“There is no panacea for the low returns implied by asset valuations today. Anyone suggesting differently is either fooling themselves or trying to fool you. But piling into the assets that have been the biggest help to portfolios over the past several years, as tempting as it may be, is probably an even worse idea than it usually is.” – Ben Inker, GMO

Today, let’s take a look at the most recent market valuations and what they are telling us about forward returns over the next ten years. But keep in the back of your mind that you can get pretty close on seven and ten-year return probabilities but it is a coin flip on what the equity returns will be over next number of months.

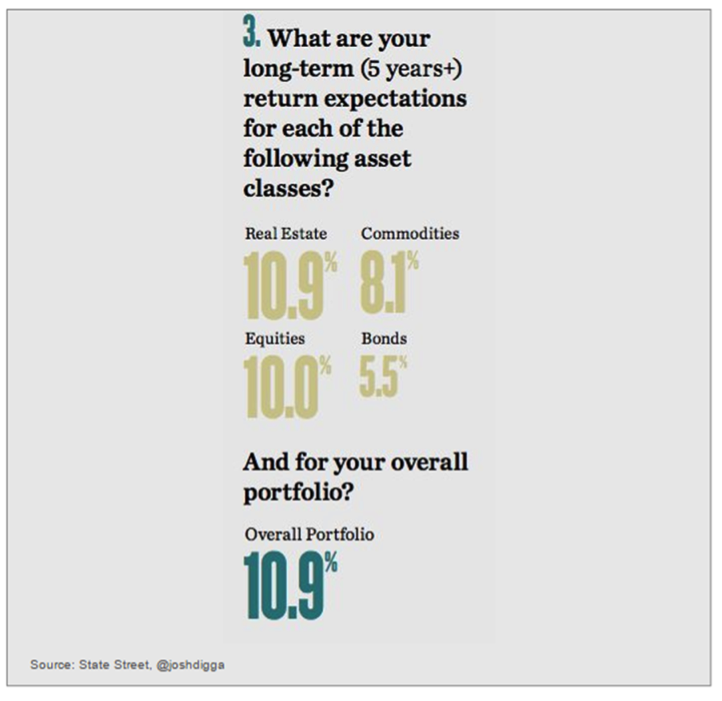

We do know that the insatiable demand for stocks with above average yield is causing valuations to diverge materially from historical norms. This may continue. In a recent State Street poll, investors were asked what their returns expectations are for the next five years and beyond for real estate, commodities, equities and bonds.

Answer: 10.9% for real estate, 8.1% for commodities, 10% for equities and 5.5% for bonds

10% for equities? I find myself wondering who spiked their punch bowl.

