The flip side of that is that there was one 10-year period where the return was -6.25% (red line). For handicapping purposes, focus on the median. The highest of achieved returns is shown in each category (green line) and lowest that happened (red line).

Source: NDR

(By the way, Ned Davis Research is an outstanding service. If you can afford it, get it. Send me a note and I’ll put you in touch with them. I’m thrilled to be a client of more than 20 years.)

I believe we’ll get to the second and third quintiles and, if we are lucky, we’ll get to the cheapest 20% or quintile 1. Then, returns will be the most attractive and the risk reduced.

On November 22, 1999, Warren Buffett commented on the stock market saying, “I think it’s hard to come up with a persuasive case that equities over the next 17 years will perform anything like — anything like — they’ve performed in the past 17. If I had to pick the most probable return, from dividends and appreciation combined, that investors in aggregate … would earn … it would be 6%.” That may prove to be a generous return forecast.

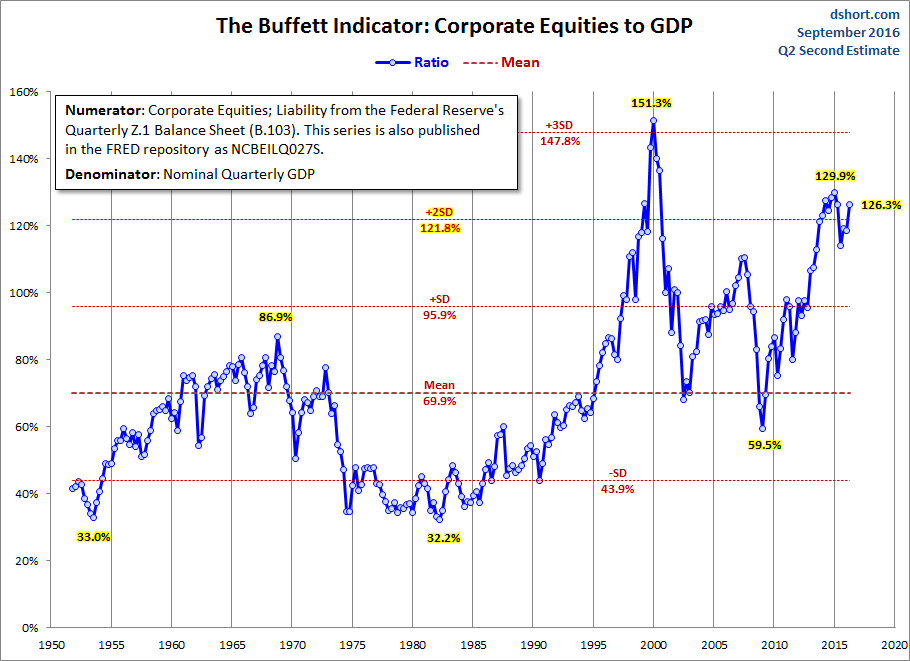

Speaking of Buffett, next is his favorite valuation indicator:

Source: Advisor Perspectives, dshort.com

What does this chart tell us? It is from Jill Mislinski of Advisor Perspectives, “In a CNBC interview in 2014, Warren Buffett expressed his view that stocks aren’t ‘too frothy.’ However, both the ‘Buffett Index’ and the Wilshire 5000 variant suggest that today’s market remains at lofty valuations — still above the housing-bubble peak in 2007, although off its interim high in Q1 of 2015.” (Source: Advisor Perspectives.)

Note that while these indicators are a good gauge of market valuation and probable 10-year forward returns, they are not useful for short-term market timing.

