“Last week, market conditions joined the same tiny handful of extremes that defined the 1929, 1972, 1987, 2000 and 2007 market peaks.” – John P. Hussman, Ph.D. (Source)

At a recent investment conference, one of the panelists was an investment officer for the China Investment Corporation (CIC) – the Chinese sovereign wealth fund. She was particularly critical of the performance of their hedge fund managers. The CIC and others have been exiting their hedge fund investments. A common theme of late.

“The secret to my success is I buy when everyone else is selling and I sell when everyone else is buying,” said the great Sir John Templeton to me in 1985. He added, “If you can do that, you’ll be amongst the best in the business.” The contrarian in me just couldn’t help but to think back to that sage advice. It seems to me like we may be arriving at one of those points in time, Sir John. Just saying.

“Sell stocks and buy gold,” former hedge fund great Stan Druckenmiller says. We’ll likely look back and say that was a great call. But such concentration into one asset class is speculation, not investing, and besides who has got the guts and conviction to do that. Stan sure does. Though I do advise to own up to a 10% portfolio weighting to gold.

Stocks are richly priced and have been for several years. I suspect that negative interest rates in Europe and Japan will drive capital from there to here and further boost U.S. stocks and bonds. Who in their right mind could have imagined nearly $12 trillion in negative sovereign bond debt in much of the developed world? The unimaginable has happened. So we watch for global capital flows to flee Europe and come here.

There is no way a pension fund or insurance company can meet its 7.5% return mandate by buying negative yielding German bonds. They will shift out of sovereign debt and seek opportunity. Where are they going to go? They need yield.

U.S. bond and dividend yields are higher than they are in Europe and Japan. The capital market’s infrastructure is the best in the world. The U.S. economy is in ok shape. A sovereign debt crisis in Europe will cause money to seek a safer haven. So watch capital flows for clues. Watch the dollar for clues. And know that what is inflated in price could grow to be more inflated. But keep Sir John in the front of your mind.

This week let’s take a look at two research letters. One is from GMO’s Ben Inker. He talks about how returns have been pushed forward due to the unprecedented drop in interest rates. All assets with long durations (stocks, bonds, private equity, real estate, etc.) have benefited by the drop in interest rates to near zero. He used the following example to explain it:

Let’s say that you will need, with absolute certainty, $1 million in 2026. The safest way to reach that goal is to buy a $1 million face value 10-year zero coupon Treasury bond maturing in 2026. Such a bond currently has a yield of 1.625%, which means it will cost you $851,127 to buy it today. Assume that tomorrow the yield falls by 1% to 0.625%. Your brokerage statement will declare the value of your bond to be $939,596, a gain of over $88,000. Whoopee! You’ve just made over half of the necessary return over the next 10 years in a single day. But the value of that bond in 2026 has not changed at all. It has a fixed maturity value of $1 million. The only thing that has changed is the discount rate being applied to that cash flow, not the cash flow itself. Assuming you still need $1 million in 2026, there is no windfall to spend. Economically, nothing has changed for you, whatever your brokerage statement says.

Ben concludes that investors should expect low returns and it is time to allocate more money to alternatives. I concur.

The second letter is from John Hussman. I bet you know of him and may have had money invested in one of his funds. He is an active mutual fund manager but missed much of the post-2008 recovery rally. But don’t let that fog your goggles. He is bright and what he shares is important to keep on your radar.

Grab a coffee and find your favorite chair.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- The Duration Connection, by Ben Inker

- Speculative Extremes and Historically-Informed Optimism, by John P. Hussman, Ph.D.

- Trade Signals – Strength in Health Care, Telecom & Fixed Income

- A Few Photos from Lake George

The Duration Connection, by Ben Inker (footnotes omitted)

Ben explains the current situation we find ourselves in very well. Following is a quick summary of a few select points (emphasis mine):

- Over the last six or seven years, most financial assets have done very well. The performance divide has not been between low-risk assets and high-risk assets or between liquid assets and illiquid assets, but between long-duration assets and short-duration assets.

- Long-duration assets such as stocks, bonds, real estate, and private equity have benefitted from a large fall in the discount rate associated with their cash flows, while short-duration assets have been hurt by the same fall.

