Introduction

It is no secret that US blue-chip dividend paying stocks are trading at extremely high valuations relative to historical norms. Interest rates remain at all-time lows, and investors hungry for yield have turned to blue-chip dividend growth stocks in order to satisfy their appetites. For the past seven years or so that strategy has worked out quite well on both a capital appreciation and dividend income growth basis. Seven years is a long time, and the longer that the bull market in blue-chip dividend growth stocks runs, the more complacency it breeds.

Complacency leads to overconfidence, and in my opinion, for investors there is only one thing more dangerous than greed. That, of course, is fear. Complacency takes time to develop until it eventually turns into greed. However, since fear is a much more powerful emotion, it can grab hold of investors almost immediately. Succinctly stated, greed is fragile while fear is potent.

Warning: You Make Your Money on the Buy Side

This is critically important, because if you are lulled into complacency by a long bull market and suddenly a bear market appears, confidence is shattered and panic sets in. As a result, it is quite common for investors to hold on too long during a bull market and then panic sell as prices fall below intrinsic value when the inevitable bear market comes. This simply defines the classic buy high- sell low mentality or trap that many investors fall into.

Investor psychologists have asserted that investors feel the pain of loss two and a half times greater than they do the pleasure of gain. Therefore, we are often too patient when the bull is running and too impatient when the bear attacks. Investors should consciously keep this reality in the forefront of their minds - all bull markets end with a bear market - and vice versa.

However, I want to be crystal clear about one thing. What I am warning about is not holding onto stocks too long during a bull market. This is not a bad practice if the stocks were purchased at a sound valuation in the first place. Instead, my warning is referencing paying too high a valuation for stocks in the late innings of the bull market. Paying too much for even the best companies will rarely lead to acceptable long-term returns. Paying too high a value at original purchase assumes too much risk with too little result in the longer run.

I believe it is an irrefutable and absolute fact that common stock investors make their money on the buy side. When you adhere to the discipline of only purchasing a common stock (no matter how strong the company) when fair valuation is manifest, your strategy is prudent and your long-term returns will be greater with less risk taken. Furthermore, when you follow a prudent valuation oriented investing strategy at initial purchase, you don’t have to worry too much about the inevitable bear market coming along.

There is a logical reason why I believe investors should not be fearful of a bear market, assuming they purchased great businesses at sound valuations in the first place. Historically, bull markets have lasted approximately 3 ½ times longer than bear markets. Remember what I said earlier, fear is a much stronger, and therefore, more dangerous emotion than greed.

Consequently, I believe that many investors subconsciously react stronger to bear markets than they do bull markets. But in reality, bear markets tend to be rather short in duration compared to bull markets. This is the primary reason why I believe it is rational to hold on to attractively purchased stocks through bear markets. The following slide courtesy of Mackenzie Investments clearly illustrates the comparative duration of bull markets versus bear markets:

If Most US-Based Blue-Chip Dividend Growth Stocks Are Overvalued, What Can I Do?

For starters, you can consider that it is a market of stocks and not a stock market. Therefore, you can look for pockets of value within an otherwise overheated market. With my last two articles I highlighted several dividend growth stocks in the US market that I considered attractively valued for new money to invest in. On the other hand, the US market is not the only market out there. With this article, I am going to look to the Toronto Stock Exchange of our Canadian neighbors to the North for attractively valued dividend growth stocks. However, I am going to limit my first examination of Toronto Stock Exchange selections to the Canadian banking industry. My primary goal is to identify not only attractively valued high yielding Canadian stocks, I am also concerned with prudence and reliability.

The Toronto Stock Exchange is quite different than the major US stock exchanges. A recent report on international investing in “the balance” described the makeup of the Toronto Stock Exchange as follows:

“The Toronto Stock Exchange consisted of over 1,500 companies, as of 2016, worth a total of $2.8 trillion in market capitalization. While the majority of these companies are based in Ontario (52%), a substantial portion of the exchange's market capitalization also comes from Alberta (25%), due to the region's rich natural resources - namely, oil and gas in the oil sands.

The exchange's breakdown of sectors by market capitalization shows a skew towards financial services (38%), energy (20%) and materials (10%), while industrials and consumer discretionary round out the top five sectors. Many of these companies consist of so-called junior mining companies focused on developing natural resources.”

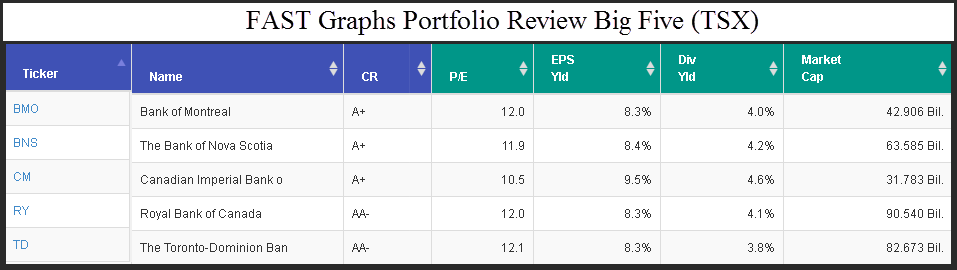

Therefore, since the majority of Toronto Stock Exchange listed companies are skewed towards financial services, I chose to cover this sector initially. The following portfolio review looks at the colloquially named “Big Five” largest banks that dominate the Canadian banking industry. The review is produced with TSX listings and is in alphabetical order. It reports each company’s credit rating, current P/E ratio, earnings yield, dividend yield and market cap.

Important Considerations Before Investing in Canadian Banks

If you are a Canadian citizen, then I would argue that investing in any of the “Big Five” Canadian banks is a rather straightforward decision. There are many institutions that consider Canadian banks some of the soundest banks in the world. Later, when we look at their individual historical operating histories, that statement will be validated.

However, if you are a US citizen, the issue becomes slightly more complicated. All of the “Big Five” Canadian banks are cross listed (interlisted) on the NYSE and the TSX. However, according to Charles Schwab and Company, US and Canadian shares are not fungible. Therefore, investing in a cross-listed stock requires that you hold the stock in US dollars and receive US dollar denominated dividends. Consequently, currency exchange rates will come into play. Moreover, for US citizens, there will be times when the exchange rate goes against you, and times when the exchange rate benefits you.

Additionally, there are no tax implications for buying cross-listed stocks because you get a tax credit against your US tax bill. For example, Fidelity explains the rules that apply to the Canadian withholding tax for their firm as follows:

“The Canada Revenue Agency (CRA) allows Fidelity to automatically apply favorable withholding tax rates if all of the following conditions are met:

- The account holder is a nonresident of Canada who is either an individual who has an address in a country with which Canada has an applicable tax treaty; or a trust with a trustee who has an address in a country with which Canada has an applicable tax treaty.”

Charles Schwab and Company discusses the tax situation for their firm as follows:

“The tax implications for buying cross-listed stocks are the same as an ADR, OTC or a foreign ordinary. If you're a U.S. citizen holding a cross-listed stock in a taxable account and pay tax in a foreign jurisdiction, you'll generally get a tax credit against your U.S. tax bill.”

With these considerations in mind, I will be presenting each of the “Big Five” Canadian banks utilizing F.A.S.T. Graphs™ on each for both their NYSE listing and their TSX listing. The NYSE listing will be reporting in US dollars (USD), while the TSX listing will be reported in Canadian dollars (CAD). However, from an analytical perspective regarding the quality of the company’s operating history, I believe the country of origin listing is the most appropriate to analyze each bank with. Nevertheless, there will be slight differences on the graphs of each company in each respective listing primarily due to currency exchange rates.

Differences When Evaluating Banks

Before I get into the particulars of each of the “Big Five” Canadian banks, a few comments regarding how to value a bank are in order. Banks, insurance companies and other financial service firms require slightly different valuation models. The most prominent differences are found in the definitions of debt and reinvestment, the rules that govern bank accounting, and that they are heavily regulated businesses.

For banks, debt is more similar to inventory or product than it is a source of capital. A bank makes its money on the spread between the interest it pays on the money it raises (deposits) and the interest it charges to those who borrow money from the bank. Consequently, with banks you can think of debt as a raw material, not capital. (Note: for these reasons F.A.S.T. Graphs™does not report debt to capital on banks.)

Regarding accounting rules, the assets of the bank are primarily financial instruments such as bonds and securitized obligations that have an active market place. Consequently, since these securities are publicly traded, they therefore have a very definable market value. As a result, accounting rules require banks to apply mark to market accounting of their assets and financial statements.

The advantage is that a bank’s assets are precisely priced with little subjective judgment applied. The disadvantage is that market values can actively fluctuate. This creates difficulties in calculating metrics that apply to other types of companies such as returns on equity or assets. This also makes estimating the cash flows of the bank difficult, if not impossible.

A high degree of regulation also requires the banks set aside reserves for loan losses. This also causes problems with attempting to apply traditional valuation methods when valuing a bank.

A Short F.A.S.T. Graphs Tutorial

Each “Big Five” Canadian bank example will be presented utilizing the earnings and price correlated F.A.S.T. Graphs™ on each. Therefore, for the reader to get the most benefit from this exercise, it's imperative that you understand what each of the earnings and price correlated graphs are revealing.

