Introduction

The S&P 500 index is commonly used as a benchmark that investors use to measure the performance of their individual portfolios against. However, the S&P 500 is comprised of a very diverse group of companies. Just about every classification of company you can imagine can be found in the S&P 500. Furthermore, it is also comprised of all of the major industry sectors. With this series of articles, I have been examining the S&P 500 constituents in the healthcare sector. In part 1, I presented what I consider to be attractively valued dividend growth stocks in the S&P 500 healthcare sector. In this part 2, I will continue to examine S&P 500 healthcare stocks; however, with this article I will focus on fairly valued non-dividend paying growth-oriented S&P 500 healthcare constituents.

Passive versus Active Investing

Choosing passive versus active stock portfolios is one of the most hotly debated subjects regarding investing in stocks. Passive investing implies investing in an index fund while active investing means carefully handpicking specific stocks that meet your own goals, objectives and risk tolerances. Personally, I have always preferred what Wall Street calls active investing. However, I take exception with that designation. My personal investment philosophy is to invest in attractively valued businesses with the objective of holding for the long-term. Consequently, my investment process could hardly be called active because there is little turnover in my portfolios.

Therefore, I reject the designations active versus passive in favor of selective versus non-selective. It is my preference to carefully select my investments based on sound valuation and sound fundamental attributes. And more importantly, I prefer to select my investments based on their precise characteristics that meet my specific goals, objectives and risk tolerances.

For example, my current personal investment objectives are to seek fairly valued high-quality dividend growth stocks with a history of increasing their dividends each year. Therefore, my goal is not simply maximum current income; I am also keenly focused on constructing a portfolio with the opportunity for that income to grow each year. In this regard, I consider long-term capital gain a secondary objective. To be clear, I do expect to generate a reasonable level of capital gains with my dividend growth stocks. Investing in them when they are attractively valued gives me confidence that I can generate capital appreciation commensurate with each company’s earnings growth. However, I am not concerned with outperforming the market on a total return basis, but I am concerned with outperforming the market on a total dividend income basis over the long term.

This leads me to pointing out additional reasons why I reject passive - also known as index investing. For example, the S&P 500 is often used by investors as the primary benchmark to judge their performance against. However, that judgment is always based on total return calculations. I also often utilize the S&P 500 as a benchmark to judge my own portfolio against. However, relative to my current income oriented investment philosophy, my measurement for performance is based on how much dividend income my portfolio generates versus the S&P 500. Moreover, I also measure how fast that dividend income is growing compared to the S&P 500.

In this dividend income regard, the S&P 500 is at a great disadvantage. I took a rough count and found that approximately 85 of the S&P 500 companies pay no dividends at all, and another 58 yield 1% or less. Using round numbers, more than 25% of the S&P 500 constituents offer none or very little in the way of dividends. Since my objective is a growing dividend income stream, I see no logical reason to own the index when so many of the constituents do not meet my specific objectives.

Additionally, there are many S&P 500 constituents that I would never invest in on my own volition. Therefore, I see no reason why I would want to invest in them by purchasing the index when I would never invest in them by my own selection process. Moreover, my recent examination of the S&P 500 index constituents also discovered that the majority of the blue-chip dividend growth companies I would typically be attracted to are currently overvalued. Once again, if I am not willing to invest in them today because they are overvalued, therefore, I would not want to invest in them today via the index.

However, with all that said, I also recognize and accept the reality that not everyone has the same investment objectives as I do. There are many prudent strategies that investors can choose to employ and there are many different kinds of individual stocks that can be selected for common stock portfolios. To me, the key is to clearly identify your personal objectives and risk tolerances, and then choose appropriate investments that are compatible with those goals. Investing is not a one-size-fits-all process.

Attractive Healthcare Growth Stocks in the S&P 500 for the Total Return Investor

Therefore, even though I personally favor dividend growth stocks, there are also valid reasons and return opportunities available through investing in non-dividend paying but growing companies. As I pointed out in part 1 of this series I have recently been examining the healthcare sector of the S&P 500 looking for attractively valued stocks. Consequently, in addition to the fairly valued dividend growth stocks I reported on in part 1, I also came across a few intriguing growth stock opportunities in the healthcare sector of the S&P 500.

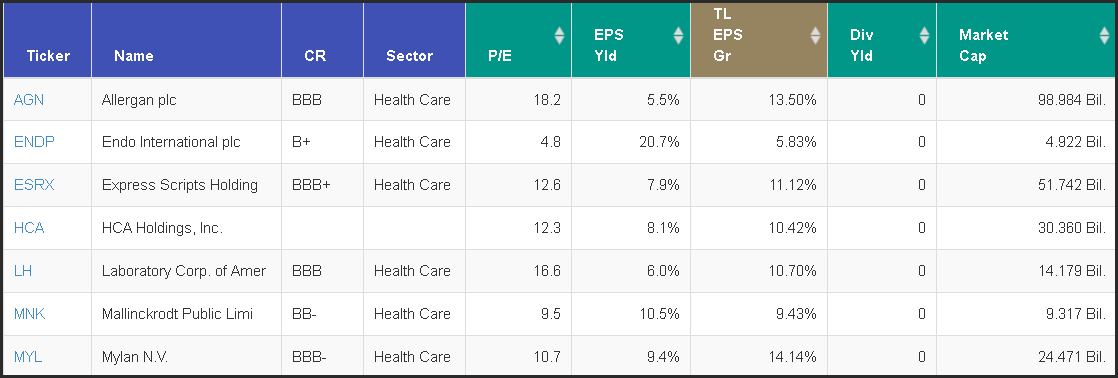

As a result, I felt compelled to share these findings with those who are interested in investing for growth or total return. The following “Portfolio Review” via FAST Graphs lists the seven S&P 500 healthcare growth stock constituents that I felt were worth taking a closer look at. There are various reasons why I chose to highlight these specific examples. In all cases, I felt that valuations were fair, and in a few cases - even compelling. On the other hand, for the few that I found compelling, there are reasons why valuations are so low. Consequently, I highly recommend conducting your own thorough due diligence and research. Nevertheless, as an old associate of mine used to like to say, the problems appear to be already in the price. Therefore, I will provide a brief commentary on each selection indicating why I chose to feature it in this article.

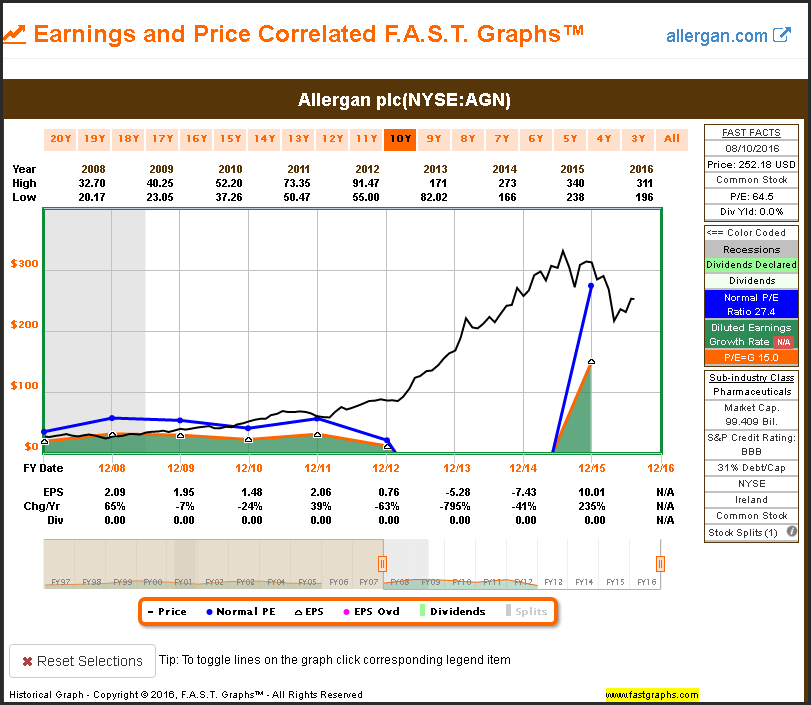

Allergan plc (AGN)

Below is a short business description courtesy of Morningstar:

“Allergan PLC is a specialty pharmaceutical company. The Company is engaged in developing, manufacturing and distributing generic, brand and biosimilar products.”

