A Comprehensive Look at Dividend Growth Stock Valuations Sector by Sector: Part 2

Introduction

Finding attractively valued dividend growth stocks is getting harder and harder to do. The overall market has been on a relentless advance for many years now, and high quality dividend paying growth stocks have been leaders. Consequently, valuations have become extended beyond historical norms and I contend prudence. Nevertheless, there are attractive dividend growth stocks available if you’re willing to look hard enough.

In part 1 of this two-part series I reviewed the prestigious S&P Dividend Aristocrats looking for attractively valued dividend growth stocks. Although I was able to identify a few potentially attractive research candidates in the Dividend Aristocrats, I lamented that the pickings were slim. I also presented examples of extremely high quality Dividend Aristocrats that have become significantly and uncharacteristically overvalued relative to their fundamentals. I did this for perspective.

In this second installment I have broadened my scope looking for attractive dividend growth stocks wherever I can find them. Later in this article I will present several examples of apparently attractive dividend growth stock research candidates across several sectors and subsectors. One important aspect of this exercise is to illustrate that the best valuations are primarily limited and available in only a few sectors. But most importantly, as should be expected in a strong bull market like we have today, the best valuations are generally found in the individual companies and sectors that are currently out-of-favor. To paraphrase the legendary Warren Buffett, you can’t buy what’s popular and expect to do well.

When conducting my research and screening for attractive dividend growth stock research candidates, my primary focus was on attractive valuation. However, I was also looking for companies with the most consistent and reliable historical records of earnings and dividend growth. However, companies with perfectly consistent operating histories are rare. Therefore, I included a few examples without stellar long-term records, but reasonably attractive records over the past five years or so. Nevertheless, I did exclude several companies that were technically attractively valued, but in my judgment I did not like the significant inconsistency or cyclicality in their operating histories.

Additionally, I limited my screen to companies offering a current yield of 2% out to a maximum of 5% for traditional companies, but I did include a few REITs with higher yields. My purpose for limiting the current yield was to avoid the most aggressive high-yield securities such as mortgage REITs, business development companies, royalty trusts and MLPs, because I consider them in a different risk category and therefore not appropriate for this exercise.

A Long-Term Historical Review

With this article I will be presenting numerous examples across all the major sectors and subsectors in the market. In all cases I will be presenting the longest operating history available to me for each company. Each example will be presented utilizing the earnings and price correlated F.A.S.T. Graphs™ on each. Therefore, in order for the reader to get the most benefit from this exercise, it’s imperative that you understand what each of the earnings and price correlated graphs are revealing.

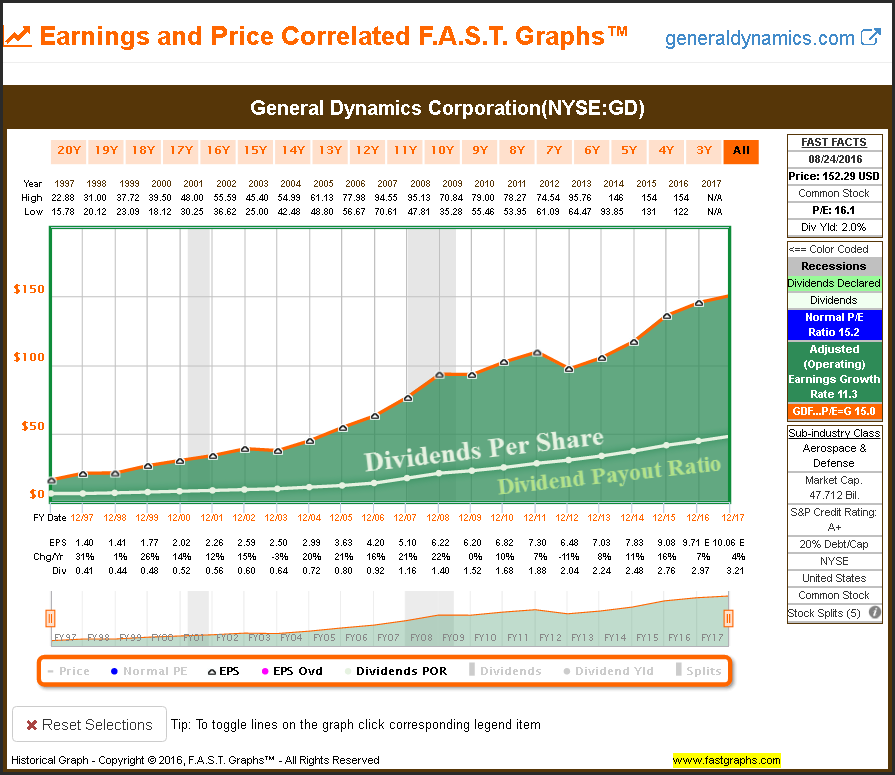

Therefore, I offer the following short tutorial where I take a complete F.A.S.T. Graphs apart and then add one metric at a time. I will be utilizing the General Dynamics’ graph as my sample .This template will apply to all of the graphics utilized in the article.

The orange line on each graph represents a valuation reference line drawn as a multiple of earnings on each company at a specific P/E ratio. In theory, this line represents a rational view of a company’s fair value. The dark green shaded area below the line represents the company’s total earnings over the timeframe graphed.

Next I have added the light green line (it appears white to many) which plots the company’s dividends per share over the timeframe graphed. A quick examination of this line will tell you whether dividends have been steadily increasing, or whether they have been cut at some point. The area below the light green line represents the portion of earnings paid out as dividends - commonly referred to as the dividend payout ratio.

Dividends are also expressed after they have been paid out of earnings as a light green shaded area and stacked on top of the orange valuation reference line. Therefore, dividends are expressed prior to being paid out by the light green (white) line, and after they have been paid out to shareholders expressed as the light green shaded area on top of the orange line.

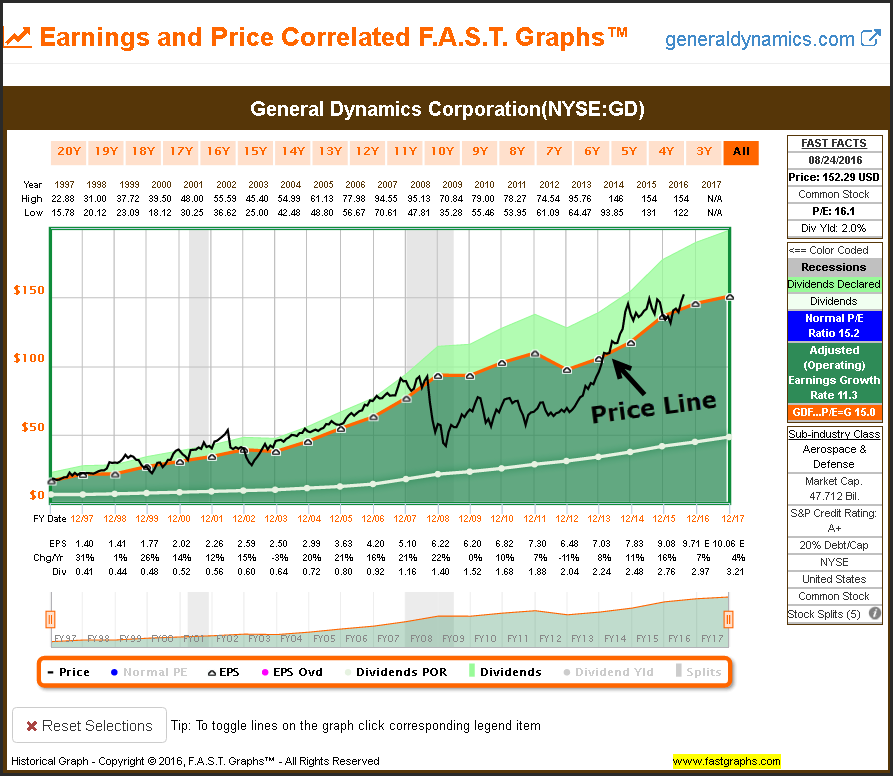

Next the black line representing monthly closing stock prices is added and correlated with the orange valuation reference line. Stated overly simplistically, when the price is above the orange line overvaluation is present, when the price is touching the orange line fair valuation is present, and finally, when the price is below the orange line undervaluation is indicated.

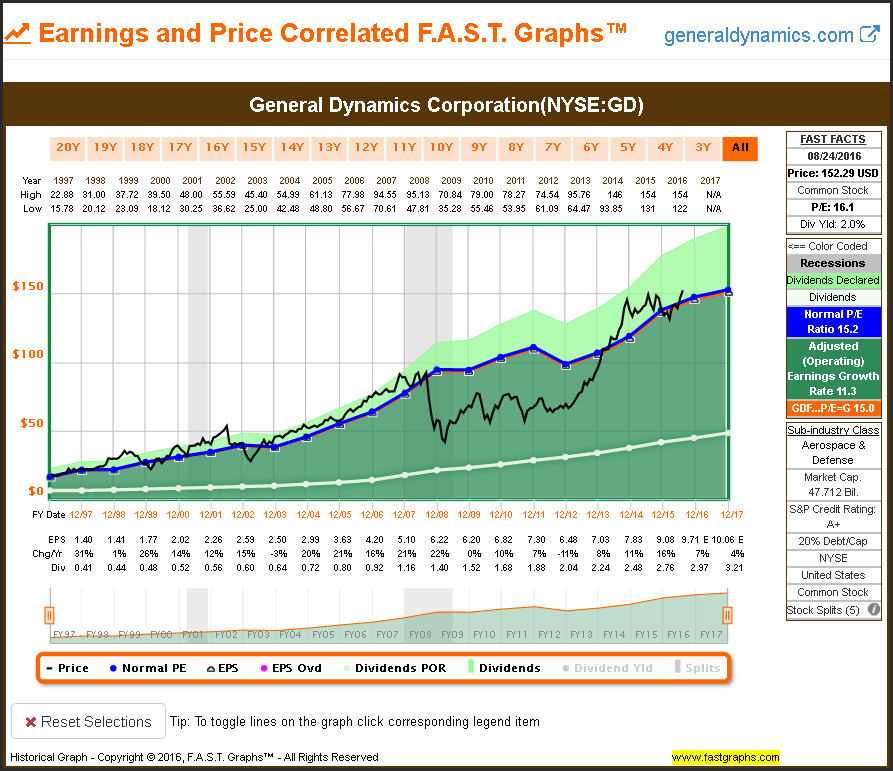

The final metric added to the graph is the historical normal P/E ratio represented as a dark blue line. This calculates the valuation that the market has typically applied to each company over the timeframe graphed. The dark blue normal P/E ratio line adds a second valuation reference to each graph. Analysis of both of these valuation reference lines provides the reader an analytical perspective of historical valuation. (Note: In the case of the General Dynamics’ example, both the orange and blue line converge, however, the blue normal P/E ratio is moderately higher and can be seen in the FAST FACTS boxes to the right of each graph).

In many of the actual examples, these lines will be separated, and the reader can decide for themselves which represents the best valuation reference for each example being examined. Furthermore, it’s important to note that these lines could change when different timeframes are drawn. However, for the purposes of this article, each graph is drawn with the maximum timeframe available.

A Sector and Subsector Valuation Review

Before the reader goes beyond this point, I would like to explain that although I have included numerous examples of apparently fairly valued dividend growth stock research candidates in this article, they represent only a very few attractively valued stocks in the context of the whole market. This was perhaps the most ambitious look at valuation I have ever personally engaged in. Using the F.A.S.T. Graphs™ screening tool I went through every sector and then every subsector looking for every reasonably valued dividend paying company in the universe comprised of more than 19,000 companies.

What I have presented here represents the very few that I considered reasonably valued enough to be included. The pickings are indeed very slim in today’s overheated market. Additionally, I will add that I’ve included names that I personally might never consider as investments in my own portfolio. However, my purpose was to provide a broad and deep look at valuations in today’s market. Perhaps many of you will find some companies you like, and like me, see many companies that you would not consider appropriate for your own portfolios. So to be clear, these are not recommendations, instead, this is a comprehensive review of the current valuations of dividend paying stocks available in today’s generally highly-valued market.

The following examples will be presented on a sector by sector basis. With each example, it will be listed in its primary sector followed by its subsector. I will provide a brief commentary on each major sector expressing my general view of the attractiveness of companies within those primary sectors.

Industrials

A common trait among industrial companies is cyclicality of earnings. However, in many cases, the long-term dividend records are quite consistent. Consequently, dividend growth investors investing in this sector can expect the occasional interruption in earnings growth even for those companies with consistent long-term records of increasing their dividends.