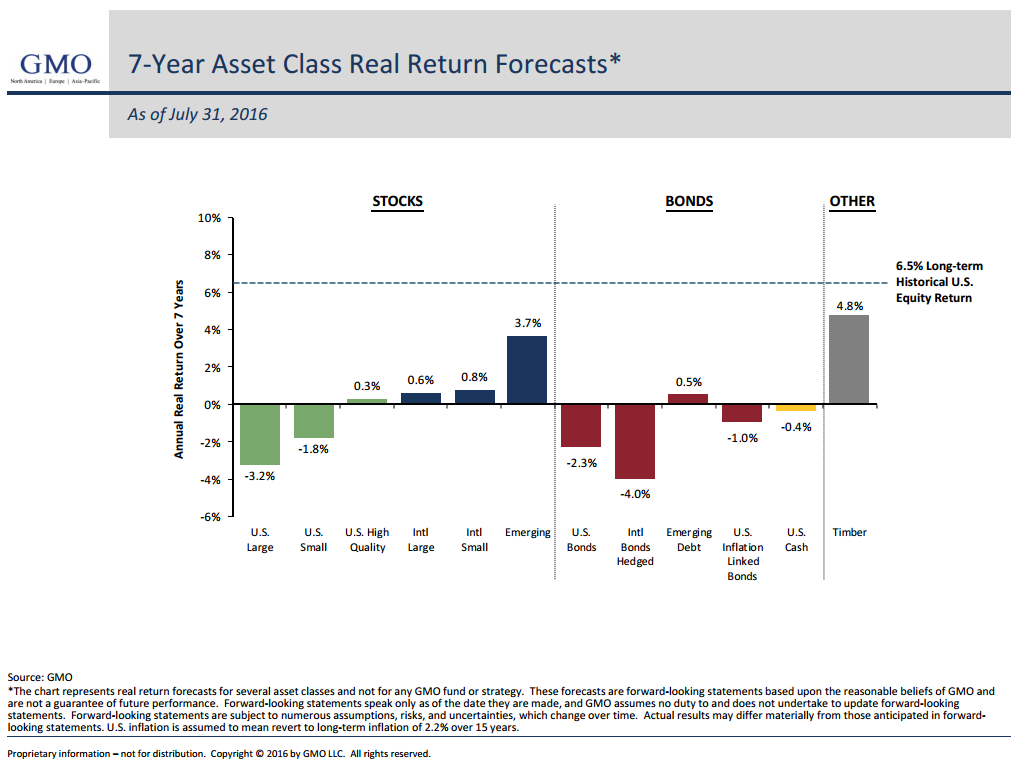

I mentioned last week that in 1999, GMO was forecasting a negative real return for the stock market of -1.9%. Many thought they were crazy. Then UNC Management Company (Endowment) Founder, President & CIO Mark Yusko was chastised by a board member about his negative forward return view on equities. The board member had his equity market love goggles on. Yusko and GMO were right.

GMO is currently forecasting a -3.2% annualized real return for large-cap equities over the coming seven years.

Like the UNC board member in 1999, your clients may have the stock market love goggles on. Feel free to share this post with them.

Consensus Earnings Estimates

I bet that you, like me, get a number of client calls that reference a Wall Street report touting forward P/Es. They watched an analyst on TV saying P/Es are cheap based on next year’s earnings estimates. The analyst compared that forward estimate based P/E, which is 17.20 as of August 31, 2016, to 23.7 (median P/E) or 26 (Shiller P/E) and says the market is not so richly priced.

Not only is that poor analysis, if you look at forward P/E and compare it to other periods in time, you’ll see that the current level is as high as it was in 2007 and higher than any other period since the 1960s with the exception of the late 1990s and early 2000s.

