Average Household Debt: $132,000 - Not Counting Mortgage

1. Fed Chair Janet Yellen Ready to Raise Interest Rates... Maybe

2. Yellen’s #2 Man Predicted Two Rate Hikes – Sept. & Dec.

3. So What is the Eco Data We’ll See Before September 21?

4. Household Debt: Another Reason For the Slow Economy

5. Why US Households Have Such Large Average Debt Levels

Overview

A new study out last week reported that the average US household has over $132,000 in outstanding debt – not counting their home mortgage. If we add the home mortgage, the average debt level soars to over $263,000. Both numbers are huge, but are still below the peak debt levels just before the Great Recession in 2008. I will give you the details below.

I will argue today that these huge household debt levels are one of the reasons that this economic recovery is so weak, with GDP growth averaging less than 1% in the first half of this year. I will also explain why the continued huge household debt level is not just because US consumers spend beyond their means. It’s an interesting dilemma.

But before we get to that, I will opine on the latest Fed discussions on when to raise short-term interest rates, especially in light of Janet Yellen’s latest policy speech last Friday in Jackson Hole, Wyoming. The big question is whether the Fed will hike rates at its next policy meeting on September 20-21. This will be a big focus of market attention between now and then.

It should make for an interesting letter, so let’s get started.

Fed Chair Janet Yellen Ready to Raise Interest Rates... Maybe

Chair Yellen made her much-anticipated policy speech last Friday at the annual Jackson Hole gathering of monetary leaders from around the world. Some expected her to deliver a “hawkish” speech in favor of raising the Fed Funds rate sooner rather than later. Others expected a continuation of her cautious “data-dependent” stance on the next rate hike.

As it turned out, both interest rate bulls and bears found something to hang onto in Ms. Yellen’s carefully scripted (as always) speech. She started out by making a case for raising the Fed Funds rate soon based on what she cited as encouraging signs regarding the economy, largely based on the continuing improvement in the labor market.

Then she turned wishy-washy and returned to her more cautious, data-dependent, we’re not in a hurry scenario. Here’s a summary of her comments. She began by saying:

“U.S. economic activity continues to expand, led by solid growth in household spending… While economic growth has not been rapid, it has been sufficient to generate further improvement in the labor market. Smoothing through the monthly ups and downs, job gains averaged 190,000 per month over the past three months.

… Looking ahead, the FOMC expects moderate growth in real gross domestic product (GDP), additional strengthening in the labor market and inflation rising

to 2% over the next few years. Based on this economic outlook, the FOMC continues to anticipate that gradual increases in the Federal Funds rate will be appropriate over time to achieve and sustain employment and inflation near our statutory objectives.

…In light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the Federal Funds rate has strengthened in recent months.”

Of course, Ms. Yellen made no specific suggestions as to when the Fed would enact the next Fed Funds rate hike. Instead, she gave the audience a nebulous chart showing three possible scenarios for “normalizing” the short-term interest rate. The chart showed no exact start-and-stop dates for the process. The closest she came to doing so was this statement:

“The Fed policy committee continues to anticipate that gradual increases in the federal-funds rate will be appropriate.”

The bottom line is that while Ms. Yellen’s speech was more upbeat about the US economy (for reasons I don’t understand), she stopped well short of predicting a hike in the Fed Funds rate at the next policy meeting on September 20-21.

Yellen’s #2 Man Predicted Two Rate Hikes – Sept. & Dec.

In my BLOG last Thursday, I discussed recent speeches by Fed Vice-Chairman Stanley Fischer and New York Fed President William Dudley, both of whom are permanent voting members of the Fed Open Market Committee (FOMC). Both argued earlier this month that the Fed Funds rate needs to be increased sooner rather than later.

Both Fischer and Dudley believe that the US economy will surge in the second half of this year, based on the questionable Atlanta Fed’s GDPNow forecast that the economy will jump by 3.6% on average in the 3Q and 4Q. None of the economic reports I see support that forecast.

The Commerce Department, for example, revised its 2Q GDP estimate last week from 1.2% in late July to only 1.1%. So growth in the anemic first half of the year fell to slightly below 1%. As I will discuss below, retail sales for July were well below expectations.

So other than the strong labor market, it remains to be seen what Yellen & Company are seeing as evidence of a “strengthening economy” of late.

Yet despite that, Fed Vice-Chair Stanley Fischer went out on a limb last Friday in Jackson Hole and predicted two rate hikes before the end of this year in an interview with CNBC following Yellen’s speech last Friday.

Asked during the CNBC interview if investors should be on the edge of their seats for a rate hike as soon as September and for more than one rate hike this year, Fischer replied:

“I think what [Yellen] said today was consistent with answering yes to both your questions, but these are not things we know until we see the data.”

