Introduction

In today’s frothy stock market, finding value in dividend growth stocks is hard to do. Unfortunately, most of the premier dividend growth stocks such as those found on David Fish’s CCC lists of Dividend Champions, Contenders and Challengers are currently overvalued. Dividend Champions have raised their dividends for 25 or more straight years, Dividend Contenders have raised their dividends for 10 to 24 straight years, and Dividend Challengers for 5 to 9 straight years.

However, not every stock on these prestigious lists are above a sound or attractive buy range. But considering the overall high valuation of the market, there is usually a reason or reasons why a specific stock might be going against the grain. The specific company could be experiencing some problems, the industry it operates in could be going out-of-favor or the company’s stock price is simply experiencing a rational reversion to the mean are typically the primary reasons. The trick is to find and identify a great business that is soundly valued based on solid fundamentals.

The dividend growth stock I am featuring in this article is the Kroger Company (KR) which is the second-largest grocery store in the country. The reason it is currently attractive is because it has reverted to the mean of fair value from being overvalued for all of 2015 and most of this year. This is my favorite kind of fair valuation find, because I consider the company strong and healthy on a fundamental basis. Consequently, the only reason that I can see for its stock being weak recently is simply because it was previously overvalued based on fundamentals.

Kroger is a Dividend Contender that paid its first dividend in 2007 and has increased it ever since (11 consecutive years) at an average dividend growth rate of 13.2% per annum. Although the current yield is not that high, the earnings growth and dividend growth past, present and future is expected to be higher than average. Therefore, I offer this to the dividend growth investor looking for total return and above-average future dividend growth.

The Kroger Company

Here is a brief description taken directly from the company’s website:

“CORPORATE OVERVIEW OPERATIONS Headquartered in Cincinnati, Ohio, The Kroger Co. is one of the largest retailers in the United States based on annual sales, holding the #20 ranking on the Fortune 100 list published in June 2015. Kroger® was founded in 1883 and incorporated in 1902.

At the end of fiscal 2015, Kroger operated (either directly or through its subsidiaries) 2,778 supermarkets, 1,387 of which had fuel centers. Approximately 42% of these supermarkets were operated in Company-owned facilities, including some Company owned buildings on leased land.

In addition to supermarkets, Kroger operates (by franchisees or through its subsidiaries) 784 convenience stores, 323 fine jewelry stores and an online retailer. Subsidiaries operated 711 of the convenience stores, while 73 were operated by franchisees through franchise agreements. Approximately 54% of the convenience stores operated by subsidiaries were operated in Company-owned facilities.

The Company also manufactures some of the food for sale in its supermarkets. As of February 1, 2015, the Company operated 38 food production plants. All of the Company’s operations are domestic.”

Although most of Kroger’s growth has been generated internally based on its superior competitive advantages that include regional scale and densely cluttered store locations, the company has recently made a strategic acquisition/merger which stands to expand their geographical reach and future profitability:

“Press Release

Kroger and Roundy's Announce Definitive Merger Agreement

Kroger to Add Complementary Footprint of 151 Stores, Including New Wisconsin Geography and 34 Mariano's Locations in Chicago

Roundy's Shareholders to Receive $3.60 Per Share in Cash; Transaction Valued at Approximately $800 Million Including Debt

Company Release - 11/11/2015 8:31 AM ET

CINCINNATI and MILWAUKEE, Nov. 11, 2015 /PRNewswire/ -- The Kroger Co. (NYSE: KR) and Roundy's, Inc. (NYSE: RNDY) today announced a definitive merger agreement under which Kroger will purchase all outstanding shares of Roundy's for $3.60 per share in cash.”