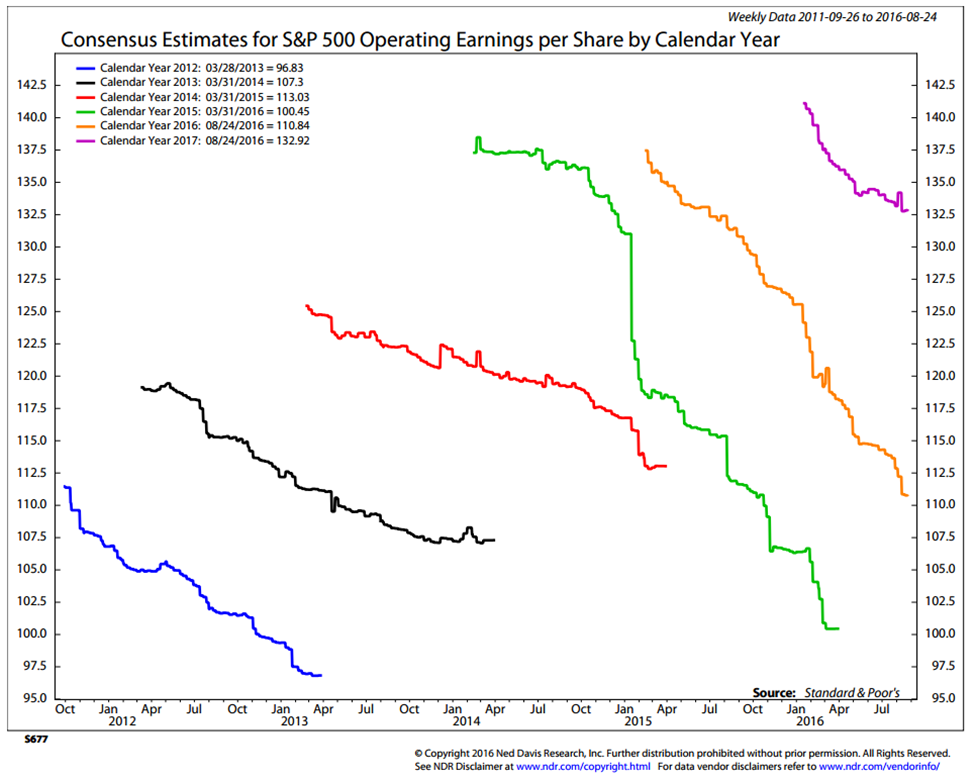

With that said, here is the main reason I don’t rely on Wall Street “consensus” earnings estimates. The next chart shows year by year where Wall Street’s estimates began and where they finished up. For example, look at the 2016 estimates (orange line). Back in March 2015, the consensus earnings estimate for 2016 was approximately $137.50 in operating earnings per share for the S&P 500. The most recent estimate, as of August 24, 2016, is $110.84 per share.

Take a look at each year. Note how it started high and how much it declined by the time the actual numbers were reported. Keep in mind we won’t know 2016 numbers until Q1 2017. And we won’t have 2017 numbers until Q1 2018. My simple point is… how can we rely on forward P/E based on Wall Street’s earnings estimates? I can’t.

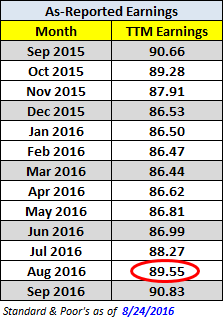

Finally, following is what has actually happened:

Compare that September 2016 $90.83 actual per share number to the 2016 estimate number that started at $137.50 per share and now sits just above $110 per share (orange squiggly line in chart above). Can we get there over the remaining four months? No way.

Further, tell me how in a 1.50% GDP world our corporations can grow their businesses to hit that $132.50 per share 2017 estimate? $90.83 actual to $132.50 by the end of 2017. Also, not going to happen.

