Premier Dividend Growth Stocks: Is There Any Value? A Sector By Sector Summary Review: Part 1

Introduction

As a value investor, I must admit to being very frustrated with the valuations I’m seeing on high-quality blue-chip dividend growth stocks. I have been vigorously searching for fairly valued dividend growth stocks to invest in. I have thoroughly screened and evaluated every company in the S&P Dividend Aristocrats, all three of the CCC (Champions, Contenders and Challengers) lists produced by David Fish, every dividend paying stock on the S&P 500, Fortune 500, NASDAQ 100, S&P 100 Large-cap, Dow Jones Industrial Average, and even the S&P 400 mid-cap universe.

Much to my chagrin, I have found the pickings to be quite slim indeed. It seems rather obvious to me that low interest rates and a large appetite for yield in an environment where fixed income yield is low, has driven valuations of high-quality blue-chip dividend growth stocks to unprecedented levels of high valuation. Consequently, the vast majority of my favorite and preferred dividend growth stocks are beyond a level of valuation that I would be comfortable investing at. In short, and in my opinion, this is a tough market for the value focused dividend growth investor.

On the other hand, I am on record many times of stating that it is a market of stocks and not a stock market. More recently, I have also added the idea that it is also a market of sectors. What these statements imply is that regardless of the level of the overall market, there will always be value to be found. Naturally, it’s easier to find value in a bear market than it is in a raging bull market like we have had for the past several years. As it relates to my market of sectors statement, this implies that various sectors of the market can be valued quite differently than the overall market at large.

From the perspective of diversification, this can be problematic, because if there are only a few sectors where attractive valuation can be found, it then becomes quite difficult to construct a properly diversified dividend growth stock portfolio. As I’ve been searching through the lists referenced above, most of the good valuations I have seen have been limited to only a few sectors. Moreover, some of those sectors, the energy sector for example, are rife with problems and challenges. Consequently, many blue-chip energy related companies such as Chevron and Exxon are trading at or near low historical prices. However, their current valuations (P/E ratios) are very high because earnings have fallen precipitously. Lower stock prices in the energy sector come with higher levels of risk today. When looking for attractive valuation, it is typically found in unpopular companies and/or sectors.

In other words, there is almost always a reason behind attractive valuations. Sometimes the reasons are valid and real, sometimes they are exaggerated, and sometimes they are completely unfounded. The trick is to understand and evaluate the reasons in order to determine if they are systemic or isolated, temporary or permanent, real or unreal. This is not always easy to do, and in my opinion, can only be done through comprehensive research and due diligence.

In order to keep this article of reasonable length, I offer the following fair valuation sector by sector review of the 50 constituents in the S&P 500 Dividend Aristocrats. For each of the nine major sectors comprising the S&P Dividend Aristocrats, I will provide, where possible, an earnings and price correlated F.A.S.T. Graphs™ example of a fairly valued and overvalued company in each sector. Additionally, I will add brief commentary regarding the relative valuation levels of the overall sector.

The key to gaining the maximum benefit and insight from these earnings and price correlated graphs is to recognize that the orange line on the graph is offered as a fair valuation reference line. Moreover, it’s also important to recognize that the P/E ratio of the orange line is the same all the way across the graph. The actual P/E multiple is listed in the orange rectangle in the FAST FACTS color-coded boxes to the right of each graph.

Once you are fully conscious of the P/E ratio multiple of the orange line, the next thing to key in on is how the price (the black line on the graph) tracks the orange line over the long-term historical period of time. Finally, when examining the overvalued examples, notice how the black price line has significantly deviated from the orange line and risen significantly above it in recent times. Additionally, notice how the black price line has moved back to the orange line, or is in the process of moving back to it, and in some cases below it, when examining the fairly valued examples.

The Consumer Discretionary Sector

There are only six consumer discretionary companies in the S&P Dividend Aristocrats. Unfortunately, I would consider five of the six too overvalued to invest in as evidenced by the following earnings and price correlated F.A.S.T. Graphs™ on Genuine Parts Company.

Genuine Parts Company (GPC)

