US Worker Productivity In Serious Decline -- The Reasons Why

1. US Worker Productivity Falls Again, Worst Showing Since 1979

2. How Productivity Affects Economy, Incomes & Living Standards

3. Possible Reasons For the Decline in US Worker Productivity

4. The Productivity Conundrum: Could the Data be Wrong?

5. Looks Like I’ll Be a First-Time “Father-In-Law” Next Year

Overview

The Labor Department reported earlier this month that US worker productivity, which measures hourly worker output, declined for the third consecutive quarter at the end of June, the worst showing since the late 1970s. The productivity rate also declined for the 12 months ended June. This news came as a surprise to most forecasters who were sure that the productivity rate would have snapped back strongly in the 2Q.

There is near-universal agreement among economists that worker productivity is the most important determinant in whether our incomes and living standards rise or fall over the years. If productivity continues to fall, the economy will be hamstrung, incomes will stagnate and our living standards will deteriorate in the years ahead.

Interestingly, there is not near-universal agreement on what is causing the current extended period of falling productivity, nor what should be done to reverse this critical trend. Today I will devote this space to explaining why productivity is moving in the wrong direction and what should, and should not, be done about it.

Given the enormous impact productivity has on our economy, our incomes and our living standards, I would hope that more Americans understand this issue better before they head to the polls in what will be the most critical presidential election in many years. Therefore, feel free to forward today’s E-Letter to as many people as you see fit.

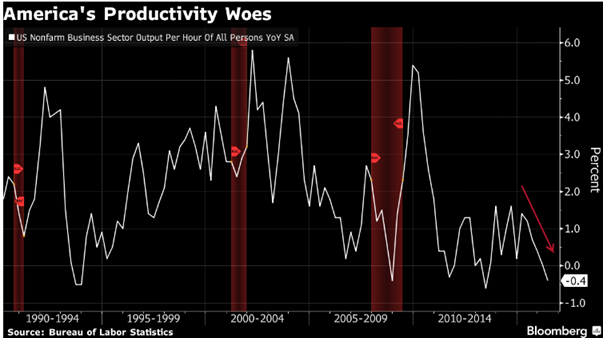

US Worker Productivity Falls Again, Worst Showing Since 1979

US non-farm worker productivity unexpectedly fell in the second quarter, pointing to sustained weakness that could raise concerns about corporate profits and companies’ ability to maintain their recent robust pace of hiring.

The Labor Department said earlier this month that productivity, which measures hourly output per worker, dropped at a 0.5% annual rate in the April-June period. That followed a decline of 0.6% in the 1Q and -1.7% in the 4Q of last year. It was the third consecutive quarterly decline, the longest such stretch of declines since 1979. Over the last 12 months ended June, worker productivity fell 0.4%, the fastest year-over-year pace of decline in three years.

After rising rapidly in the 1990s as computers made workers more efficient, productivity has fallen as companies have been reluctant to invest in new equipment in the past several years, given the outlook for sluggish economic growth globally. Productivity has increased at an annual rate of less than 1.0% in each of the last five years, less than half the historical rate.

The latest government revisions to worker data going back to 2013 also confirmed the softening productivity trend, even though strong employment gains have helped to raise output overall with US payrolls growing by more than 500,000 jobs in June and July combined.

The reason the economy has still been able to expand modestly is because of the strong labor market. Firms are hiring people at a reasonably healthy rate, as evidenced by the very low unemployment rate (4.9%), but most economists say this can’t last because weak productivity signals a further deterioration in corporate profit margins going forward.

The current trend of falling worker output is a serious problem because in the long-run higher incomes and rising living standards depend on rising productivity. So are we destined for lower incomes and falling living standards? Maybe, but there are some outstanding questions. Let’s first take a look at the relationship between worker productivity and incomes and living standards.