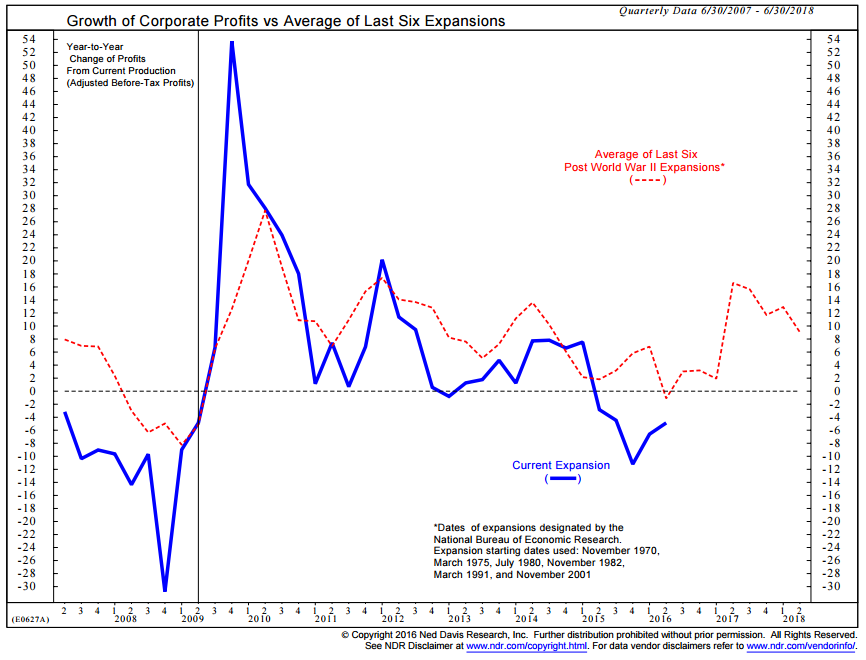

And despite all of the eggs that we have gotten, the next chart shows the growth in corporate profits and compares it to the average of the last six expansions. Something is structurally wrong here. Do you agree?

Don’t trust forward P/E based on consensus estimates. I favor handicapping probable forward returns based on actual reported earnings… I like median P/E.

The Dirty Harry Jobs Report, by Danielle DiMartino Booth

I just love how the former Fed insider writes. Danielle is brilliant. In “The Dirty Harry Jobs Report,” Danielle takes a look at today’s jobs numbers and various other economic data. She begins:

“For avid film critics, comparing one big screen hero of the action variety to another is serious arm chair sport. Recent favorites in the critic’s corner: James Bond’s suave but strong Daniel Craig vs. the no nonsense badass of the Bourne series’ Matt Damon. The contrasting characters uncannily align with what was on offer to 1971 moviegoers. Sean Connery was turning James Bond into a legend, ordering his martinis, “Shaken, not stirred,” before saving the world in Diamonds are Forever.

And then there was Clint Eastwood as Dirty Harry and the moment that secured his spot in the Badass Hall of Fame. Close your eyes, and recall that scene we’ve all seen: From his vista at a local San Francisco diner, Inspector “Dirty” Harry Callaghan observes a bank robbery in progress. He proceeds to calmly kill two of the robbers and wound a third, to whom he had this to say:

“I know what you’re thinking: ‘Did he fire six shots or only five?’ Well, to tell you the truth, in all this excitement, I’ve lost track myself. But being this is a .44 Magnum, the most powerful handgun in the world, and would blow your head clean off, you’ve got to ask yourself one question: ‘Do I feel lucky?’ Well, do you punk?”

Investors no doubt went into this morning’s August jobs report asking themselves the same question, whether they too felt lucky. It’s a good question, all things considered.”

There is much more in her piece like:

- Bank Credit Analyst reckons that valuations on the stock market are near record levels as gaged by median PE (we covered that above).

- She said this about the jobs number out this morning: “Forget the abysmal pace of job creation in May – that paltry 24,000 figure was an aberration. By the same token, discount the strength in June and July, where average gains of 273,000 also look deceptively high.

- Focus instead on the 12-month average of 204,000. That’s the best yardstick against which to compare August’s 151,000-gain, which fell short of consensus estimates of a 180,000 gain.

- On the ISM report: “By far the biggest surprise arrived with the headline miss for the August Institute for Supply Management manufacturing report, which fell far short of estimates.

- Yes, the factory sector is a small part of the economy, but manufacturing’s tendency to lead the direction of economic growth stands firm.

- With that, the employment sub-index within the ISM was 48.3 in August and has been south of 50 for 9 out of the last 11 months; 50, you may recall, is the line in the sand that divides expansion from contraction.

- And this on the Recession Watch front: The national ISM, it should also be noted, saw backlogs decline by 2.8 points to 45.5, the lowest level in 7 months, which does little to presage strength as we head into the fall.

- “Disequilibrium like this does not last,” warned AIG’s Head of Business Cycle Research, Jonathan Basile. “If the Chicago backlog starts printing consistently below 40, that’s a slam dunk recession signal – and we’re talking every postwar cycle.”

- Basile also worries about what the folks who hold the keys to the credit kingdom have been reporting. Though not a commonly considered labor market proxy, it would be best to not dismiss the National Association of Credit Managers Index.