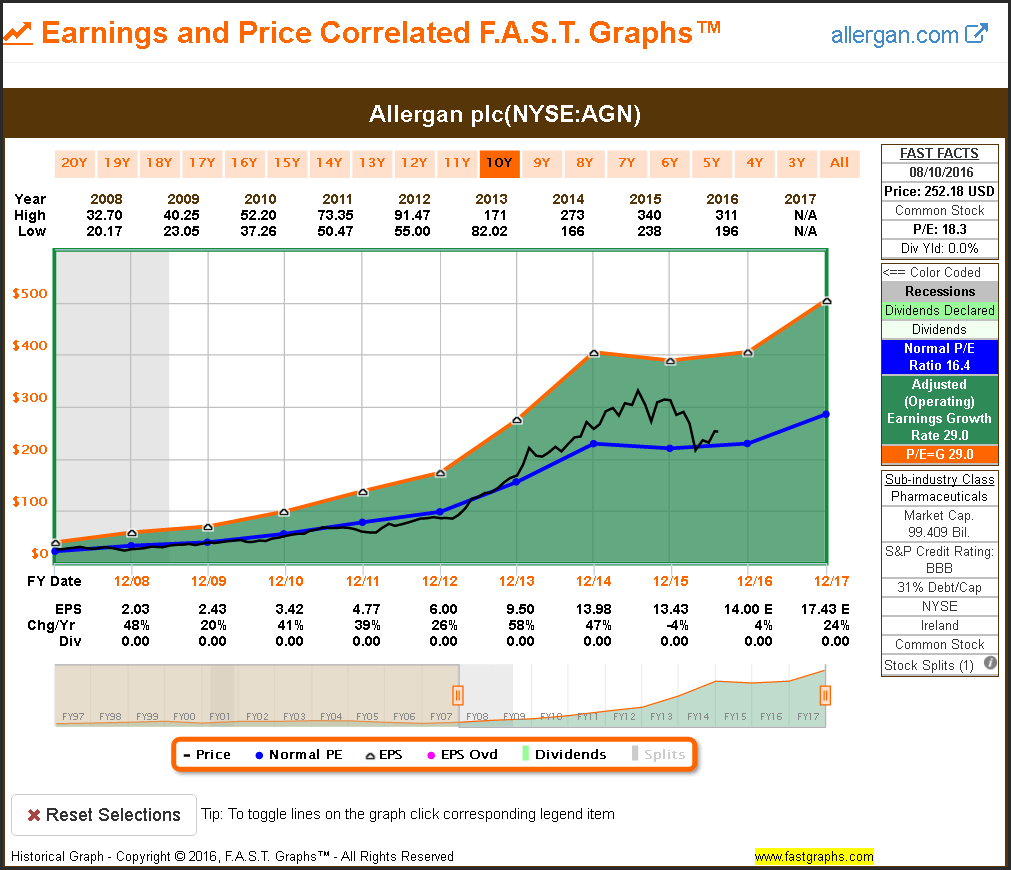

I was attracted to Allergan based on its high and relatively consistent earnings growth since 2008. However, I was also struck by the fact that the market has valued Allergan’s high earnings growth achievements at a market (average) valuation. I find this interesting, because it is very rare to find a company with such a high rate of earnings growth available at such a reasonable valuation. As evidenced by the blue normal P/E ratio line on the graph, the market has recently valued this stock at a 16 P/E ratio more or less. To me, that is a low valuation for a company that has grown earnings at 29% per annum.

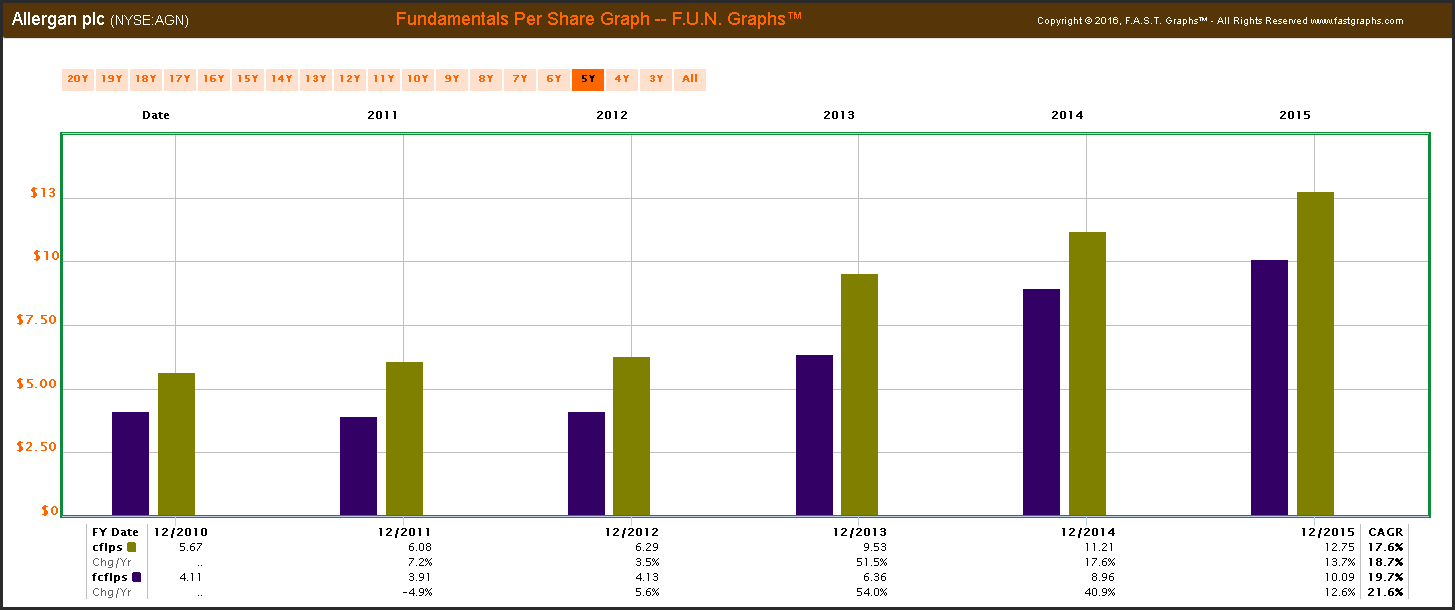

Cash Flow Per Share (cflps), Free Cash Flow Per Share (fcflps)

I was further intrigued by Allergan when I examined the company’s cash flow and free cash flow per share. Both of these metrics suggest that the business is quite healthy on an operating basis.

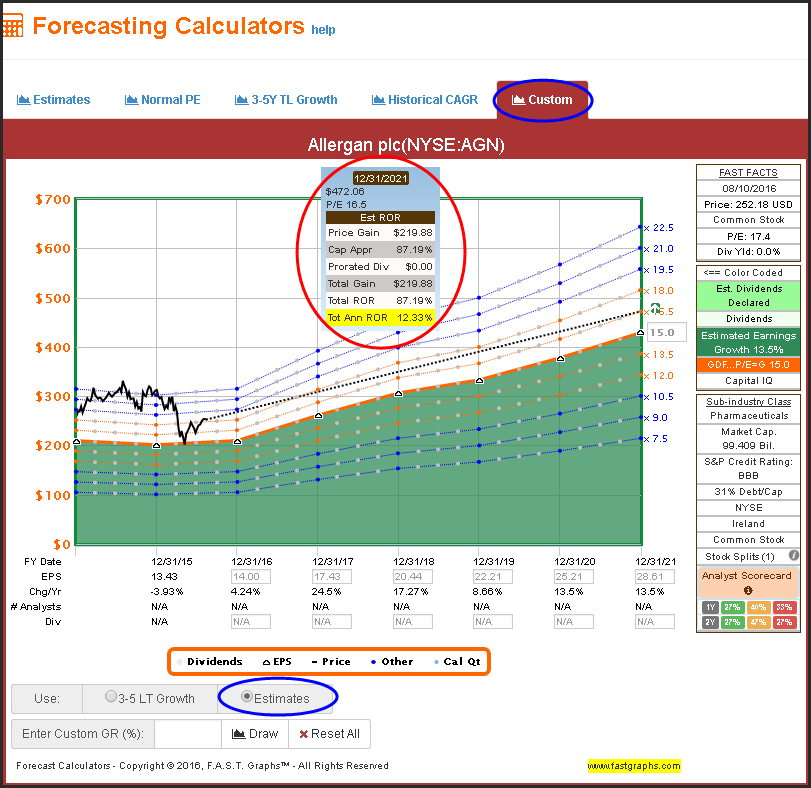

Judging by its historical earnings growth rate, I was not surprised to see that the consensus estimates of analysts expect this company to continue growing at mid-double-digit rates. I was also not surprised to see that expected earnings growth was lower than historical norms considering the company’s already approaching a $100 billion market-cap.

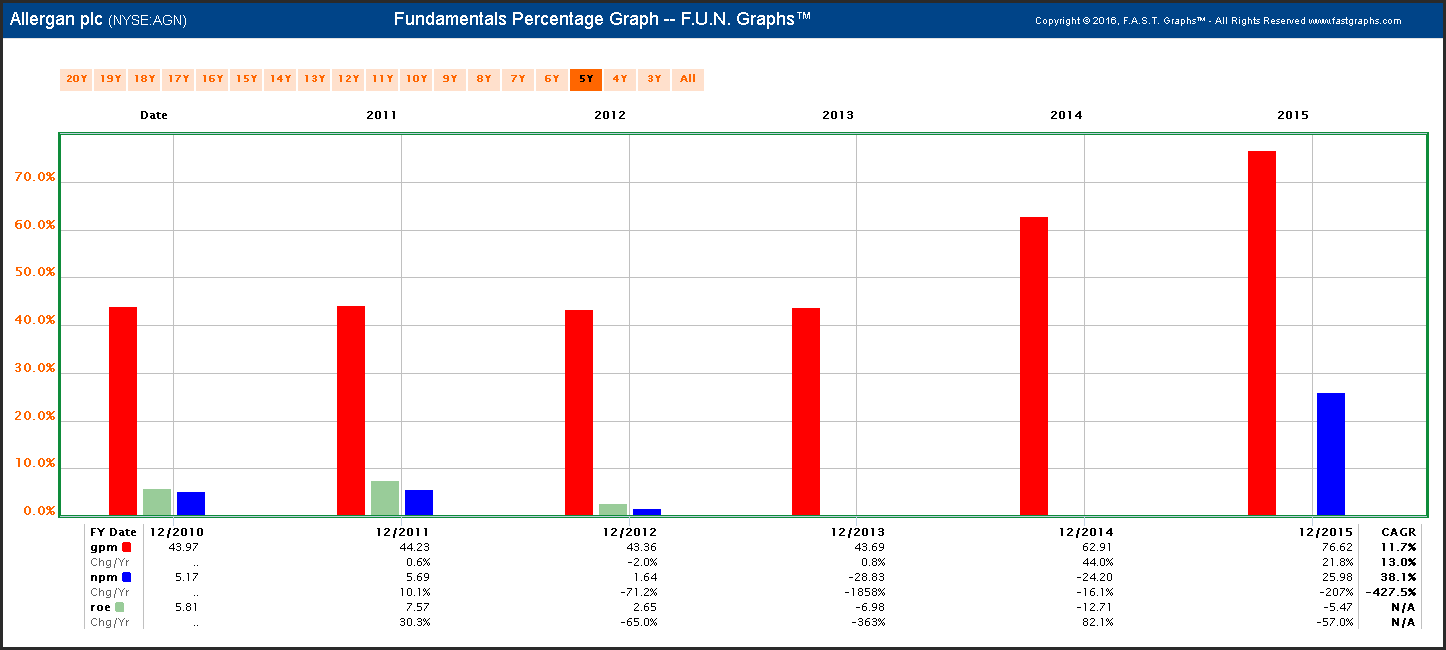

Gross Profit Margin (GPM), Net Profit Margin (NPM), Return On Equity (ROE)

When I first examined gross and net profit margin, I was shocked to see that net margins virtually disappeared from 2012 through 2014. However, there were legitimate reasons why this happened, to include acquisition costs, failed mergers and other theoretically nonrecurring events.