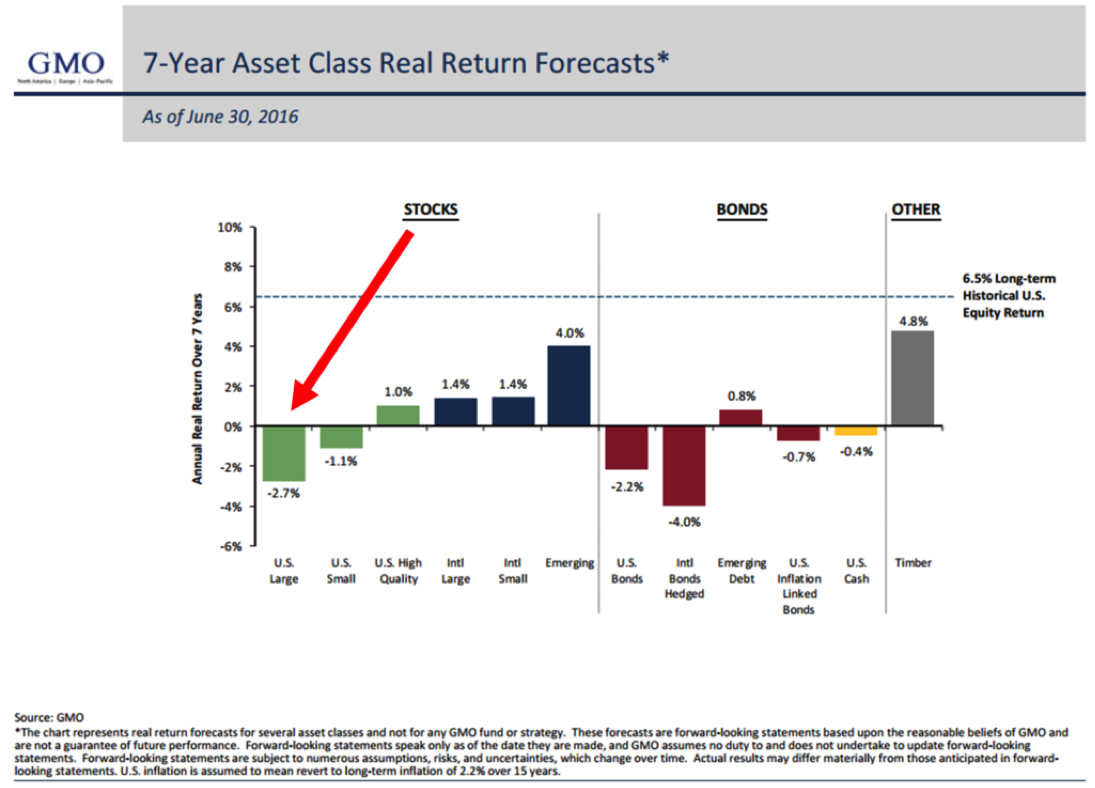

I previously wrote that in December 1999, GMO’s seven-year forward return forecast predicted a negative annualized real (after inflation) return for stocks. They took a lot of heat but they were proven right.

In the intro quote above, Ben noted, “There is no panacea for the low returns implied by asset valuations today. Anyone suggesting differently is either fooling themselves or trying to fool you.” Amen brother.

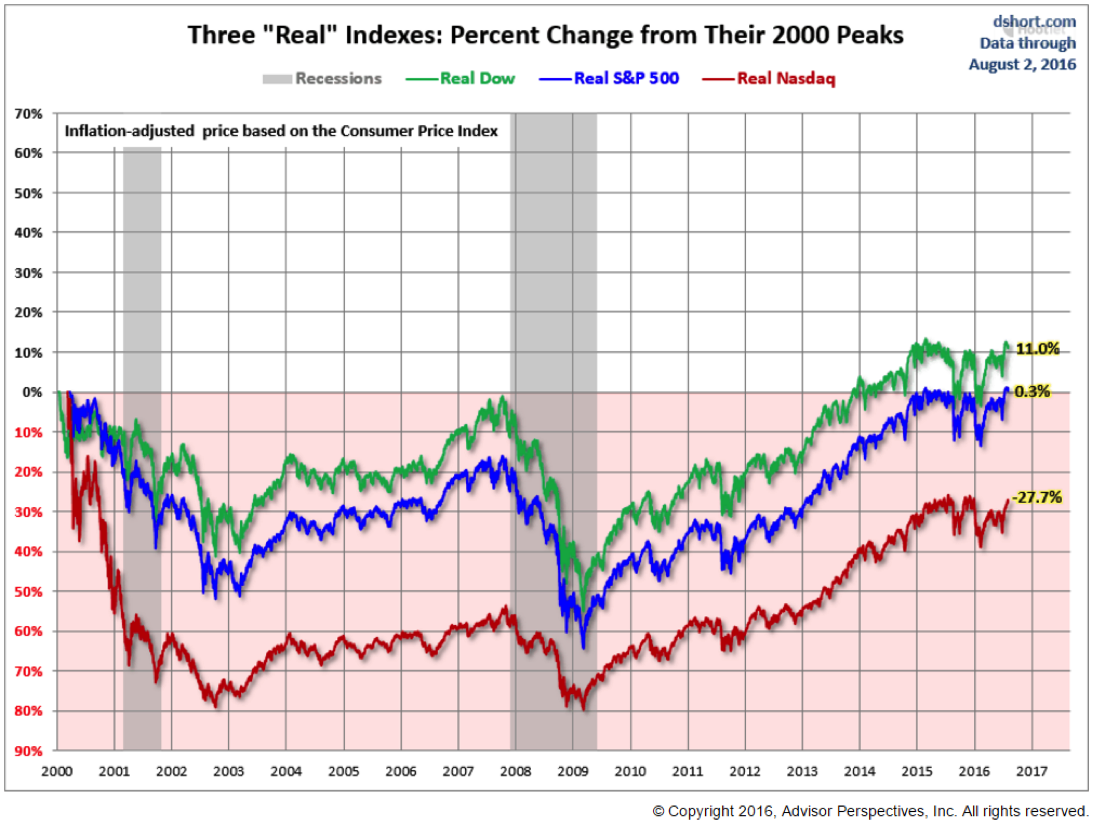

Let’s go back a few years to another point in time when valuations were stretched and investors were “fooling themselves.” Note the two red arrows in the next chart.