- In August, it fell to a seven-year low for both manufacturing and services suggesting revenue pressures are building. We won’t know for sure until third quarter earnings are released. But you’d best listen to credit managers – they get paid to know whether or not their employers are going to get paid.

She concludes with this: “Taking in all of the data, the labor market expansion is exhibiting signs of exhaustion, as in acting very late-stage. A turning point would appear to be upon us. If the August slowdown does presage an inflection point, the Fed’s determination to hike rates by year end will be severely tested in the coming months. It’s as if the data are taunting the Fed to commit a policy error, which brings to mind an even more famous Dirty Harry line. Of course you know what’s coming: “Go ahead, make my day.””

Here is a link to the full piece.

Trade Signals – Overvalued, Sentiment Remains in Bullish Extreme (S/T Bearish for Stocks), Cyclical Bull Uptrend (August 31, 2016)

S&P 500 Index 2165

Posted each Wednesday, Trade Signals looks at several of my favorite stock, investor sentiment and bond market indicators. It is my weekly risk management dashboard, designed to keep me better in sync with the major technical trends. I hope you find the information helpful in your work.

Click here for the most recent Trade Signals blog.

Concluding Thoughts

If the stock market was attractively priced and probable 10-year forward returns high, I’d say overweight equities and expect good returns and a pretty smooth ride. The opposite holds true today. My view remains the same, underweight equities, diversify and hedge.

Expect a bumpy road in the stock market, stay patient and prepared to take advantage of the opportunity the next recession creates.

For now, the trend is up and the eggs keep coming. Most of our indicators are bullish. High yield and fixed income have done very well. Tactical All Asset is doing reasonably well. We’ve seen somewhat mixed managed futures strategy returns, generally flat to up, but I like the return potential and risk management/diversification benefits. Find good managers. I am happy to share a few ideas with you.

Money compounds over time by limiting loss. I believe we should keep risk management front of mind.

Personal Note

“To refer to a personal taste of mine, I’m going to buy hamburgers the rest of my life. When hamburgers go down in price, we sing the ‘Hallelujah Chorus’ in the Buffett household. When hamburgers go up in price, we weep. For most people, it’s the same with everything in life they will be buying — except stocks. When stocks go down and you can get more for your money, people don’t like them anymore.”

— Warren Buffett on the stock market (December 2001)

Speaking of hamburgers, one last long summer weekend is ahead. I’ll be manning the grill. But before I do, there is a big game this afternoon for the Shipley Gators. This year they are playing for something much bigger than themselves. Tragically, they lost their captain and best player a month ago. The family, the team and the entire community is hurting. Especially the family. There are no words.

My son Matthew is a senior (number 6 in the center) this year with eyes on Penn State next year. Of course, that is music to my PSU ears. Kyle is a junior goalie and is positioned directly behind him in the blue jersey. I’ll be attending every game I can. It is such a wonderful time of life.

I’ll be speaking on portfolio construction using ETFs at the Morningstar ETF Conference on September 7-9 in Chicago. If you are going to be there, shoot me a note and let’s grab a coffee. Denver follows on September 13-15 where I’ll be attending a one-day S&P Dow Jones Indices forum entitled “Managing Risk Without Curbing Returns.” A meeting with John Mauldin and team follows the event.

Late September finds me in Charlotte (a business meeting to be followed by golf at Quail Hollow), then a speaking engagement in Indianapolis on the 22nd, followed by a trip to NYC for the Bloomberg Most Influential Forum September 27-28. Lou Holtz is the keynote speaker and the Indianapolis event is hosted by one of our advisor clients. I’m really looking forward to meeting and listening to Coach Holtz. That should be fun.

If you find the “On My Radar” weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles I feel are worth the read on twitter. You can follow me @SBlumenthalCMG.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Have an outstanding weekend. Wishing you and your family the very best!

I see a yummy Ballast Point Grapefruit Sculpin IPA in my immediate future. With beer in hand, I’ll raise my glass and toast to you and to me and to great optimism now and forever in our future.

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group