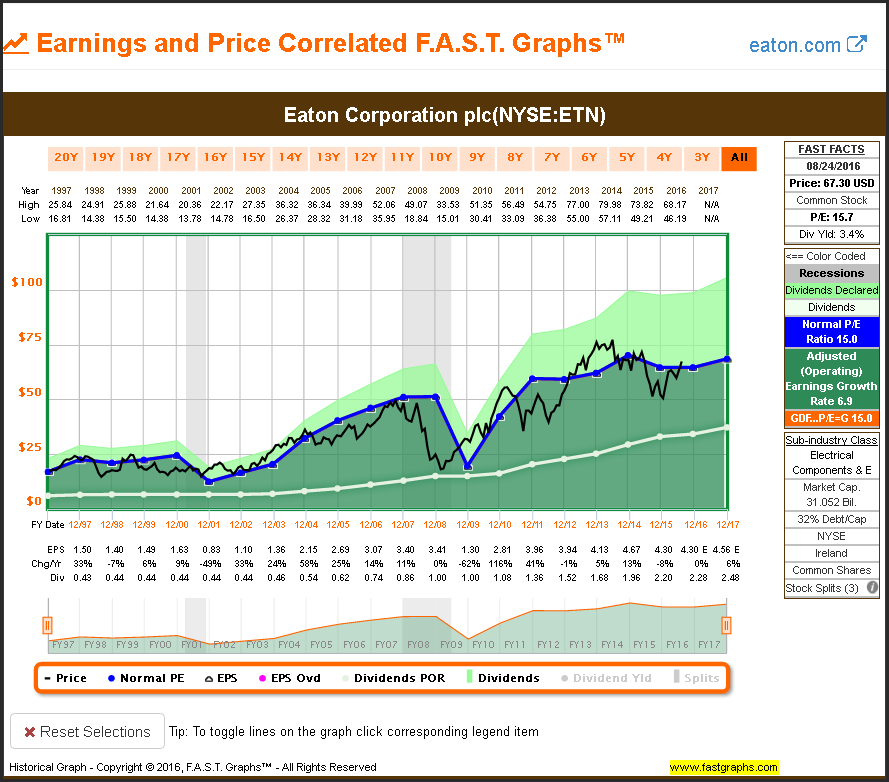

Industrials – Aerospace and Defense

Industrials – Electrical Components and Equipment

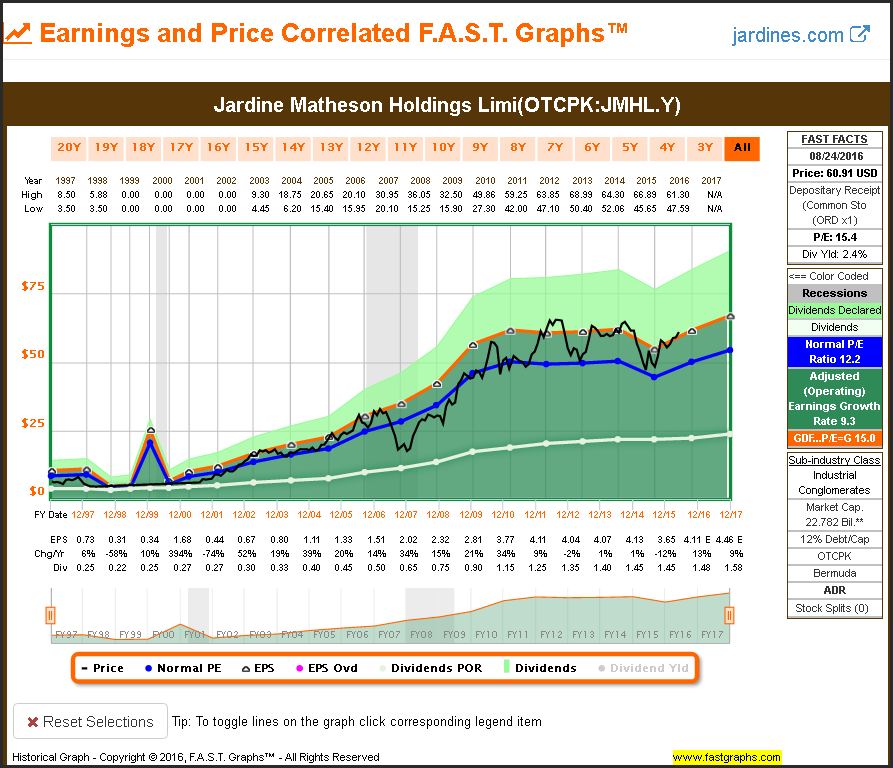

Industrials – Conglomerates

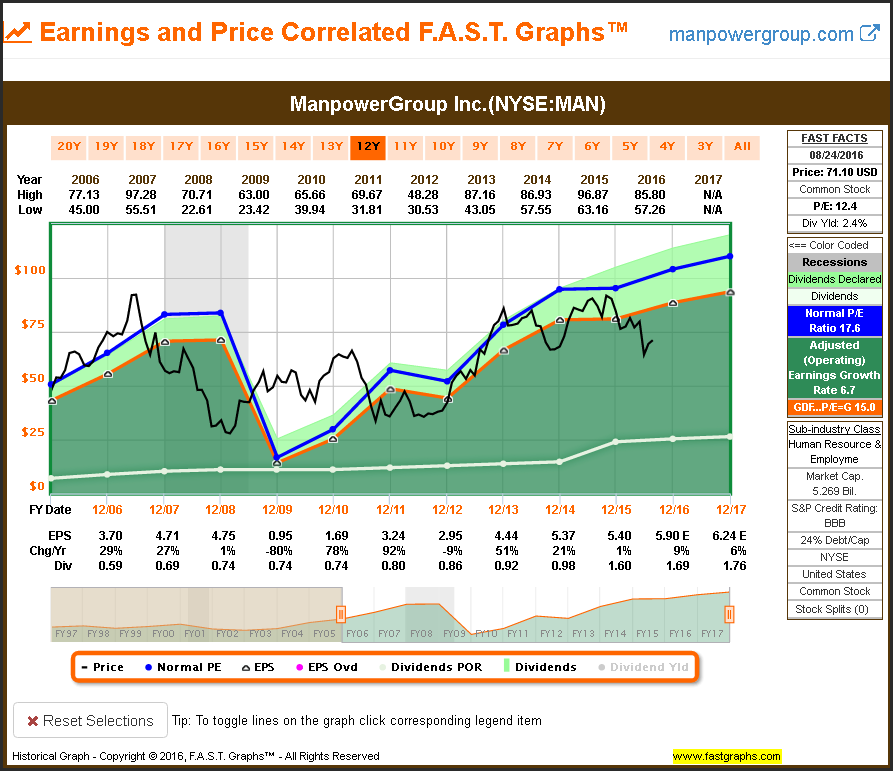

Industrials – Human Resources and Employment

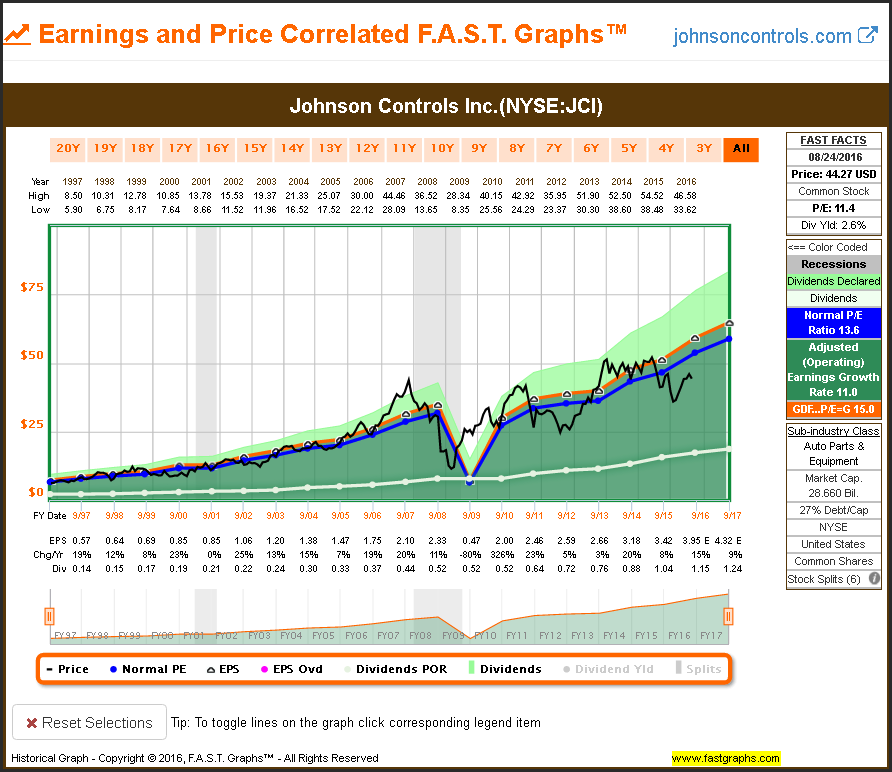

Industrials – Construction and Machinery

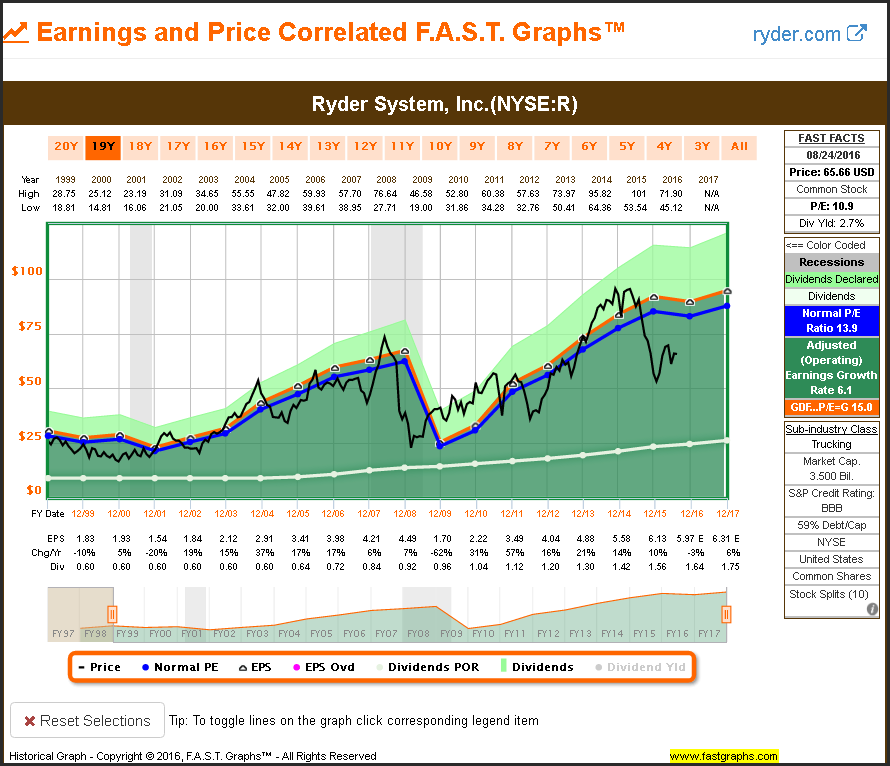

Industrials – Trucking

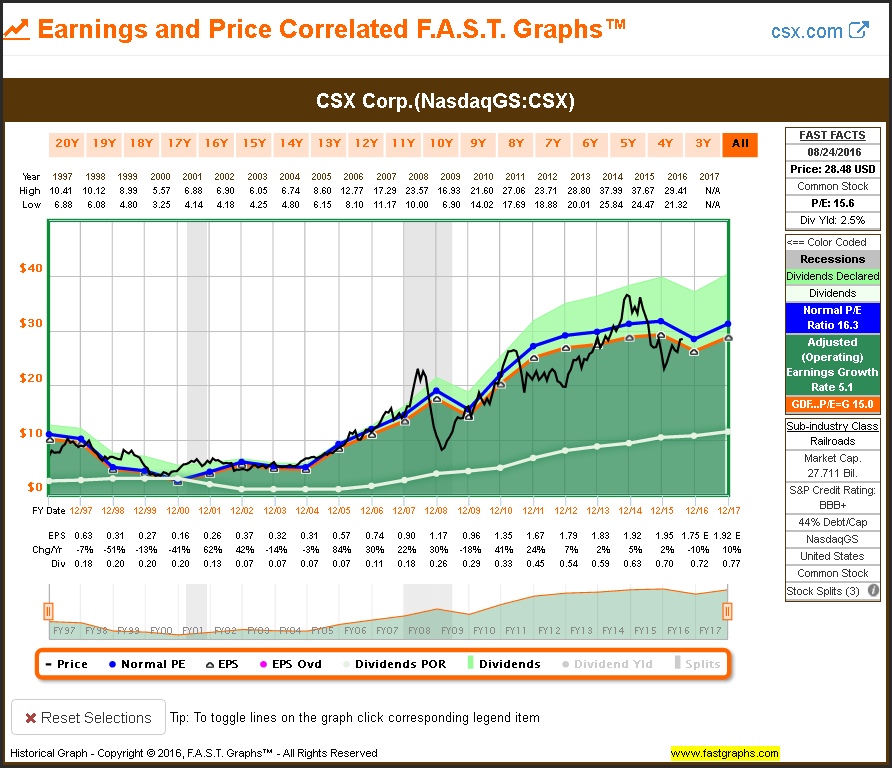

Industrials – Railroads

Materials

The materials sector is another sector comprised of companies, many of which have quite cyclical operating histories. Moreover, my analysis has led me to conclude that the dividend records in this sector are also questionable. However, there are many prominent and widely-recognized names within this sector, and some that many of you may not have looked at before.