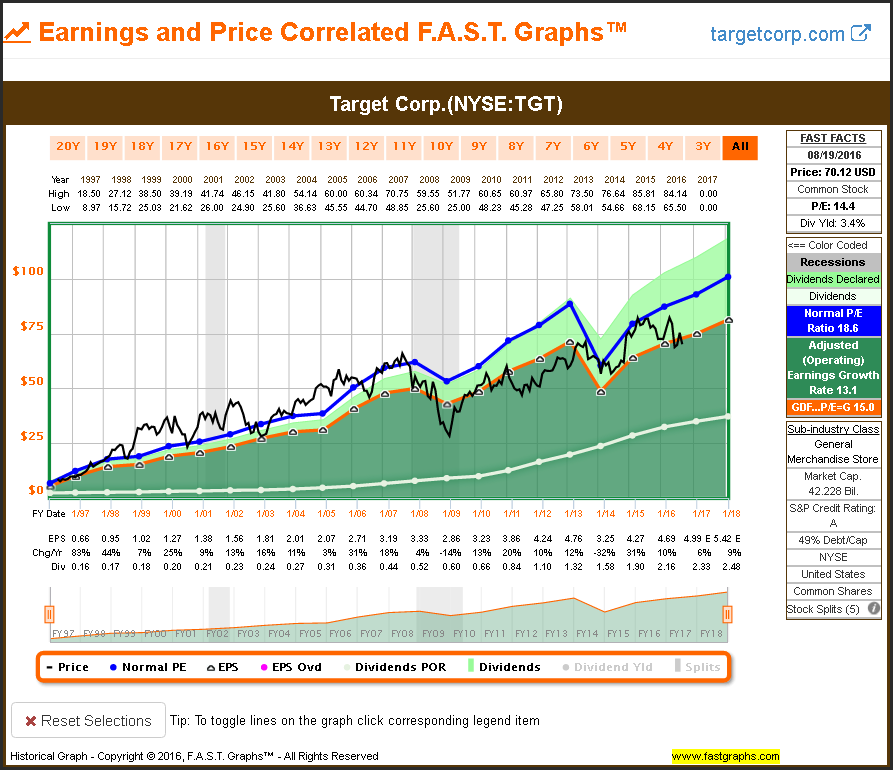

The only consumer discretionary company in the Dividend Aristocrats that I consider reasonably attractive is Target. However, I question whether or not it belongs in the consumer discretionary sector considering that Wal-Mart is considered a consumer staples company. Nevertheless, notice how the price is currently related to the orange valuation reference line indicating fair value.

Target Corp (TGT)

The Consumer Staples Sector

There are only 13 consumer staples sector companies in the S&P Dividend Aristocrats. However, I consider all of them too overvalued to invest in currently. Brown-Forman Corporation represents a classic example. Low interest rates have driven the valuation of this company significantly above historical norms, and also notice that this has been occurring for a long period of time.

Brown-Forman Corporation (BF.B)

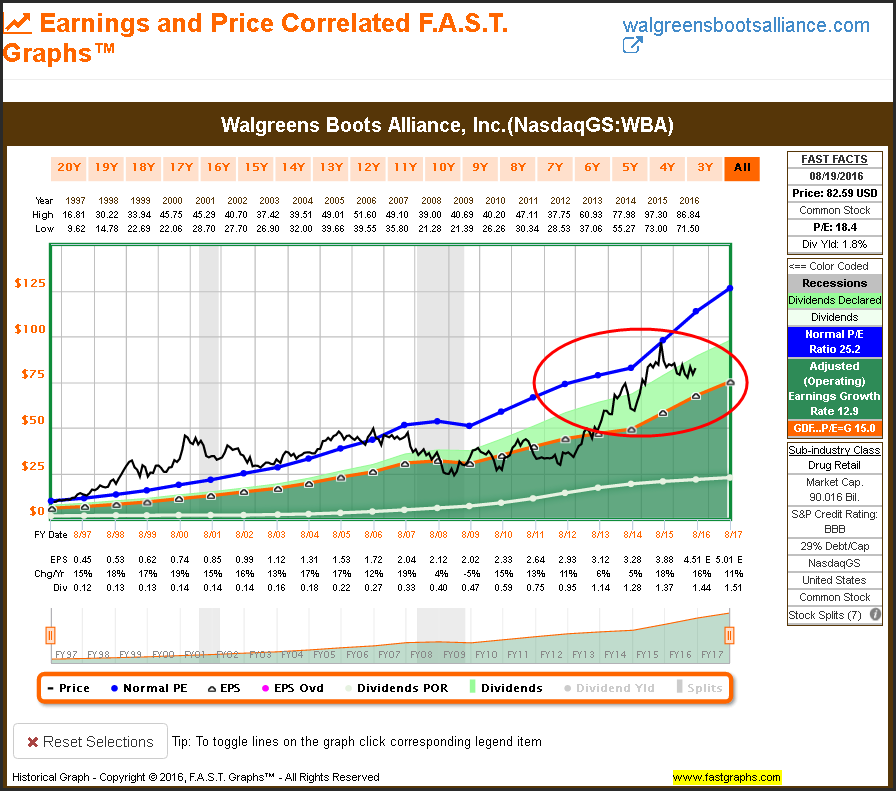

I also consider Walgreens Boots Alliance overvalued at this time. However, this company has been gradually moving towards fair value since the summer of 2015. When, and if, the price gets down to below the orange line, I would consider this an attractive investment opportunity for the dividend growth investor. But personally, I would not invest in Walgreens Boots Alliance until valuation appears more attractive.

Walgreens Boots Alliance Inc (WBA)