As a result, when I looked at diluted earnings (GAAP) I saw a completely different perspective compared to what I saw when I looked at operating earnings and cash flows. Although I always like to examine GAAP results, I differ from many people regarding their importance or relevance as a valuation tool. When valuing a stock for potential investment, I am more concerned with how the business is performing as an operating company. Nevertheless, I felt it was important to point these issues out on this research candidate.

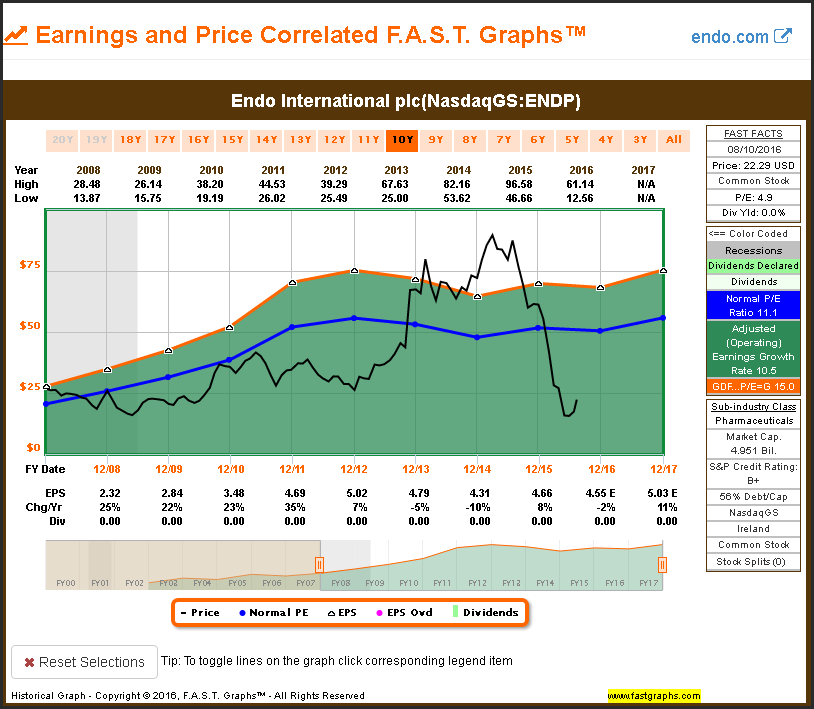

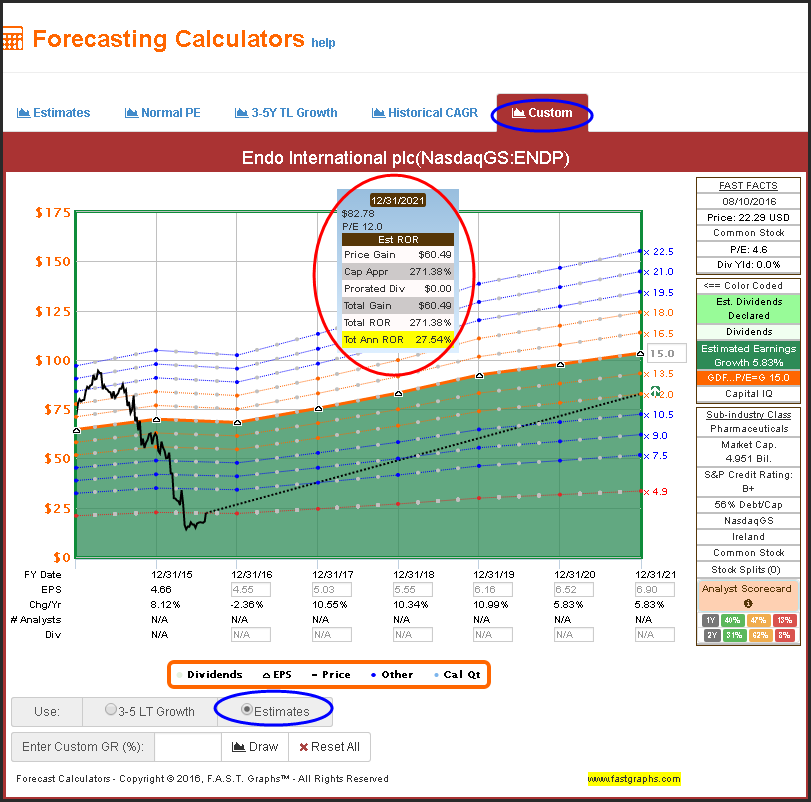

Endo International plc (ENDP)

Below is a short business description courtesy of Morningstar:

“Endo International PLC is a specialty healthcare company. The Company is engaged in developing, manufacturing, marketing and distribution of branded pharmaceutical and generic products as well as medical devices.”

What struck me about Endo International was its extremely low valuation. Earnings have clearly flattened in recent years, but I believe the stock price reaction seems way overdone. Consequently, I included this research candidate as a compelling valuation and potential recovery candidate. Therefore, I was not surprised to see the stock surge yesterday based on an impressive second-quarter earnings report. Nevertheless, I offer this as an interesting speculation based on compelling low valuation. However, as I looked deeper into additional important fundamental metrics, the speculative nature of this particular research candidate is important to note.

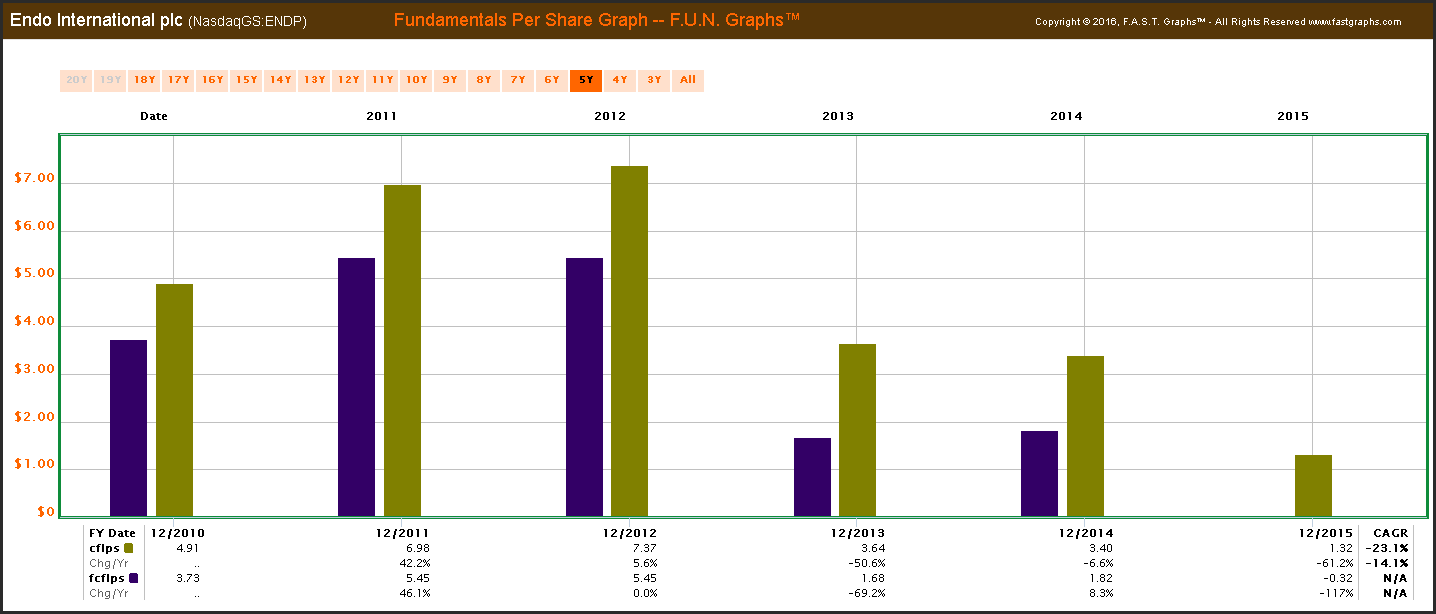

Cash Flow Per Share (cflps), Free Cash Flow Per Share (fcflps)