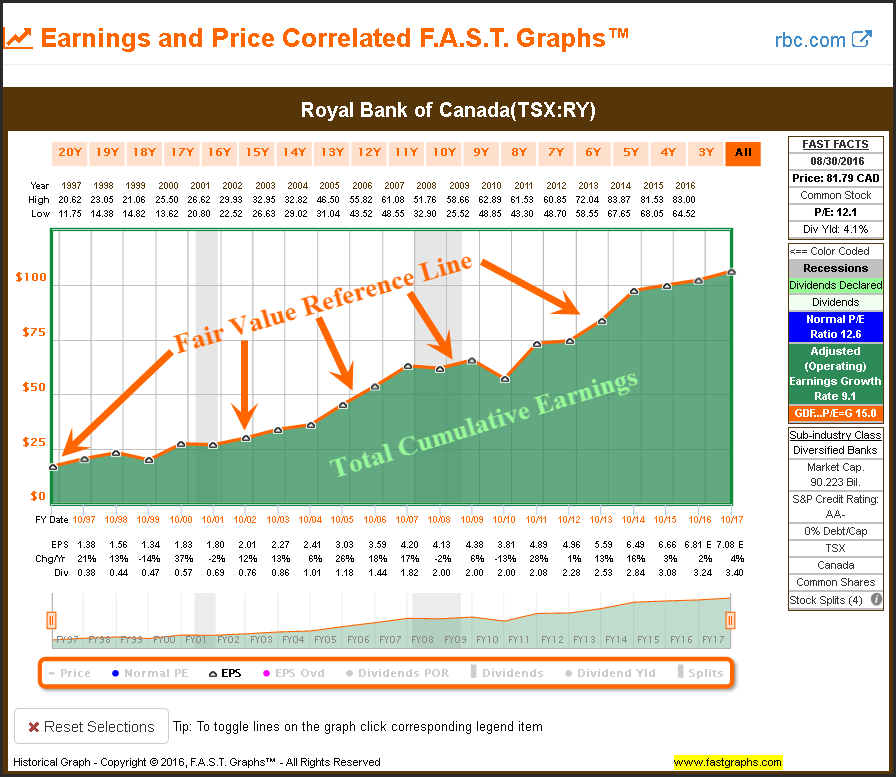

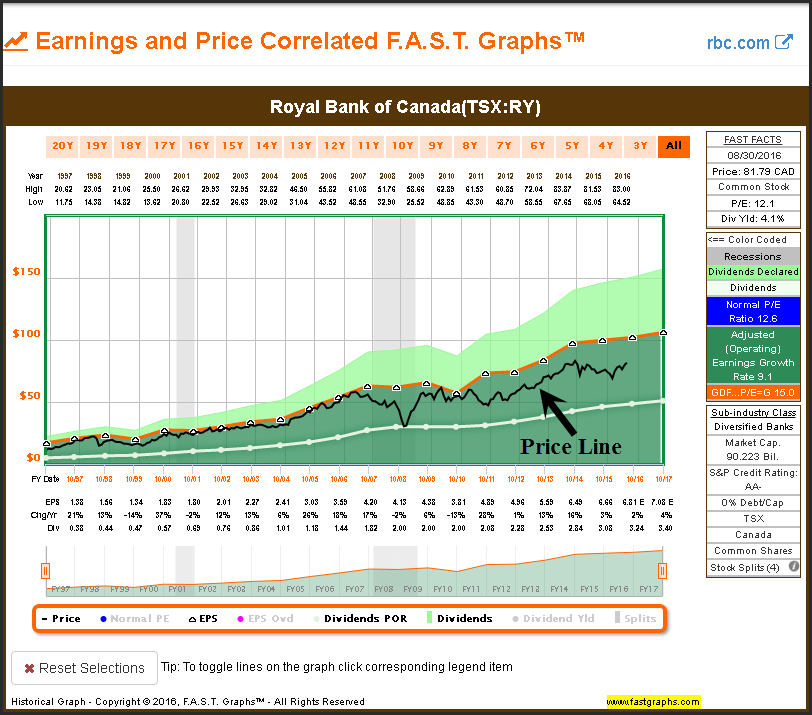

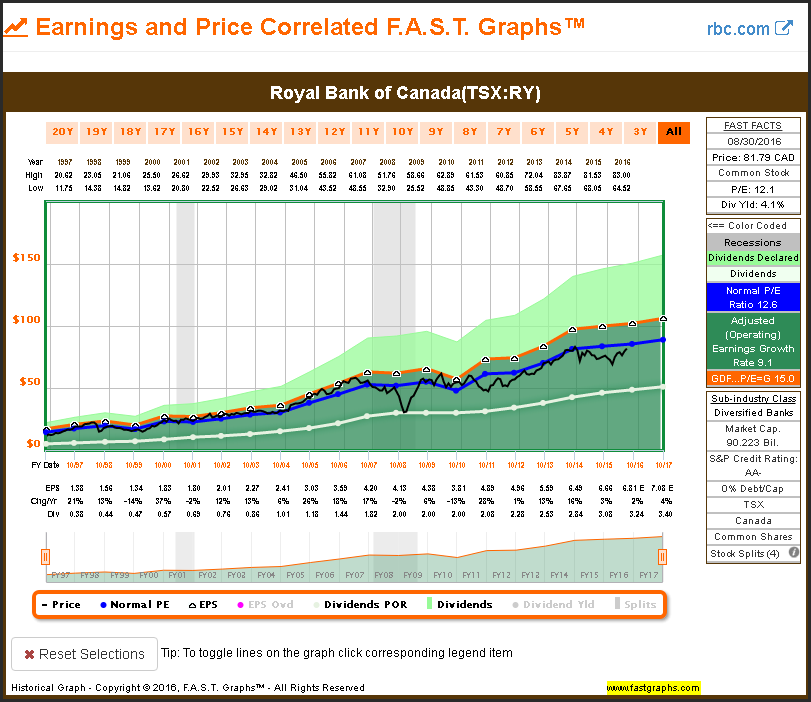

Therefore, I offer the following short tutorial where I take a complete F.A.S.T. Graphs apart and then add one metric at a time. I will be utilizing the Royal Bank of Canada graph as my sample. This template will apply to all of the historical graphics utilized in the article. For disclosure, I am long the Royal Bank of Canada.

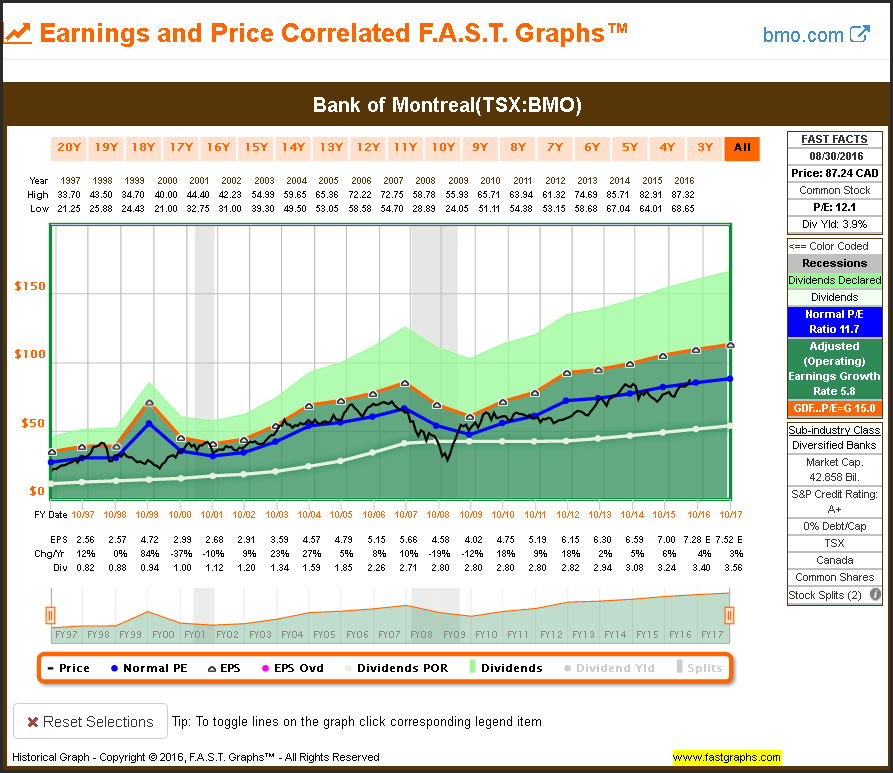

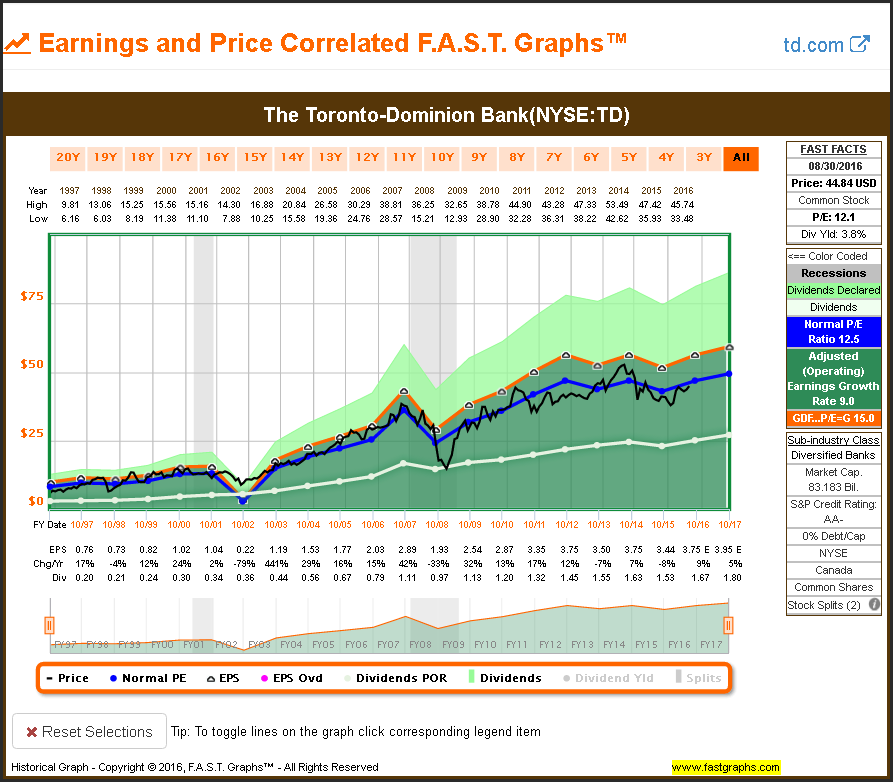

The orange line on each graph represents a valuation reference line drawn as a multiple of earnings on each company at a specific P/E ratio. In theory, this line represents a rational view of a company's fair value. The dark green shaded area below the line represents the company's total earnings over the timeframe graphed.

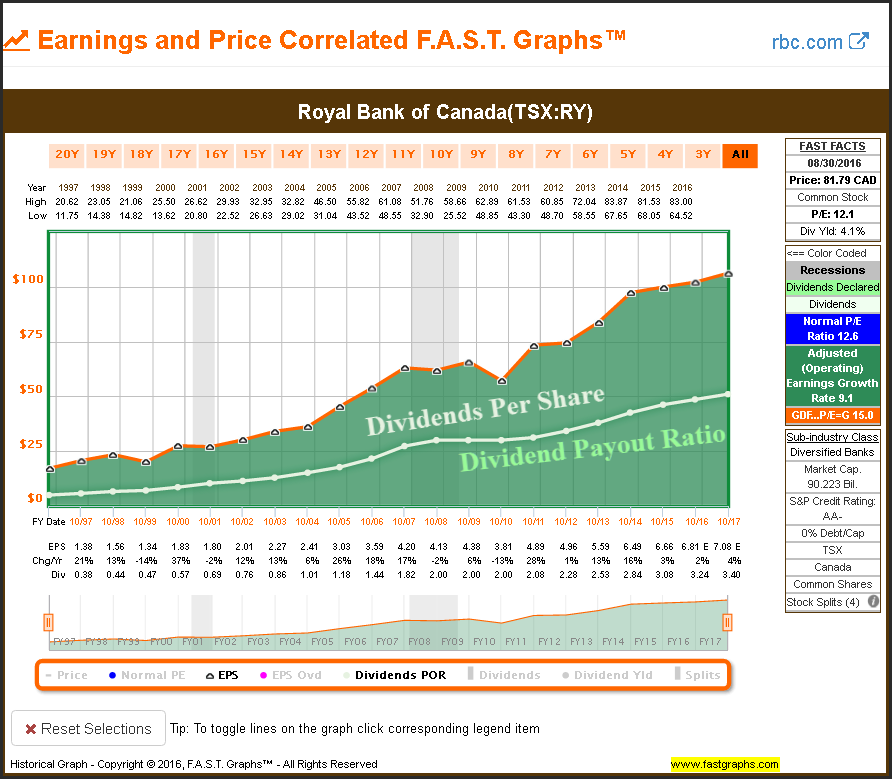

Next I have added the light green line (it appears white to many) which plots the company's dividends per share over the timeframe graphed. A quick examination of this line will tell you whether dividends have been steadily increasing, or whether they have been cut at some point. The area below the light green line represents the portion of earnings paid out as dividends - commonly referred to as the dividend payout ratio.

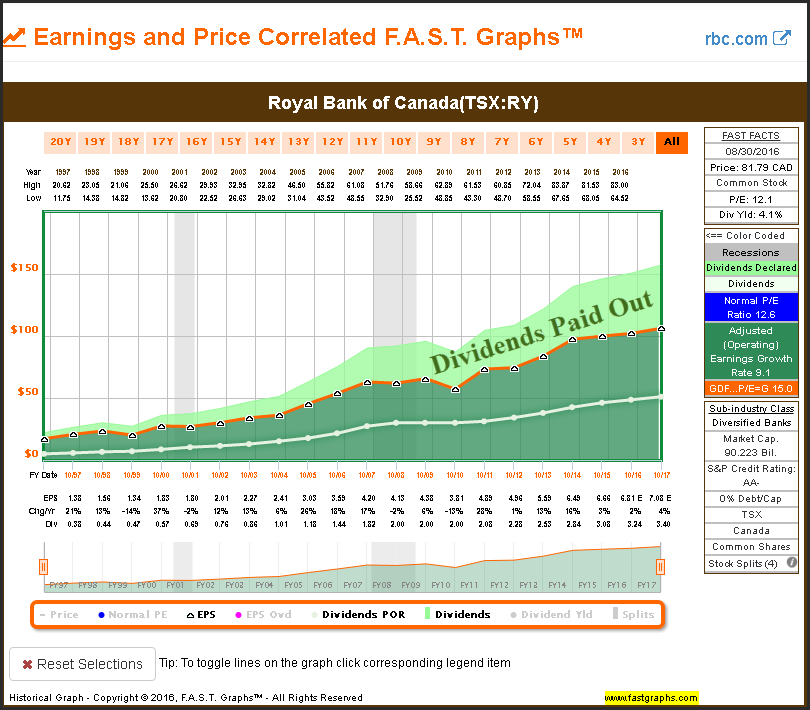

Dividends are also expressed after they have been paid out of earnings as a light green shaded area and stacked on top of the orange valuation reference line. Therefore, dividends are expressed prior to being paid out by the light green (white) line, and after they have been paid out to shareholders expressed as the light green shaded area on top of the orange line.

Next the black line representing monthly closing stock prices is added and correlated with the orange valuation reference line. Stated overly-simplistically, when the price is above the orange line overvaluation is present, when the price is touching the orange line fair valuation is present, and finally, when the price is below the orange line undervaluation is indicated. However, with this example note how commonly the price line sits below the orange fair valuation reference line. You will discover a similar valuation relationship on all of the “Big Five” Canadian banks.

The final metric added to the graph is the historical normal P/E ratio represented as a dark blue line. This calculates the valuation that the market has typically applied to each company over the timeframe graphed. The dark blue normal P/E ratio line adds a second valuation reference to each graph. Analysis of both of these valuation reference lines provides the reader an analytical perspective of historical valuation.

Note: in the case of Canadian banks, the reader might consider that the dark blue historical normal P/E ratio line provides the most conservative view of fair valuation. Although both the orange fair valuation reference line and the dark blue historical normal P/E ratio valuation reference line provide important analytical perspectives, with all cases it is a fact that the market has tended to value the “Big Five” Canadian banks at a modest discount to the orange fair valuation reference line. Consequently, it seems prudent to make decisions about the fair valuation of Canadian banks based on the dark blue normal P/E ratio valuation reference line.