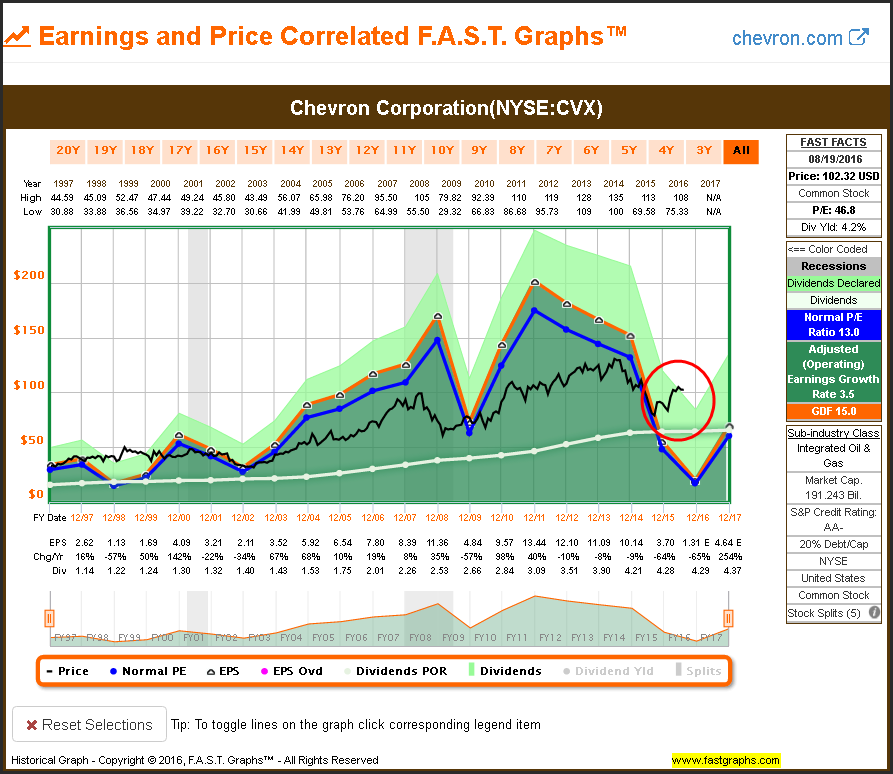

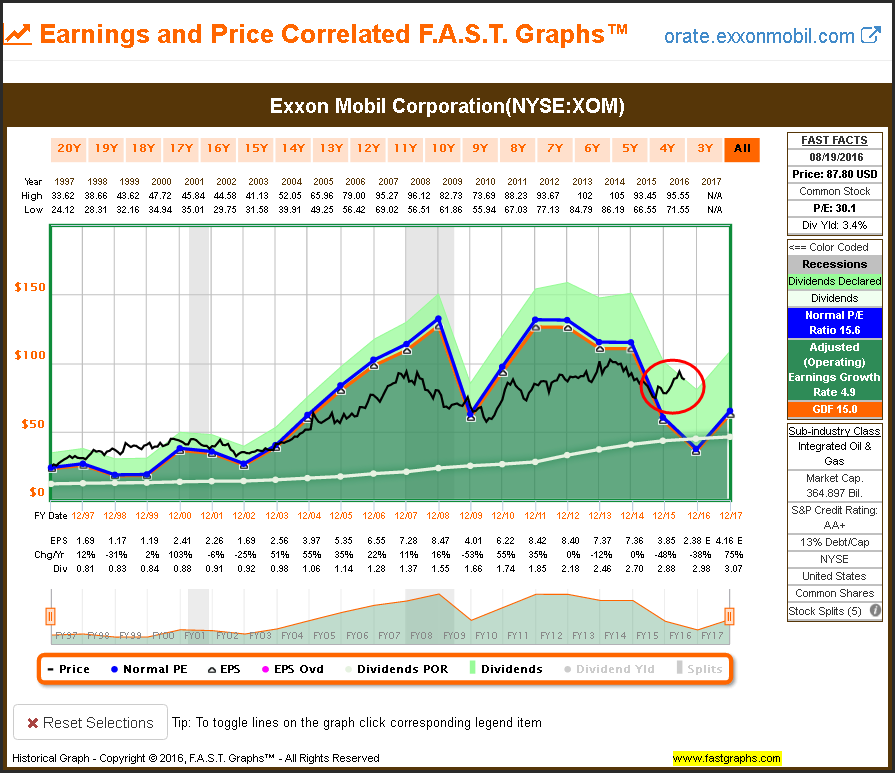

There are only two energy sector companies in the S&P Dividend Aristocrats - Exxon Mobil Corporation and Chevron Corporation. However, they are easily considered the premier energy companies in the world. Current P/E ratios are extremely high because earnings have been in a freefall as the price of oil has collapsed. The real question here is what the future valuations look like based on forward earnings if and when energy prices recover.

Chevron Corporation (CVX)

Exxon Mobil Corporation (XOM)