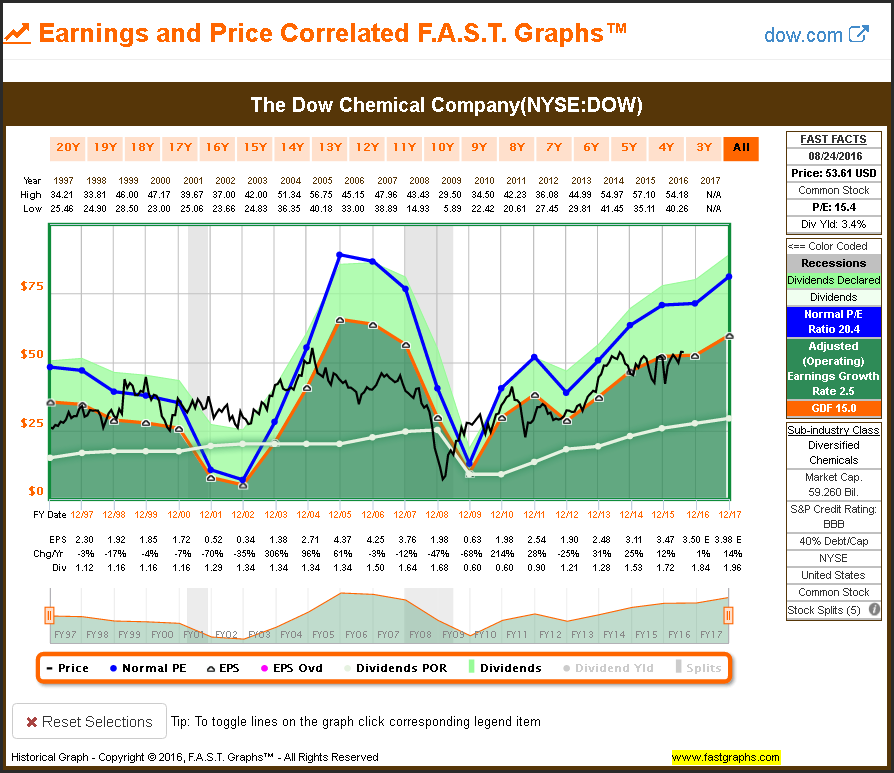

Materials – Diversified Chemicals

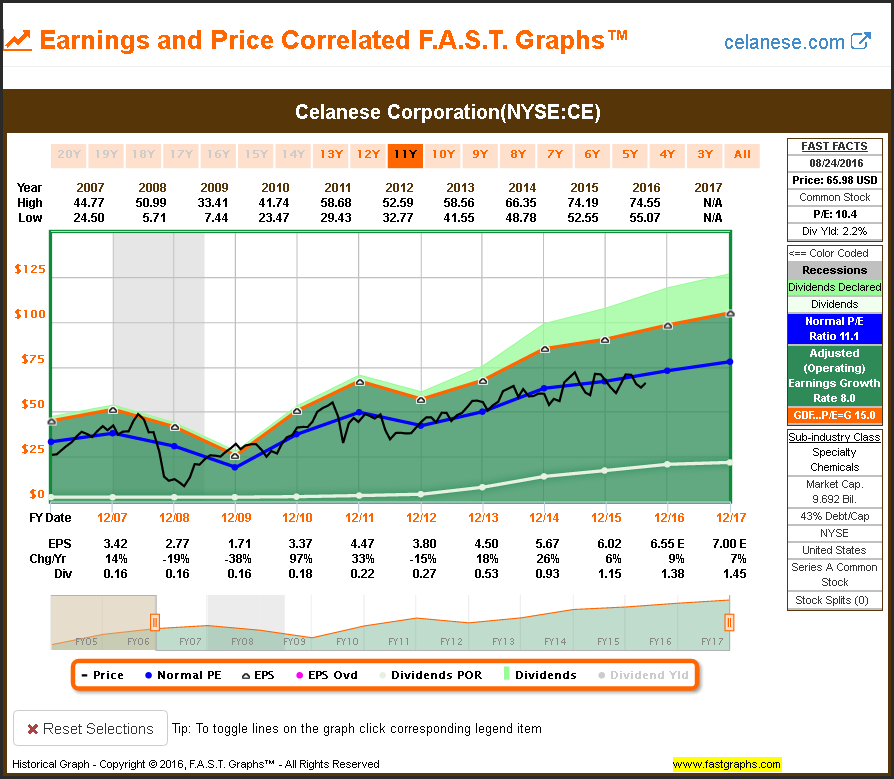

Materials – Specialty Chemicals

Materials – Aluminum

Materials – Steel

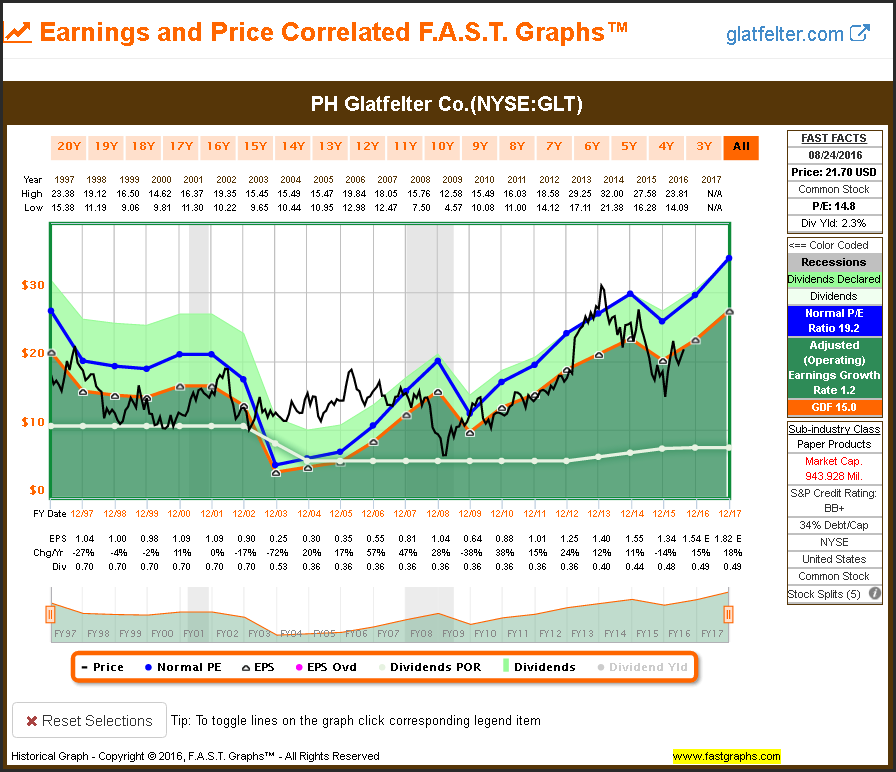

Materials – Paper Products

Financials

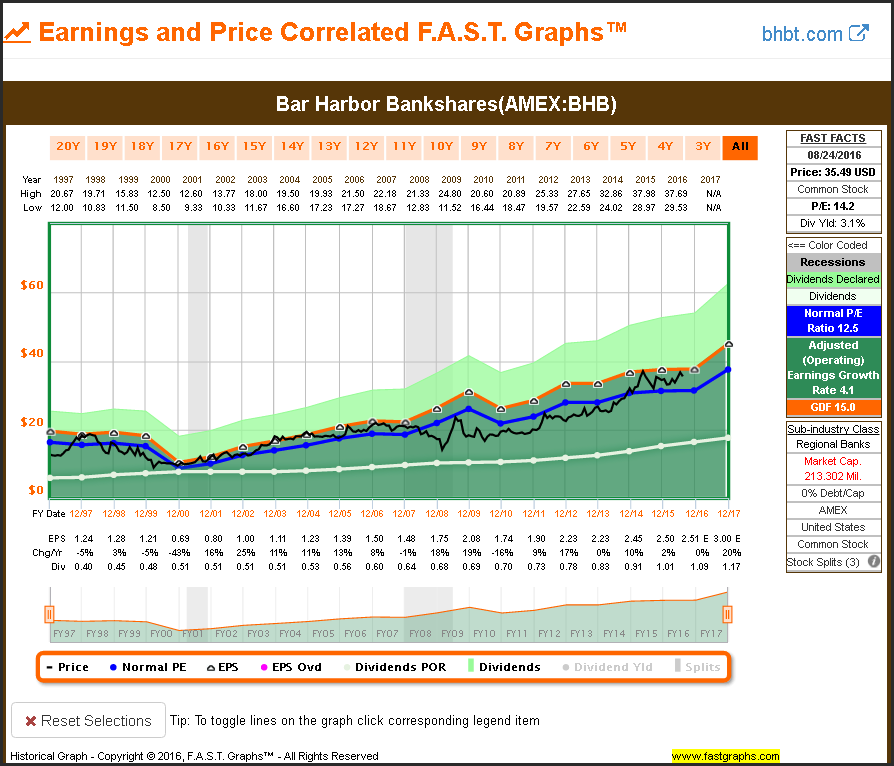

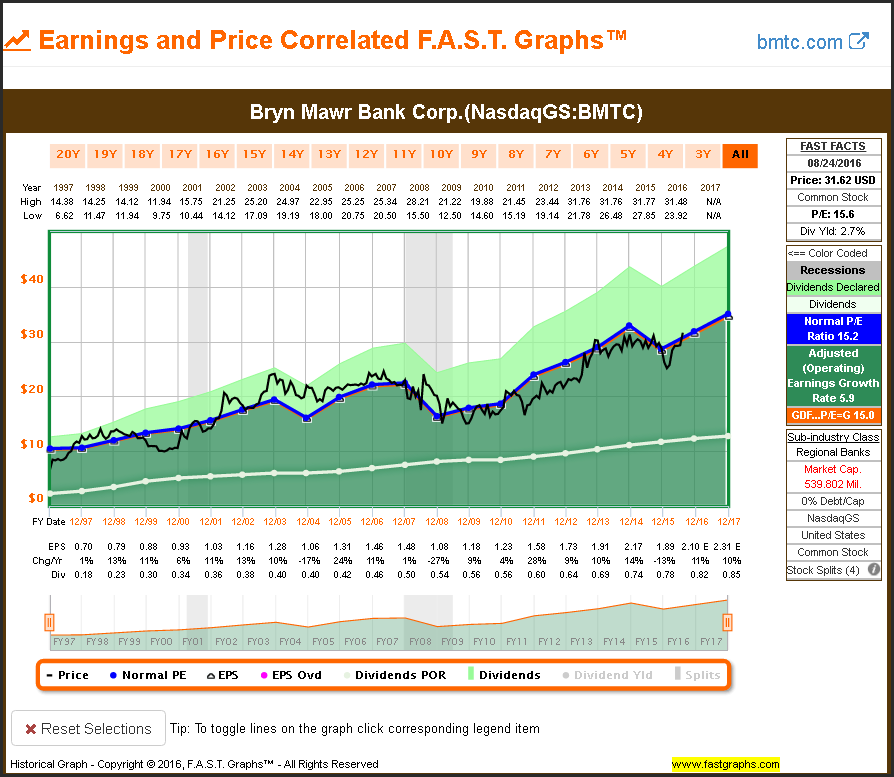

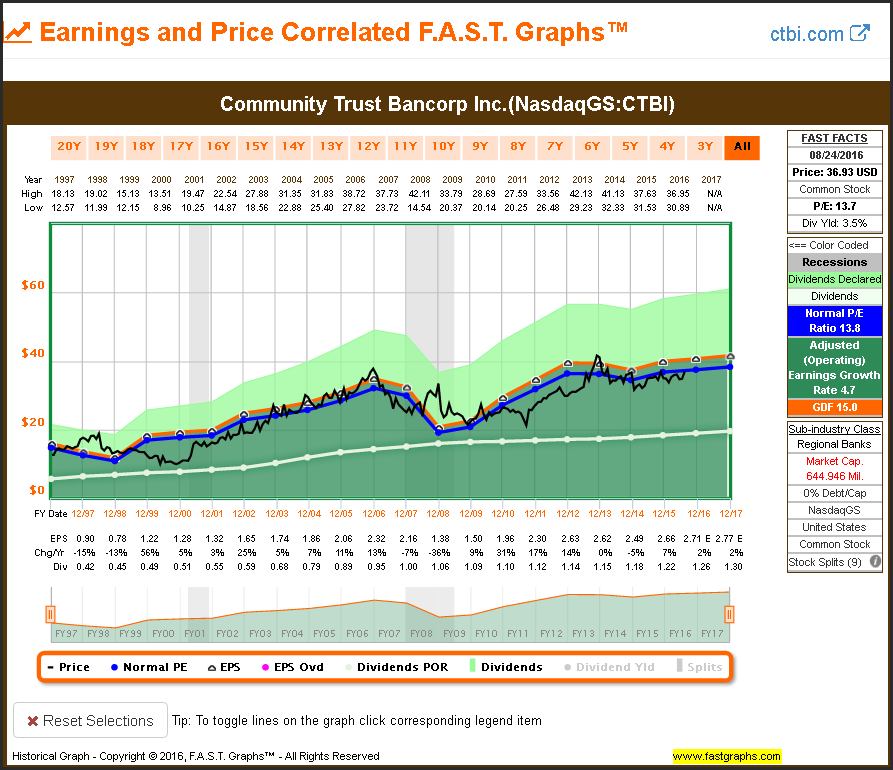

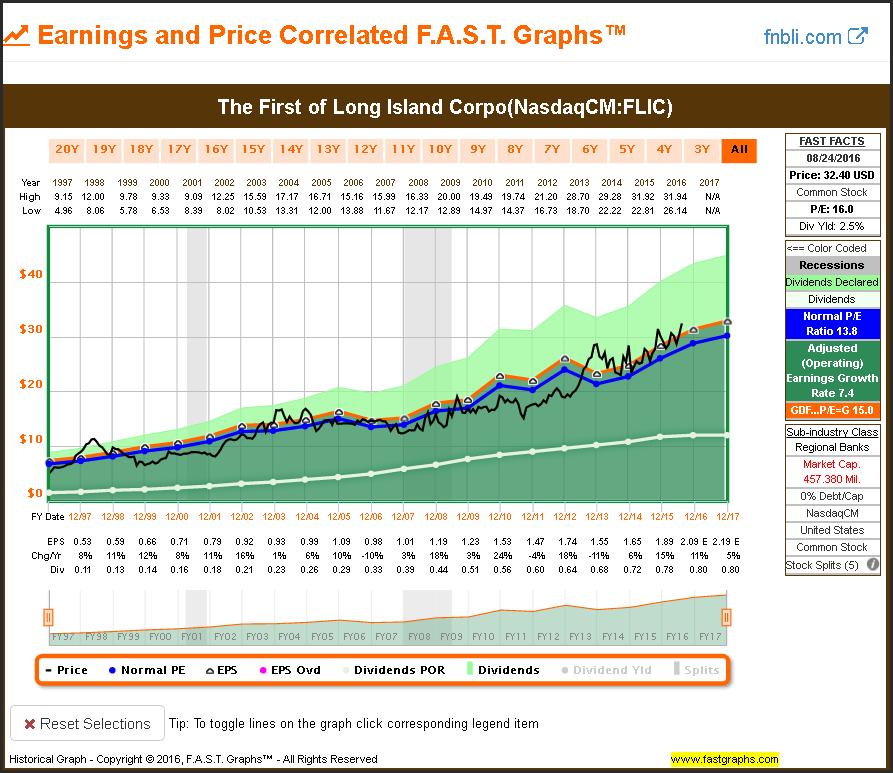

The financial sector has been one of the most out-of-favor sectors since the Great Recession debacle, which many believe was created by companies within this sector. Consequently, this is one sector where I was able to find lots of attractively valued research candidates. The regional bank subsector is where I found the most value, as well as banks that did not participate in the so-called avarice and greed of their larger counterparts. Consequently, I’ve included several, but not all, of the attractively valued regional banks I came across.