The Big Five Cross-Listed or Interlisted Canadian banks: A Historical Review

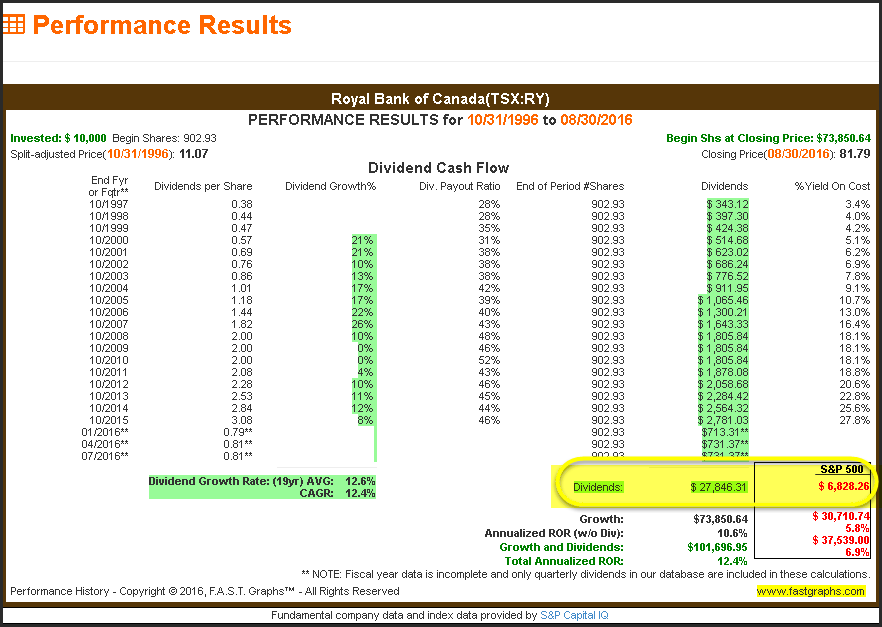

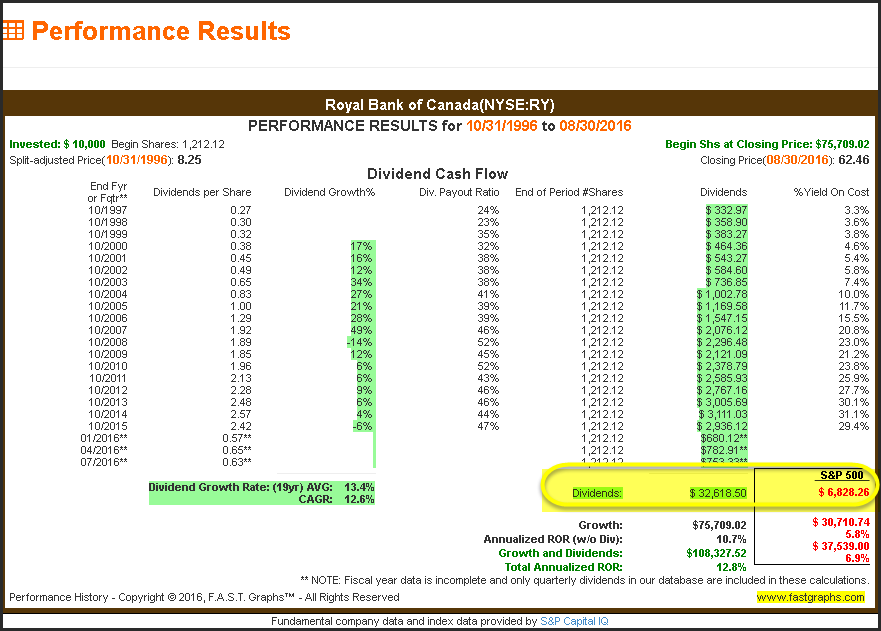

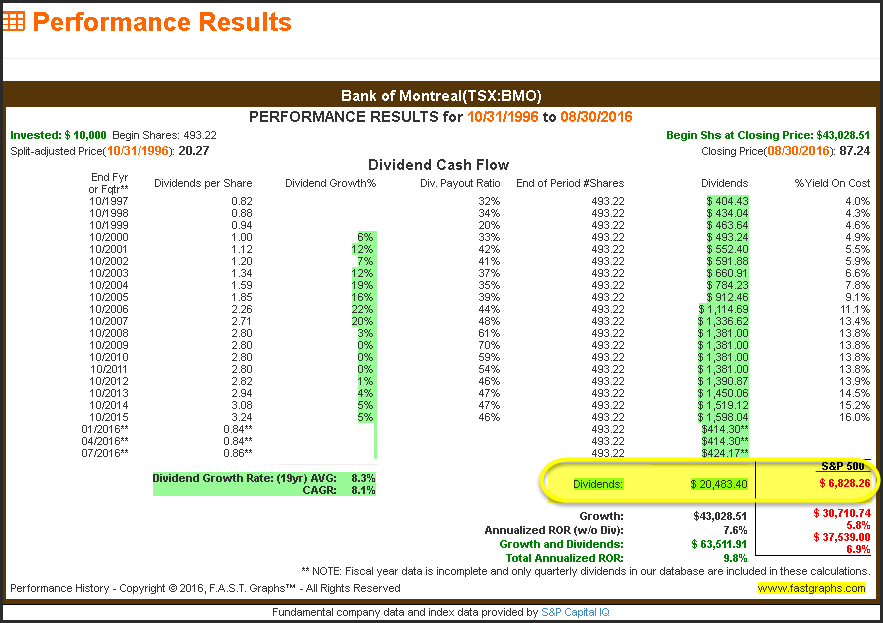

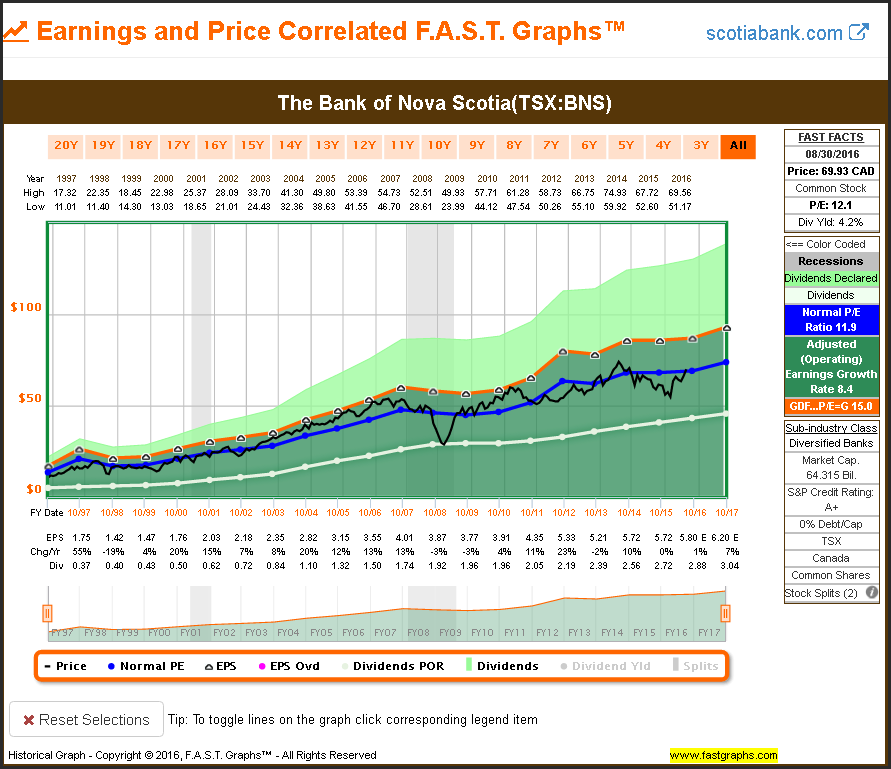

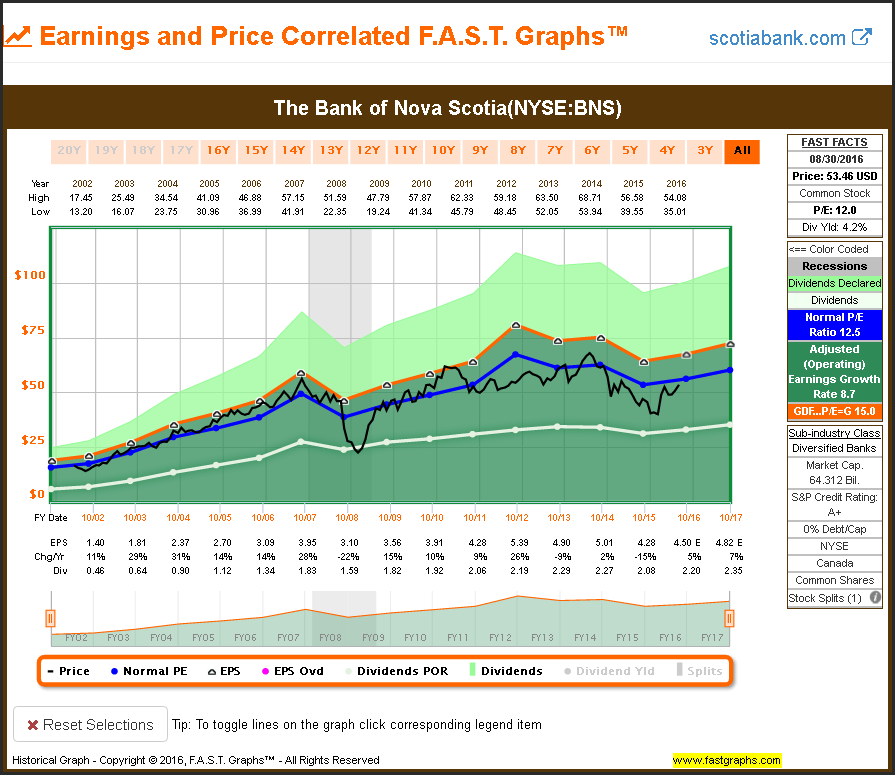

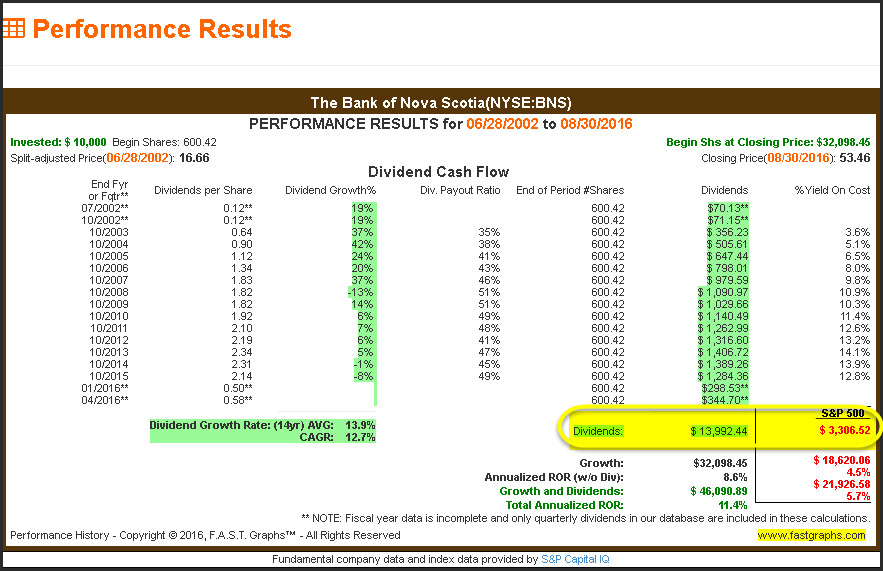

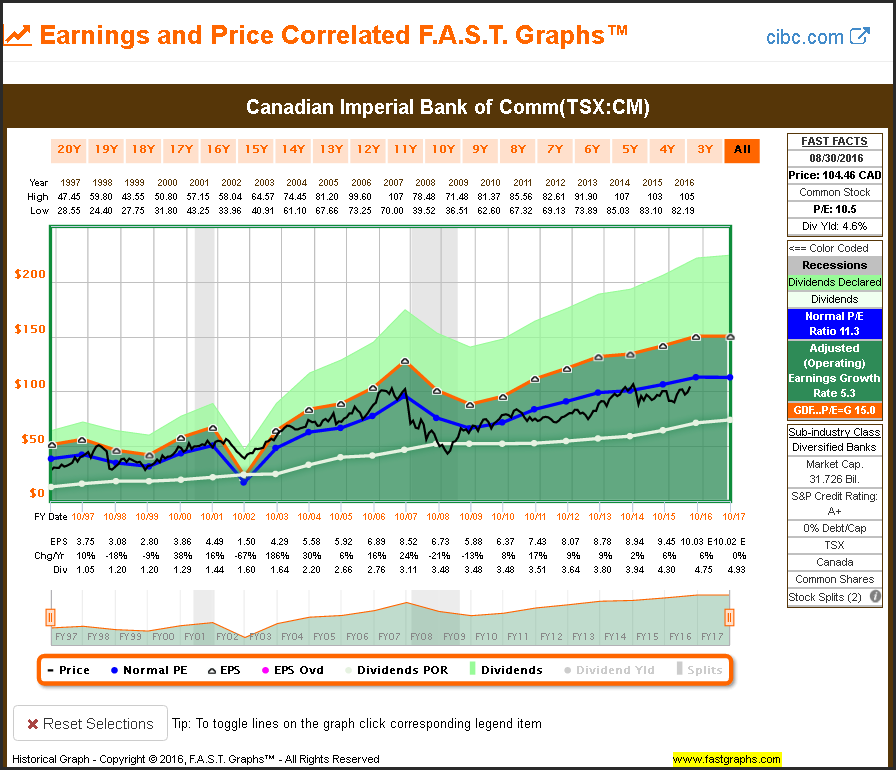

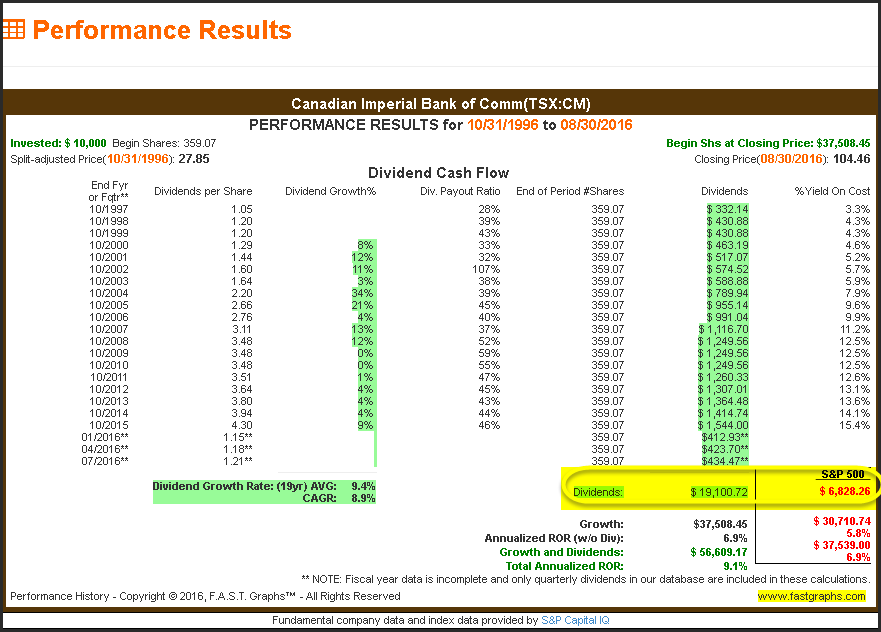

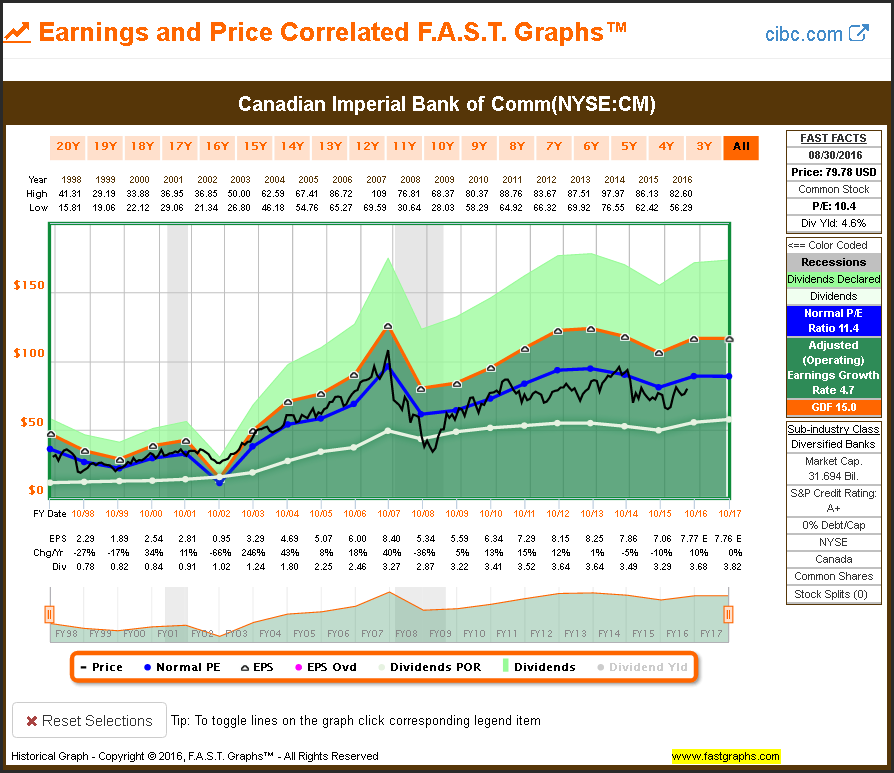

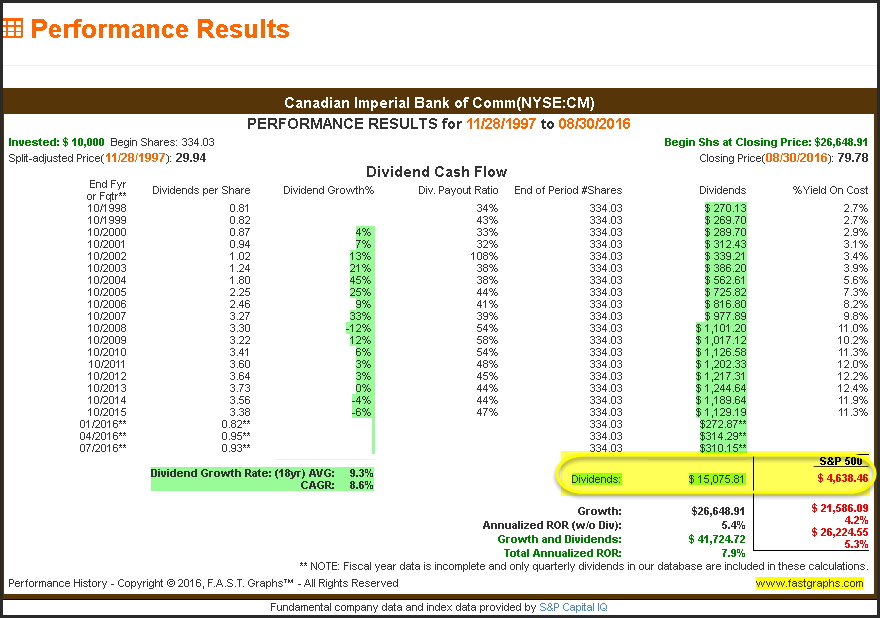

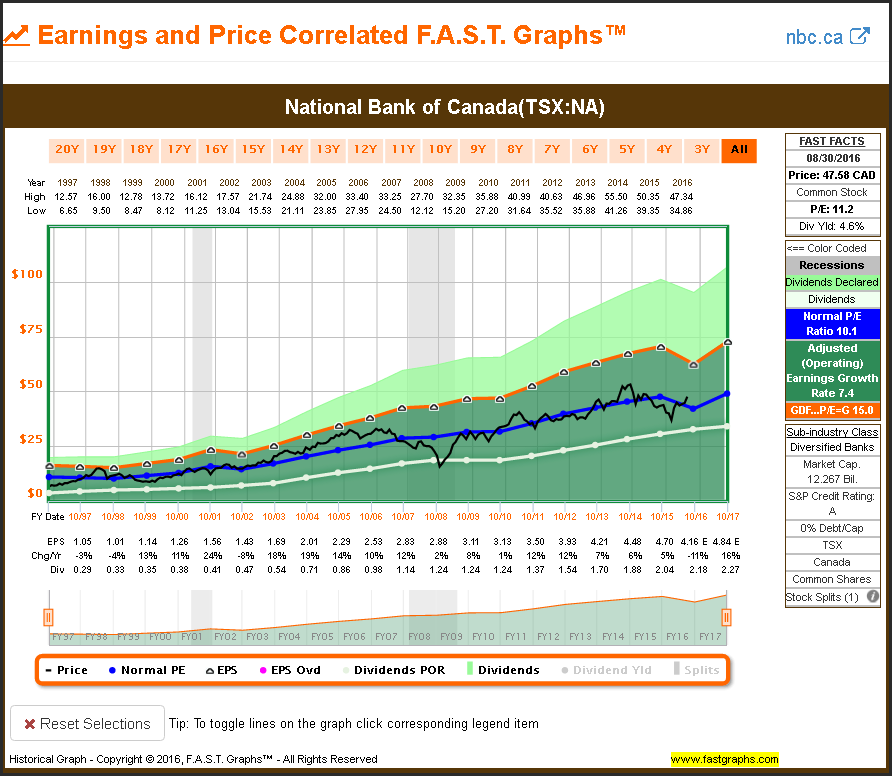

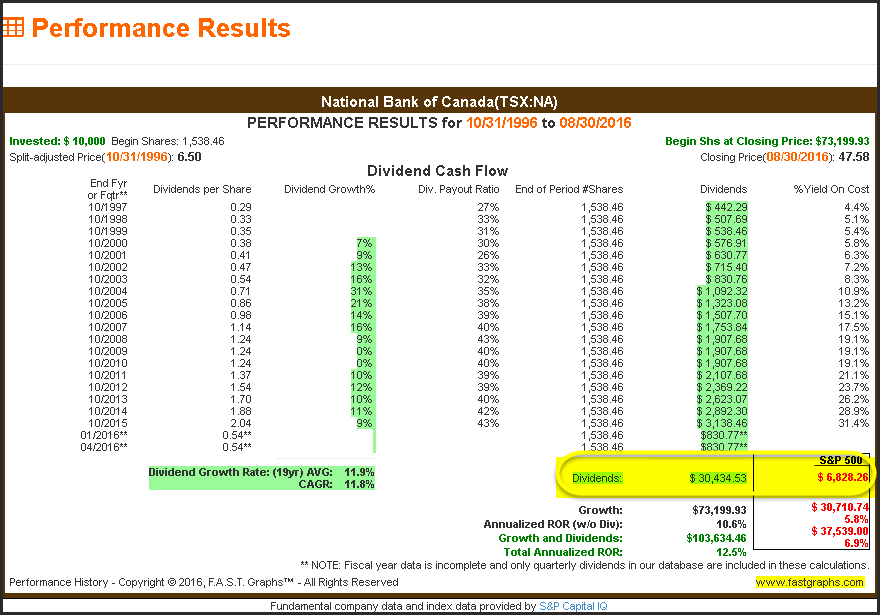

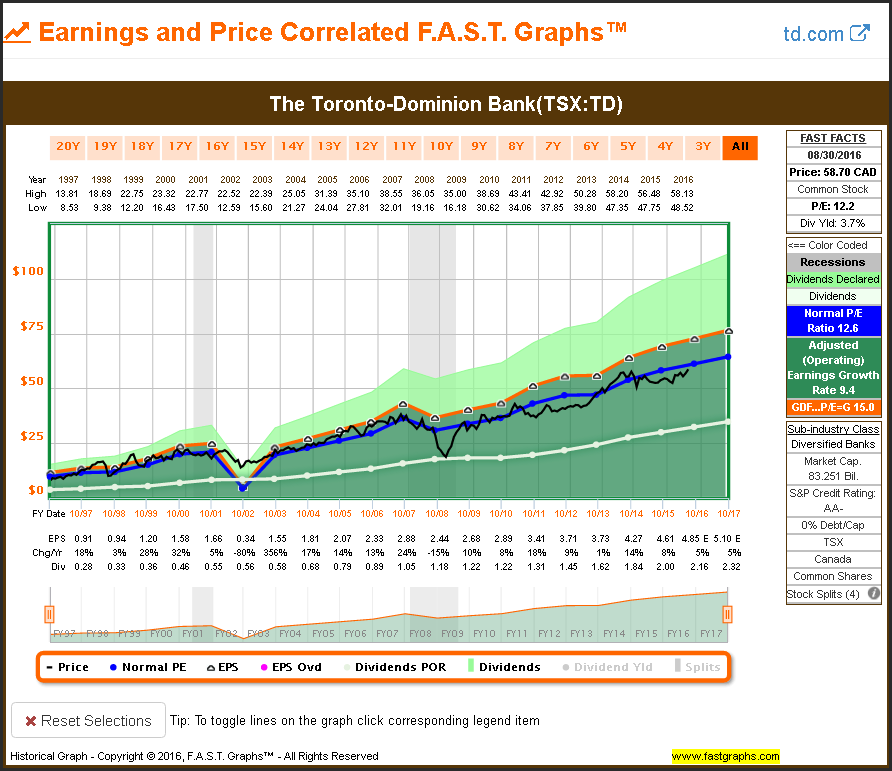

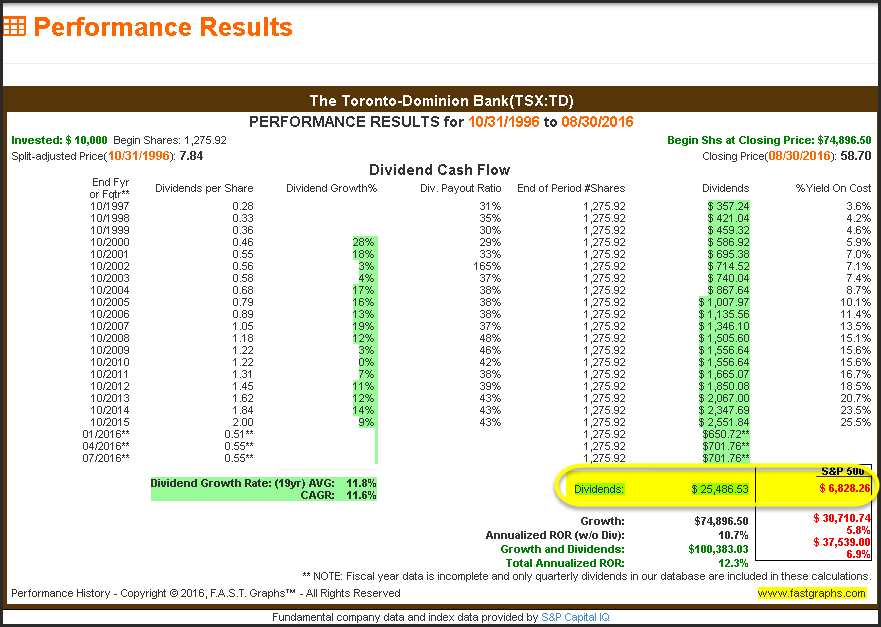

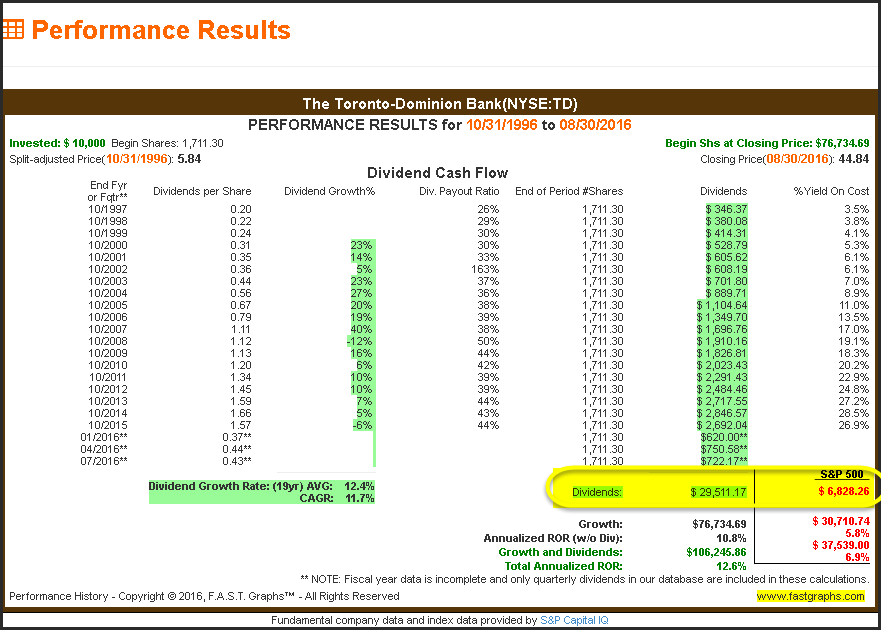

The following earnings and price correlated historical F.A.S.T. Graphs™ illustrate the undeniable correlation and relationship of price to earnings on each example. A careful analysis of each of these long-term histories clearly indicates the relative valuation of each of the “Big Five” Canadian banks. The current yields of each are also very attractive, and their historical dividend growth rates consistent and high.