How Productivity Affects the Economy, Incomes & Living Standards

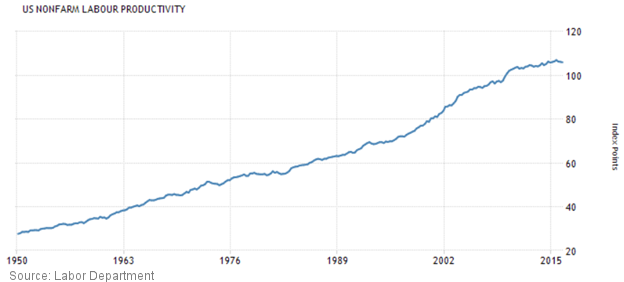

Over the long haul, technological progress raises productivity, which in turn generates higher wages and living standards. The question is, can we continue to increase productivity indefinitely? The answer is YES, assuming that technology continues to advance as it has over the last century or longer.

Productivity, therefore, is really one of the main numbers in the economy that we unambiguously want to be going up. Even if you don’t want people to be consuming so much (inflation fears), you still want this number going up – because it means that people can take more leisure time (vacations, etc.) while still producing the same amount of goods and services.

For many years, economy-wide productivity growth and wage growth have tended to have a one-to-one relationship. When productivity rose rapidly, as it did in the period from 1945 to 1973, wages also rose rapidly. When productivity growth flattened out, as it did between 1973 and 1995, wage growth also stagnated.

Yet in the US over the past 20 years, the tight relationship between productivity growth and wage growth has broken down. Wage growth has fallen behind productivity growth. Economists debate why this breakdown has happened, and how long the situation might last.

Some point to the rising cost of non-wage benefits, such as health insurance, which employers have increasingly provided to their workers in recent decades. Others point to the fact that we’ve had two severe recessions since 2000 as the reason for sluggish wage growth.

But none deny that, over the long-term, a healthy rate of productivity growth is a requirement for a further rise in living standards. Or that an anemic rate of productivity growth is a recipe for stagnation and class conflict.

For example, between 1947 and 1973, output per hour (the standard measure of labor productivity) rose at an annual rate of about 3%. Then, between 1974 and 1995, the rate of productivity growth fell by half, to 1.5%. Not coincidentally, this was the period when wage growth started to stagnate.

Things started to improve after 1995. For a decade or so, perhaps owing to the development of the Internet, the rate of productivity growth returned to about 3%, and wages started to rise again. Optimists predicted a bright future – one that unfortunately didn’t materialize.

Possible Reasons For the Decline in US Worker Productivity

Since 2007, the annual rate of productivity growth has averaged only about 1.3%. Since 2010, it has been even lower, at about 0.5%. According to the latest figures, in the twelve months that ended in June, the growth rate of output per hour was negative 0.4%. So what could be the causes of this serious trend?

Before we get to that, I should mention that the decline in worker productivity hasn’t been restricted to the United States. Something similar has happened in countries like Japan, Germany, France and the United Kingdom. Whatever is driving the slowdown in productivity growth, it appears to be affecting the advanced world as a whole.

One likely explanation for the global decline in productivity is the decline in business investment spending (capital expenditures) on such things as plants, equipment, tooling, hardware, software and other technology. Since the Great Recession, many businesses have been scrimping on capital investments, preferring to hoard cash or spend it on stock buybacks.

There is a growing theory that as long as the Fed and other central banks around the world hold interest rates to near zero – or even negative rates in many cases – business investment spending that emboldens productivity will remain hobbled. Many business leaders believe that the continuation of ZIRP (zero interest rate policy) means that the economy will remain weak.

Another serious issue is that many corporations aren’t seeing enough demand for their products to justify large new investments. And even when they do see an uptick in demand, they tend to hire new workers but have them make do with existing equipment. So employment growth looks healthy, but the economy remains stuck in a low-growth, low-investment, low-productivity trap.

Another possible explanation is that technological advancements over the past couple of decades have not had the impact of previous innovations. Robert Gordon, an economist at Northwestern University and author of “The Rise and Fall of American Growth,” argues that technological breakthroughs like the Internet and “smartphones” – while marvelous products of human ingenuity – simply don’t match up to previous technological innovations such as indoor plumbing, the internal-combustion engine, electrification, jetliners, etc.