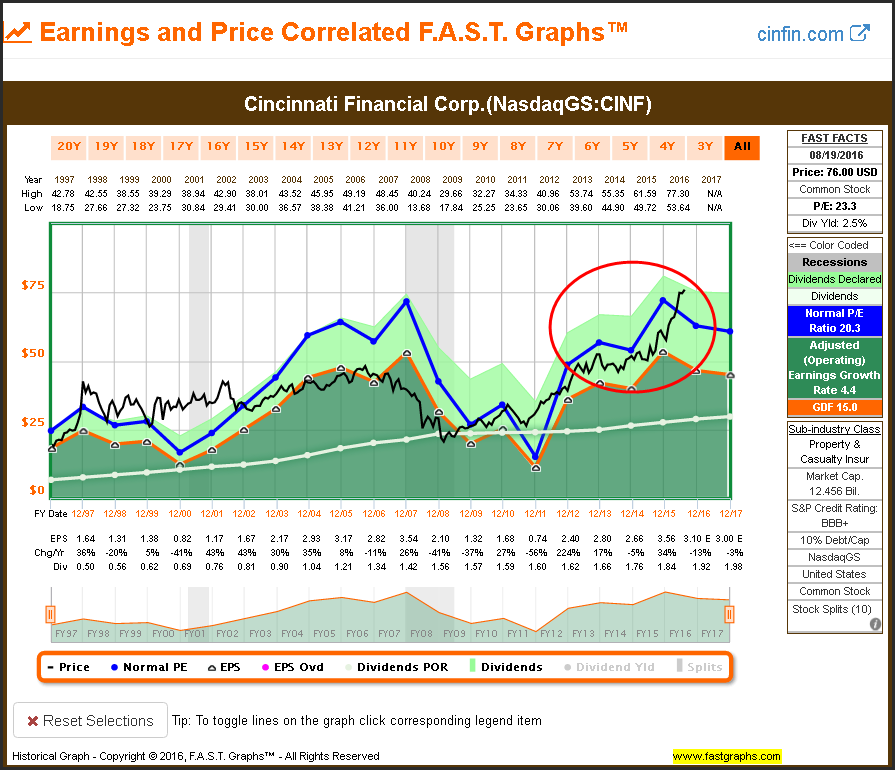

There are only five financials sector companies in the S&P Dividend Aristocrats. However, with the exception of Cincinnati Financial Corp, I consider all of the other five attractively valued. Further note the cyclical historical earnings record of Cincinnati Financial Corp in spite of the fact that their dividend has increased steadily over time. The financial sector is one sector where reasonable or attractive valuations can be found today.

Cincinnati Financial Corp (CINF)

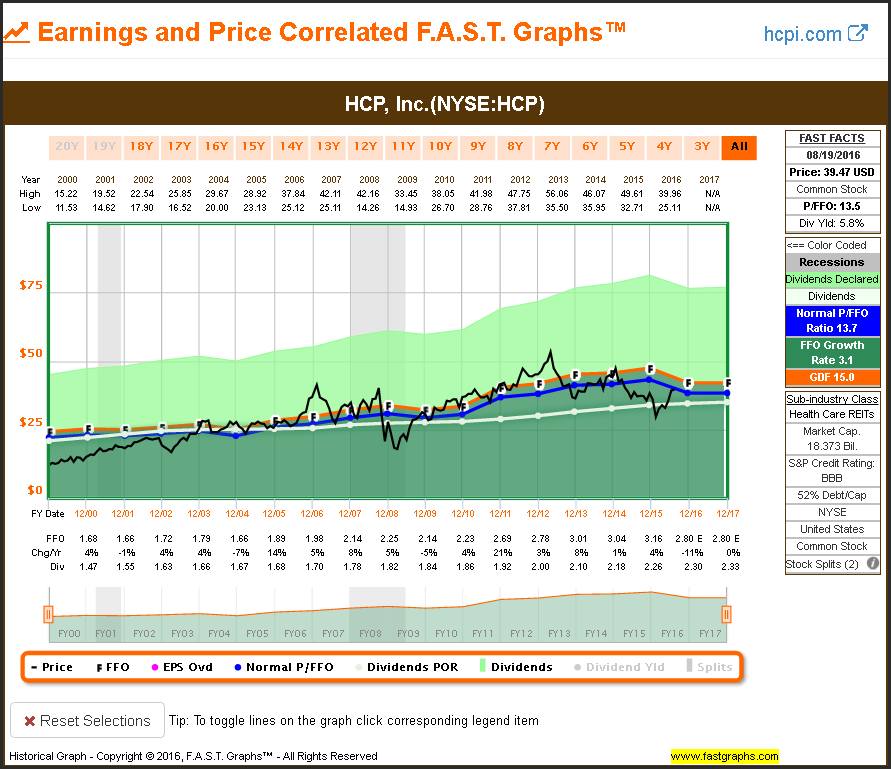

HCP Inc is a healthcare REIT that appears attractively valued on a price to FFO basis. However, FFO is expected to be down 11% this year. As previously stated, attractive valuation is often associated with a reason, especially in an inflated market environment like we have today. I also found it interesting that the price has recovered strongly in 2016 after falling precipitously for most of 2015.

HCP Inc (HCP)

There are only seven healthcare sector companies in the S&P Dividend Aristocrats. There are two Dividend Aristocrats in this sector that I consider attractive or fairly valued. Cardinal Health Inc is one, and the other is AbbVie, Inc. However, AbbVie was created as a result of the spinoff or split-up of Abbott Laboratories. Consequently, I consider it a stretch to be included in the Dividend Aristocrats because its dividend history as an independent company is quite short.