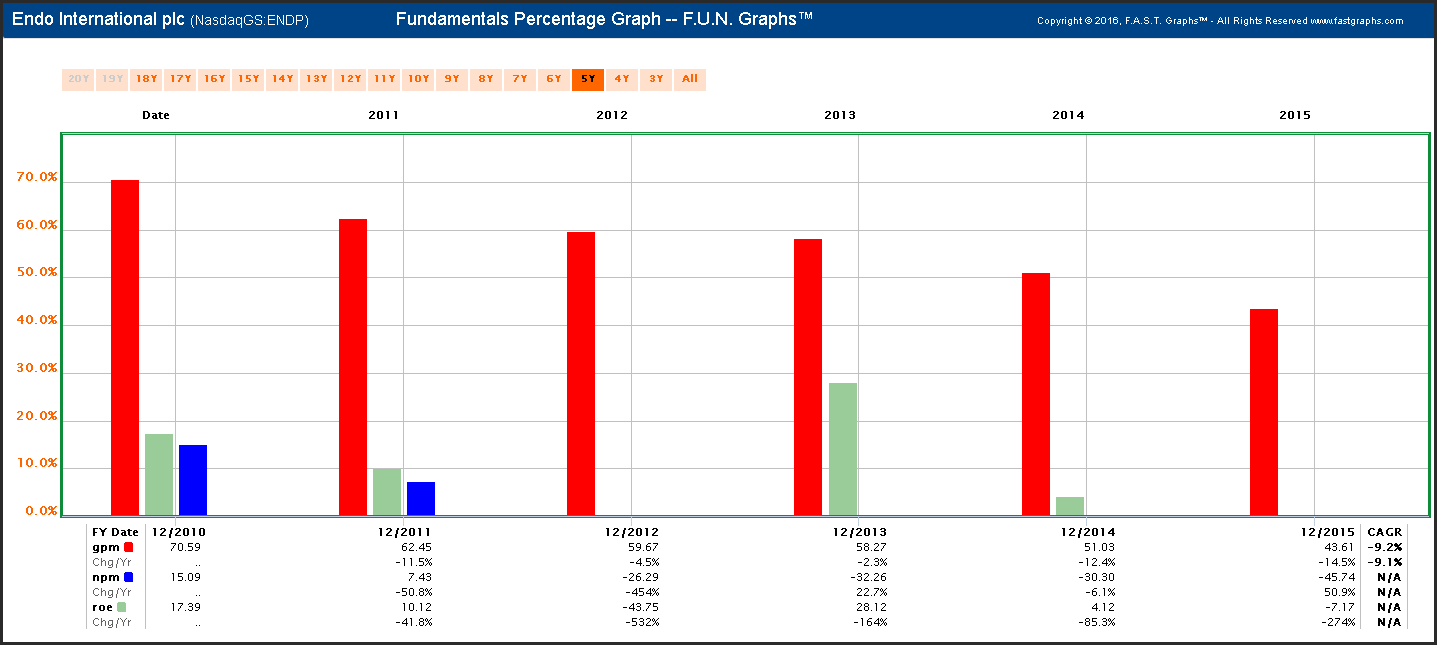

Gross Profit Margin (GPM), Net Profit Margin (NPM), Return On Equity (ROE)

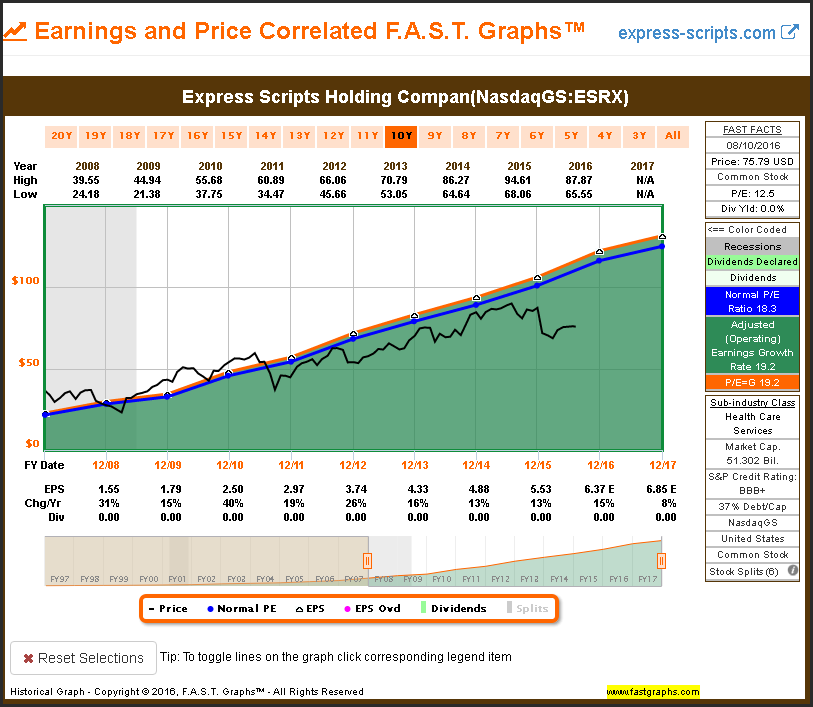

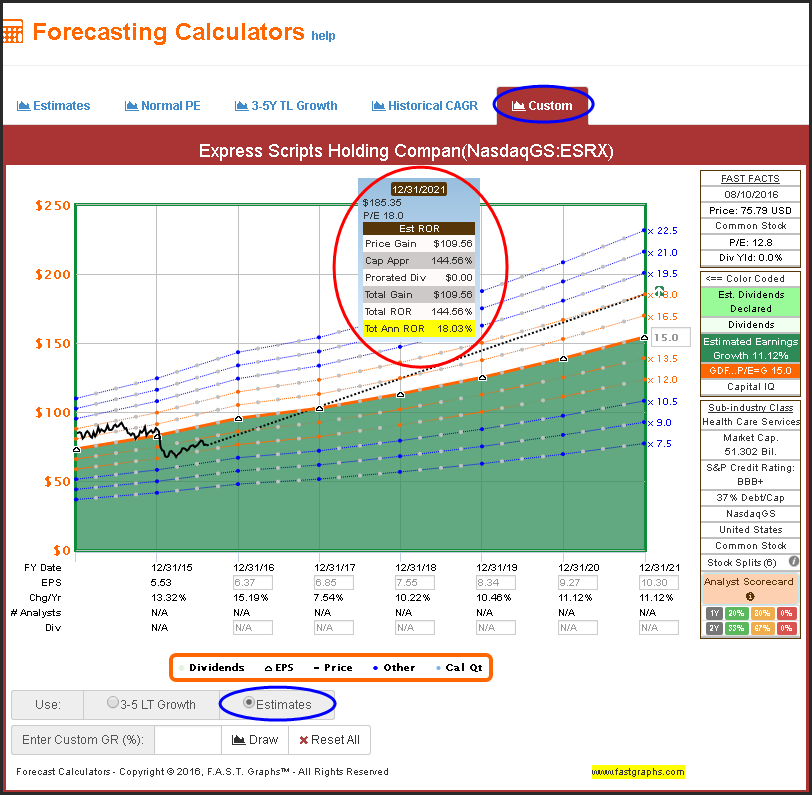

Express Scripts Holding (ESRX)

Below is a short business description courtesy of Morningstar:

“Express Scripts Holding Co offers healthcare management & administration services such as managed care organizations, health insurers, workers' compensation plans & government health programs.”

To me, there was very little not to like about Express Scripts and its consistently strong earnings growth rate history. But what I liked most was its compelling valuation. As I indicated earlier, it’s hard to find a company with this type of earnings growth record trading at such a low valuation.

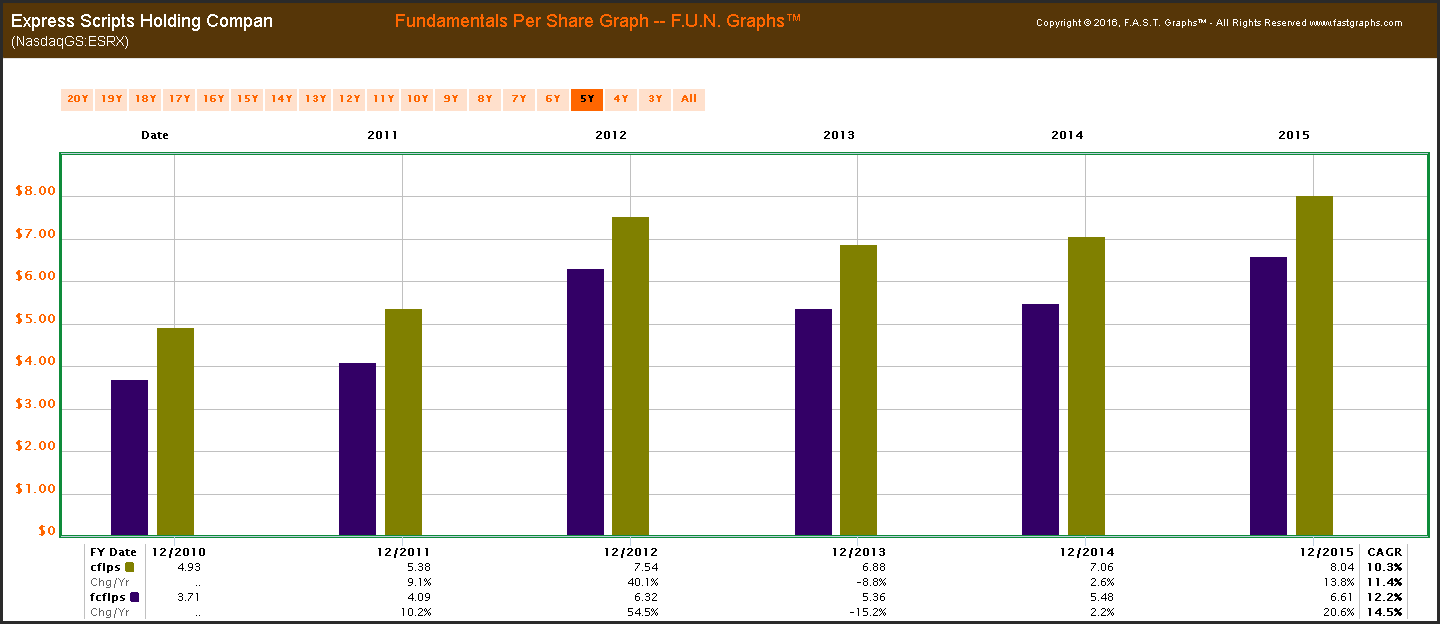

Cash Flow Per Share (cflps), Free Cash Flow Per Share (fcflps)

Gross Profit Margin (GPM), Net Profit Margin (NPM), Return On Equity (ROE)