Here is that same chart after inflation is calculated in.

Source: DShort Advisors Perspectives

We find ourselves at a position much like the late 1990s. After a 17-year bull market, valuations were simply too high. Everyone was racing into technology. The market may go higher but what are the implications over the next five, ten and fifteen years — both before and after inflation. And boy, does the Fed wish to create inflation.

As of June 30, 2016, GMO’s seven-year real (after inflation) return forecast for equities is even more negative than it was in 1999 (then a negative 1.9% forecast). Imagine a negative compounded -2.7% per year over the coming seven years.

Let’s go back to that State Street survey: 10% for equities? 5.5% for bonds?

$100,000 compounded at 10% per year for ten years equals approximately $259,000. That is almost 2.6 times on your money. GMO uses a seven year forecast but I also like ten-year forward return forecasts so let’s consider several investment choices (bets) over the coming ten years.

Maybe you’re not in the 10% return camp? Maybe you are not as bearish as GMO but believe 10% is unlikely. Let’s call it the “hope so” camp so for simplicity’s sake, let’s halve the potential return to 5%. That means that by the end of June 2026, you look back and find that your $100,000 grew to $163,000 or 1.63 times your initial investment.

Finally, let’s consider the GMO outcome. While their return prediction is for a -2.70% after inflation (the actual market return less inflation), let’s assume that inflation is 2.70% and thus makes the nominal (before inflation is subtracted out) return 0%.

Overall, inflation is important because your money has to grow in a way that covers the rising costs of things you need. If inflation is 2% per year, you need a return of 2% on your investments just to keep pace. But I digress.

Three bets to consider: 10%, 5% or 0%.

- #1 State Street Poll (pays you 2.6 to 1) – your $100,000 grows to $260,000

- #2 Hope So (pays 1.63 to 1) – your $100,000 grows to $163,000

- #3 GMO (pays 1 to 1) – your $100,000 grows to $100,000

But before you place your bet, think of GMO as “the house” in the casino. By this I mean they’ve done a great job at calculating the odds of winning. They’ve been posting their forecast metrics out for many years and their accuracy rate is impressive at a high 0.93 (1.0 is a perfect correlation while -1.0 is a perfect non-correlation). No guarantee, of course. Just saying that in the geek world in which I live, 0.93 is really good. Put that calculation in the back of your mind as you place your chips on the table.

Hold on just one additional second. One last option for you to consider. My thinking is that sometime within the next several years, like times in the past, a correction will take place that will reset the opportunity deck and make forward equity returns good again. Think about the opportunity you had to buy equities in the summer of 2002 or late 2008. So add into the mix option #4:

- #4 GMO/Patience/Defense/Opportunity (pays 1 to 1 over two years then 2 to 1 over the remaining eight years: for overall odds of 2.14 to 1) – your $100,000 grows to $214,000 *(I took 0% over the next two years and then 10% for the remaining eight)

Ok – Step to the table and place your bet. My heart and wallet is hoping for #1 but to me the odds favor #4. That’s my bet. And I hope that my portfolio arrives at the opportunity with principal preserved. That’s the goal. A recession or rising interest rates or both will most certainly hit the popular 60-40 portfolio mix hard. No guarantees.

Early each month, I like to run through the latest valuation measures. Let’s do that today. We’ll take a look at various measures, including my favorite “Median PE”. We’ll also look to see what valuations might be telling us about 10-year forward return probabilities.

If you didn’t take note, go back and look at the chart above that shows the performance of the DJIA, S&P 500 and NASDAQ since 2000. The Dow performed best but take that 56.2% and divide it by 16.5 years. That equates to a compounded annualized return of approximately 3% (before inflation is calculated in). Also, take a look at that 1.8% gain in the NASDAQ. Recall that most of the money was flooding into technology stocks in the late 90s. 1.8% divided by 16.5 years is not so good and that is before inflation is considered.

If you are a CMG client, please note that we may be positioned in high yield bonds, government bonds, equities or seek the safety of treasury bills depending on an investment factor called “momentum.” For example, if you are invested in our CMG Opportunistic All Asset Strategy, you’ll note that we’ve seen technology ETFs showing strong relative price strength. I’m very bearish on high yield over the next several years yet our high yield trend following process has us invested in high yield funds today. Tactical strategies are based on price and trend activity. They do not consider whether the market is over or undervalued.