Financials- Regional Banks

Financials – Diversified Banks

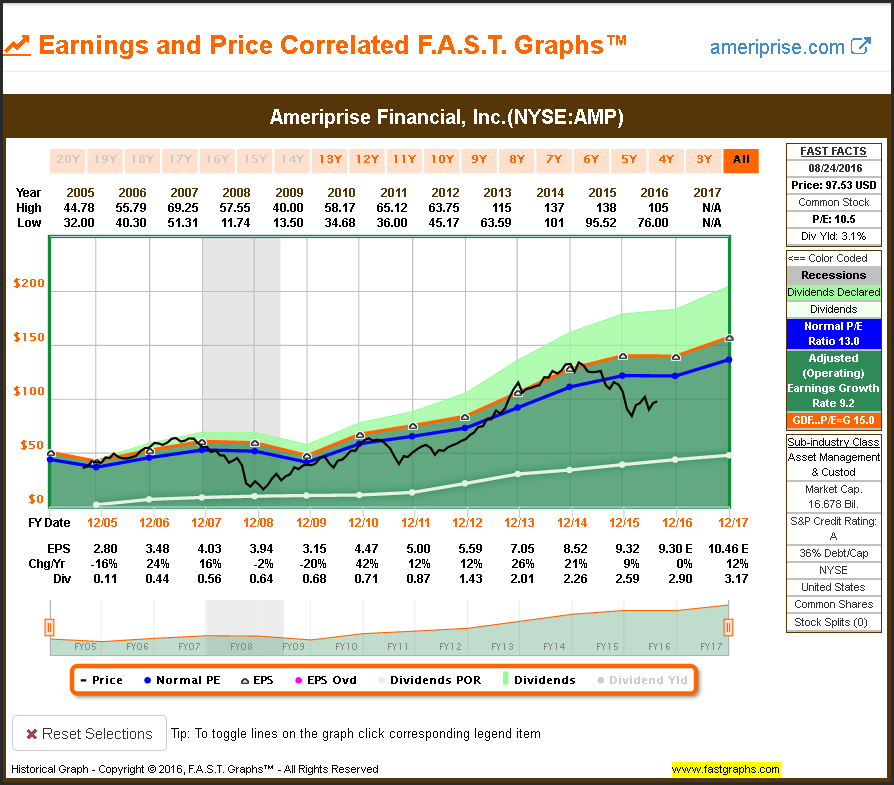

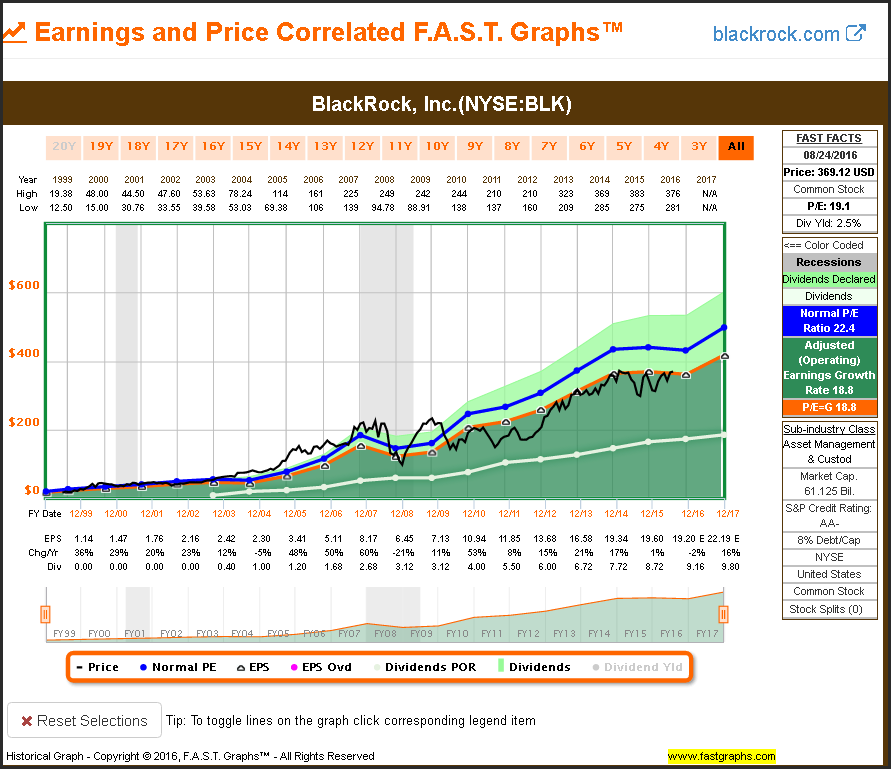

Financials- Asset Management

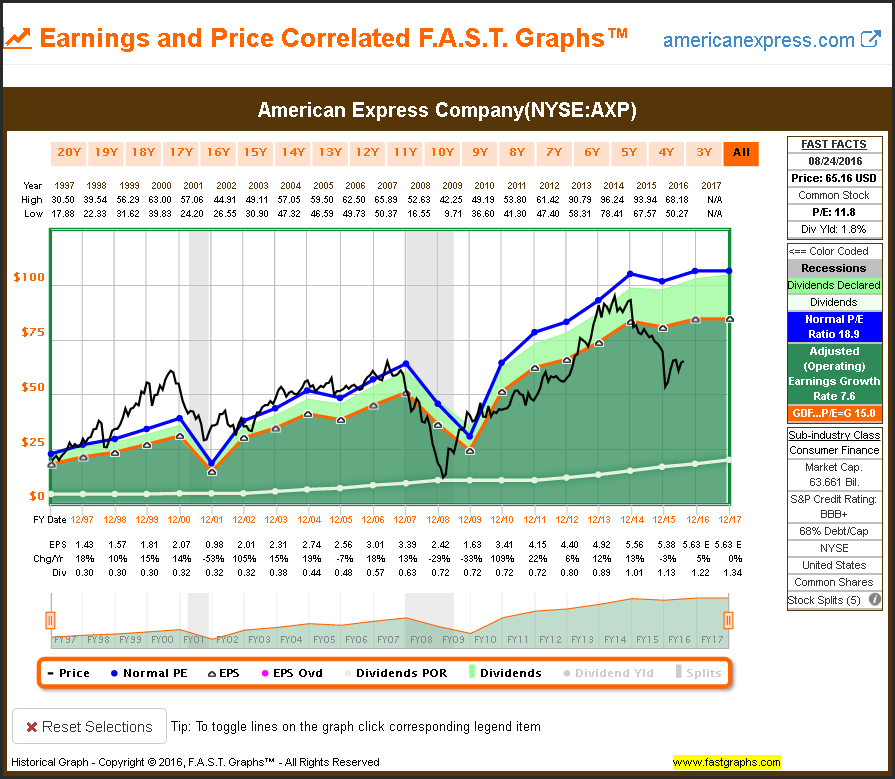

Financials – Consumer Finance

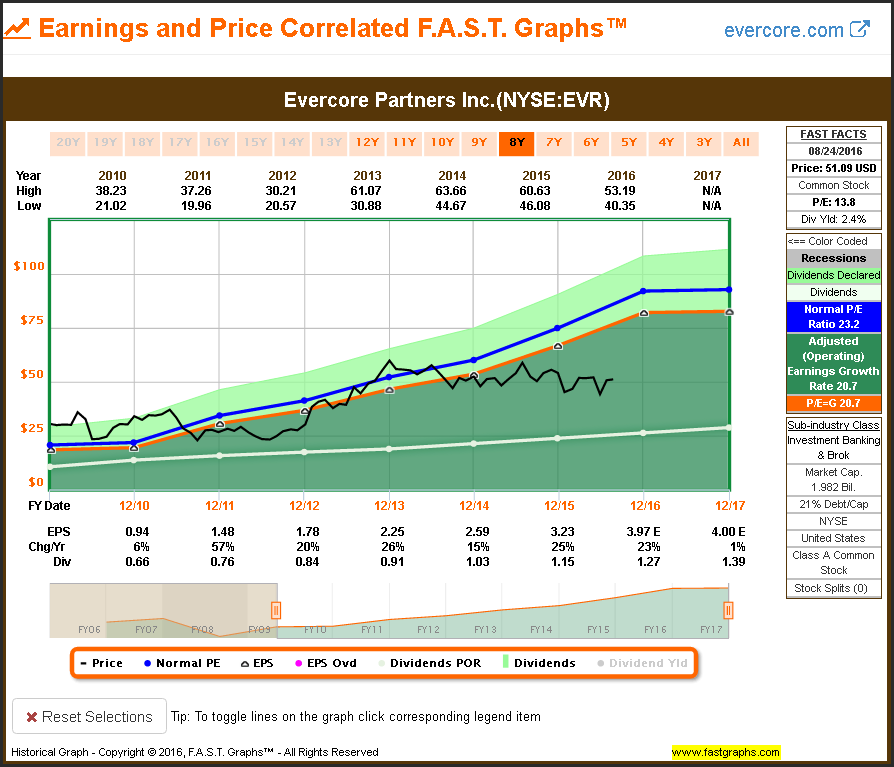

Financials – Investment Banking and Brokerage

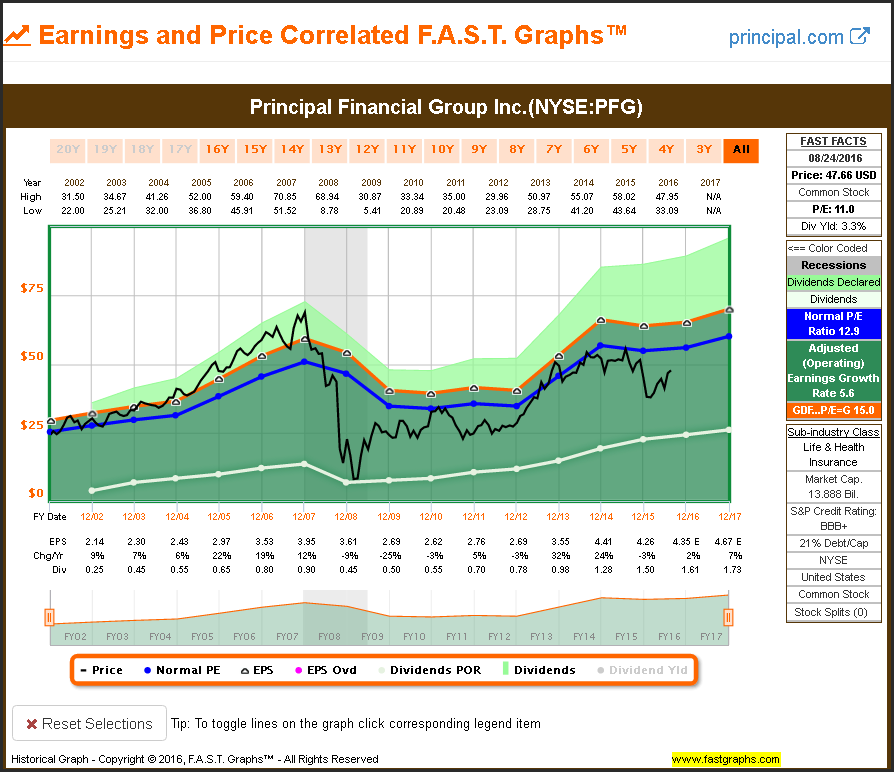

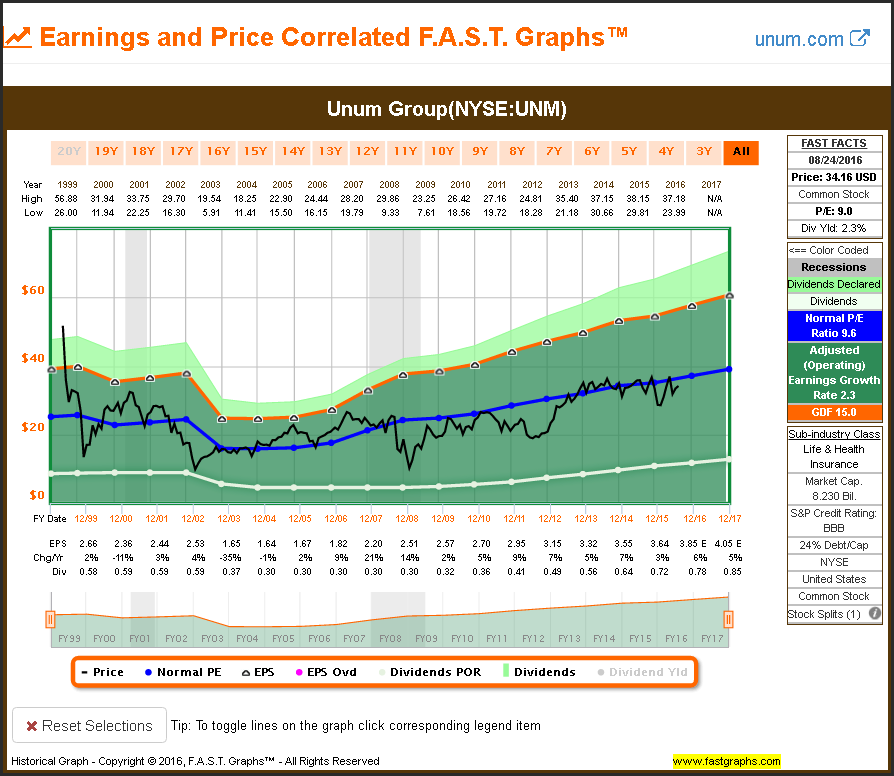

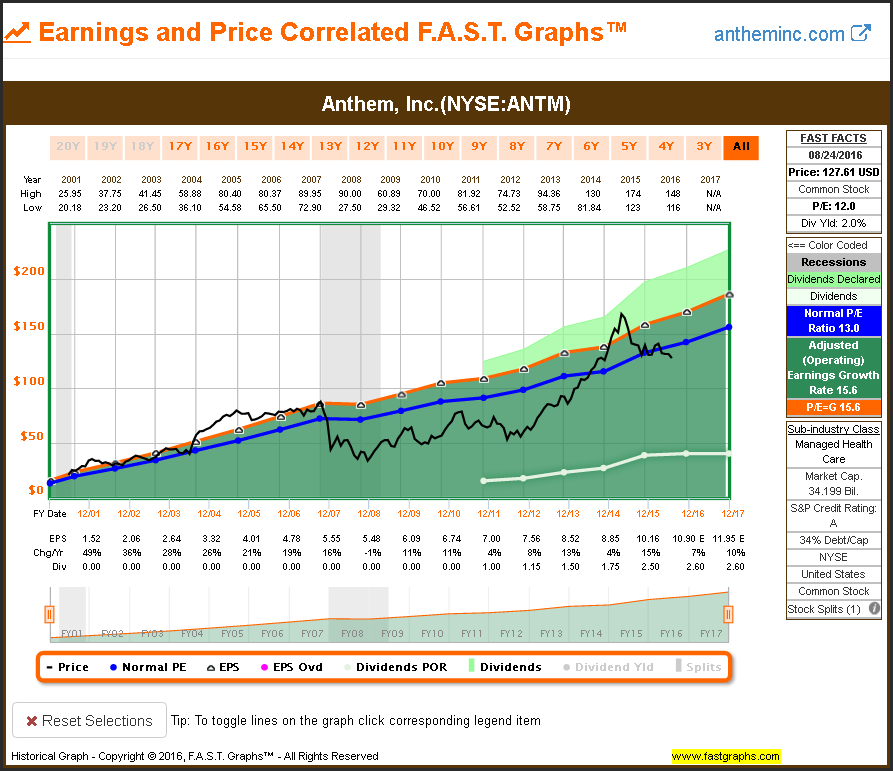

Financials – Life and Health Insurance

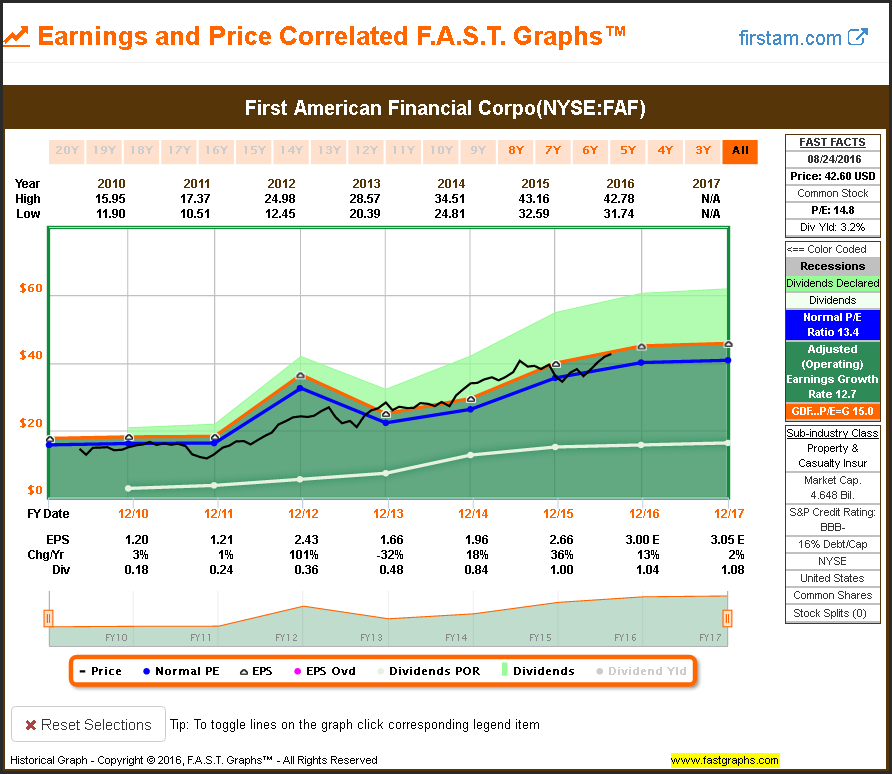

Financials – Property and Casualty Insurance

Healthcare

The healthcare sector is rather diverse and comprised of dividend growth stocks and several pure growth stocks. Of course, for the purposes of this article, I only included the healthcare companies that paid a current dividend of 2% or better. The reader might also notice that the healthcare sector