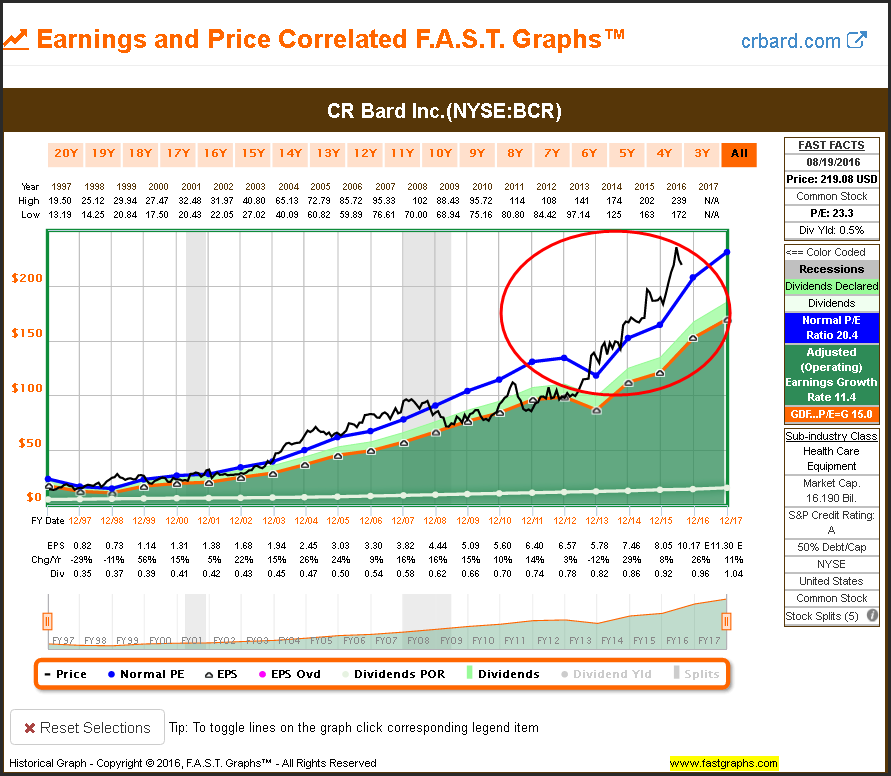

CR Bard Inc represents another classic example of how overvalued the other healthcare companies and the Dividend Aristocrats are. Although this company has historically commanded a premium valuation as illustrated by the dark blue normal P/E ratio of 20.4, its stock price has recently risen above even that high standard.

CR Bard Inc (BCR)

Cardinal Health represents an example of an overvalued healthcare sector Dividend Aristocrat that has recently moved back into fair value territory.

Cardinal Health Inc (CAH)

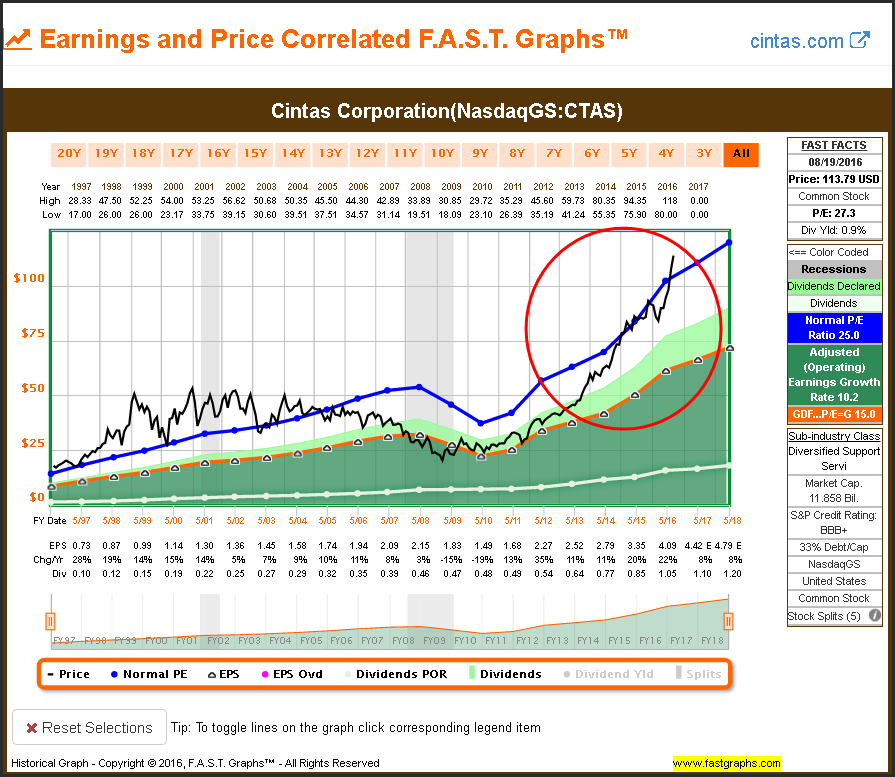

There are only eight industrial sector companies in the S&P Dividend Aristocrats and I consider all of them overvalued. Cintas Corporation represents a classic example of how overvalued the companies in this sector are. What I consider truly enlightening about this example is how significant overvaluation from 1999 into the Great Recession led to extremely poor price performance in spite of good earnings growth and a rising dividend. The average total annual rate of return over this timeframe was a -5.3%. I think it should be clear that overvaluation and not poor business performance was the culprit.

Cintas Corporation (CTAS)