Because of the flexible nature, the ability to get defensive and the low buy-and-hold equity market return potential, I favor an overweight to tactical and other liquid alternative strategies. They can help balance the risks for upside potential with downside protection.

Grab that coffee and let’s take a quick look at the latest stock market valuations and what the numbers may tell us about forward return probabilities.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- The Q Ratio

- Median PE

- Taking The “E” Train South

- Trade Signals – Bond Market Risks, Zweig Bond Model a Buy, HY Weakening, Sentiment at Bullish Extreme, Gold Trend Positive, CMG Opportunistic All Asset Strategy 45% Equities/55% Fixed Income

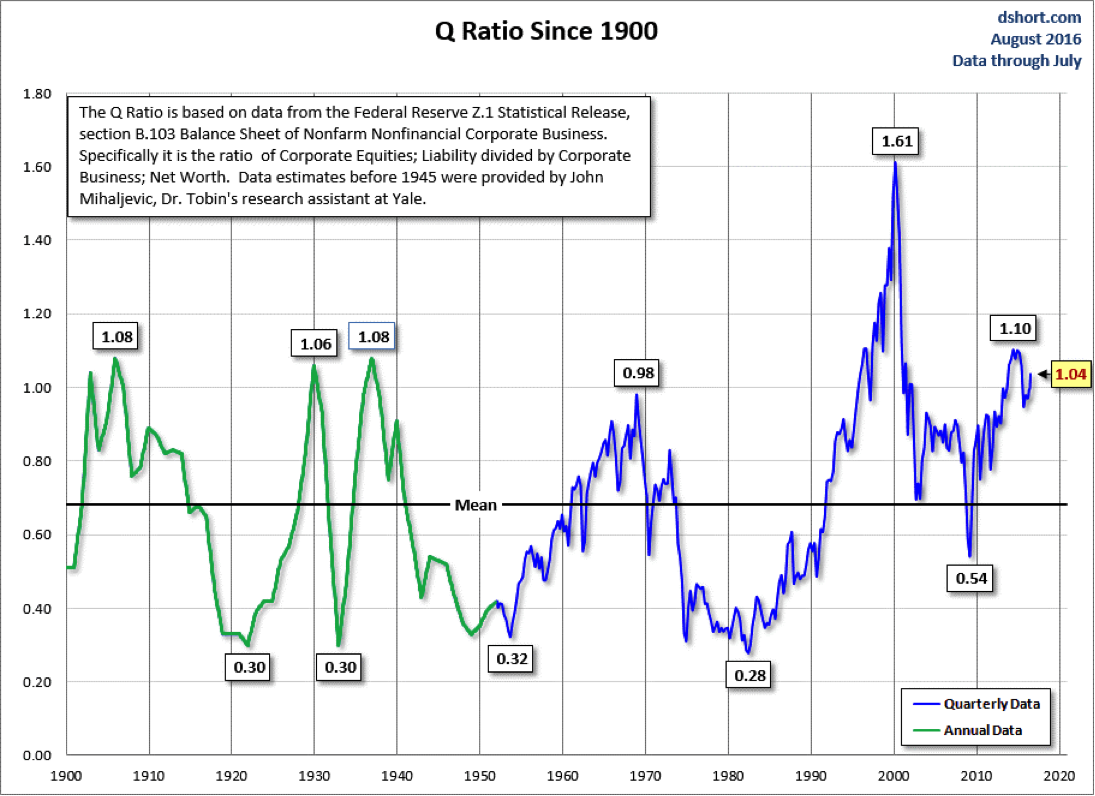

The Q Ratio

The Q Ratio is a popular method of estimating the fair value of the stock market developed by Nobel Laureate James Tobin. The Q Ratio is the total price of the market value divided by the replacement cost of all its companies.