The Kroger Company: Fundamental Strength And Growth

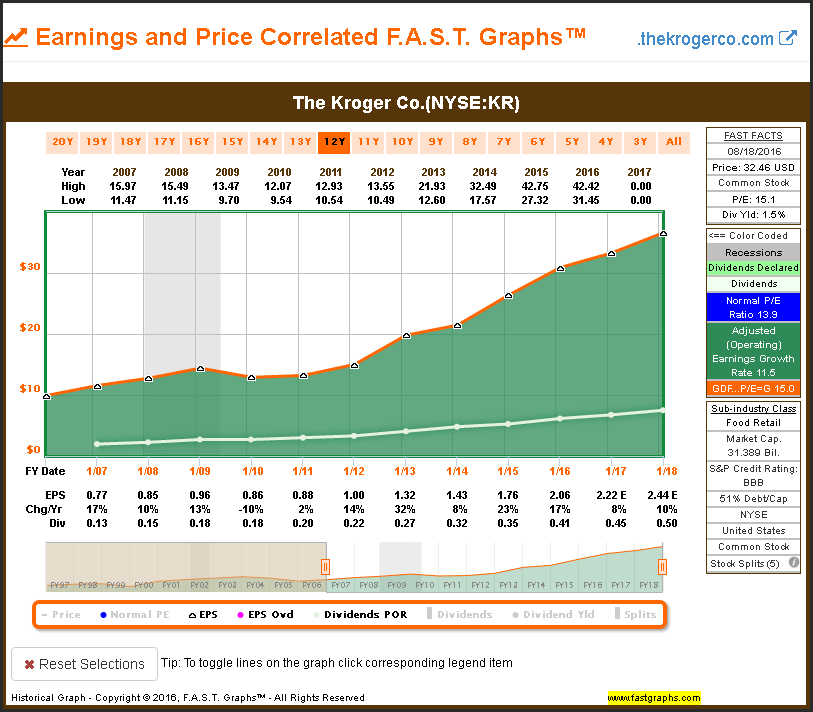

In the long run, earnings drive shareholder returns and dividend growth. The following F.A.S.T. Graph plots Kroger’s earnings since 1997. Although earnings growth has been a little lumpy, Kroger has produced higher and more consistent earnings growth than any other grocery store that I have reviewed. Additionally, notice how earnings growth has accelerated since 2011.

With this next graph I’ve added the light green dividend line (white looking) indicating that Kroger paid their first dividend in 2007, and it has increased it every year since at an average dividend growth rate of 13.2%. The dark green shaded area below the light green line represents the portion of earnings paid out to shareholders, or the dividend payout ratio. Therefore, you can graphically see that the company pays out approximately 20% of their earnings currently. Consequently, the dividend payout ratio is low and there is certainly room for it to grow.

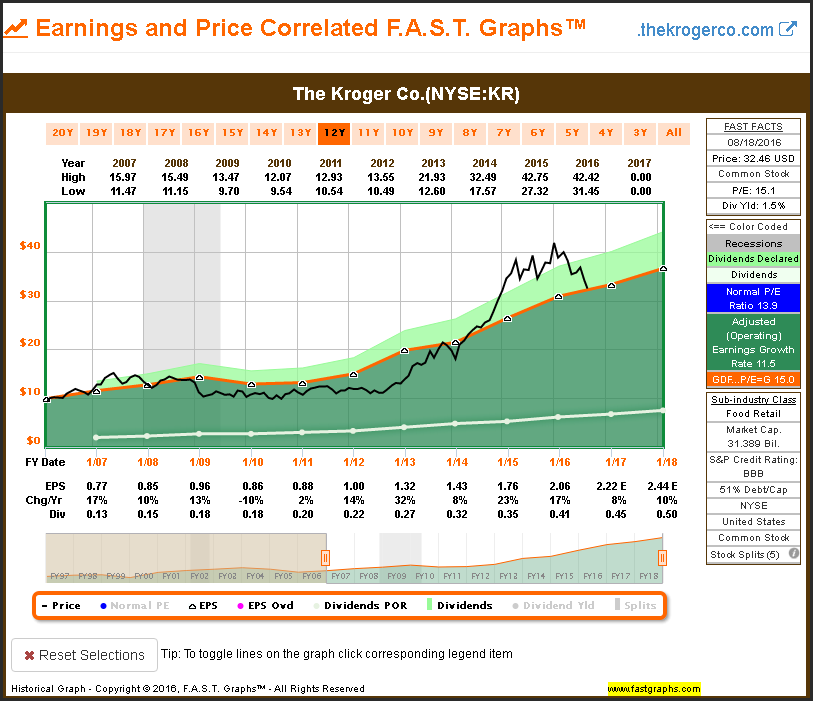

On this next graph, I’ve added the company’s monthly closing stock prices (the black line). Clearly, we see a high correlation between Kroger’s earnings and its stock price over time. But most importantly, we clearly see how Kroger’s stock price became significantly overvalued in 2015 as it disconnected from the orange line, and how it has been reverting to the fair value mean throughout 2016.