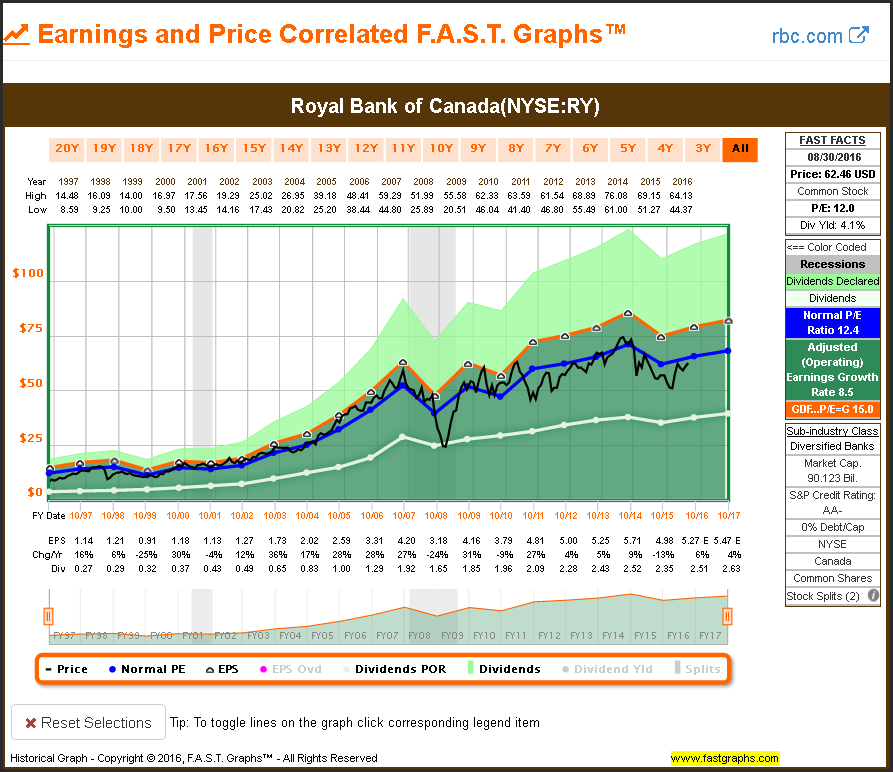

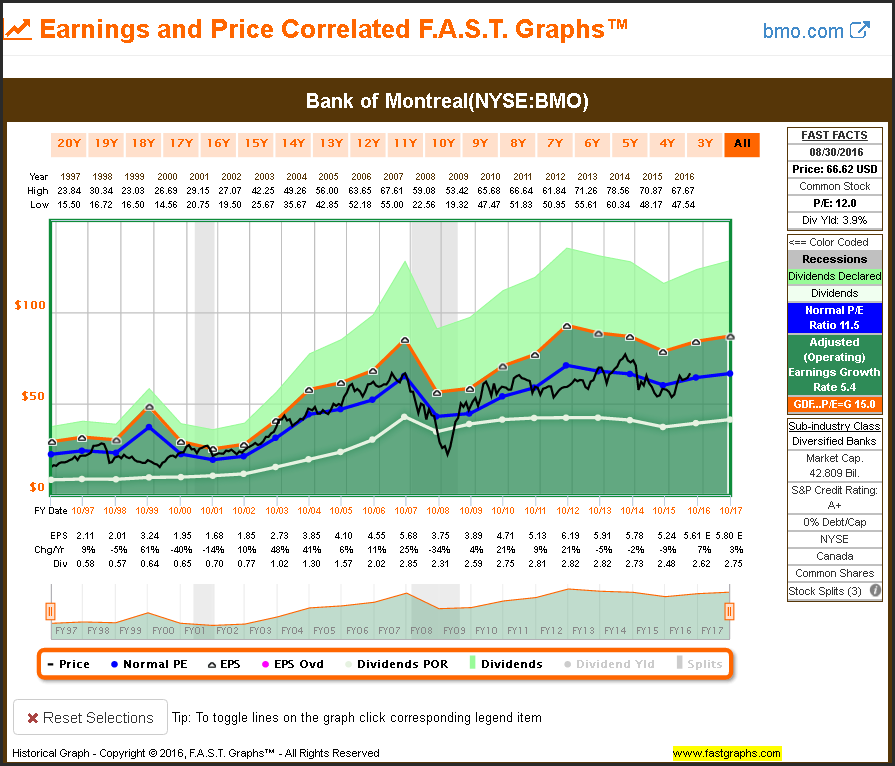

The differences between the TSX and the NYSE versions are attributed primarily to currency exchange rates. As previously stated, I believe the best analysis of the quality and consistency of the performance of these banks is through analyzing them by their country of origin (TSX).

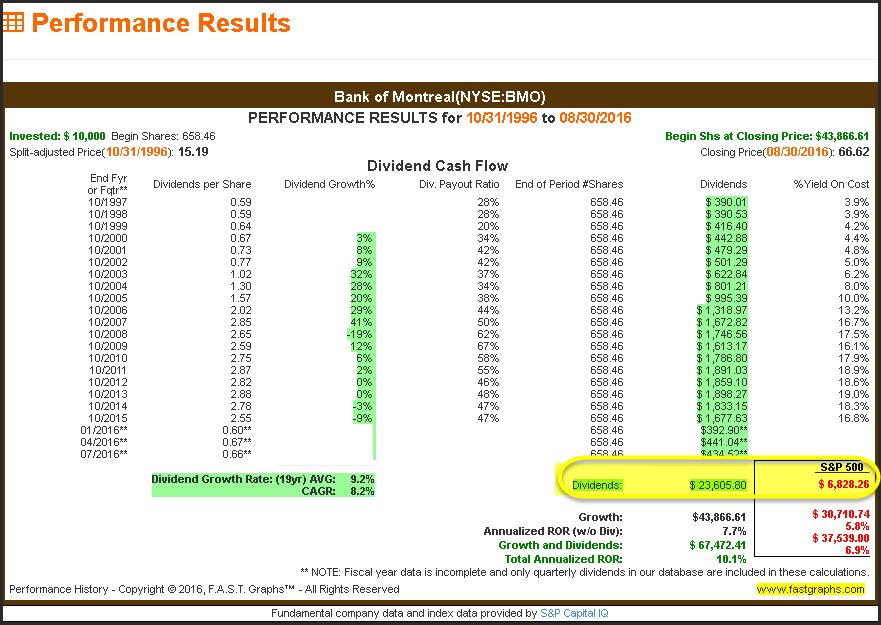

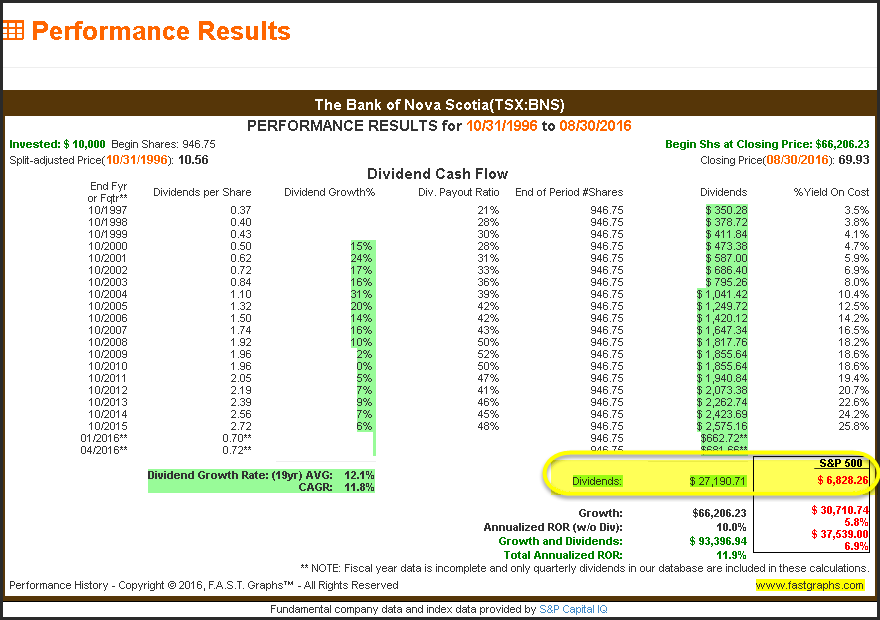

When reviewing the associated performance results I suggest that the reader look closely at the cumulative total dividends paid for each company on both exchanges. These Canadian banks have clearly been exceptional long-term dividend income generators. On the other hand, they have also outperformed the S&P 500 on a capital appreciation basis as well.

Royal Bank of Canada (TSX:RY) Graph and Table Produced in Canadian Dollars

Royal Bank of Canada (RY) Graph and Table Produced in US Dollars

Bank of Montréal (TSX:BMO): Graph and Tables Produced in Canadian Dollars

Bank of Montréal (BMO): Graph and Table Produced in US Dollars

The Bank of Nova Scotia (TSX:BNS) Graph and Table Produced in Canadian Dollars

The Bank of Nova Scotia (BNS) Graph and Table Produced in US Dollars

Canadian Imperial Bank of Commerce (TSX:CM) Graph and Table Produced in Canadian Dollars

Canadian Imperial Bank of Commerce (CM) Graph and Table Produced in US Dollars

National Bank of Canada (TSX:NA) Graph and Table Produced in Canadian Dollars

The Toronto-Dominion Bank (TSX:TD) Graph and Table Produced in Canadian Dollars

The Toronto-Dominion Bank (TD) Graph and Table Produced in US Dollars

Canadian Bank Forecasts - More of the Same

There are many analysts that believe that Canadian banks benefit from fewer regulatory restrictions and lower competition than their US peers. However, forecasts for growth in the US economy are moderately higher than those predicted for Canada for this year and next. However, Toronto Dominion Bank and Bank of Montréal are expanding into the US banking market.