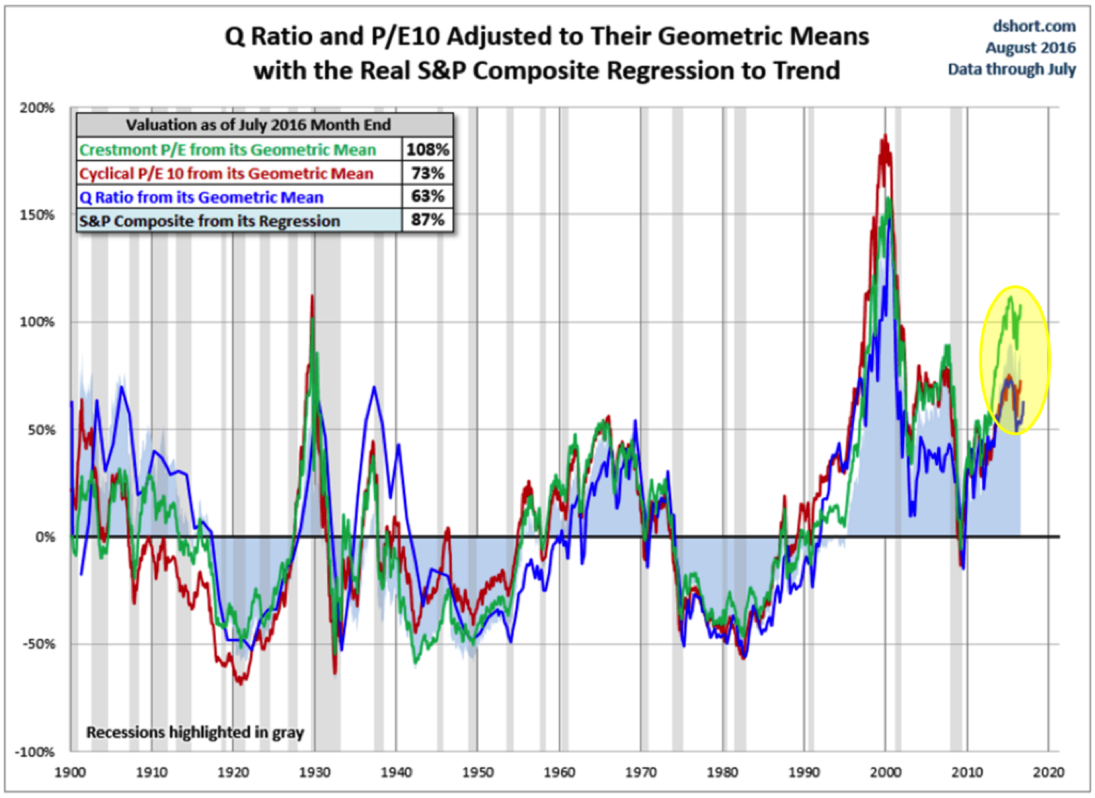

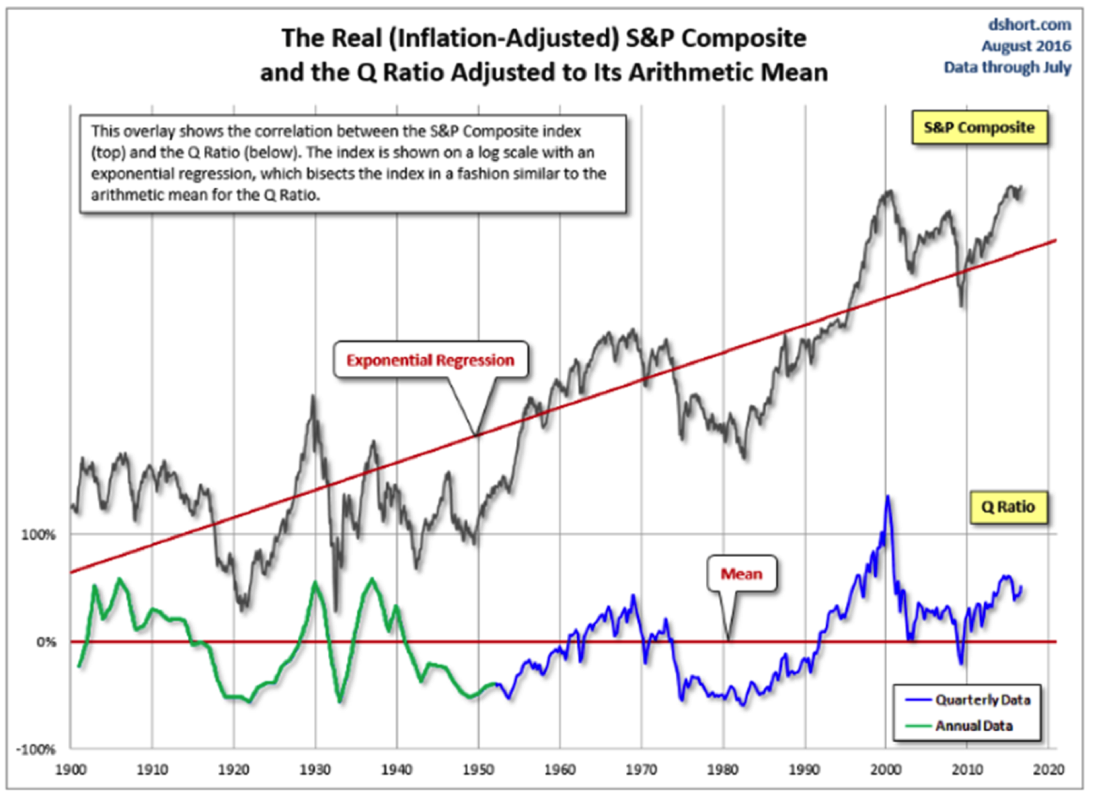

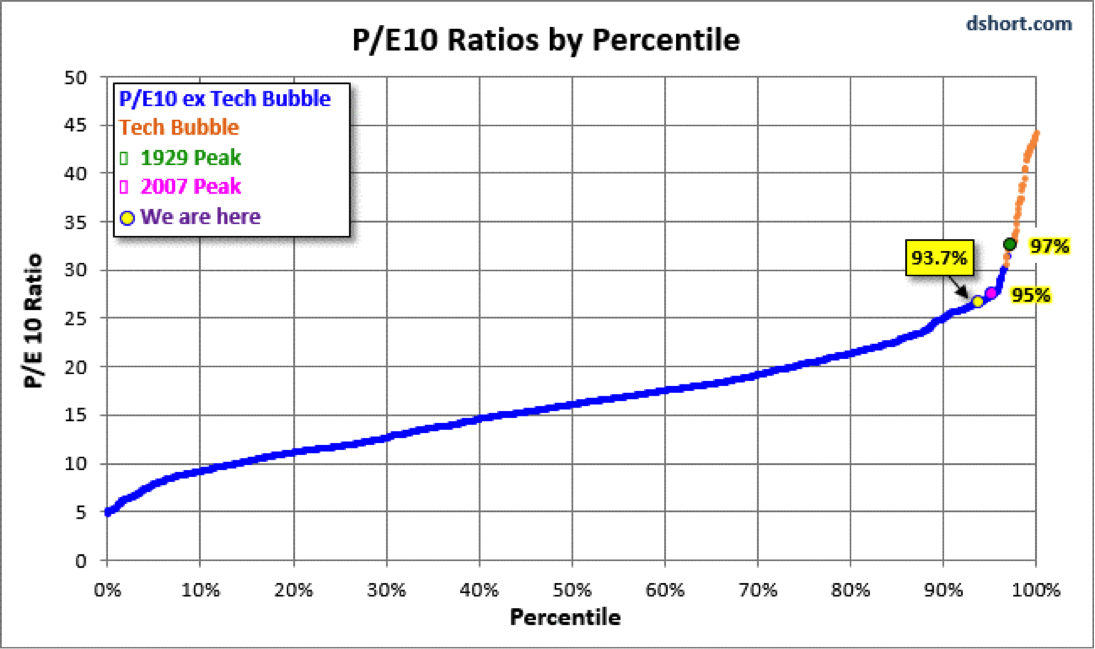

Note in the next few charts the current valuation measures (far right) vs. historical numbers. The quick conclusion is the market is expensively priced.

Next are three popular valuation measures. Shiller PE, Crestmont PE and the Q Ratio. Yellow circle is where we are today.

What this means in plain English: Markets move between overvaluation and undervaluation over time. When it gets too far from the norm, it tends to correct. Best to be an aggressive buyer when the ratio is below the red line in the next chart — cautious and hedged when above.

Is the stock market cheap? No. Click here.

Click here to learn more – source.