This has caused many people to question Kroger’s stock. People get agitated when a company’s stock price drops. However, to me it is clearly a function of overvaluation. Therefore, I see nothing wrong with Kroger other than the fact that it was overvalued. Irrational stock price action can occur on any company, and I believe the recent overvaluation on Kroger is a classic example.

Morningstar currently estimates Kroger’s fair value at $32 per share. Therefore, I found it interesting that this is approximately the valuation that Kroger’s stock price has fallen to. However, Morningstar has also announced that they have assigned this stock to a new analyst and expect to publish a new fair value estimate by August 19. Given the company’s recent drop in stock price, I am quite curious to see what that might do to their new fair valuation estimate (Note: Morningstar has updated their fair value estimate on Kroger dated August 8, 2016 and if The fair value estimate and $32 per share). Here’s an excerpt from Morningstar’s current fair valuation discussion on Kroger:

Kroger currently trades at Morningstar’s current fair valuation estimate:

“Our fair value estimate for Kroger is $32 per share, which implies a forward price/earnings ratio of 14 times, an enterprise value/EBITDA ratio of 7 times, and a free cash flow yield of about 2%. Our base-case fair value estimate reflects 0%-1% square footage growth annually over the next decade, identical-store sales growth of around 3.0%-3.5% over the next five years and near 3% (the middle of management's 2.5%-3.5% long-term target) over the latter stages of our explicit forecast period.”

With this next graph I’ve added the dividends after they have been paid out of earnings (the light green shaded area on the graph). F.A.S.T. Graphs™ does this to illustrate that the price following earnings is what generates the capital appreciation component of total return, and the dividends paid out generate the income component. Combined they provide the company’s total return.

It’s important to note on the above graph that Kroger’s stock price was fairly valued at the beginning and has now come back into fair value at the end. Consequently, Kroger’s capital appreciation over this timeframe of 12.7% correlates very closely with their 11.5% earnings growth rate over this timeframe. The difference is easily explained because Kroger’s P/E ratio on January 1, 2006 was 13.9 and the current P/E ratio on the graph is slightly higher at 15.1. In other words, earnings growth of 11.5% coupled with modest P/E ratio expansion from 13.9 to 15.1 explains the 12.7% capital appreciation.

Kroger’s Valuation Based On Cash Flow

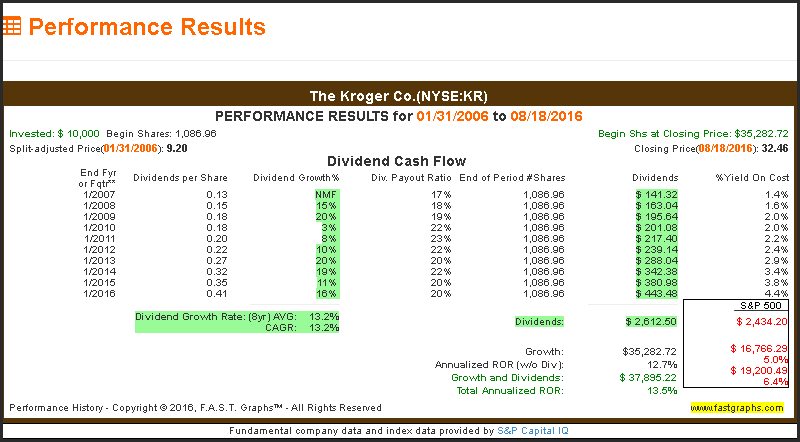

Whenever I am evaluating a company for prospective investment, I always start out by looking at the company’s earnings and price relationship over time. Additionally, I always run multiple timeframes in order to establish whether growth is accelerating, decreasing or staying the same. However, I also then look at the company’s cash flow and price relationship as well. To me, this is especially important when evaluating dividend paying stocks.