So What is the Eco Data We’ll See Before September 20-21?

Clearly, Fischer and Dudley would like to see a quarter-point Fed Funds rate hike on September 21 and another one on December 14 at the conclusion of the last policy meeting of the year. In the next few weeks, the US stock and bond markets will be laser-focused on the odds for a rate hike on September 21. Fed Funds futures now place the odds at 30% for a September rate hike (up from 24% before Yellen’s speech) and a 57.2% chance in December.

The question is, what important economic data will we see between now and then? The answer is, not much. The most important report we will see between now and September 21 is this Friday’s August unemployment report. Pre-report expectations are for the headline unemployment rate to remain unchanged at 4.9%.

Assuming that’s true, then the big focus will be on the new jobs created number, which can be very volatile. As noted above, new jobs have averaged 190,000 over the last three months. So a number above 200,000 will likely signal a rate hike on September 21, while a number well below 200,000 would suggest that the Fed sits tight until the December meeting.

So it’s a wait and see game. If it looks like the Fed is going to hike the Fed Funds rate two times this year (September and December), I expect the major US stock indexes to come under pressure. A correction from today’s near record levels could be nasty.

Household Debt: Another Reason For the Slow Economy

US retail sales slowed unexpectedly in July, the latest month for which we have data. The Census Bureau reported earlier this month that retail sales were flat in July (0.00%) versus the pre-report consensus of +0.4%. But it gets worse. If we strip out auto purchases, retail sales for July were -0.3%.

Economists and forecasters continue to scratch their heads as to why retail sales are not stronger at this point in the recovery. Remember that this slowdown is occurring against a backdrop of much lower gasoline prices and an improving labor market.

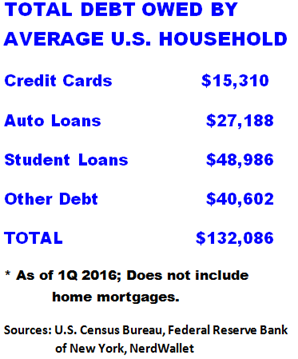

One argument is that many American households are worried about having too much debt. The latest numbers on household debt from the Census Bureau and the New York Fed may surprise you. Here is the average US household debt for just four classes of debt held.

For households with these four types of debt, that’s a combined average debt of $263,259. That translates into an average of $6,658 a year just in interest payments alone, which is especially tough when compared to the median household income of $75,591.

That means American households are spending 9% of their gross income just on interest payments alone – on just these four types of debt. Here is how that debt translates into financial stress: 14% of households have more debts than assets, which puts their net worth in negative territory.

[Side Note: If you’re questioning how the average household could have student loan debt of almost $49,000, let me add this. Outstanding student loan debt has skyrocketed from $260 billion in 2004 to a staggering $1.3 trillion today, making it the second-largest form of consumer debt in America. Also consider that in many households, the husband and wife both have outstanding student debt.]

Many analysts agree that it is not reasonable to include home mortgage debt when considering overall household debt, since home values generally equal or exceed their outstanding mortgage balance.

So let’s take a look at those household debt figures – minus the mortgage but adding in other debts in addition to credit cards, auto loans and student loan debt shown above.

In this perhaps more realistic presentation, we see that the average US household has outstanding debt of $132,086, if we don’t include home mortgages. While this figure is down from the peak household debt just before the Great Recession, it is still very high.

Why US Households Have Such Large Average Debt Levels

The kneejerk answer to this question is simply that families spend more than they earn. And that would be true, but there’s more to it than that. The rise in the cost of living has outpaced income growth over the past 12 years.

While median household income has grown 26% since 2003, household expenses have outpaced it at 29%-- with medical costs growing by 51% and food and beverage prices increasing by 37% in that same span (2003-2015).

While 3% may not seem like a significant difference, note that the cost of living has exceeded income every year since 2008. And this gap becomes much more significant for Americans that have acute or chronic health problems, or live in a city with a high cost of living or are attending college.

Only three of the major spending categories haven’t outpaced income growth: apparel, recreation and transportation. But apparel and recreation are relatively immaterial expenses; they don’t make up a large portion of the typical consumer budget.

Given these factors, it makes more sense, then, that debt has increased during this time. The cost of living has simply outpaced household incomes on average.

The point to be made here is that US household debt, while down from the peak before the Great Recession, is still huge – at over $132,000 if we don’t include home mortgages, and over $263,000 if we do include them.

These debt levels are daunting for most American families. This is yet another reason the economic recovery since 2009 has been the slowest since 1949.

Wishing you a great end of summer,

Gary D. Halbert

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent. |