- Investors tend to tilt their portfolios in favor of those assets that have done well, and today that pushes them to be increasing effective duration in their portfolios, just when the potential returns to those assets have dropped.

- What we believe would be most helpful to investors are short-duration risk assets, as they offer the potential of decent returns over time with less vulnerability to rising discount rates.

- These assets, generally lumped together under the “alternatives” title, are generally out of favor today given their disappointing performance since the financial crisis, but the characteristics that made them disappoint may well prove a blessing if discount rates start to rise.

- Performance of most financial assets has been very strong, with assets from US equities to global real estate and infrastructure to credit and government bonds all giving strong returns.

- Even the laggards – non-US developed and emerging equities – have been disappointing on a relative, though not really an absolute basis.

- It isn’t all that often that everything does well at the same time.

- We have been conditioned to think of stocks and bonds as complements to each other, with one doing well when the other does poorly.

- In this cycle, we’ve gotten an almost magical benefit, where on a daily basis the correlations have been negative, but over the full seven years both assets have gone up strongly, along with most other assets.

- Apart from emerging equities, the only assets that have really disappointed seem to be commodities, cash, hedge funds, and other hedge-fund-like alternative assets and strategies.

- We believe there is a common factor that explains much of this. “Duration.”

- We believe further that it is important to realize that the strong returns to the assets that have done well over the last seven years are at best a one-off benefit and, more plausibly, will have to be given back over time.

- To us, this suggests that while alternatives have been a drag on institutional portfolios over the last six or seven years and privates (real estate, private equity, venture capital) have been a boost, in coming years the reverse may well be true.

Ben goes on to explain “The Duration Effect” – he shows a few really interesting charts but the general idea is that zero bound interest rates have brought forward returns we would have achieved over time to today. Investors forced into risk assets have bid up prices to lofty levels. Click here for the full piece.

Portfolio Implications

- Given this pattern, it is no surprise that many institutional clients are questioning their allocation to alternatives and increasing their allocation to private assets.

- The most shocking hole that will be blown through people’s portfolios is if discount rates rise again fairly quickly.

- Even if the circumstance is one in which the global economy is doing well, the impact of a 1.5% increase in the discount rate on equities from here is a fall of over 30%, which would almost certainly be enough to swamp the earnings impact of the decent growth.

- For bonds, of course, there would be no possible counter to the discount rate effect.

- For a portfolio that is fully invested in long-duration assets (i.e., consists of a combination of stocks, bonds, real estate, and private equity), the possible performance implication is on the order of the falls experienced in the financial crisis – perhaps a 20-33% fall depending on the weightings – despite the fact that the global economy was doing just fine.

So what can we do to protect portfolios against this possibility?

- One answer would be to hold cash, which, as a zero-duration asset, would be a beneficiary of rising discount rates. The trouble with cash, of course, is that if the discount rates do not rise, it is doomed to deliver little or nothing.

- What we would ideally like is to hold a short-duration risk asset – one where if nothing changes we are getting paid a decent return but where a rising discount rate will not destroy multiple years’ worth of returns.

- We believe alternatives fit the bill pretty well. If things hold together, we should expect to make money from activities such as merger arbitrage or exploiting carry trades or global macro.

- If the world does surprisingly well and causes investors to raise their expectations for discount rates, these strategies should be largely unaffected and could still make money.

- If we head into a severe recession or financial crisis, they will presumably lose money, as we saw in 2008, but that is no different from other risk assets.

- To be clear, I’m not arguing that the returns to alternatives are likely to be a lot higher than we have seen since 2009-10. Alternatives have been mildly disappointing since 2009, doing almost 1% worse than one might have expected.

- The more sobering truth is that the 4.2% return they have achieved since then simply looks pretty good given the other choices on offer, and

- Their lack of vulnerability to rising discount rates is a comfort in a world where almost everything in a traditional portfolio is acutely vulnerable to discount rate rises should they happen.

- Today does not look like a great opportunity to reach for risk, despite the temptation in the face of unprecedentedly unattractive yields on government debt.