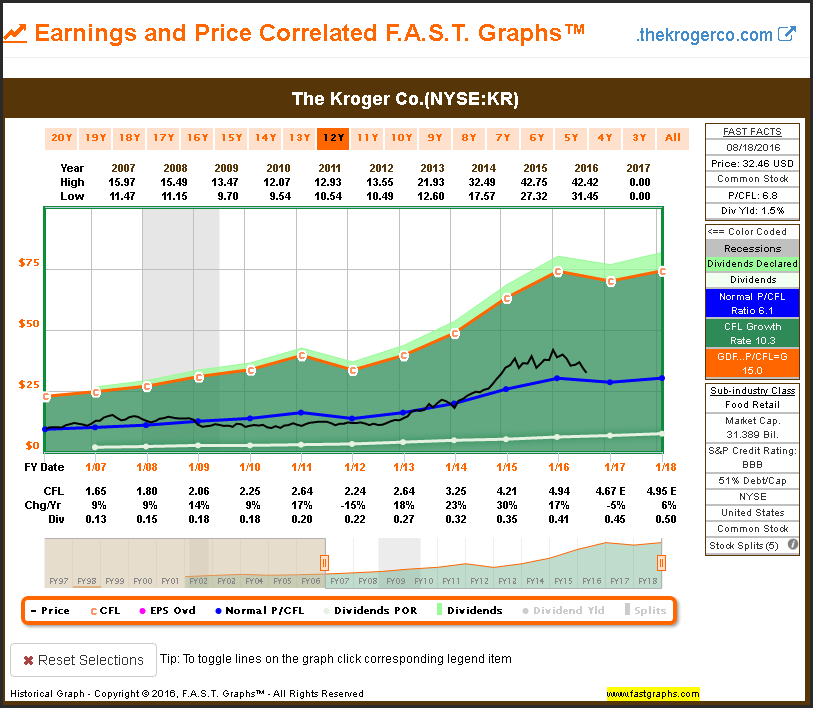

The dark blue historically normal price to cash flow (P/CFL) illustrates that Kroger’s stock price is well within its normal historical range relative to cash flow. In addition to being another important valuation measurement, evaluating a company based on cash flows provides insights into the company’s ability to pay and continue paying a dividend.

However, I never stop there. After I reviewed the price-to-earnings and price to cash flow graphs, I like to look a little deeper under the hood. The following FUN Graph (financial underlying numbers) graphs Kroger’s cash flow per share (cflps), operating cash flow per share (ocflps), free cash flow per share (fcflps) and dividends paid per share (dvpps). These metrics clearly illustrate that Kroger’s dividend is amply covered by all of its cash flows.

Cash Flow Per Share (cflps), Operating Cash Flow Per Share (ocflps), Free Cash Flow Per Share (fcflps), Dividends Paid Per Share (dvpps)