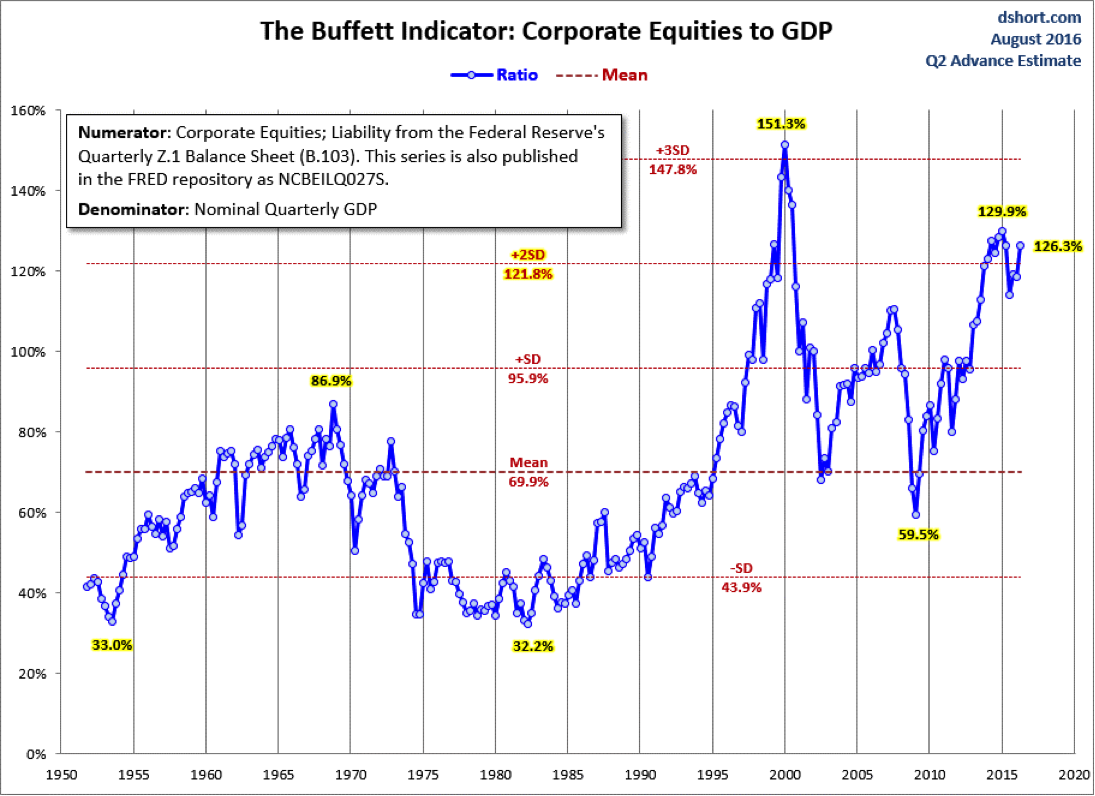

Here is the Buffett Valuation Indicator

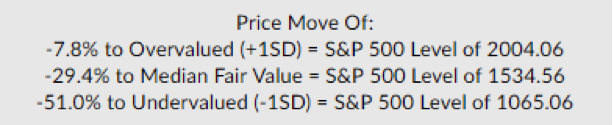

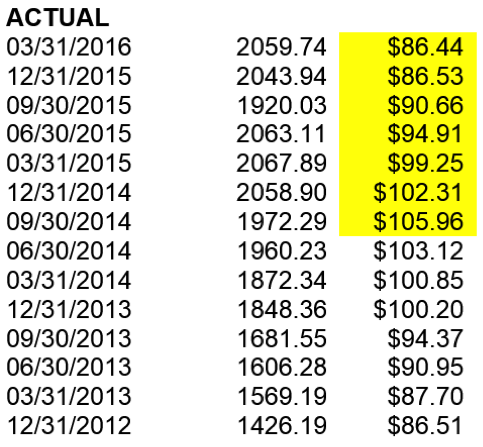

Median PE – Overvalued!

Median PE reached 24 at the end of July. I was surprised to see the number so high. If we consider the 52.4-year median of 16.9, fair value for the S&P 500 Index is 1534.56. With the index near 2175, it would need to decline 29.4% to get back to fair value.

Quants like to use the term Standard Deviation (SD) to explain extreme moves from a trend. If we look back over history (1964 to present), Median PE never breached a 1SD move until 1997. Think of 1SD as overvalued. By this valuation measure, the market is overvalued.

Source: NDR

What this means in regards to forward potential returns? A median PE of 24 puts the valuation level well into the overvalued zone. It puts the market in the most expensive 20% of monthly readings dating back to the 1950s. Past history advises us to expect annualized returns in the 2% to 4% range, before inflation, over the coming ten-years and I would anticipate a bumpy ride along the path to those low returns.

Either E (earnings) has to increase significantly or P (price) has to drop. What is overvalued can grow to become even more overvalued. The bigger picture is, I believe, a better entry point remains ahead.