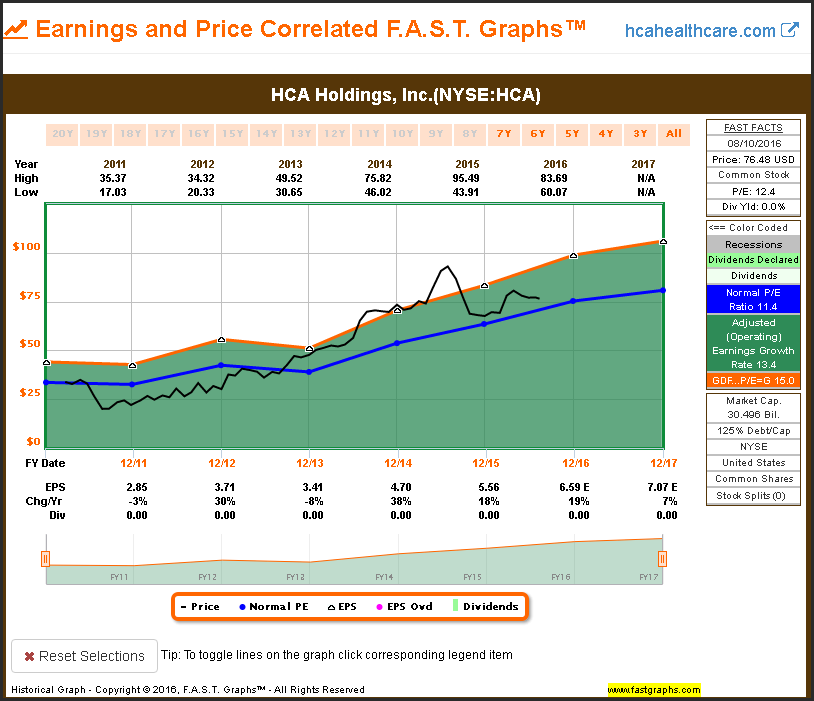

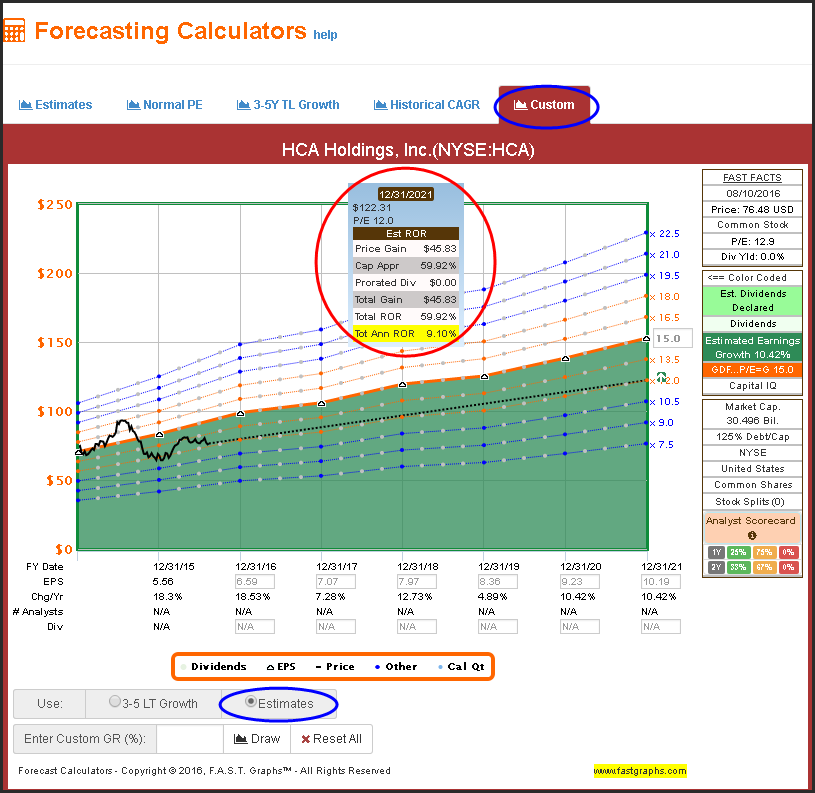

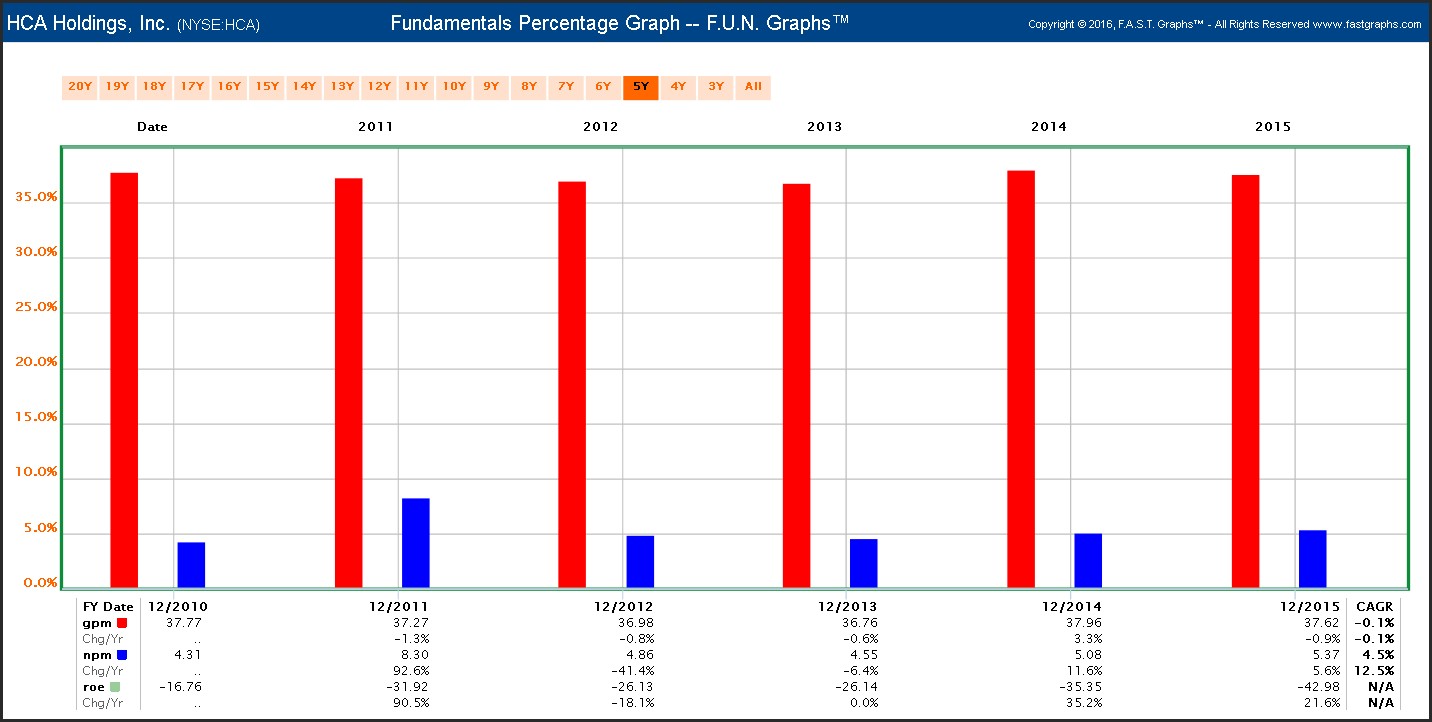

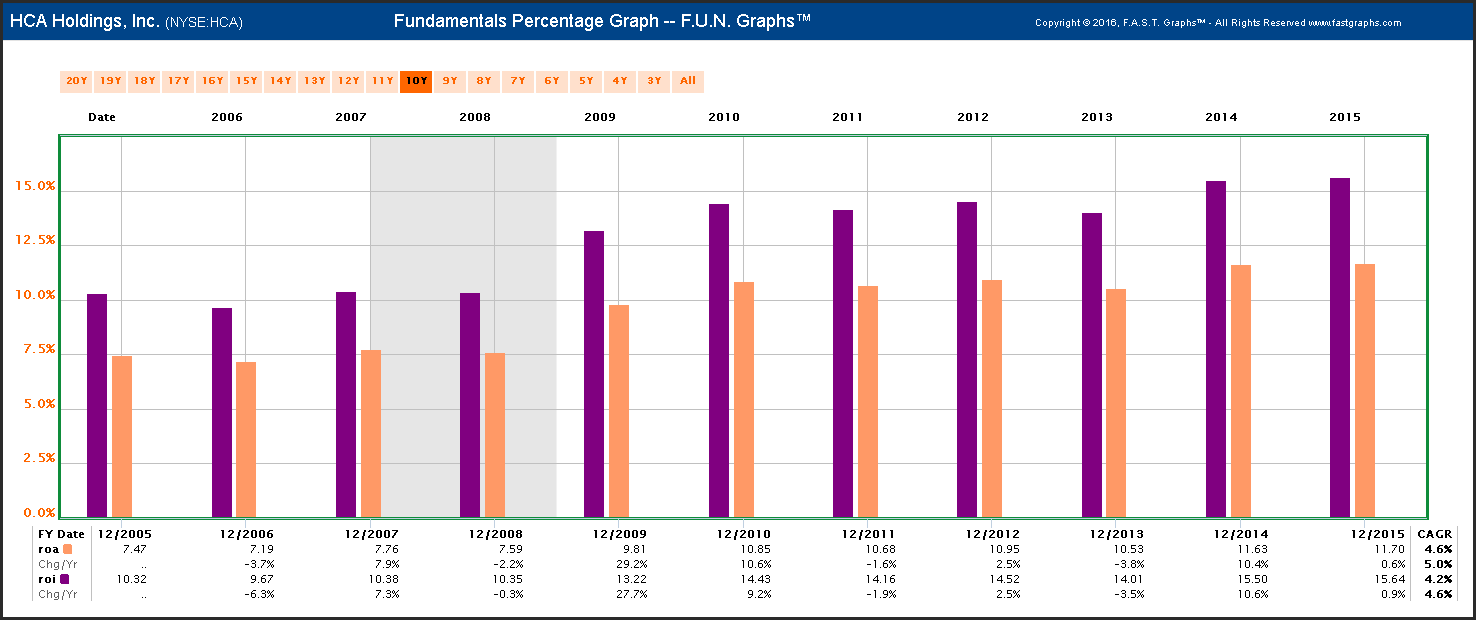

HCA Holdings Inc (HCA)

Below is a short business description courtesy of Morningstar:

“HCA Holdings Inc is a health care services company. It operates general acute care hospitals, psychiatric hospitals; and rehabilitation hospitals. It also operates freestanding surgery centers.”