has recently been out-of-favor. Consequently, many of the research candidates presented appeared currently attractively valued after being overvalued in 2015.

Healthcare – Healthcare Distributors

Healthcare – Biotechnology

Healthcare – Managed Healthcare

Healthcare – Pharmaceuticals

Consumer Discretionary

The consumer discretionary sector is also comprised a very diverse set of companies and numerous subsectors. Nevertheless, I found it difficult to find attractive valuation in this broad sector. However, I was able to find a few.

Consumer Discretionary – Apparel

Consumer Discretionary – Auto Parts

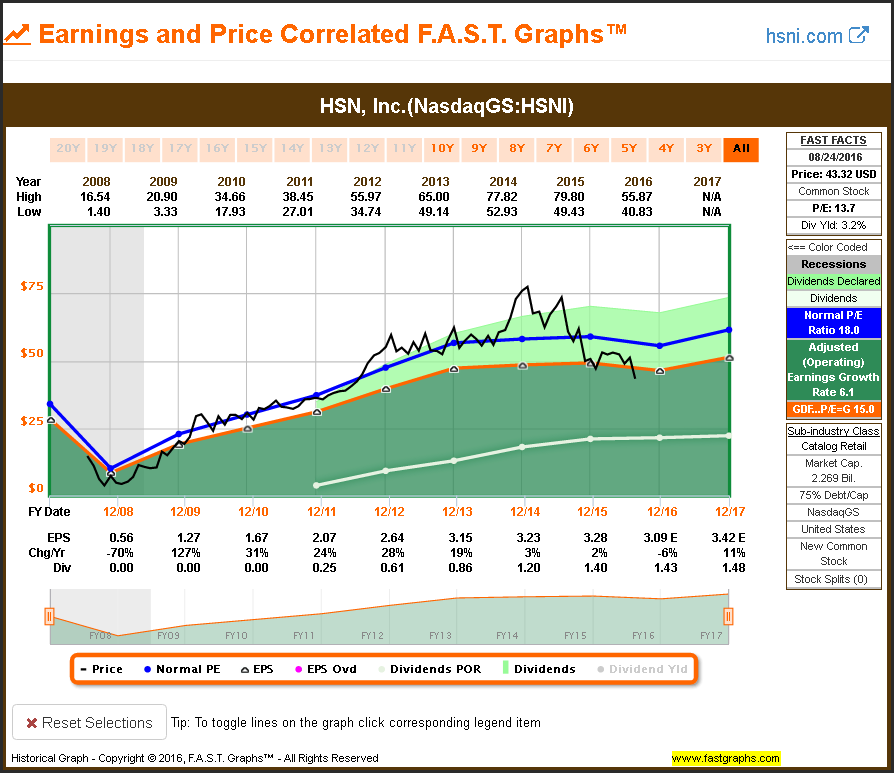

Consumer Discretionary – Catalog

Consumer Discretionary – Computer and Electronics Retail

(Note: Please excuse my boast, but as a proud father I wanted to give a shout out to my son Colton’s article on Best Buy published on August 11.)