Taking the “E” Train South

The “P” in the PE ratio stands for price. When the PE is high, it means the price is high relative to what stocks are currently earning. Over time, we want the companies we invest in to grow their earnings. Price should follow, but when P is high and the “E” (earnings) component is heading south, we need to be careful. It is important to note that PE is a very poor timing tool, yet is a very good forward return forecasting tool. Meaning it tells us little about returns over the short-term but much about returns over the longer-term.

What concerns me today is that the “E” train has been heading south. Six quarters in a row of a decline in S&P 500 index earnings. You may be hearing a lot about the current “earnings recession.” The following chart shows us what it looks like since 2012. Pay particular attention to the earnings decline over the last six quarters:

History tells us that past earnings declines have proceeded recession. In this way, the stock market is a leading economic indicator. That doesn’t mean the market can’t move higher. For now, the chase for yield remains in theme, yet we must not blink. It is unusual to see six quarters in a row of decline.

Concluding Thoughts

“In an experiment that will ultimately have disastrous consequences, the Federal Reserve’s policy of quantitative easing intentionally encouraged yield-seeking speculation in this cycle far beyond the point where these warning signals emerged.” John Hussman

I’m reminded of the reckless behavior of Greenspan prior to the 2007 financial crisis and his there is no real estate bubble, no irrational exuberance comments. In the Fed we place great trust. We should be careful! They have enabled an environment of extreme speculation.

Zero interest rate policy has caused investors to race into stocks with above average dividend yields and other high risk assets like junk bonds. They are seeking the perceived safety of dividends and reduced price volatility. I believe they will get just the opposite.

We will look back and identify this market as one of the most reckless financial bubbles of all time. We will look back and identify the next correction as one of the greatest buying opportunities of all time.

Investors are expecting their advisors to deliver 10% returns. There will be disappointment. A lot of money is going to be in motion. I favor a broad-based, holistic asset diversification. Include strategies that may gain in both bull and bear markets. Own some gold. Risk protect that equity exposure and stay tactical with your high yield bond exposure. Robo-like 60/40 is in trouble.

Trend Following Works! Learn more about trend following here. Ahead, I see it as a great opportunity for you and your business.

The “E” train will turn back north. It is best to hop on when prices are attractive. Until then, stay tactical and mindful of risk.

As a quick aside: I share a number of views on the markets and the global economy each week in On My Radar. If you are a CMG client, you may find that our current allocations may be invested in ETFs that may seem contrary to our macro view. For that reason, I wrote a piece called, “What On My Radar Means as it Relates to Our Investment Strategies and Your Clients’ Portfolios.” I hope you find it helpful.

Trade Signals – Bond Market Risks, Zweig Bond Model a Buy, HY Weakening, Sentiment at Bullish Extreme, Gold Trend Positive, CMG Opportunistic All Asset Strategy 45% Equities/55% Fixed Income

Click through to find the most recent Trade Signals. My favorite weight of evidence indicator, the CMG NDR Large Cap Momentum Index, remains in a sell signal. Trade Signals is posted each Wednesday. Here is a link to the Trade Signals blog page.

Personal Note

I hope your summer is going well.

I’m in NYC next Monday to meet with Barron’s and dinner follows with my friend John Mauldin. There is much to catch up on.

The beach follows August 13-20. Brie is coming down for the first weekend and Susan’s oldest boy Tyler is coming back from a grueling five weeks of training with the Navy. He is in ROTC at Cornell. What a kid. My youngest Kyle has been in the Colorado Rocky Mountains the last month and flies home next week. The gang is getting older and it is so much fun when we are all together. Let’s just say I’m not the first pick for the family beach volleyball team anymore.

I’ll be speaking on portfolio construction using ETFs at the Morningstar ETF Conference on September 7-9 in Chicago. Please let me know if you will be attending. Denver follows on September 13-15 where I’ll be attending a one day S&P Indexing Conference.

Wishing you and your family the very best! Relax. Have fun and don’t let the high valuations get you down. As Art Cashin says, “Stick with the drill – stay wary, alert and very, very nimble.”

If you find the On My Radar weekly research letter helpful, please tell a friend … they can sign up for the letter by clicking the “subscribe here” link that follows:

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal Chairman & CEO CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History:

Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Following are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

https://www.trademonster.com/marketing/upcomingWebinarEvents.action?src=TRADA2&PC=TRADA2&gclid=CKna3Puu6rwCFTRo7AodRiQAlw

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group