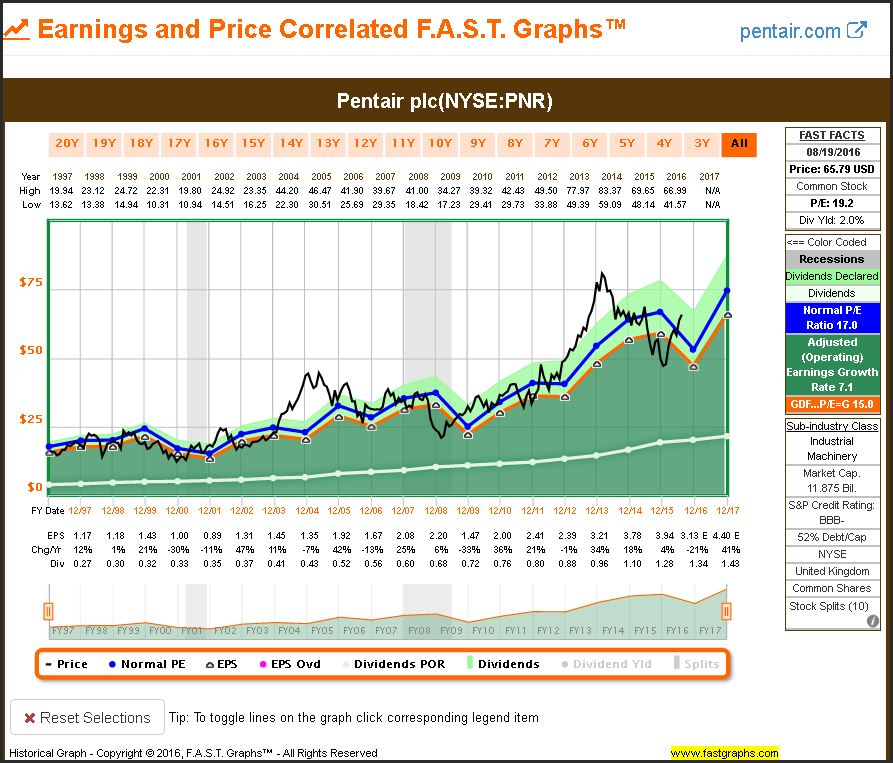

Pentair presents the only Dividend Aristocrat in the industrial sector that is even close to a reasonable valuation today. However, I do consider it overvalued on a current earnings basis, but perhaps less so on forward earnings estimates.

Pentair plc (PNR)

There is only one information technology sector company in the S&P Dividend Aristocrats. Automatic Data Processing Inc represents a classic example of a company that the market has historically placed a premium valuation on. However, if you are comfortable paying a premium valuation for this company, then its current valuation is only modestly above historical norms.

Automatic Data Processing Inc (ADP)

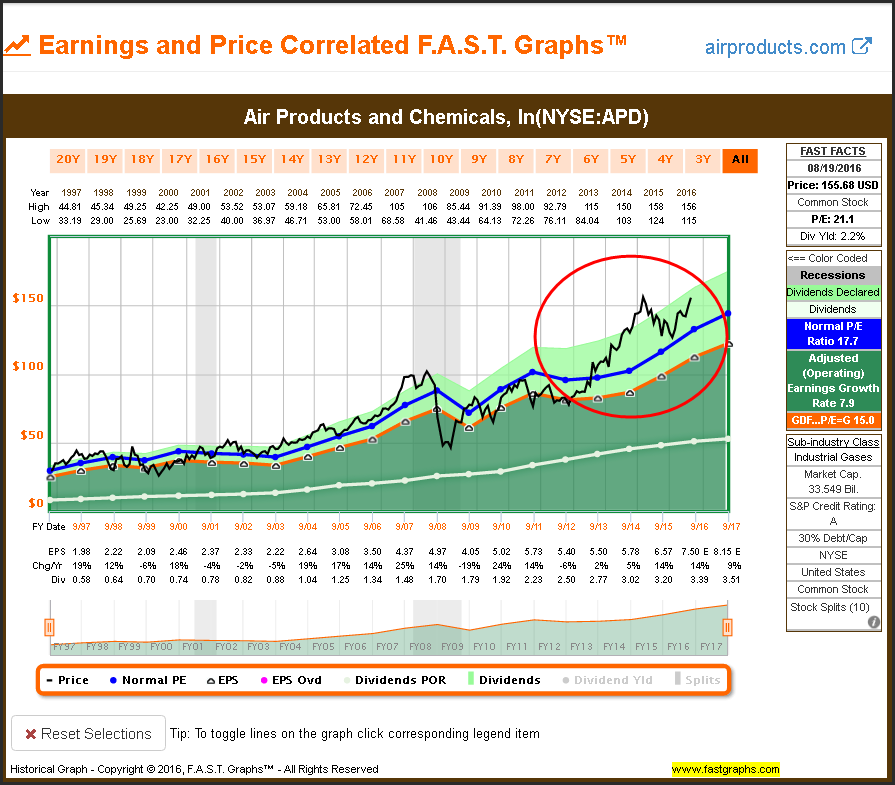

There are five materials sector companies in the S&P Dividend Aristocrats. I consider all of them currently overvalued as evidenced by the Air Products and Chemicals earnings and price correlated graph below.

Air Products and Chemicals (APD)