Conclusion (bold emphasis mine)

The unwelcome truth is that there is not a tremendous amount investors can do about the fall in prospective returns. If the shift is permanent – the “Hell” scenario we’ve written of before – returns will be lower to all assets for which the discount rate has fallen, but at least the windfall gains will have to be repaid only very slowly. If the shift is temporary, we will wind up giving back the windfalls of the last six to seven years. The temporary shift scenario is better for investors in the long run, but it would be massively painful in the interim, because it will affect almost every asset in most investors’ portfolios.

The charm of alternatives today is that we believe they should perform similarly in either the temporary or permanent shift scenario, and there are almost no other assets with expected returns above cash for which that is the case. The problem with alternatives is that they are more complicated to manage than traditional assets, generally have higher fees associated with them, and require more oversight. Normally, those problems are enough to make them less appealing than traditional risk assets such as equities and credit. Today, however, they seem well worth the extra effort. Their generally disappointing performance over recent years, rather than a sign to dump them once and for all, should probably be recognized as a signal of their potential utility in the market environment we face in the coming years.

There is no panacea for the low returns implied by asset valuations today. Anyone suggesting differently is either fooling themselves or trying to fool you. But piling into the assets that have been the biggest help to portfolios over the past several years, as tempting as it may be, is probably an even worse idea than it usually is. And a deeper analysis of what led returns to be disappointing for the asset classes that have lagged may help investors avoid the error of abandoning decent assets just when their time may be about to come.”

Ben Inker is co-head of GMO’s Asset Allocation team and is a member of the GMO Board of Directors. In addition, he oversees the Developed Fixed Income team. He joined GMO in 1992 following the completion of his B.A. in Economics from Yale University. In his years at GMO, Mr. Inker has served as an analyst for the Quantitative Equity and Asset Allocation teams, as a portfolio manager of several equity and asset allocation portfolios, as co-head of International Quantitative Equities, and as CIO of Quantitative Developed Equities. He is a CFA charterholder.

Speculative Extremes and Historically-Informed Optimism, by John P. Hussman, Ph.D.

I share with you Hussman’s introduction and bullet point a few of his main ideas. Further below I provide a link to his full piece:

There’s a field in one of our data sets that rarely sees much play, being driven primarily by only the most extreme combination of overvaluation, overbullish sentiment, and overbought conditions we’ve identified across history. It’s one of a variety of such syndromes we track, and I’ve simply labeled it “Bubble,”because with a single exception, this extreme variant has only emerged just before the worst market collapses in the past century. Prior to the advance of recent years, the list of these instances was: August 1929, the week of the market peak; August 1972, after which the S&P 500 would advance about 7% by year-end, and then drop by half; August 1987, the week of the market peak; March 2000, the week of the market peak; and July 2007, within a few points of the final peak in the S&P 500, with a secondary signal in October 2007, the week of that final market peak.

John adds that this cycle has a unique characteristic:

- “In an experiment that will ultimately have disastrous consequences, the Federal Reserve’s policy of quantitative easing intentionally encouraged yield-seeking speculation in this cycle far beyond the point where these warning signals emerged.”

In a series of signals between late-2013 and the beginning of 2014, that rare “Bubble” signal emerged again. This time, however, it was accompanied by quantitative easing, a Treasury bill yield averaging just 0.03%, and uniform market internals across a broad range of individual stocks, industries, sectors, and security types (when investors are inclined to speculate, they tend to be indiscriminate about it). The S&P 500 retreated, but by just 3%, followed by an advance for several more months until market internals deteriorated early in the second-half of 2014. Since then, the broad market has essentially gone sideways, though capitalization-weighted indices such as the S&P 500 have recently clawed to new highs on enthusiasm about negative interest rates abroad (which I believe actually reflect fresh deterioration in global economic conditions across Britain, Europe, Japan, and China).

Last week, market conditions joined the same tiny handful of extremes that defined the 1929, 1972, 1987, 2000 and 2007 market peaks. Still, the false signal near the start of 2014 (and lesser extremes before then), helpless in the face of single basis-point Treasury bill yields and uniform market internals, encourages a certain level of humility and flexibility.

Here are a few more bullet points in an attempt to give you the digest version though you can find the full piece here.

- First, regardless of short-term speculation, the present yield-seeking speculative extreme is likely to be seen in hindsight as one of the three most reckless financial bubbles in U.S. history, on par with the 1929 and 2000 extremes.