On the other hand, there are concerns regarding real estate values in Canada that could impact the future profitability of Canadian banks. Perhaps this partially explains why leading analysts are generally forecasting lower growth relative to historical norms over the next few years. However, assuming that analyst estimates are reasonably accurate, the potential returns from investing in Canadian banks is quite attractive - as indicated on the “Forecasting Calculators” graphs below. (Note: each of the following forecasting calculators is drawn utilizing the more conservative historical normal P/E ratio calculator).

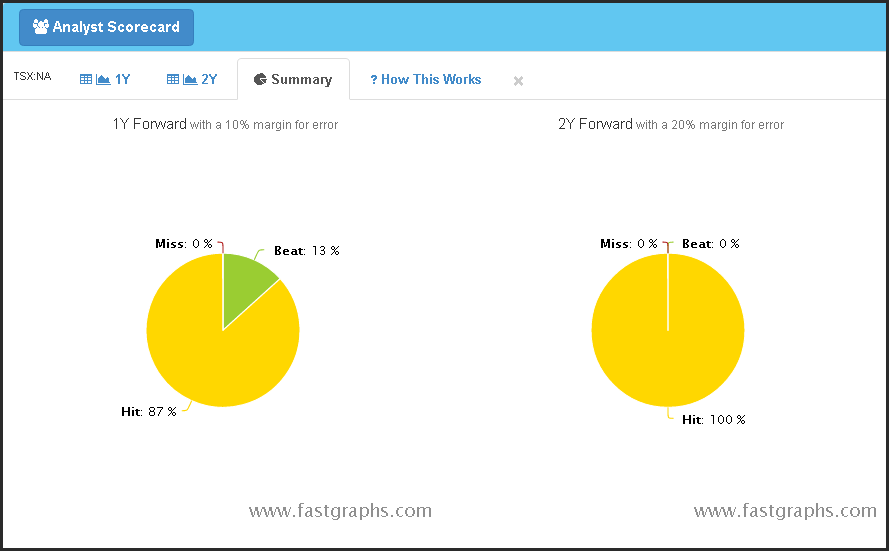

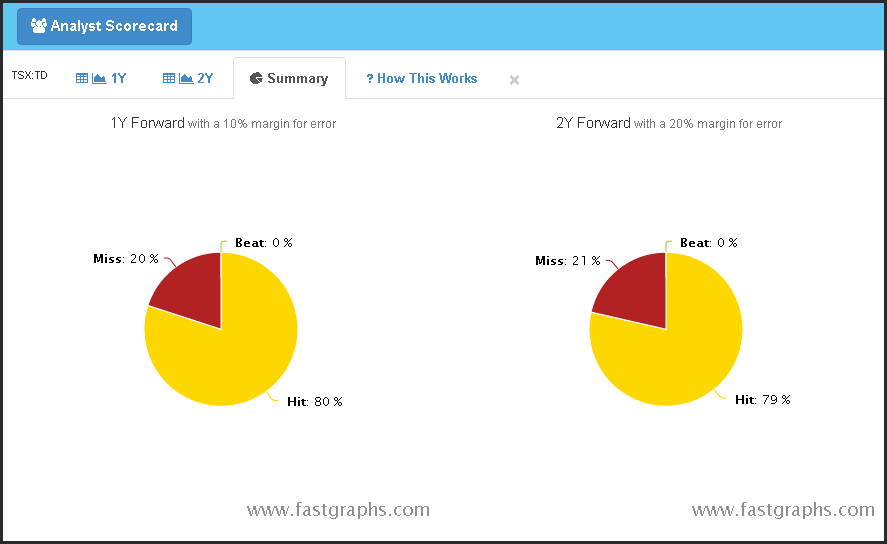

For insights into the potential accuracy of these analysts forecasts, I have also included a summary of the “Analyst Scorecard” on each example. The bottom line is that analysts have put together a strong track record of forecasting the earnings of these banks on the one year and two years forward basis. Nevertheless, I recommend that each investor conduct your own research and due diligence before investing.

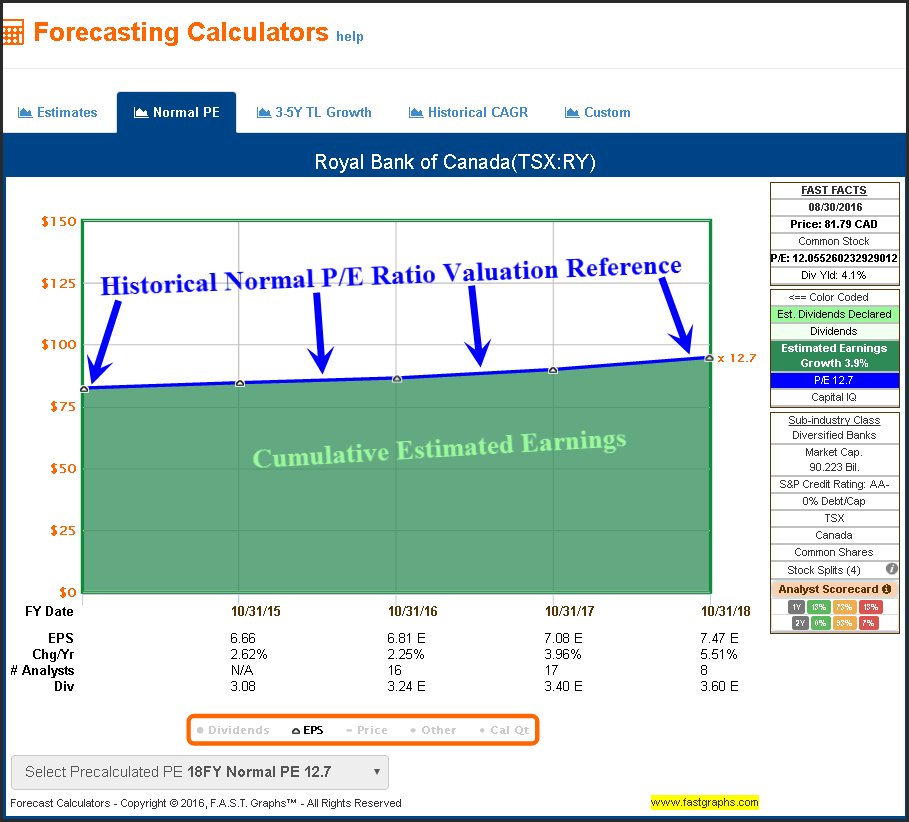

Royal Bank of Canada Forecasting Graph and Tutorial

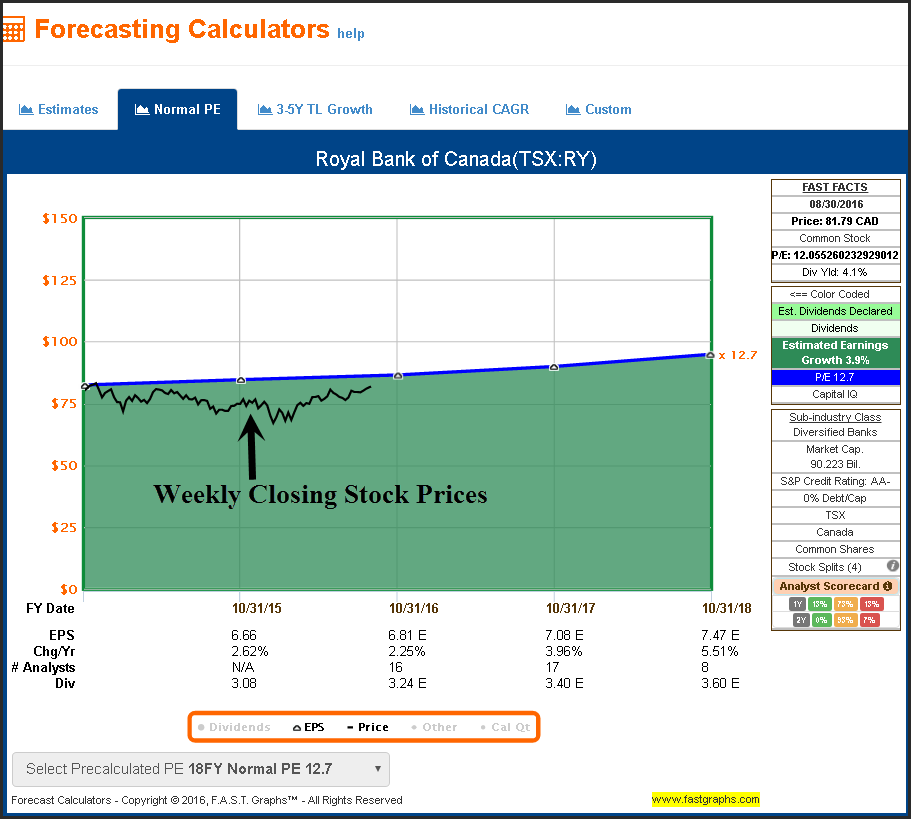

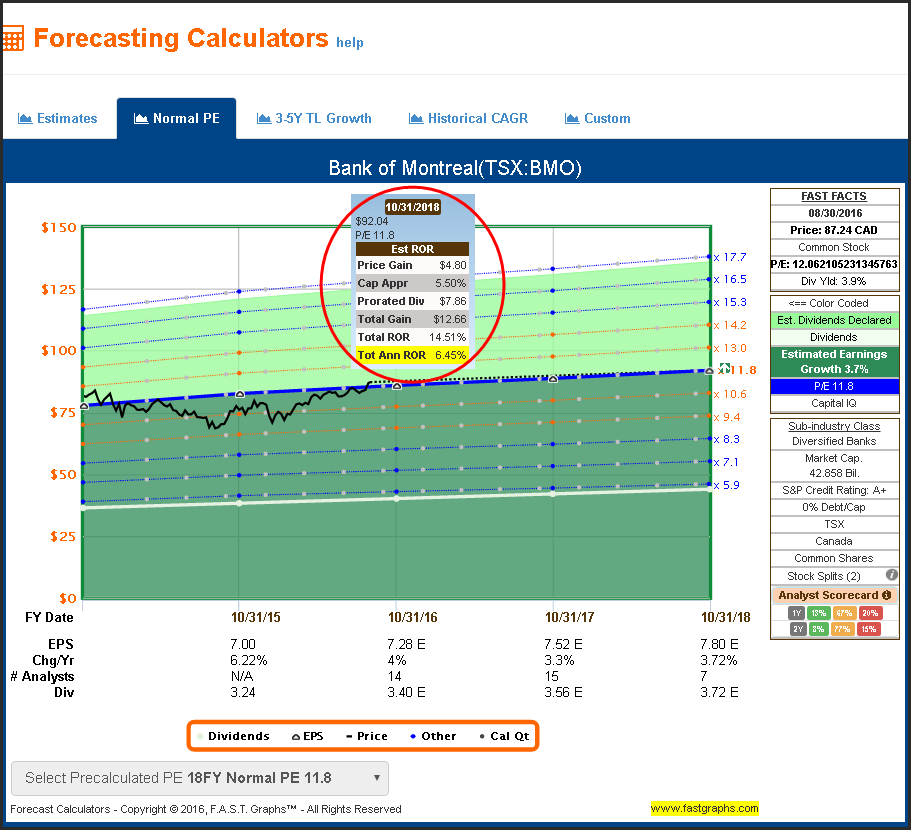

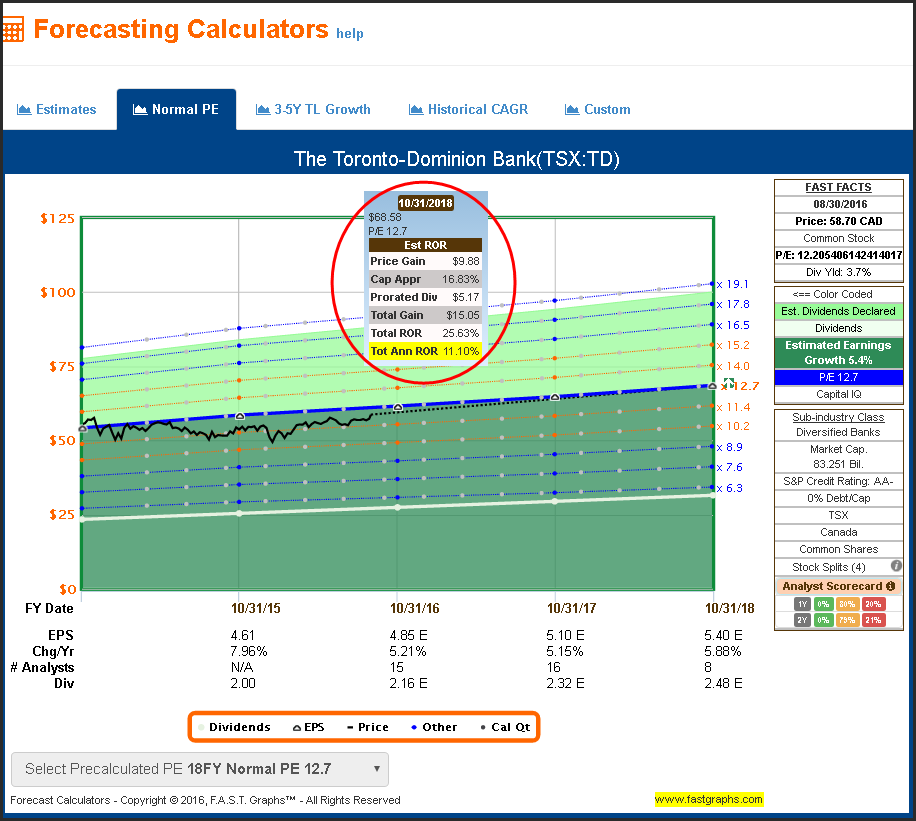

Readers have suggested that I include a tutorial on the F.A.S.T. Graphs™ “Forecasting Calculators” just as I did with the historical graphs above. Therefore, I have taken the “Forecasting Calculator” on Royal Bank apart in order to explain what each forecasting graph is expressing.