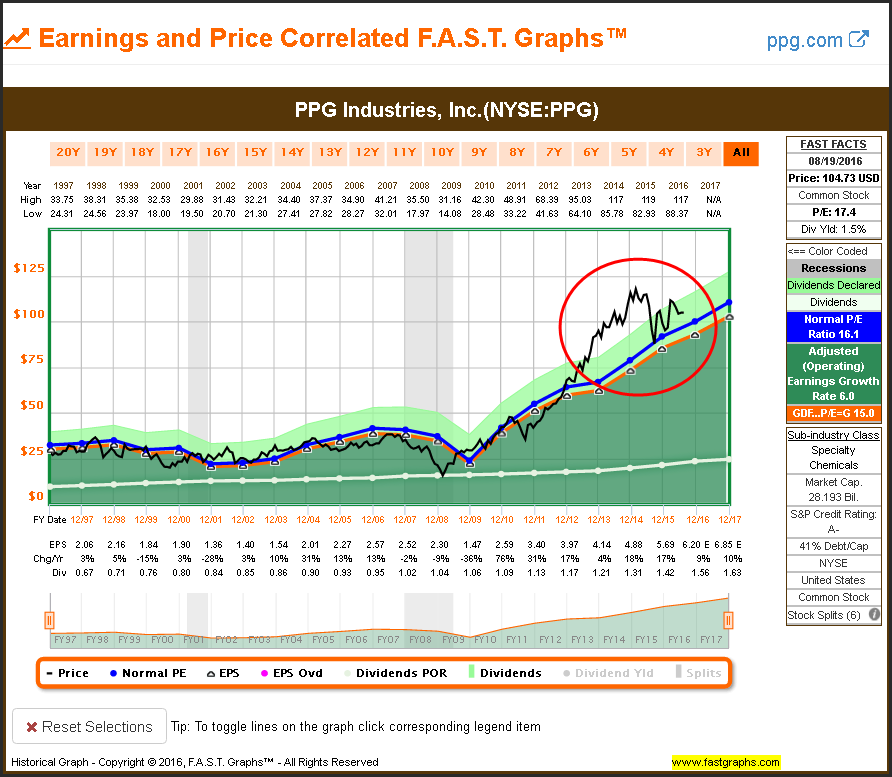

PPG Industries Inc looks moderately overvalued on a long-term historical basis. However, the company is currently off of its previous overvalued highs. Additionally, note the acceleration of earnings growth post the Great Recession.

PPG Industries Inc (PPG)

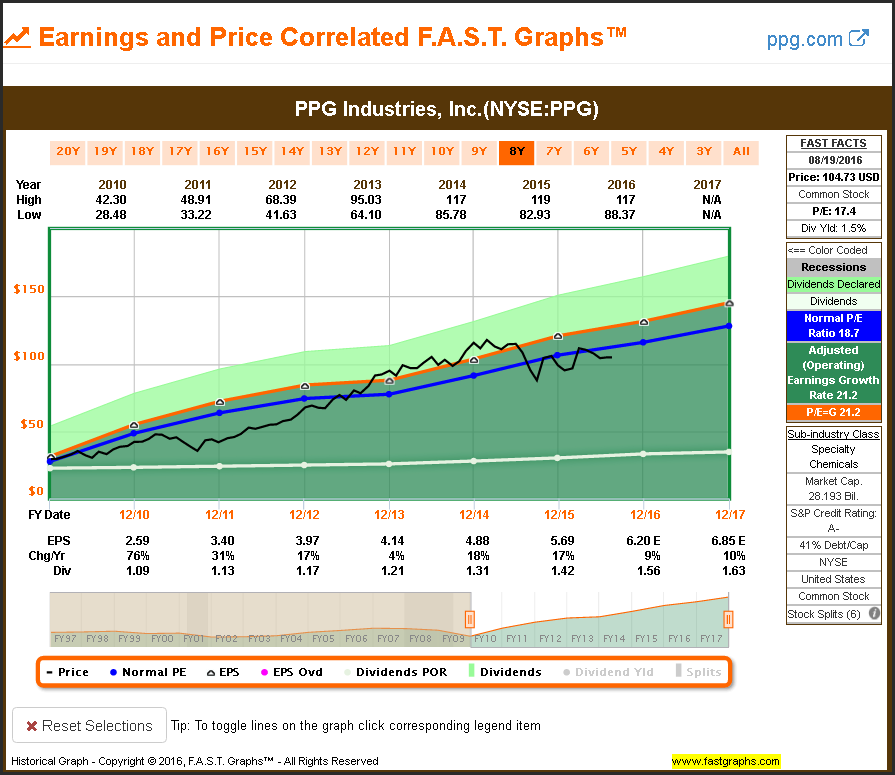

I have added a second shorter term graph on PPG Industries Inc that suggests that this company might be undervalued based on recent earnings growth. However, the question is whether or not this accelerated growth is sustainable long-term or not?

