Return on equity (ROE) is one of the foundational measures of profitability in finance. it is taught in many first year finance courses in college, it’s a staple in the CFA curriculum, and is widely used as a “go-to” indicator of how profitable a firm or an industry is in the investment management profession. In many industry groups ROE is as high as 20% even as world is mired in a slow growth environment. There seems to be a disconnect among the macro data and the the company data. Given this, why isn’t there more discussion about how unrealistically high ROE’s seem to have become for many industry groups in the face of ever slower global growth?

Regular readers know that we believe company financial statements are increasingly losing its relevance in explaining stock price returns. The primary reason reason this is occurring is that corporations have shifted its asset base composition from one that is primarily only tangible fixed capital (i.e. classic property, plant and equipment) to one that includes a large percentage of intangible capital (i.e. research and development, codified information, brand equity, patents, unique business process). However, due to archaic accounting rules put in place prior to the invention of the personal computer, let alone decades before the internet came into existence, companies are forced to expense intangible investments rather than treat them as an investment as one would property, plant and equipment. In this blog, we have highlighted many times how this non-symmetrical treatment of investments impacts the asset side of the balance sheet by understating total assets. In this post, we are going to illustrate how that distorts profitability measures such as ROE as well.

Return on equity is of course made up of two numbers: net income and shareholder’s equity (we will leave DuPont ROE breakdown for another day). So how is net income effected by the current accounting rules for intangible investments? For companies that invest heavily, and persistently in intangible assets, net income is artificially suppressed because investments are forced to be treated as expenses. This drives up current period expenses which drives down current period net income. This is effect is partially offset when financial statements are adjusted for intangibles by a larger depreciation expense. When intangible are removed from the balance sheet and instead treated as a long-term investment, this reduces current period expenses (which increases current period income) but also creates a larger depreciation expenses (which then reduces current period income) since there are more long-term assets on the balance sheet. However, the net effect is that reported net income is usually lower than it would be if intangible investment was treated the same as fixed investment. Let’s use the pharma, biotech, and life science industry group to illustrate this. Aggregate net income is about 7% higher after adjusting for intangibles than the reported data would lead you to believe.

So if net income is actually understated after adjusting for intangibles, how could ROE be overstated? It comes back to the equity component. Because intangible investments are almost universally 100% equity financed (because you can’t get a loan from a bank if you don’t have any hard collateral to lend against), the liability component of the balance sheet doesn’t increase when companies increase the intangible asset component of the balance sheet. This means the equity component is the balancing mechanism and consequently, the financial community is greatly understating how much equity companies are utilizing to produce profits. For the pharma, biotech, and life science industry group, aggregate total equity is understated by a whopping $450 billion, or 52%! With the denominator being understated by more than 50%, it’s no wonder ROE looks high.

So bringing this all together, ROE for the pharma, biotech, and life science industry group is 41% artificially inflated because of how companies are forced to account for intangible investments. To the street, the pharma, biotech, and life science industry group seems to be returning a hefty 15.3% on equity, which is just slightly down from the 18-20% heyday in the earlier 2000s. More importantly, it looks as though ROE has held steady between 14-16% for well over decade. However, once one accounts for intangible investments, we see that ROE for this group has been steadily declining for over 15 years from 17% to 10.85% today. Again, more importantly it is clear that trend in profitability in this group has been downwards for well over a decade which is in stark contrast to what the reported data would lead you to conclude. And of of course, this then greatly impacts the multiples investors would be willing to pay for this profitability profile.

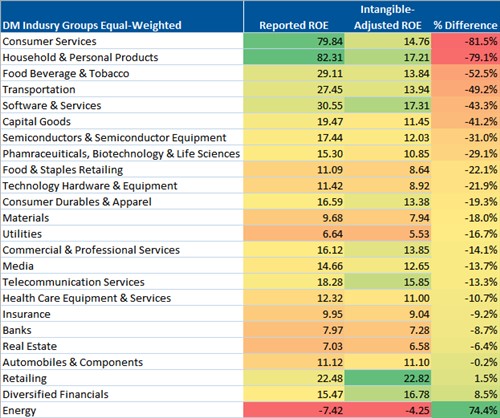

Lastly, this doesn’t effect just one industry group but affects all industry groups to varying degrees. And in a few cases, ROE is actually higher once adjusted for intangible investments. However, for most industry groups, ROE is greatly overstated using reported data.