I was attracted to HCA Holdings’ current valuation in light of the moderately high overvaluation that the stock traded at through the summer of 2015. The stock price correction since then has potentially created a buying opportunity. My one caveat is the company’s high debt-to-capital ratio. However, the company does have strong cash flows, and I’ve read reports where management is focused on improving their debt situation.

Cash Flow Per Share (cflps), Free Cash Flow Per Share (fcflps)

Gross Profit Margin (GPM), Net Profit Margin (NPM), Return On Equity (ROE)

Return on assets (ROA), Return on Invested Capital (ROI)

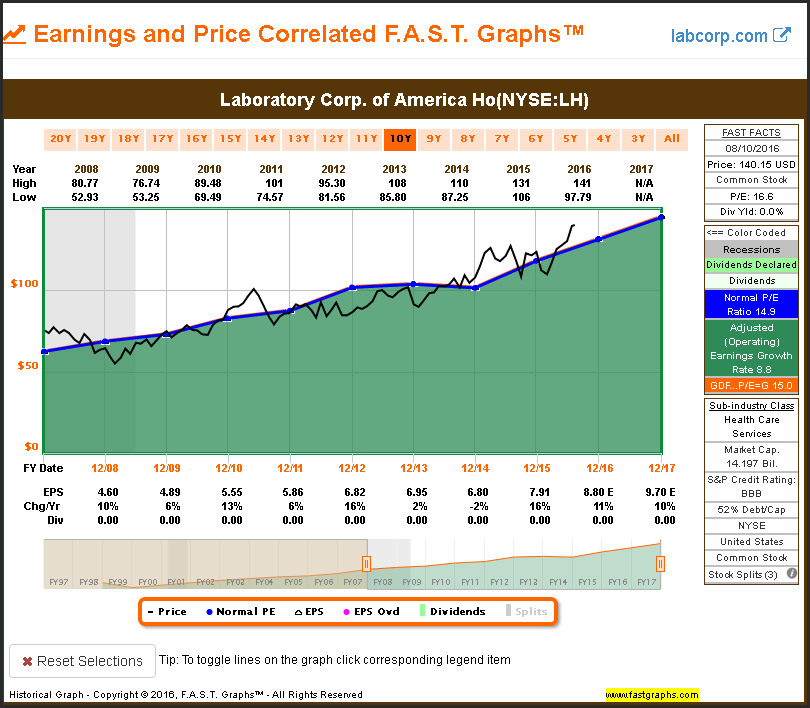

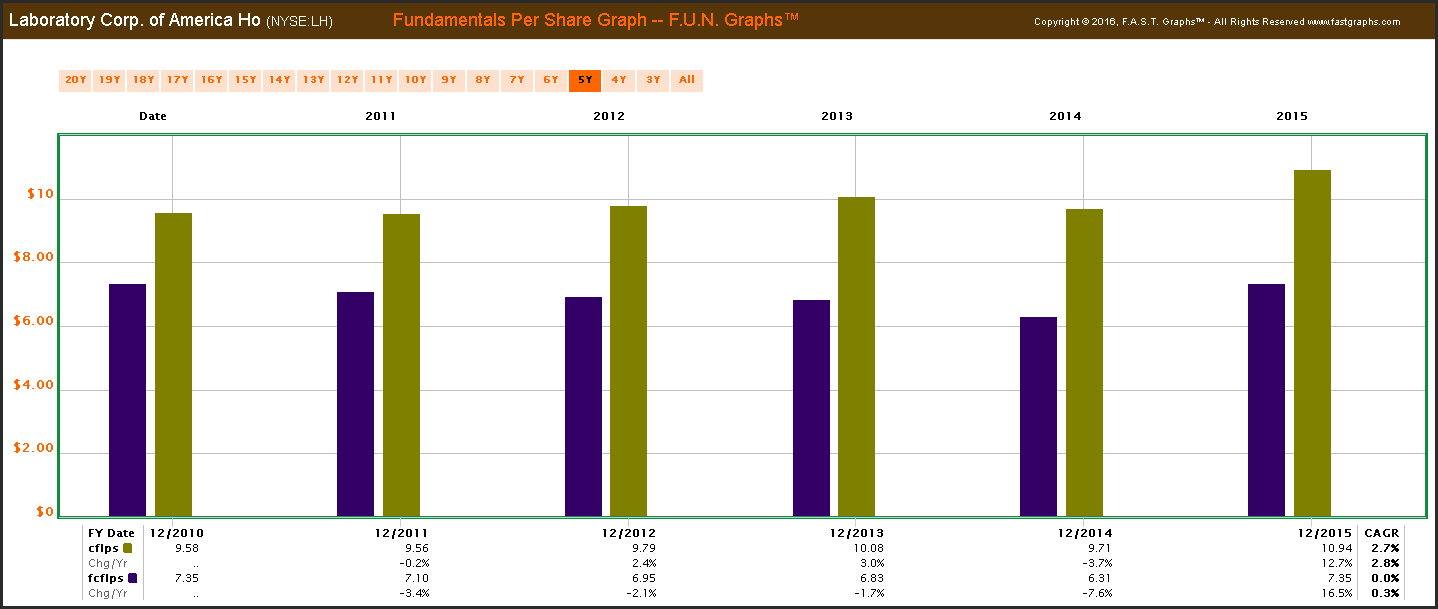

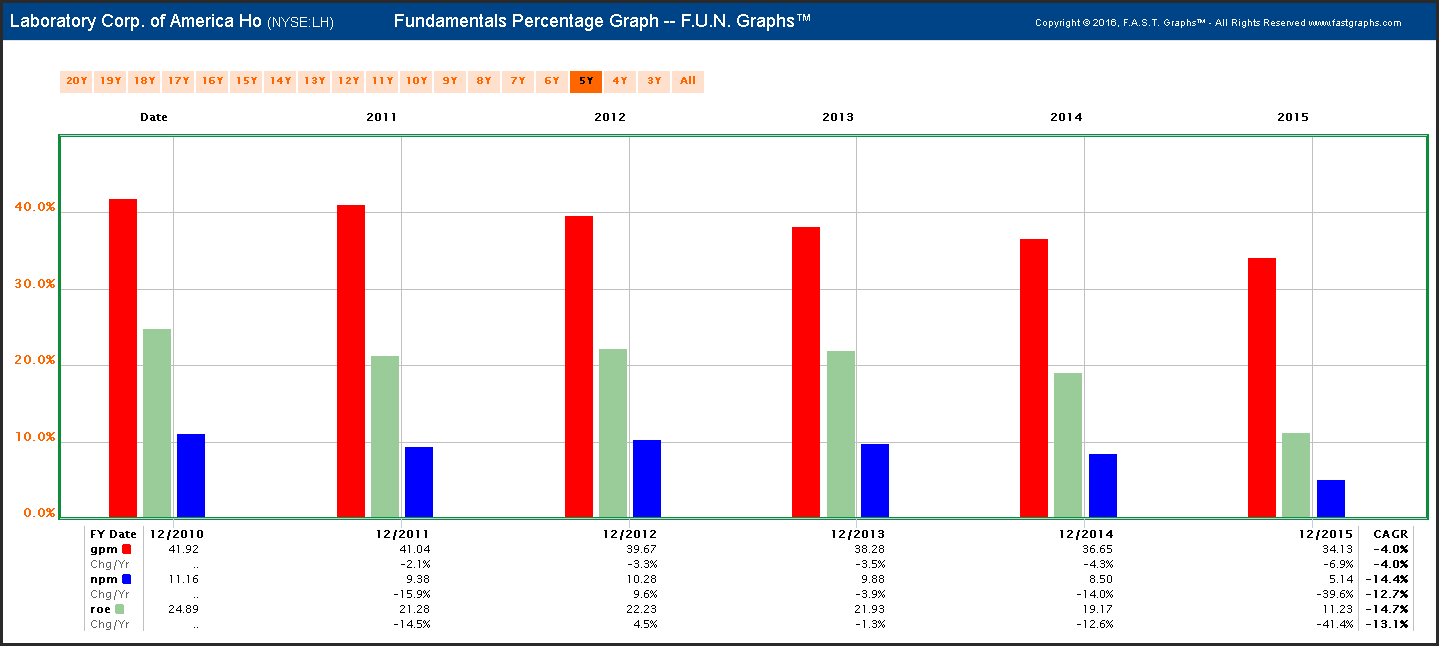

Laboratory Corp of America (LH)

Below is a short business description courtesy of Morningstar:

“Laboratory Corp of America Holdings is a healthcare diagnostics company. The Company along with its subsidiaries provides clinical laboratory services and end-to-end drug development support.”

Although I really like the consistent operating history that Laboratory Corp of America Holdings has produced, I do want to point out that I consider its valuation a little high. Consequently, I would suggest looking for a better entry point. Nevertheless, I felt it was worthy of inclusion in this article in spite of its moderately high valuation.