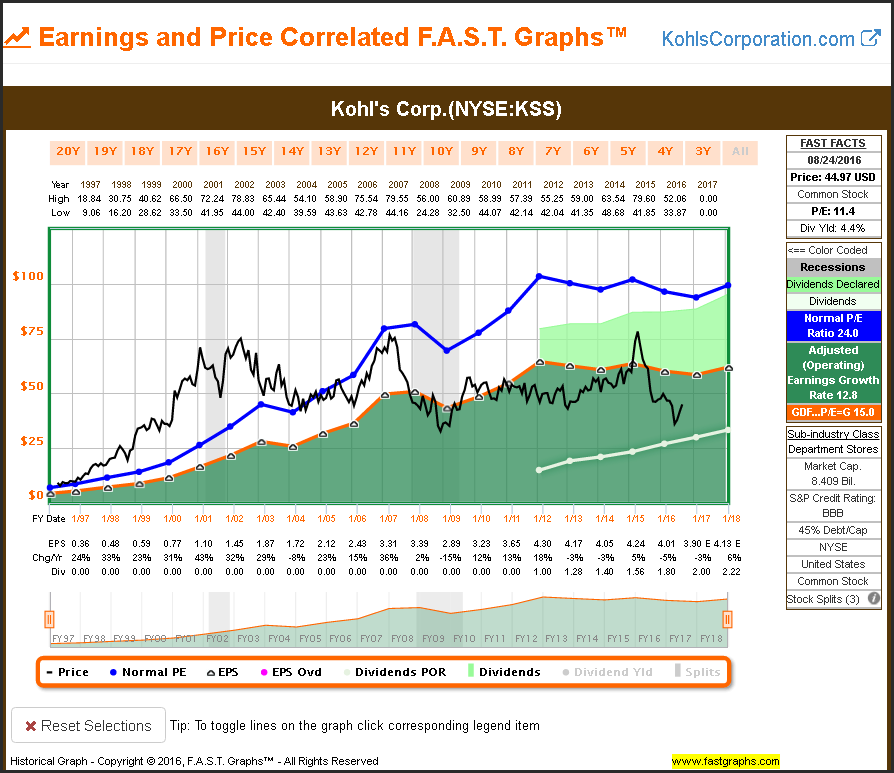

Consumer Discretionary – Department Stores

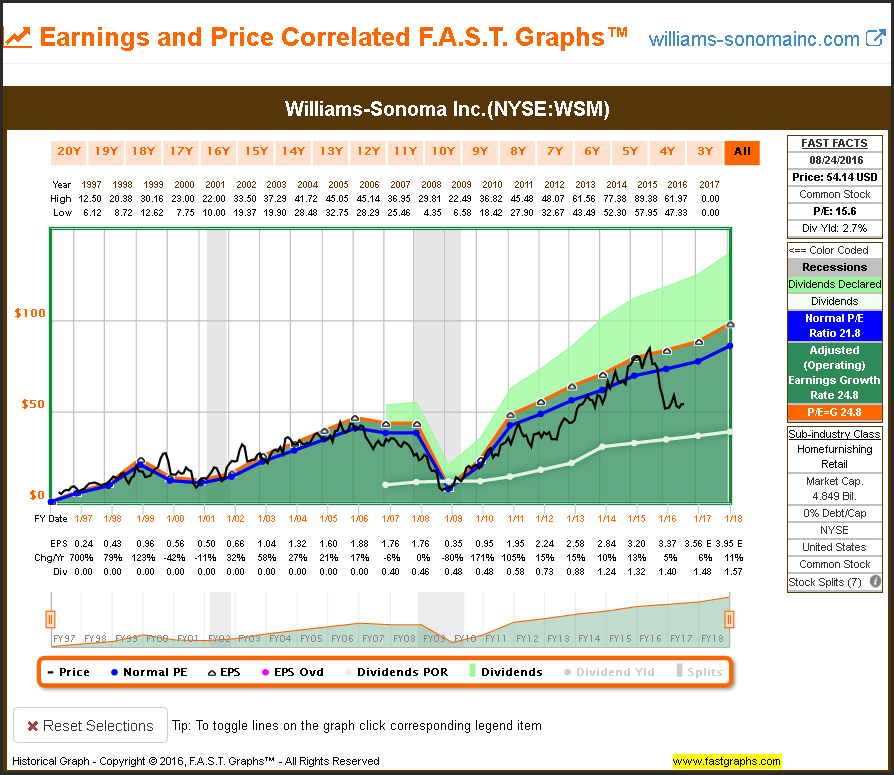

Consumer Discretionary – Home Furnishings Retail

Consumer Discretionary – Hotels, Resorts and Cruise Lines

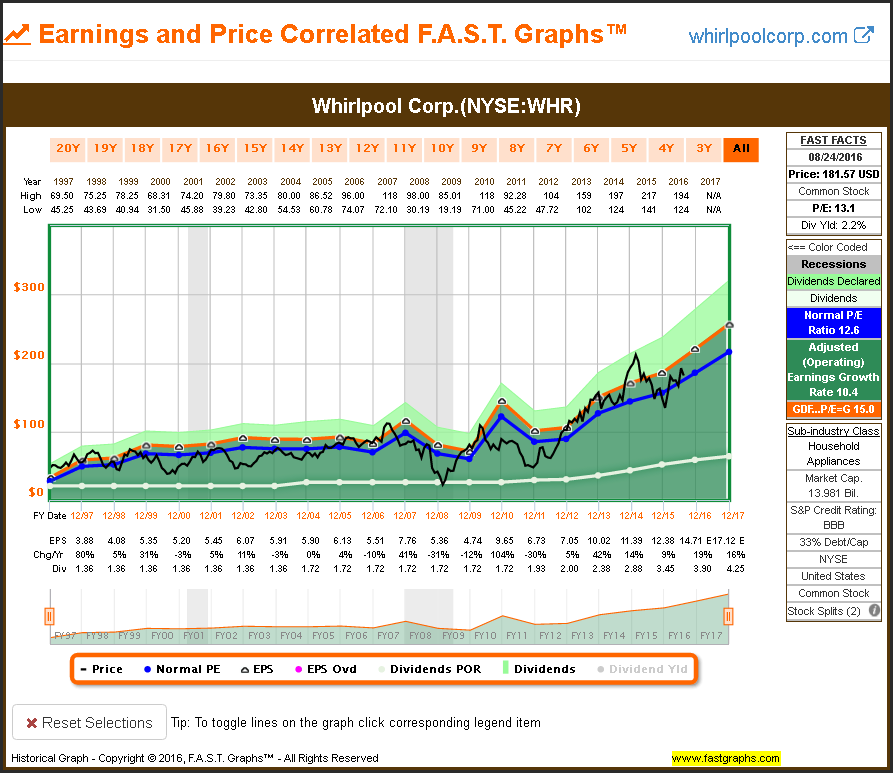

Consumer Discretionary – Household Appliances

Consumer Discretionary – Hypermarkets and Supercenters

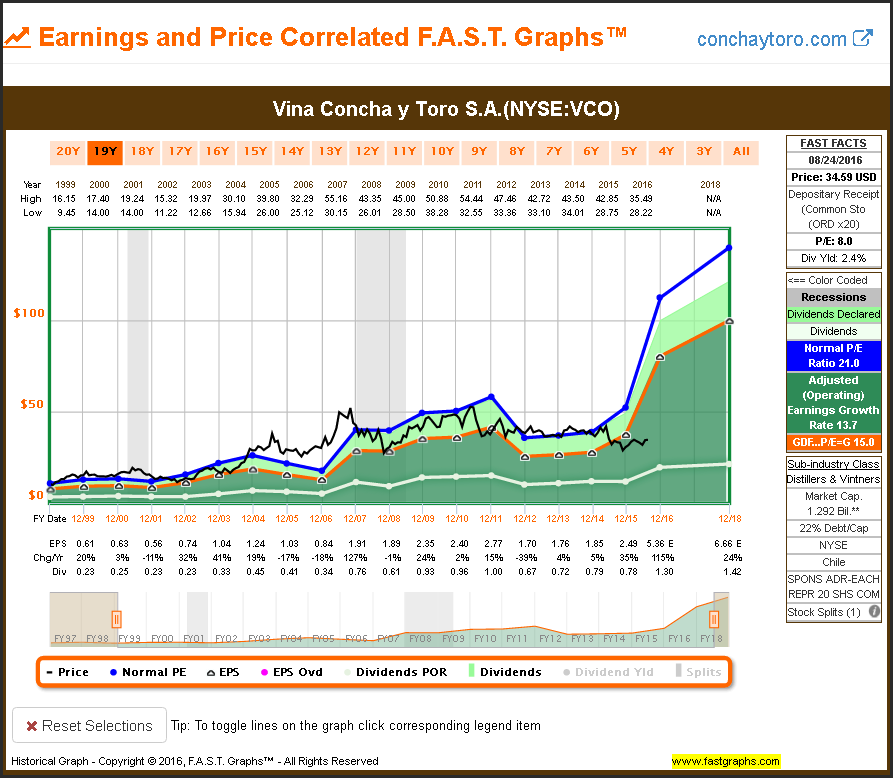

Consumer Discretionary – Distillers and Vintners

Consumer Discretionary – Agricultural Products

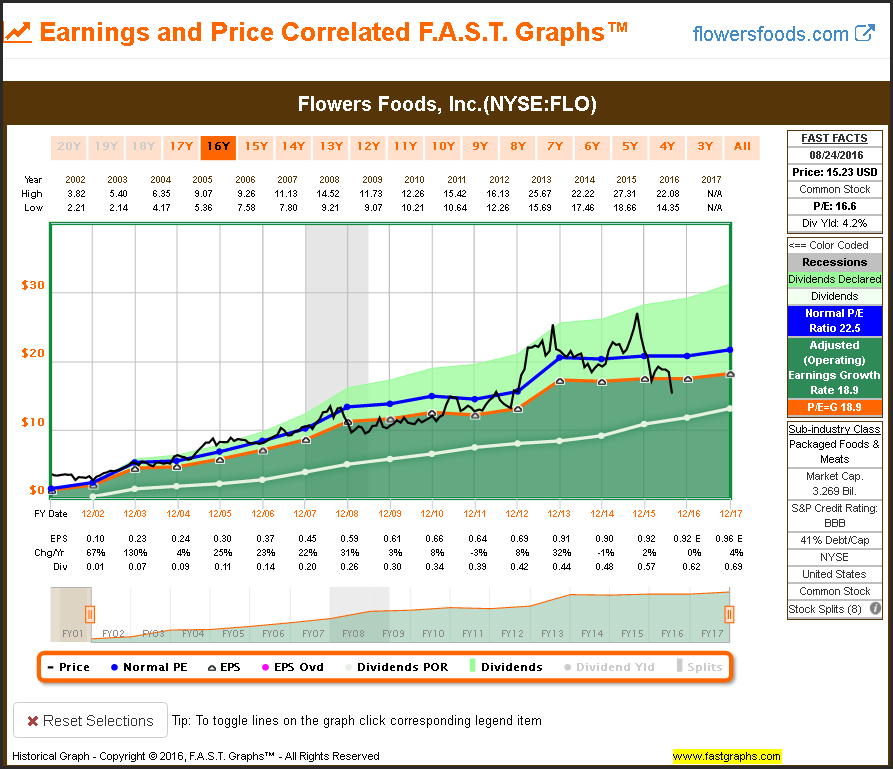

Consumer Discretionary – Packaged Foods and Meats

Consumer Discretionary – Home Improvement Retail

(Note: I presented Home Depot’s graph only since 2011, because it represents a period of time where they achieved exceptional growth. Home Depot would look overvalued on longer term graph).

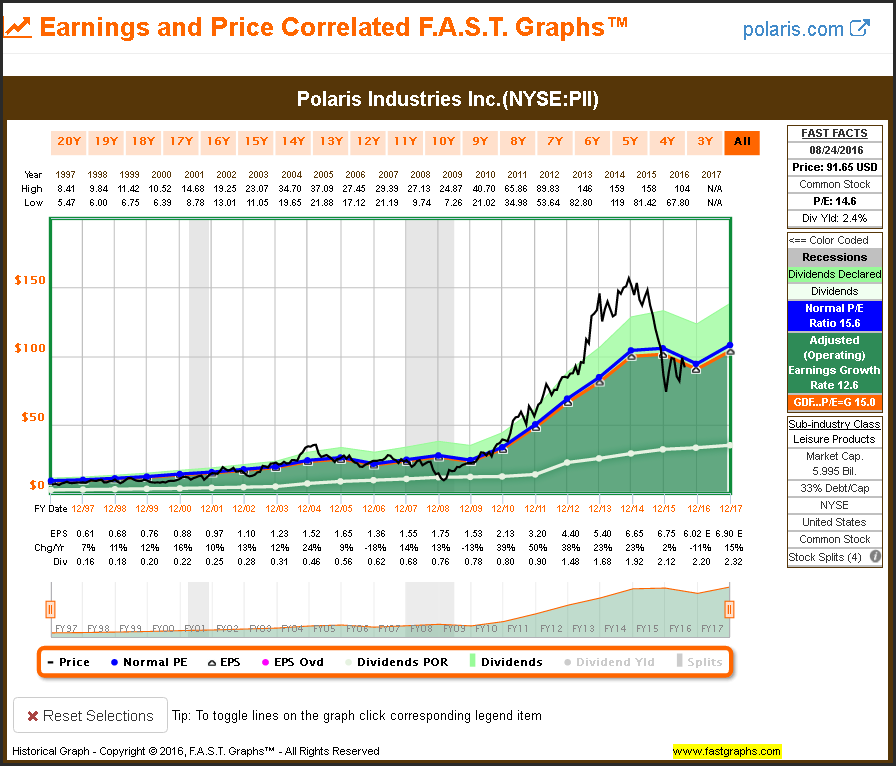

Consumer Discretionary - Leisure Products

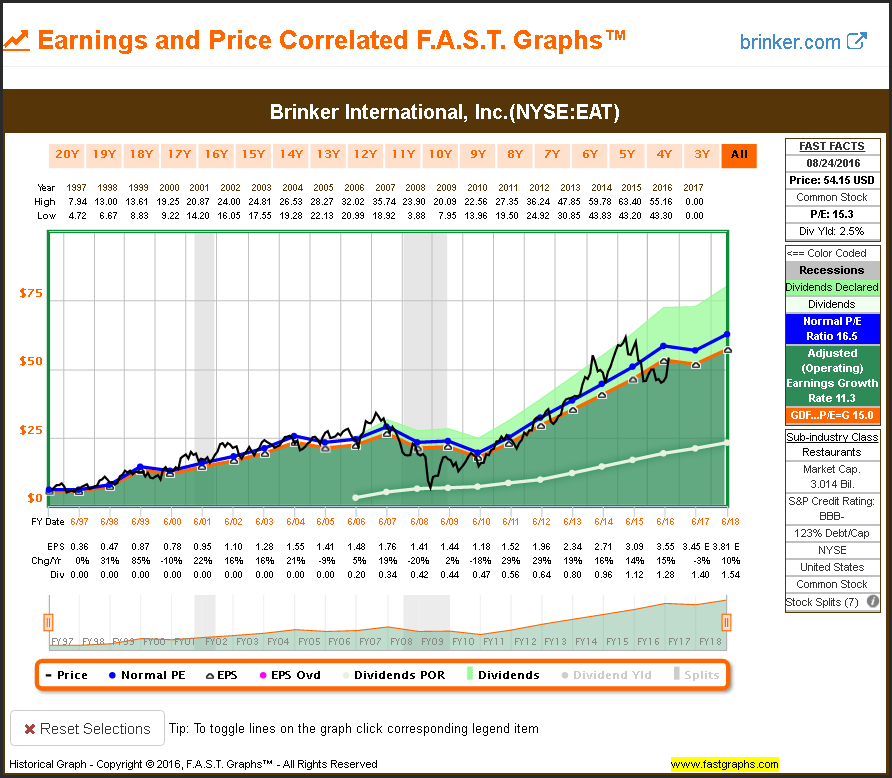

Consumer Discretionary – Restaurants

Information Technology

Information technology is another interesting sector with companies operating in numerous and diverse subsectors. Moreover, as it relates to the dividend growth investor, several companies in this sector have recently morphed from pure growth stocks into dividend growth stocks. Consequently, many do not have a long history of increasing their dividends as seen in other sectors, but some do.