Just as we saw on the historical graphs, the first metric is simply a plotting of the specific earnings estimates over the next two to three years. The fair valuation reference line is dark blue because I am utilizing the historical normal P/E ratio as the fair valuation reference. The average estimated earnings growth rate is presented in the green color-coded FAST FACTS box to the right.

The estimated earnings numbers are listed at the bottom of the graph and marked with a capital “E” indicating estimate. Just below the earnings estimates is a calculation of the earnings growth change per year (Chg/Yr), and just below that is the number of analysts making those forecasts for each specific year. Finally, the forecast dividend calculations are based on growing the dividend at the same rate of earnings.

With this next graph I’ve added weekly closing stock prices (the black line) for the past actual fiscal year and the current fiscal year we are in. This provides an expression of current valuation. In these examples, when the price is below the blue normal P/E ratio fair valuation reference undervaluation is indicated.

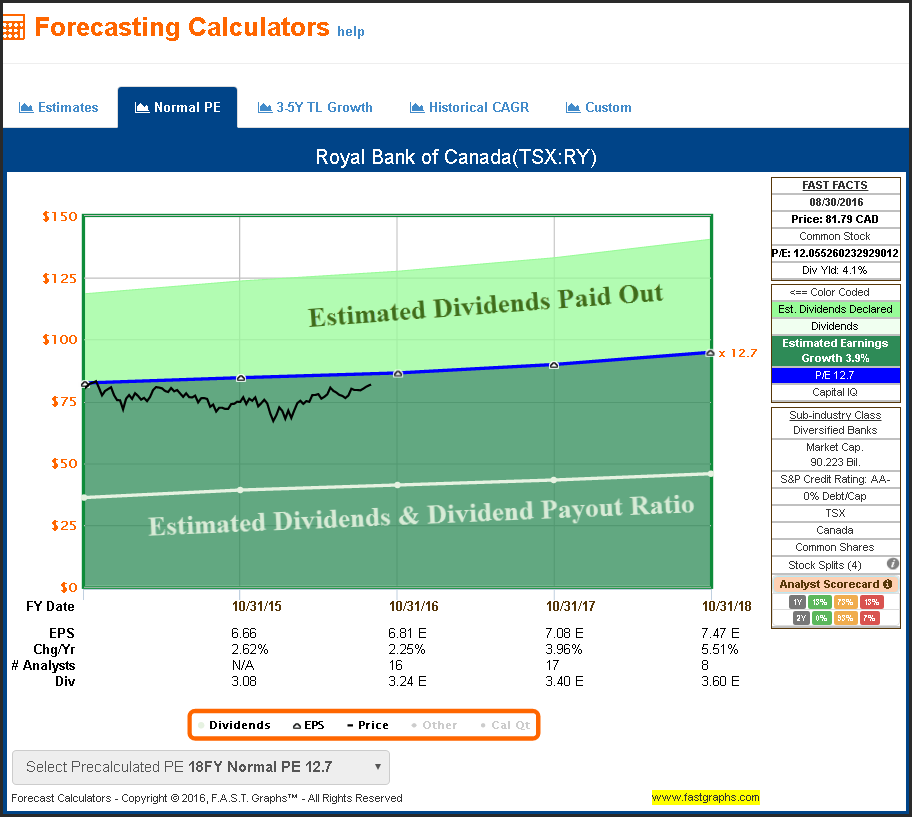

Next I have added the dividends expressed as part of earnings by the light green line (white looking line) in the dark green shaded area, which also graphically illustrates the dividend payout ratio. The lighter green shaded area above the blue fair valuation reference line indicates dividends after they’ve been paid to shareholders.

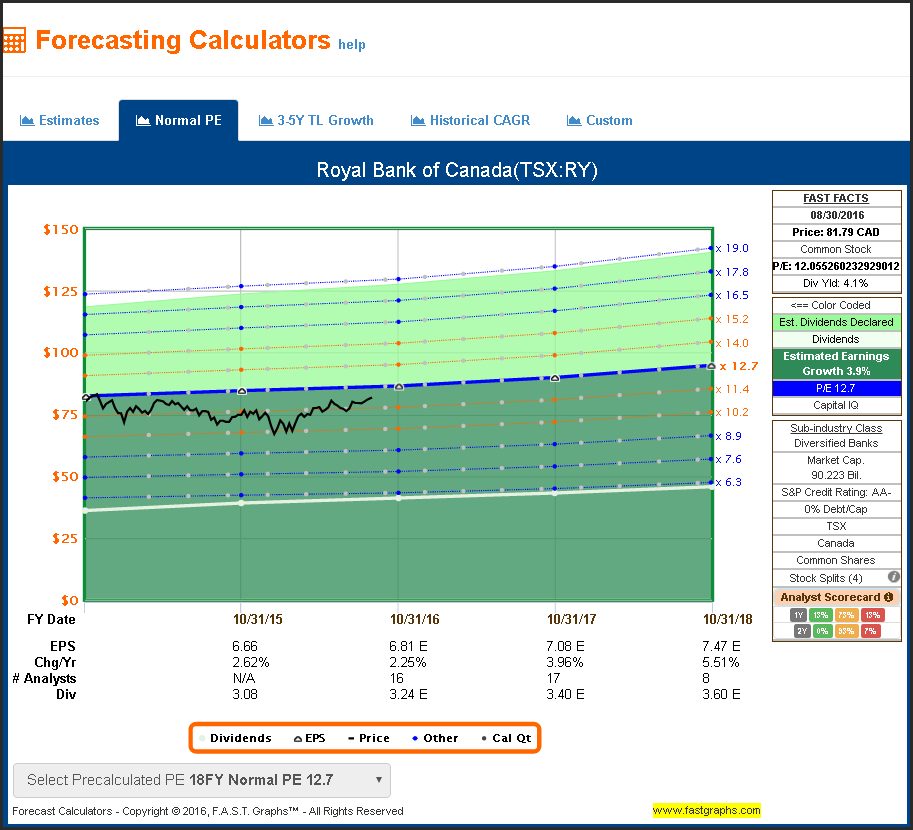

The next metric included in the forecasting calculators are comprised of five parallel lines above the fair valuation reference line and five parallel lines below the fair valuation reference line. Each of these lines represents an additional and specific P/E ratio that will later be utilized to calculate potential future returns. Consequently, several “what if” calculations can be made by pointing to the dots associated with those various parallel lines.

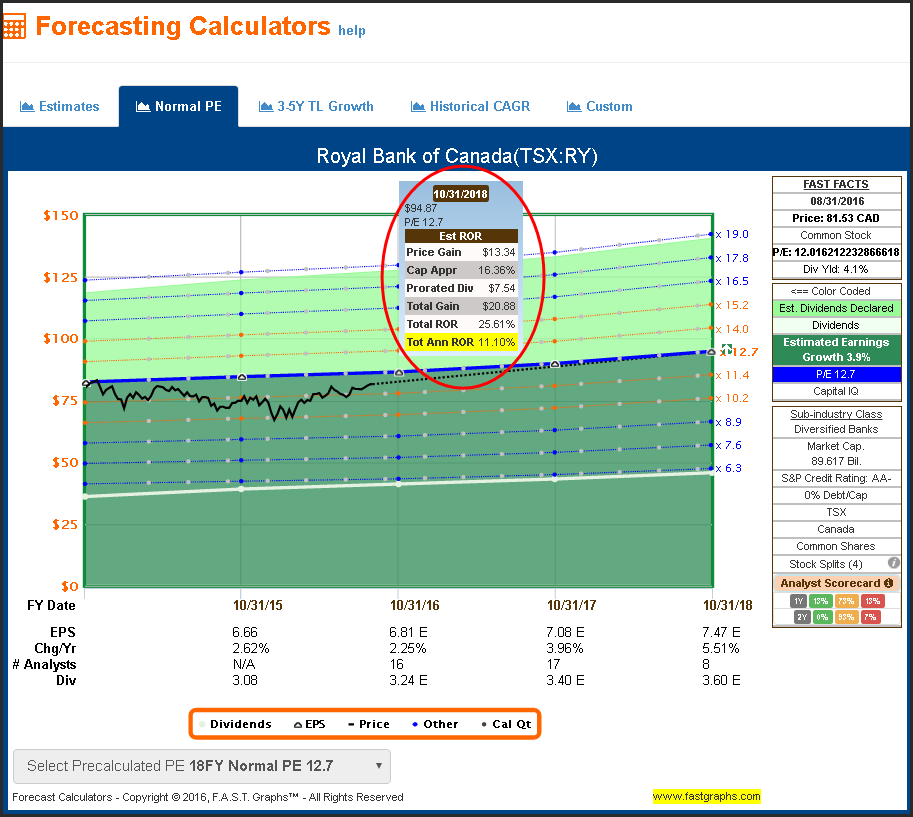

This next graph represents a complete “Forecasting Calculator” with additional quarterly dots added to the parallel lines for “what if” calculating purposes on a live graph. I have also included the total annual return calculation to include dividends based on the last earnings estimate and utilizing the dark blue normal P/E ratio fair valuation reference line.

As indicated, the Royal Bank of Canada could offer double digit returns out to fiscal year-end October 2018 - assuming the estimates are correct and the stock trades at its normal P/E ratio. All of the following “Forecasting Calculators” will only include the complete calculator with calculations.

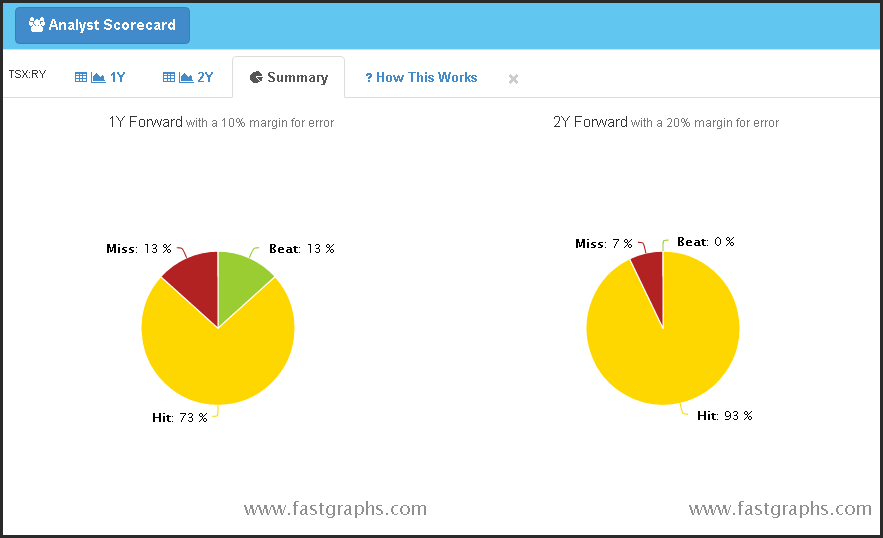

Royal Bank of Canada Analyst Scorecard Summary

The “Analyst Scorecard” summary illustrates how accurate analysts have historically been when making forecasts one year prior to the actual reporting and two years prior to the actual reporting by the company. In the case of Royal Bank, analysts have been accurate with their forecasts the majority of the time when previously forecasting earnings on this company. This simply provides additional insights on how much credence you might place on the forecasts presented in the forecasting calculators.