Cash Flow Per Share (cflps), Free Cash Flow Per Share (fcflps)

Gross Profit Margin (GPM), Net Profit Margin (NPM), Return On Equity (ROE)

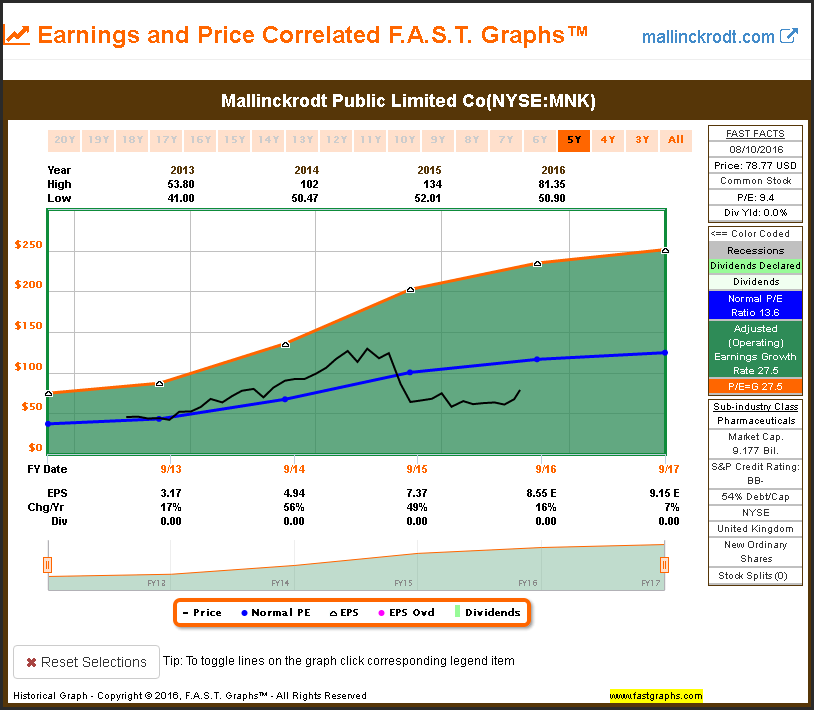

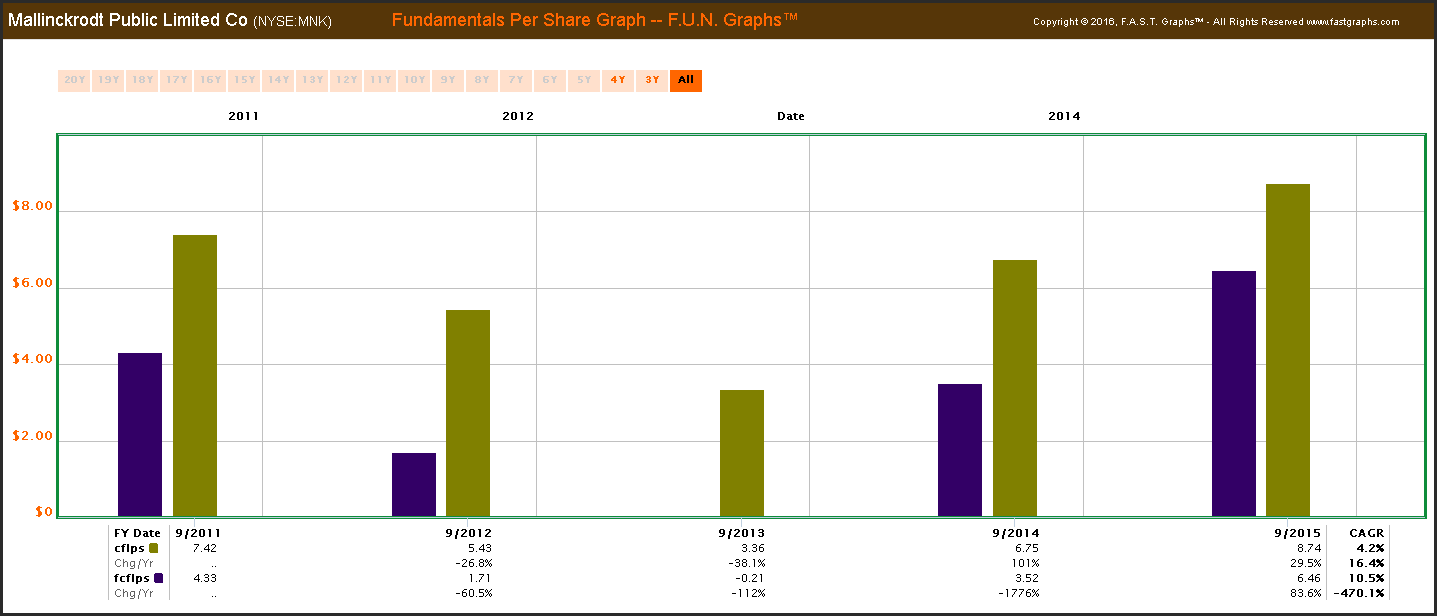

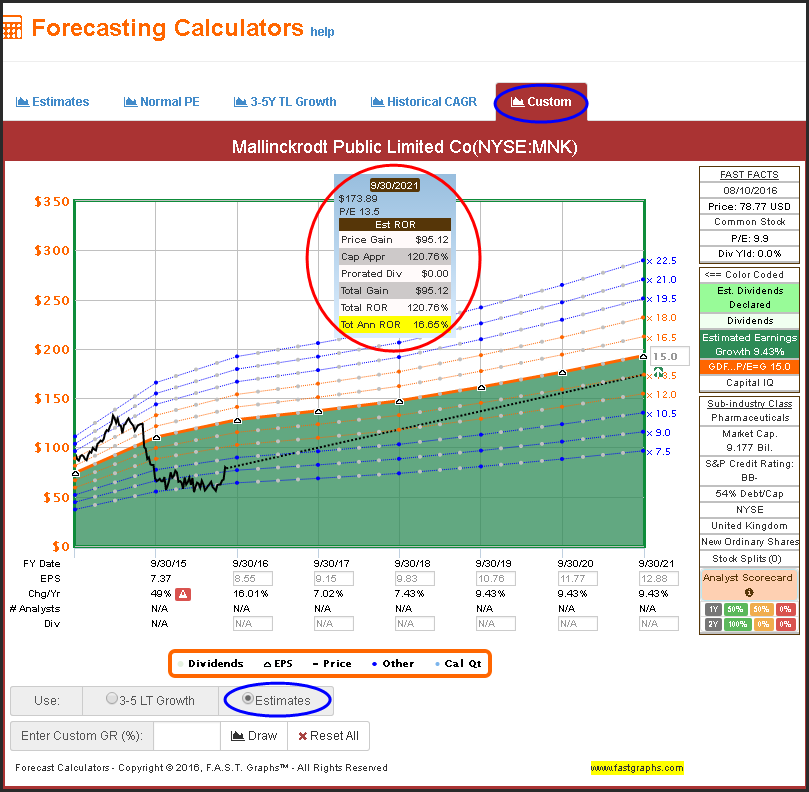

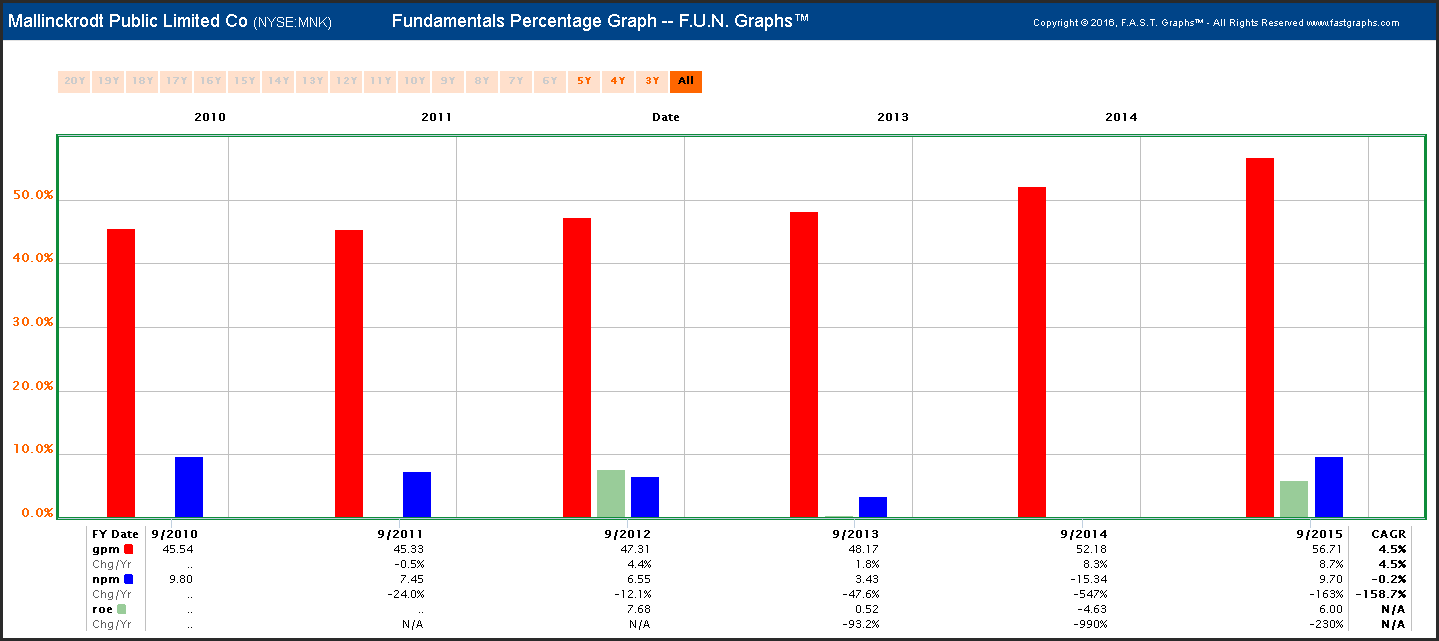

Mallinckrodt Public Limited (MNK)

Below is a short business description courtesy of Morningstar:

“Mallinckrodt PLC along with its subsidiaries operates in a specialty biopharmaceutical and nuclear imaging business that develops, manufactures, markets and distributes specialty pharmaceutical and biopharmaceutical products and nuclear imaging agents.”