Information Technology – IT Consulting and Other Services

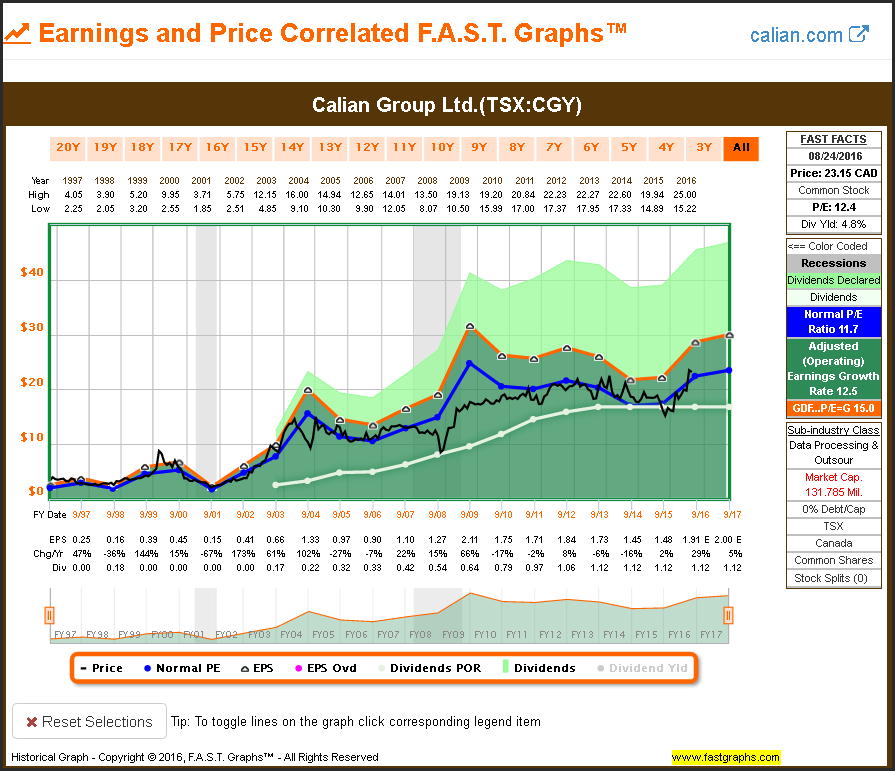

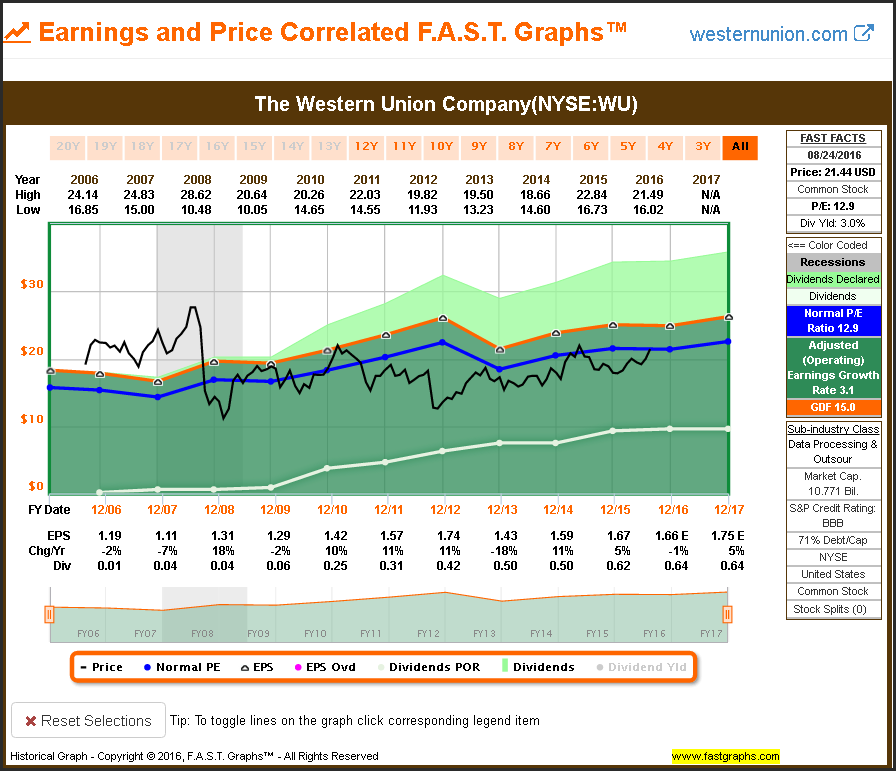

Information Technology – Data Processing and Outsourcing

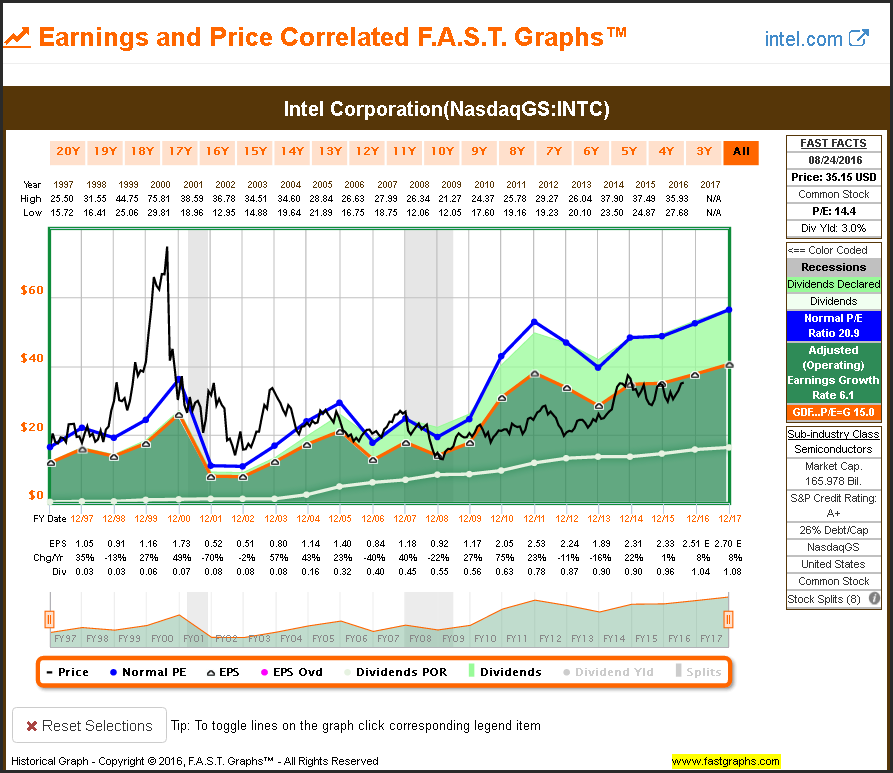

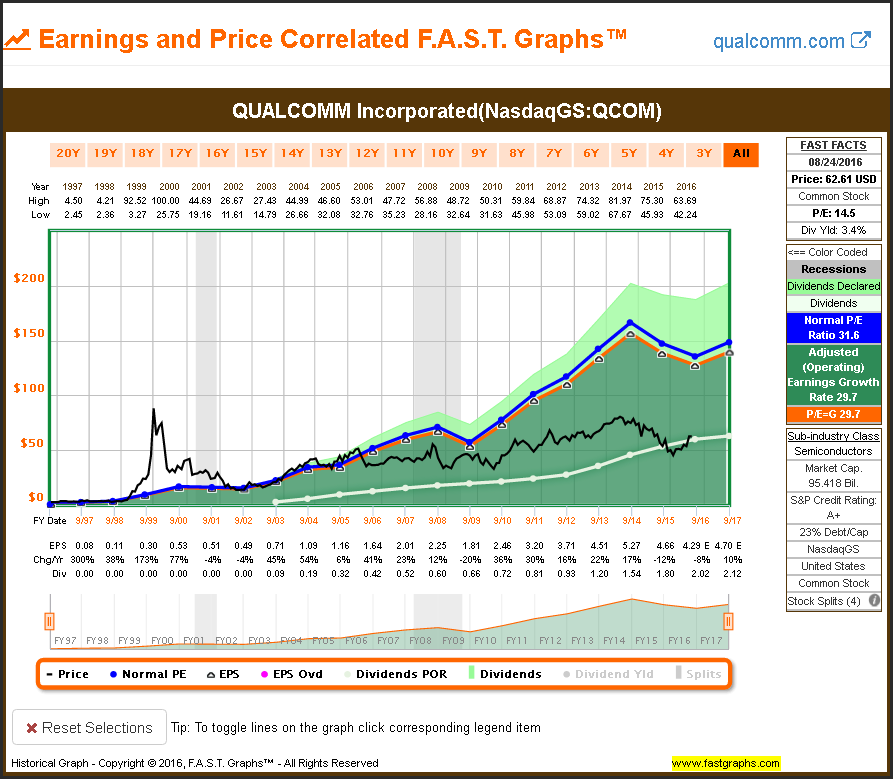

Information Technology- Semiconductors

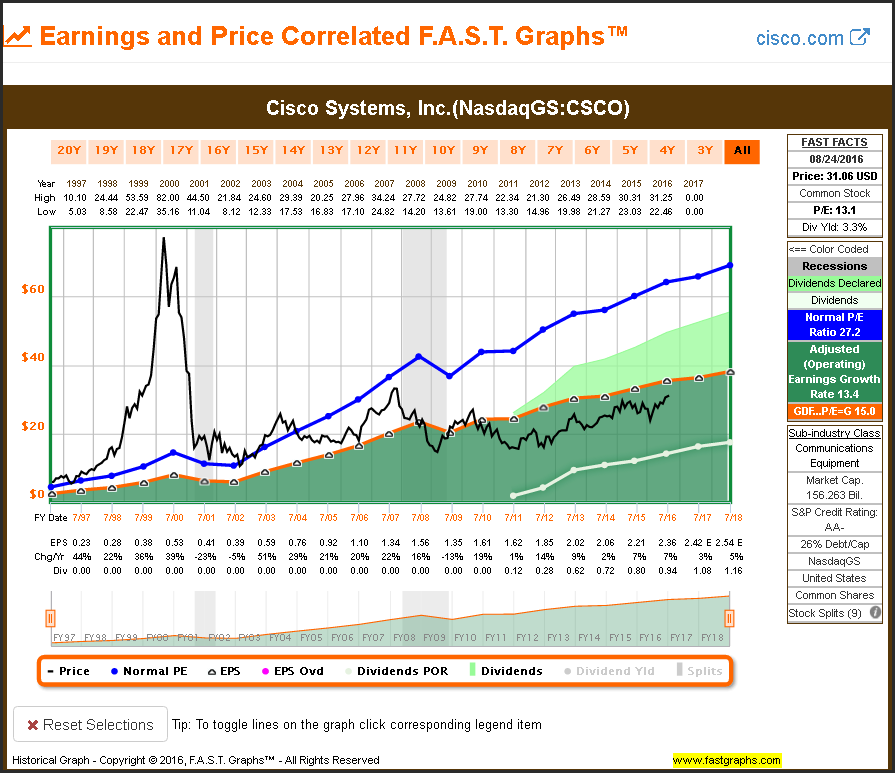

Information Technology - Communications Equipment

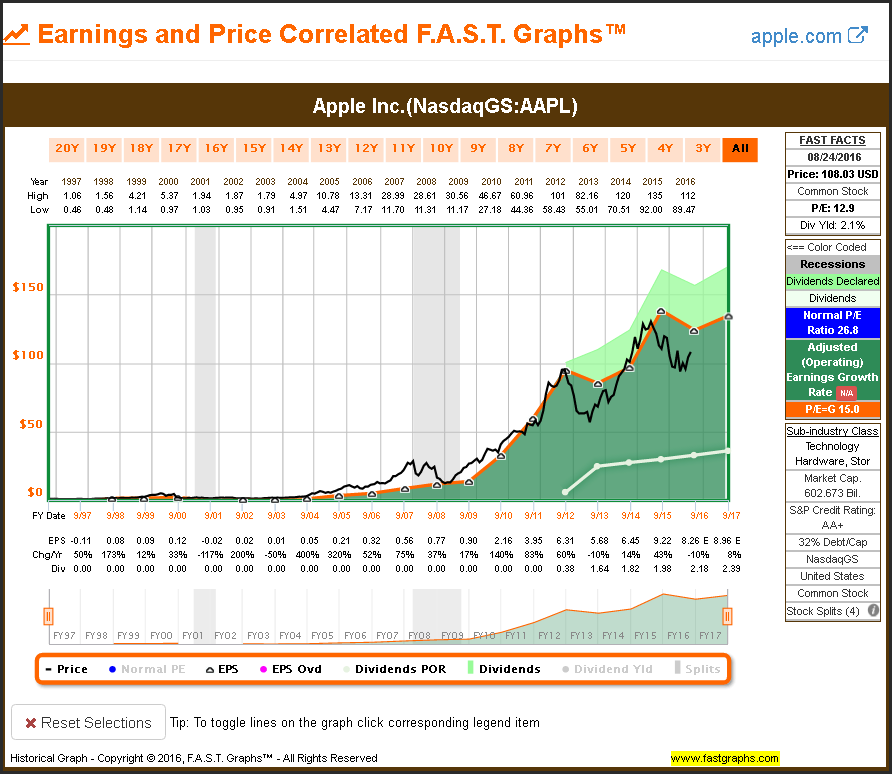

Information Technology – Technology Hardware, Storage

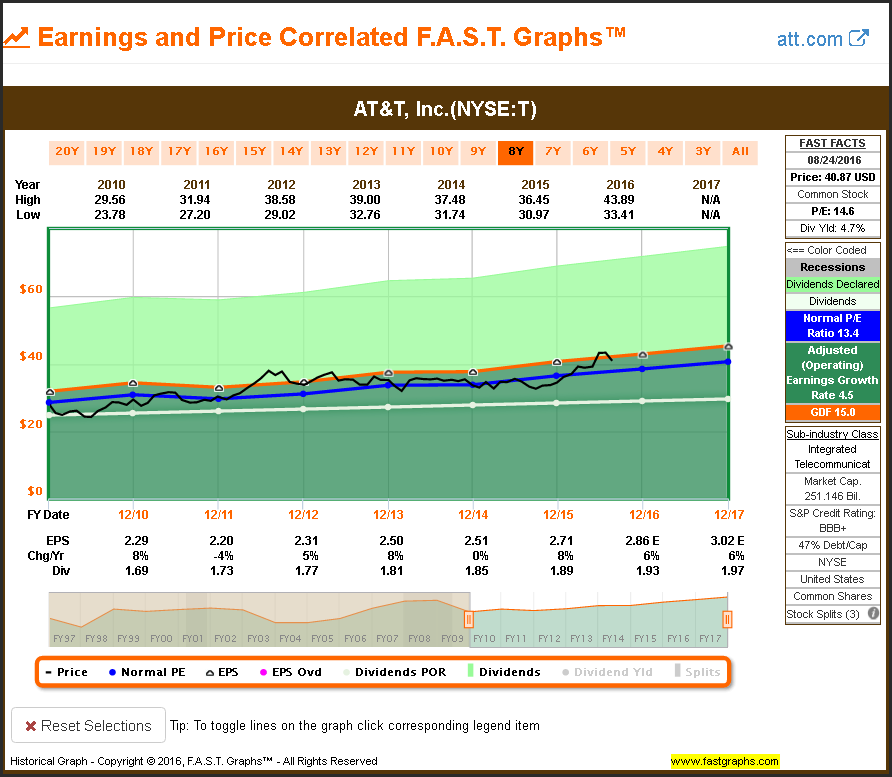

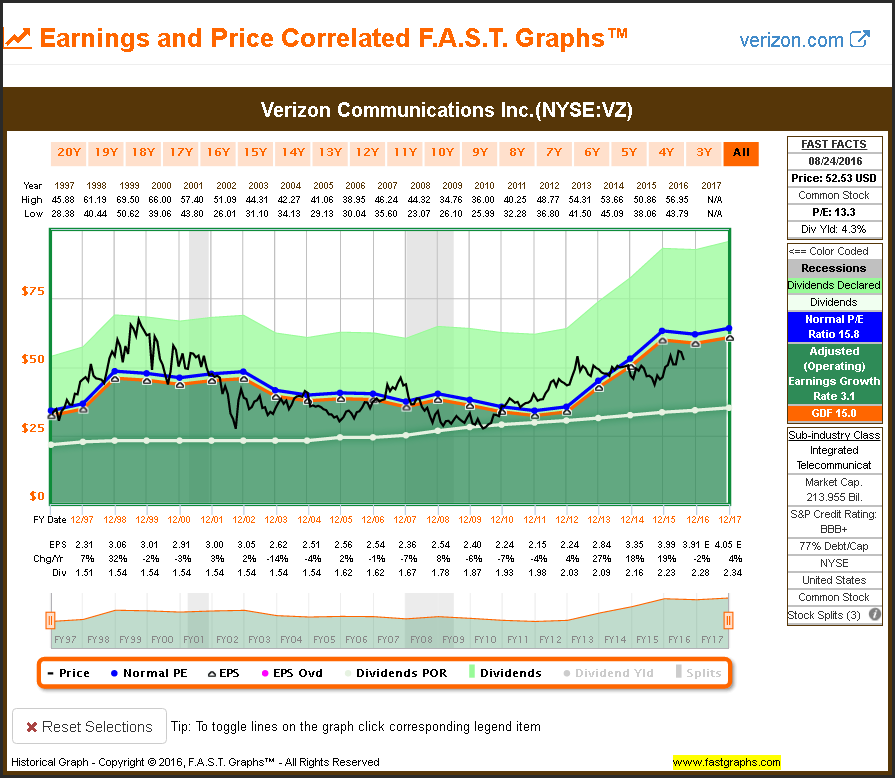

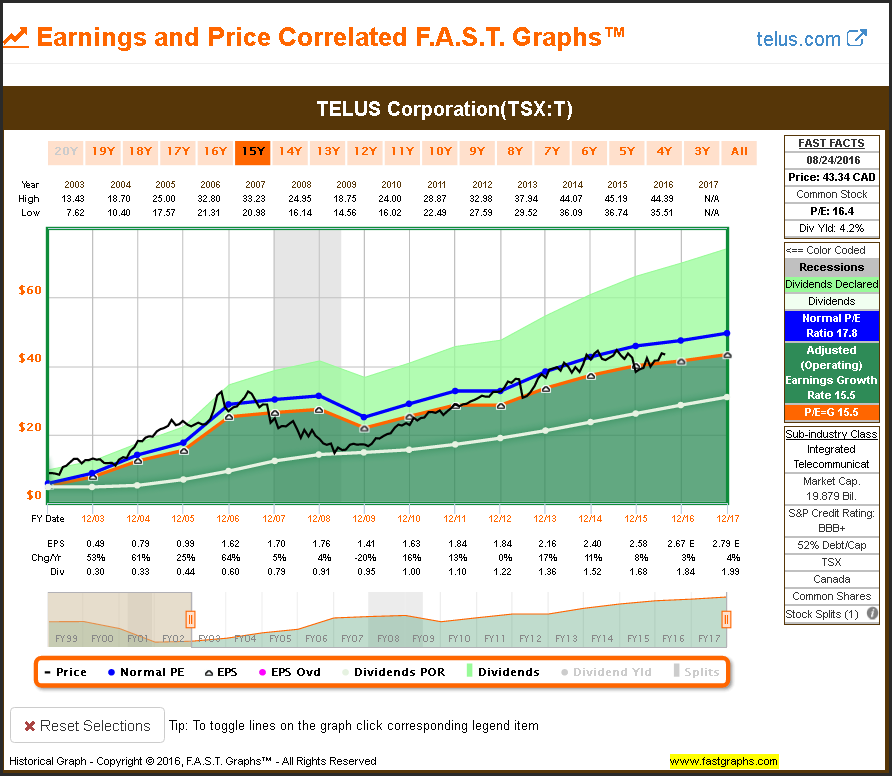

Telecom Services – Integrated Telecommunications

Utilities

As a general statement, the utility sector is highly regulated, and as a result, comprised of companies with low rates of historical earnings and dividend growth. Consequently, I caution readers to be even more fastidious about valuation when looking for investments in the utility sector. Unfortunately, I consider most utility stocks overvalued today. Therefore, I was only able to find one that I was comfortable presenting as a reasonable valuation research candidate.

Utilities – Multi-Utilities

REITs

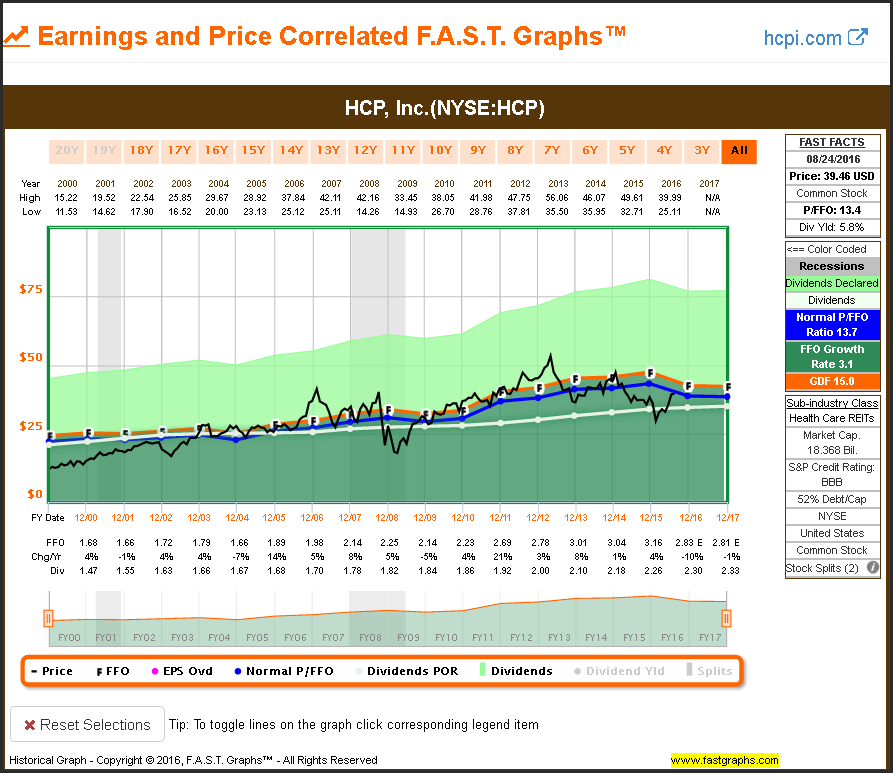

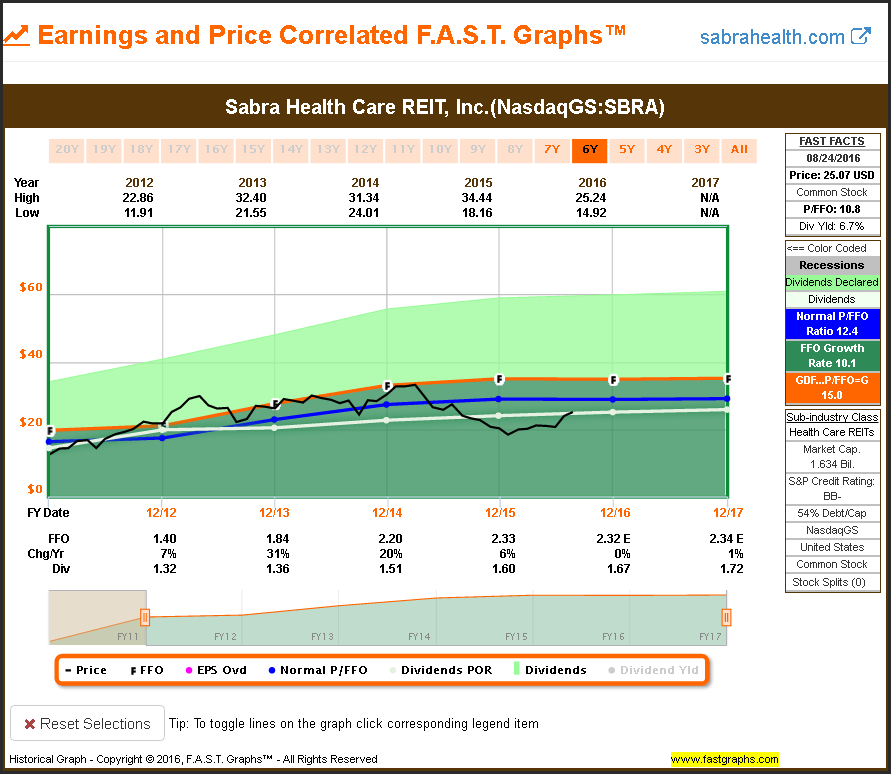

As a general statement, and probably because of their typically higher yields, REITs have been a popular sector for most of 2016. However, one REIT subsector that has not been especially popular has been healthcare REITs. Consequently, most of my REIT selections are comprised of healthcare REITs. However, I did include one relatively new office REIT.

REITs – Healthcare

REITs – Office REITs

Brad Thomas recently covered this office REIT found here.

Summary and Conclusions

The purpose of this article was to take a broad and comprehensive look at the general valuations of dividend growth stocks across all sectors. The conclusion should be obvious, attractively valued high-quality dividend growth stocks are hard to find in today’s long-running bull market. The thirst for yield has driven many dividend growth stocks to historically high valuations.

Importantly, I want to be clear that I am not recommending the numerous dividend paying companies I presented in this article. Instead, my objective was to provide the reader a broad and comprehensive overview of where fair valued dividend growth stocks can be found today. As I previously stated, there are many that I presented that I would not personally choose for my own portfolio. However, I will let the reader decide for themselves if any of these selections appeal to them.

With sound valuation so hard to find in domestic dividend growth stocks today, my next article will look to the north where I will review and present what is often referred to as the big 5 Canadian banks. There are many that believe that the big Canadian banks offer better value than US banks, and I think you will see that valuations are attractive in dividend yields and growth appealing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs™. All rights reserved.