Bank of Montreal Forecasting Calculator

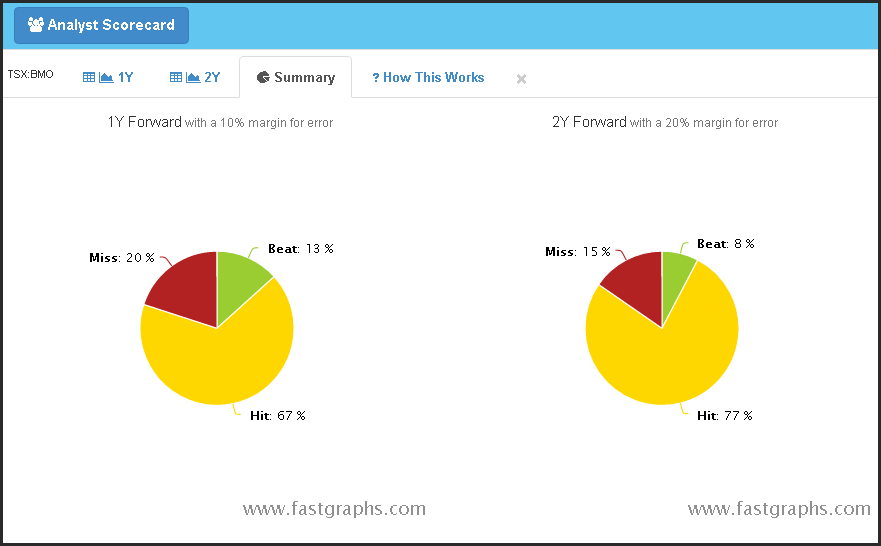

Bank of Montreal Analyst Scorecard Summary

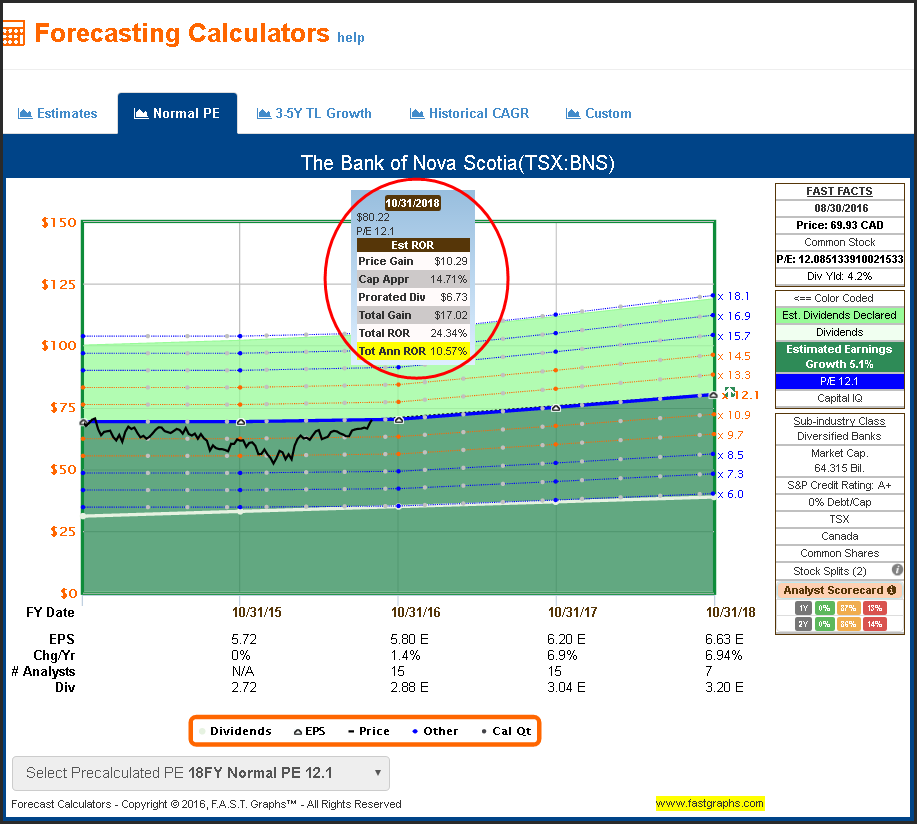

The Bank of Nova Scotia Forecasting Calculator

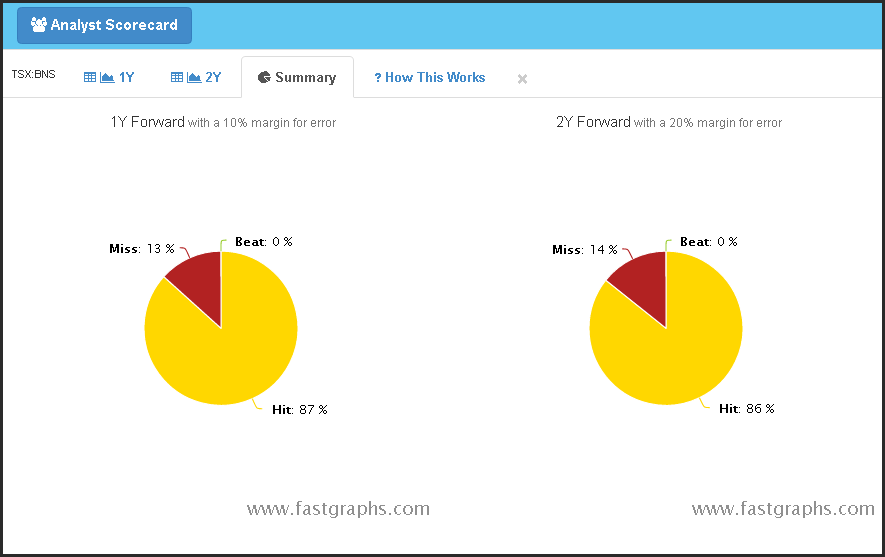

The Bank of Nova Scotia Analyst Scorecard Summary

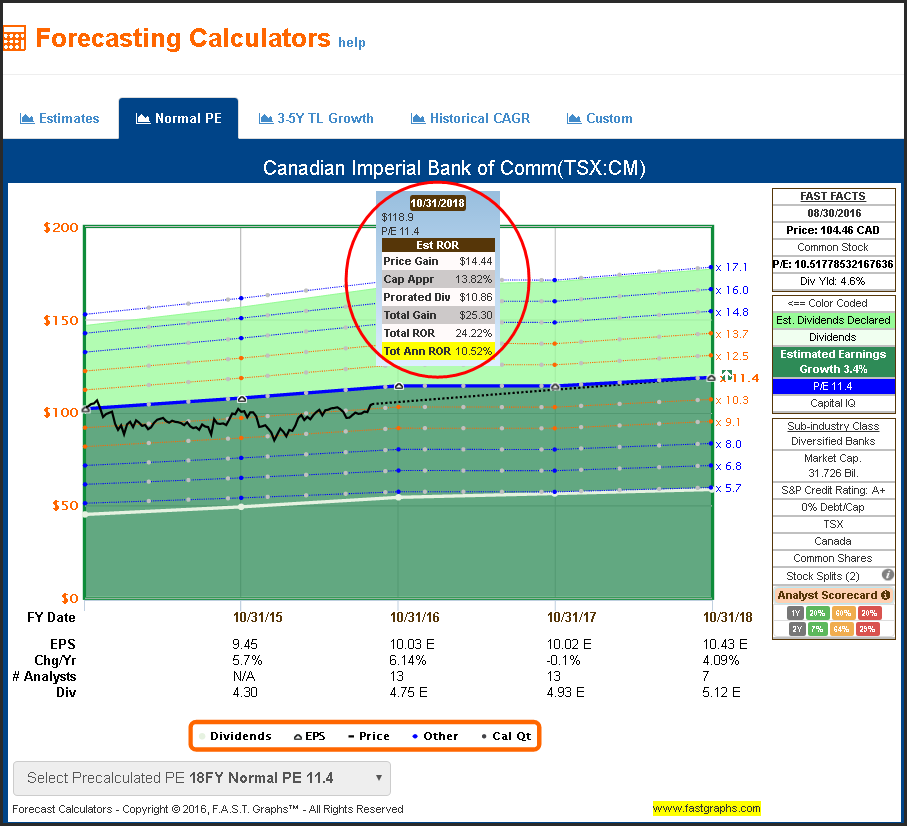

Canadian Imperial Bank Forecasting Calculator

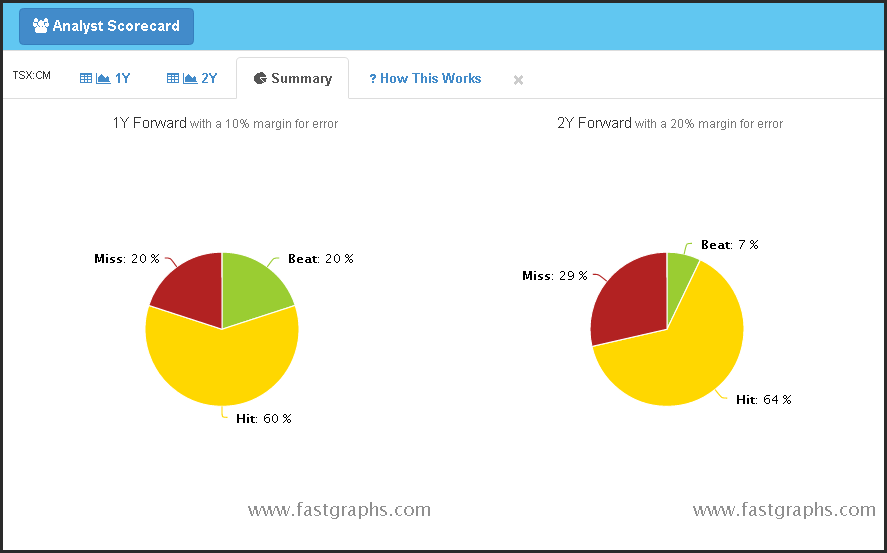

Canadian Imperial Bank Analyst Scorecard Summary

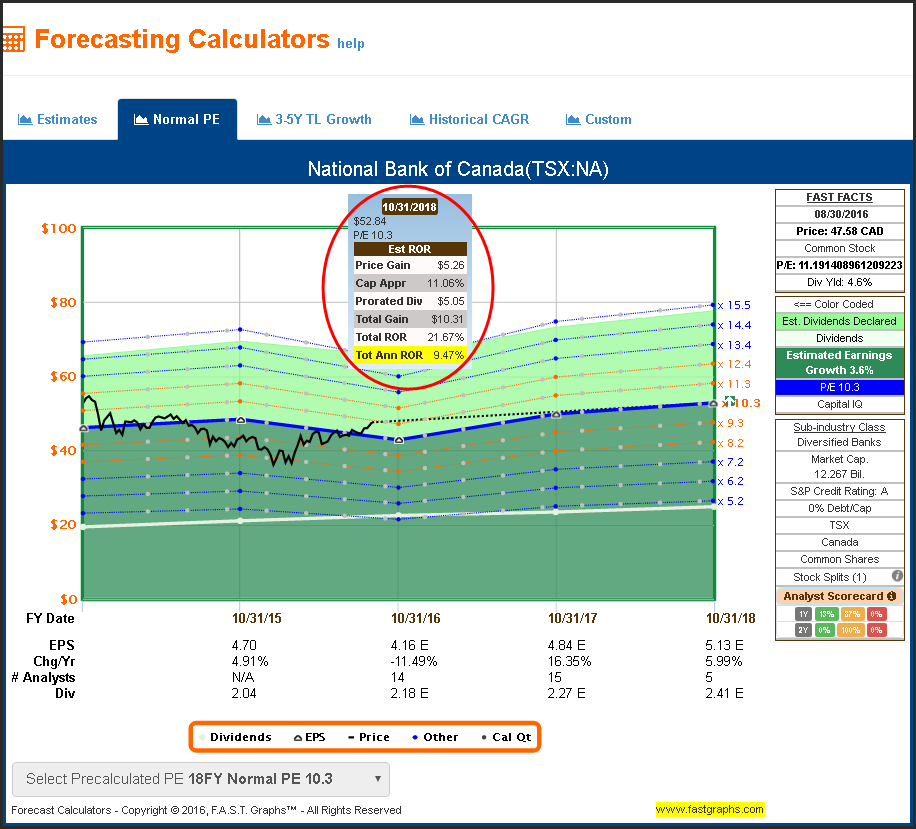

National Bank of Canada Forecasting Calculator

National Bank of Canada Analyst Scorecard Summary

The Toronto-Dominion Bank Forecasting Calculator

The Toronto-Dominion Bank Scorecard

Summary and Conclusions

For those investors seeking above-average dividend yield with the possibility of dividend growth and capital appreciation, I believe that all of the “Big Five” Canadian banks represent attractive options. Each provides the dividend growth investor above-average dividend yields in today’s low interest rate environment, and all of them appear to be attractively valued, if not slightly undervalued at this time. Although my personal favorite is the Royal Bank of Canada, the Canadian Imperial Bank offers the highest current yield and perhaps the lowest valuation, however, its operating history is not quite as consistent. Although I do not believe investors can go wrong with any of these selections, I leave it up to each of you to decide for yourselves.

Disclosure: Long RY

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.