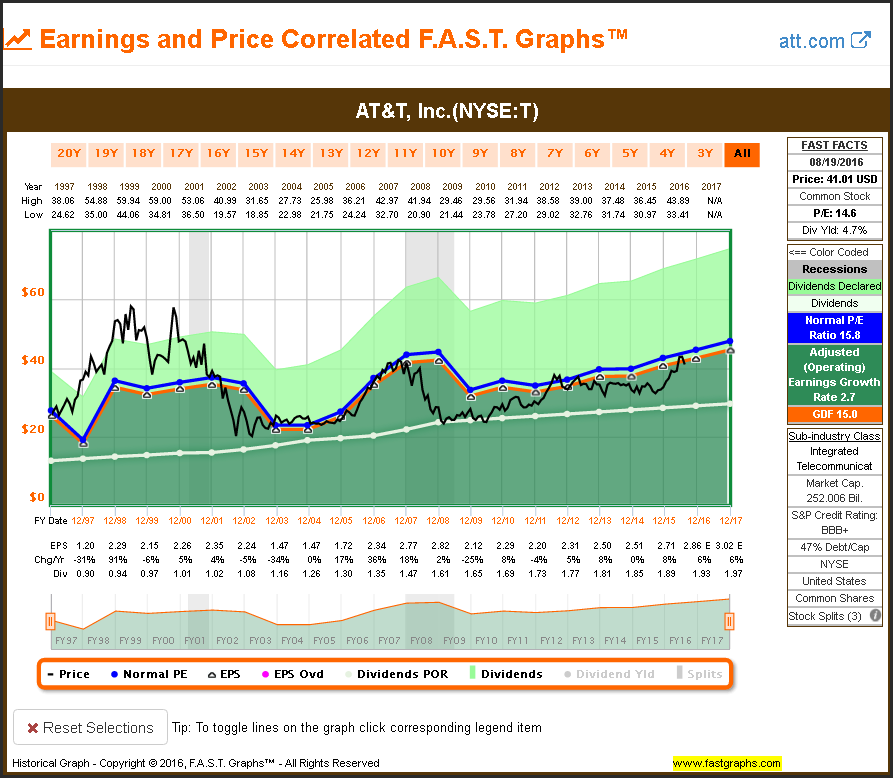

There is only one company in the telecom services sector in the S&P Dividend Aristocrats. AT&T Inc appears attractively valued today and offers an above-average current dividend yield. However, this company’s valuation was much more attractive last year than it is today.

AT&T Inc (T)

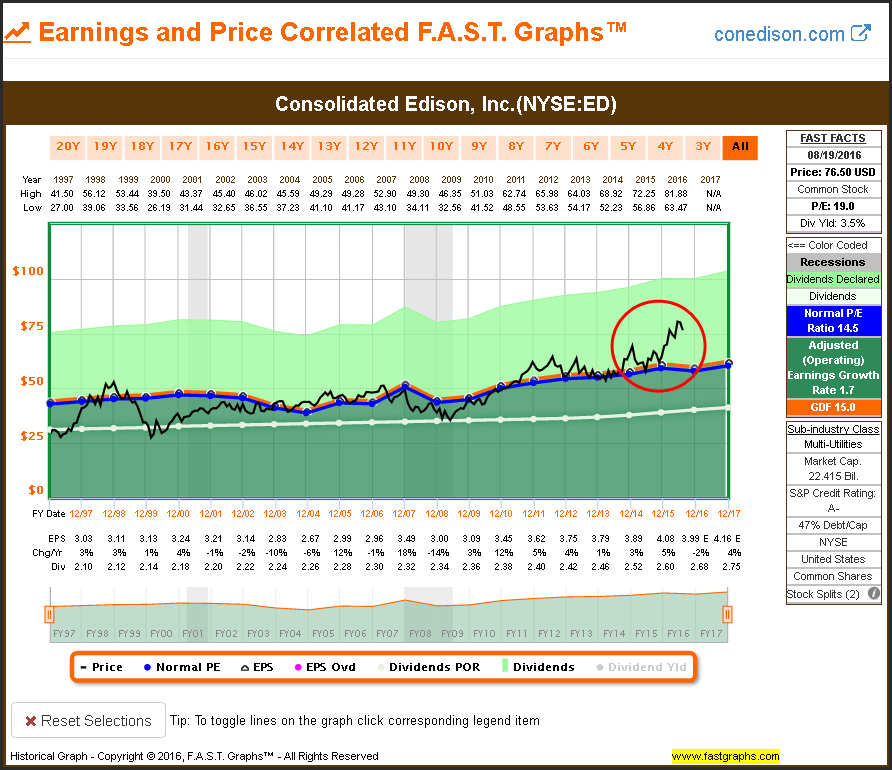

There is only one company in the utilities sector in the S&P Dividend Aristocrats. However, as a general statement, most utilities have become significantly overvalued in 2016 relative to their rather low or subdued earnings growth potential. Consolidated Edison represents a classic example of utility stocks being currently overvalued.

Consolidated Edison (ED)

Putting Fair Valuation Into Perspective

Fair valuation and its importance is a concept that I have written about extensively. However, it is also the concept that I believe is often misunderstood. If you spend some time examining the examples presented in this article, you will note many cases where overvalued stocks continue to advance in spite of high valuations. Low interest rate levels over the past several years have contributed to this chronic overvaluation.

Therefore, it should be understood that high valuation does not necessarily indicate a losing investment. However, I do contend that paying a high valuation will always indicate taking on a greater level of risk for the returns that a stock will give you over the long term. Sometimes it works out well over the intermediate or short-term. However, if you’re a long-term investor, I contend that investing when valuations are too high will lead to returns that are lower than the risk you are assuming to earn them. I wrote extensively about this in a recent article titled “Get Higher Returns and More Dividend Income – in Less Time with Less Risk.”

Summary and Conclusions

With this article I have surveyed the relatively small universe of S&P Dividend Aristocrats in order to illustrate the overvaluation conundrum that exists with premier dividend growth stocks today. In today’s low interest rate environment, the quest for yield has clearly attracted a lot of money into high-quality dividend growth stocks. The Dividend Aristocrats are clearly the crème de la crème of dividend growth stocks. However, as I have illustrated with this article, finding attractive valuation in these premier dividend growth stocks is very rare today.

In part 2, I will broaden my scope into a larger universe looking for value in dividend growth stocks. My primary emphasis will be revealing the specific sectors where attractive valuations do exist in today’s inflated market.

Disclosure: Long ED,T,GPC,TGT,CVX,XOM,HCP

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.