Mallinckrodt is offered as a speculative undervalued research candidate. The primary appeal here would be the potential for P/E ratio expansion back to the 13-15 range.

Cash Flow Per Share (cflps), Free Cash Flow Per Share (fcflps)

Gross Profit Margin (GPM), Net Profit Margin (NPM), Return On Equity (ROE)

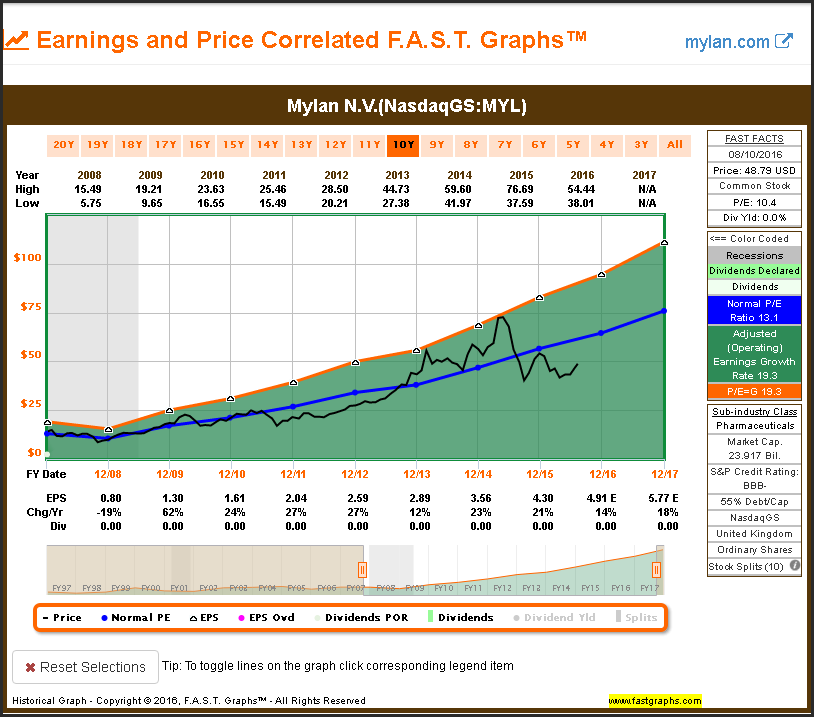

Mylan N.V. (MYL)

Below is a short business description courtesy of Morningstar:

“Mylan NV along with its subsidiaries is a pharmaceutical company. The Company develops, licenses, manufactures, markets and distributes generic, branded generic and specialty pharmaceuticals.”

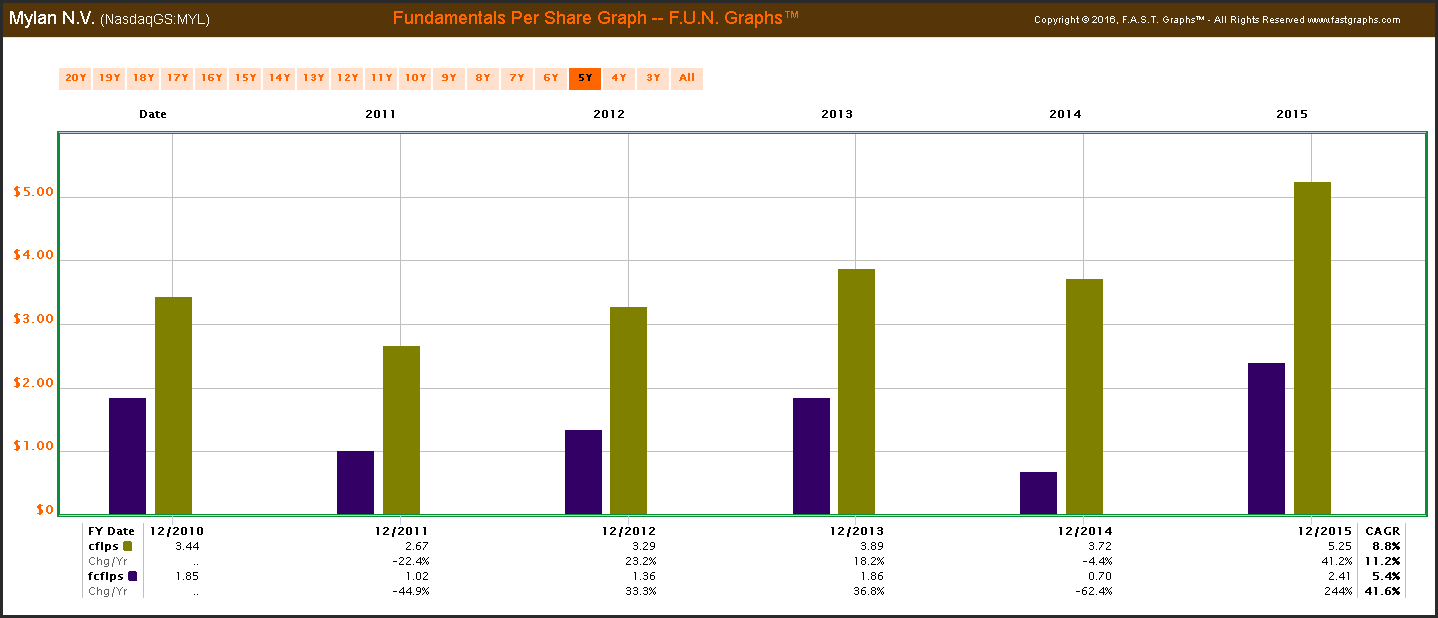

I was attracted to Mylan because I consider the stock extremely undervalued and I like its long-term growth prospects. I believe that recent acquisitions have added to this company’s appeal, and I suspect future acquisitions are likely going forward. All in all, I believe that Mylan looks like a significantly undervalued above-average growing investment opportunity.

Cash Flow Per Share (cflps), Free Cash Flow Per Share (fcflps)

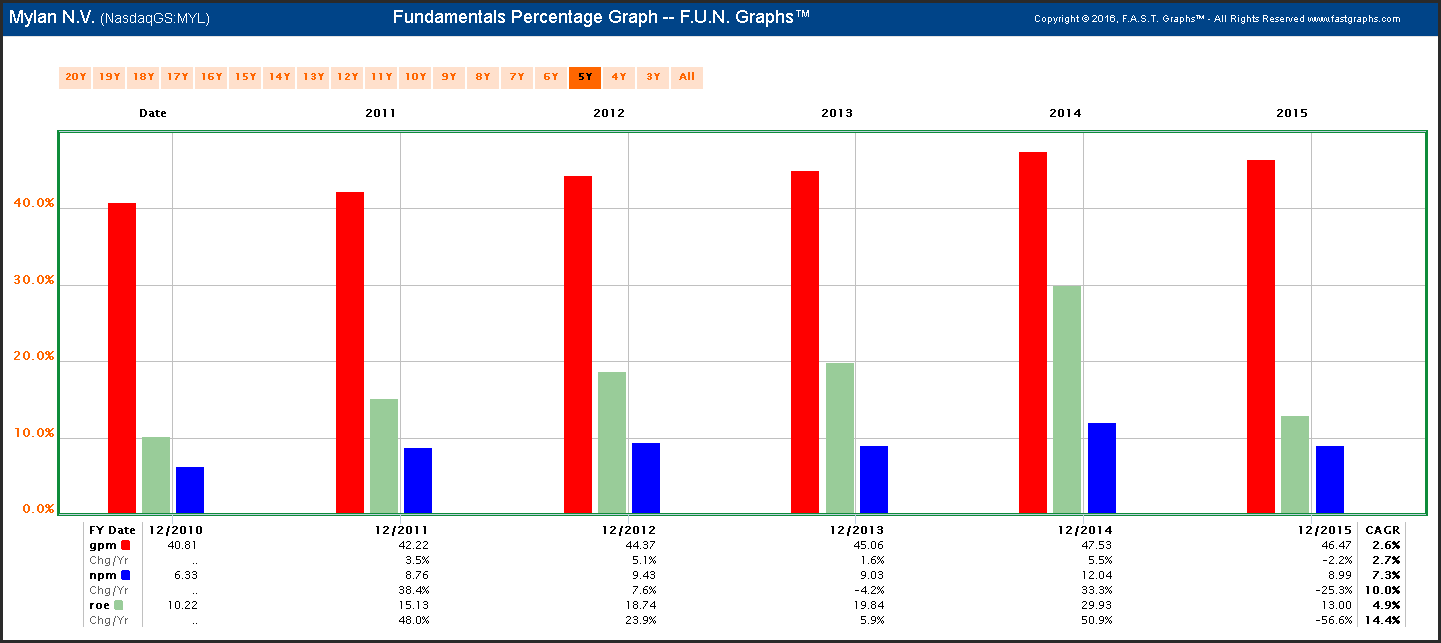

Gross Profit Margin (GPM), Net Profit Margin (NPM), Return On Equity (ROE)

Summary and Conclusions

With this two-part series I looked at what appeared to be attractively valued stocks in the healthcare sector of the S&P 500. In part 1, I highlighted dividend growth stocks. In this part 2, I highlighted more growth oriented S&P 500 healthcare constituents. Although I do believe that finding attractive valuation today is difficult, I do believe there are attractive investments available for those who are willing to look beyond the valuation of overall market.

If you enjoyed this article, scroll up and click on the "Follow" button next to my name to see updates on my future articles in your feed.

Disclosure: Long ESRX

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.