If Gordon is right, sagging productivity figures simply reflect the fact that scientific progress doesn’t have as much impact on the economy as it once did. Rather than waiting for productivity growth and wages to rebound on their own accord, Gordon supports policies designed to expand the size and quality of the labor force, such as raising the retirement age, letting more immigrants into the country and expanding access to higher education. That’s a debate I’ll save for another time.

Another possibility is the accelerating exit of the Baby Boomers from the workforce. Boomers are turning 65 at the rate of 10,000 a day, and the vast majority of them are choosing to retire at age 65 or thereabouts, thus taking a huge amount of talent out of the economy.

Recent studies have shown that the Boomers’ exit takes a double toll on productivity. In the first case, the company and the economy are losing the retiring individual permanently. This is often a seasoned employee (often a manager) with a tremendous amount of technical, practical, industry, and institutional knowledge.

The second of the two hits in productivity has to do with employees working with or around the Boomer who is retiring. Studies have shown that when a seasoned performer leaves, his or her coworkers’ productivity goes down as well – since that person isn’t there sharing all that knowledge and experience.

The Productivity Conundrum: Could the Data be Wrong?

Since the end of the Great Recession in early 2009, we have seen an unprecedented bull market in stocks, and the bull market in bonds has exceeded all expectations as a result of the Fed’s controversial activist monetary policy.

Likewise, we have seen steady growth in the economy even though the recovery has been the slowest since 1949. Despite the slow growth, this has been one of the longest economic expansions on record.

It is not surprising then that there has been increasing skepticism of the Labor Department’s methodology in measuring worker productivity. In recent years as productivity has declined, we have seen mounting criticism that the government’s calculation methods are too antiquated to keep up with today’s hyper-connected economy, in which new goods and services are introduced at a breakneck pace.

The Labor Department has admitted that it is struggling to adapt its various economic gauges to today’s warp-speed environment where so much business is conducted on the Internet, without “paper” reporting in many cases.

This has led some analysts to assume that the Labor Department’s figures on worker productivity are fatally flawed. Some have even suggested that productivity could actually be rising in recent quarters. In my opinion, this is clear speculation.

While the government data is far from perfect, and needs improvement to keep pace with today’s Internet economy, worker productivity and business investment spending are both trending lower. This critical trend must be reversed if we want to see incomes and living standards improve.

In regard to these two issues, we have a clear choice in the November election. One candidate is for bigger government, higher taxes and more regulation. These policies would do nothing to help productivity and will likely make it even worse.

The other candidate is for limited government, less regulation and lower taxes. This candidate vows to cut the corporate tax rate from 35% (the highest in the developed world) to 15%. He proposes lowering the corporate tax rate for profits held outside the US to 10% for a time. This would almost certainly lead to some $2-$3 trillion of offshore profits returning to the US very quickly.

These two proposals alone could quickly increase business investment spending and therefore worker productivity significantly. The economy could rebound measurably in a fairly short time.

Personally, I don’t like either of the candidates we are being forced to choose between. We don’t have any reason to trust either one of them, especially Hillary.

For me, I would much rather have a non-politician businessman in the White House, despite all his baggage, than Hillary who will give us higher taxes, much more regulations and an even weaker economy.

But as usual, I’m probably preaching to the choir.

Looks Like I’ll Be a First-Time “Father-In-Law” Next Year

Over the weekend, our son (our oldest child – 26) got engaged to his sweetheart of the last couple of years. They plan to be married early next May. They were in town this past weekend to look at wedding venues on beautiful Lake Travis where we live near Austin.

Our son is an engineer and works for a multinational defense contractor in its Dallas/Ft. Worth complex. He works on things for the government that he can’t tell us about due to the high security involved. His wife-to-be is also an engineer and works at a different large company in Dallas.

Debi and I are very excited about this latest development. Both our son and his fiancé are devoted Christians, and we welcome her into our family. Now it’s on to planning a wedding, and a LOT has changed since Debi and I married 30 years ago.

Our daughter (age 24) is not married yet. When that day comes, I know it will be harder to give my baby girl away. But I have faith I will be able to handle it.

It seems like it was just yesterday when I was teaching our kids to water ski and drive the boat on the lake. Time flies…

All the best,

Gary D. Halbert

|

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent. |