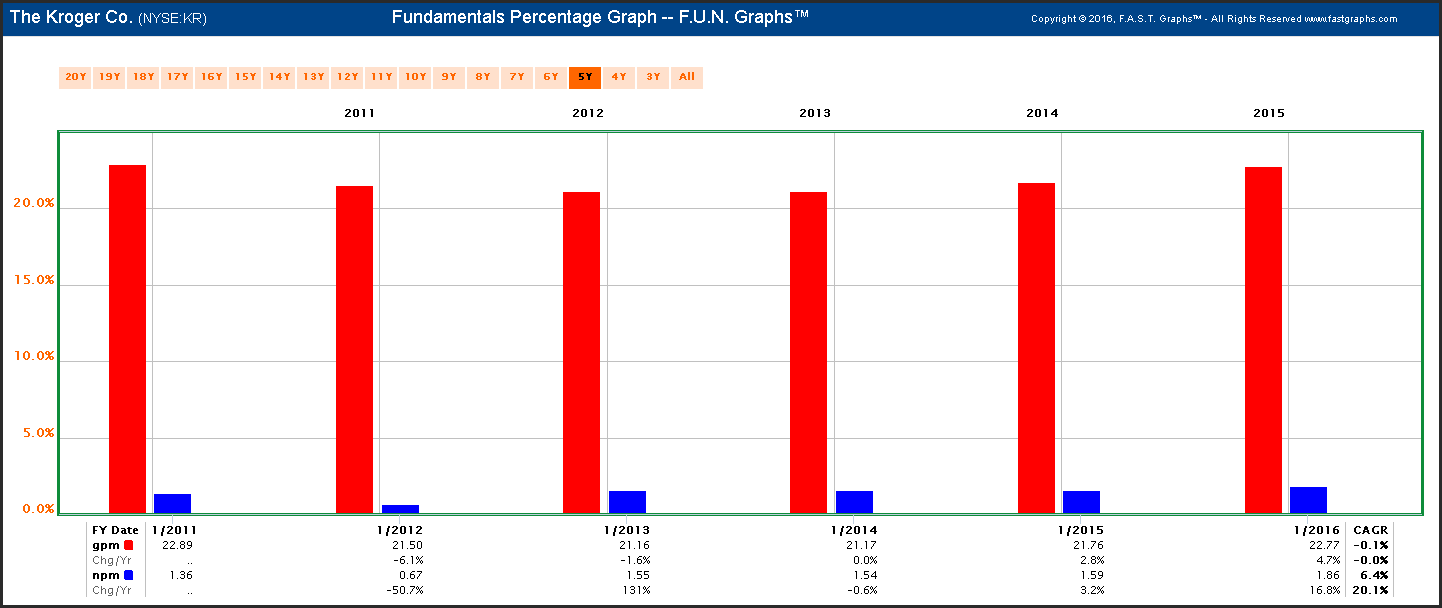

Grocery stores are notoriously low net margin businesses. However, Kroger does produce strong gross profit margins, and its net profit margin is higher than most of its peers, as indicated below.

Gross Profit Margin (gmp), Net Profit Margin (npm)

For a grocery store, Kroger generates very attractive returns on invested capital. The following graphs illustrate Kroger’s returns on invested capital for the past 12 quarters, and the second graph plots Kroger’s returns on invested capital since 2001. The following excerpt from Morningstar indicates that they believe that Kroger’s attractive returns on invested capital support their moat.

Morningstar’s economic moat:

“We believe that Kroger, as the second-largest grocer in the U.S. with $110 billion in annual sales, has a narrow economic moat due to throughput-driven cost advantages and a brand intangible asset resulting from superior locations, private label brands, and consumer analytics. Kroger’s ability to sustain excess ROICs, which we project to continue averaging around 11%-12% (versus our 6.6% weighted average cost of capital estimate), is driven by its ability to drive traffic and volume through its stores at the local and regional level.”

Return On Invested Capital (roi)

Return On Invested Capital Quarterly (roiq)

Looking To The Future: Kroger’s Earnings Growth

The consensus long-term estimated earnings growth forecasts for Kroger by 9 analysts reporting to S&P Capital IQ is 9.24%. If these forecasts are reasonably accurate, then long-term shareholders of Kroger going forward could enjoy double-digit rates of return, including dividends.

Zacks is in agreement with the consensus estimates as evidenced by the following excerpt:

“Zacks: We believe that given the robust identical supermarket sales growth (excluding fuel) for about 50 successive quarters and better-than-expected bottom-line performance for 10 consecutive quarters, Kroger is poised to achieve its long-term earnings per share growth rate target of 8%−11%. We expect the company to sustain its earnings growth momentum, buoyed by the Customer 1st strategy, effective cost management and share repurchase activities.”

Summary and Conclusions

Kroger is not the highest yielding Dividend Challenger in the universe. However, it is one of the fastest growing and one of the most attractively valued. Consequently, I suggest that dividend growth investors looking for an above-average total return from a high quality and fairly valued dividend growth stock might want to take a closer look at Kroger.

Disclosure: No position.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.