- The present market cycle is likely to be completed by a collapse where a wholly run-of-the-mill outcome would be a decline of 40-55% in the S&P 500 Index.

- On the basis of valuation measures most tightly related to actual subsequent long-term market returns, we also estimate that the S&P 500 is likely to be lower 12 years from now, compared with current levels, though dividend income may push the total return just over zero on that horizon. We view all of these outcomes as unavoidably baked-in-the-cake as a consequence of current extremes.

- Despite this outlook, the uncomfortable possibility of further short-term speculation still exists. The extent to which we make that allowance is dependent on market internals and interest rate conditions.

- For now, they remain less supportive than speculators may imagine. As I detailed several months ago in Reversing the Speculative Effect of QE Overnight, moving the target Federal Funds rate from zero to 0.25% quietly (and perhaps inadvertently) had an effect that is observationally-equivalent to removing $1.7 trillion from the Federal Reserve’s balance sheet, back to where it was in 2009.

- A return to a zero target by the Fed would create greater pressure to speculate than remains at present.

- As for market action, despite record highs in capitalization-weighted indices, the broad market has had less traction, particularly since mid-2014.

- A more uniform improvement in market internals (reflecting indiscriminate speculation) could signal more durable risk-seeking among investors.

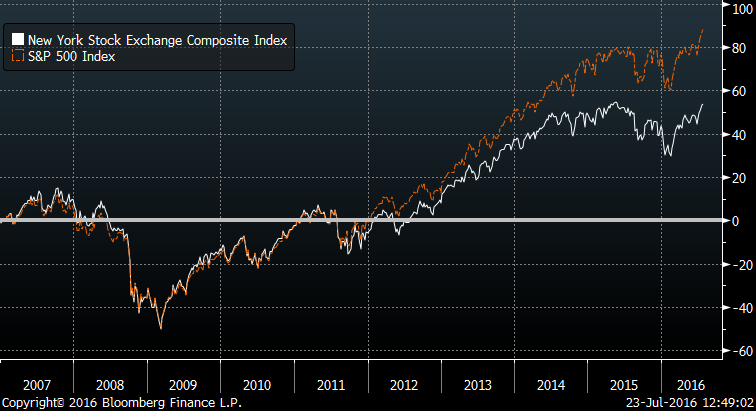

- The chart below shows the behavior of the broad-based NYSE Composite versus the S&P 500 Index (which has been more heavily driven by speculative, large-cap components). The performance gap that has blown out between these two indices is not just an indication of dispersion, but particularly since mid-2014, has also been a major, if temporary, headwind for hedged-equity strategies that hold a broadly diversified portfolio of stocks and hedge using the major indices.

Ok. The market is richly priced. Bubble! Trouble? After writing and then re-reading the above, I set out to find some peace. And I found this…

Some good advice…

Concluding Thoughts

I find myself in the “money is going to race to the U.S.” camp. Most cyclical bull market peaks end in mass speculation. Recall tech in early 2000 or real estate in 2007. The mother of all bubbles is in the bond market and, well, stocks just don’t do as well in rising interest rate environments. We haven’t seen such mania yet. And we may not.

Markets move from cyclical bull to cyclical bear and back again. To me, it feels a bit like a game of musical chairs. We all think we can get that last chair. We all think we can get out of the market in time. The reality is the odds are not so good. What is clear is that a better high probability buying opportunity is ahead. Just not yet.

Someone is going to call the next move right. My money is on Stan but he’ll tell you it is a probability game and he may quickly change course. He is one of the great hedge fund investors of all time. Am I right on a capital flight to U.S. stocks? I wouldn’t bet the whole bank on it.

Investing is different. It is about trying to achieve a particular return relative to a risk that is acceptable to you. Modern portfolio theory… The efficient frontier… Diversification.

I favor owning equities but hedged. The cost of downside protection is worth the price. Think of it like fire insurance on your house and hope you never need it. Diversify to other asset classes. Find a global macro manager, a managed futures manager and tactical go anywhere strategy. Allocate to more than one.

This adds an additional hedge and potential return drivers to your portfolio. For now, I favor underweighting equities, underweighting fixed income and overweighting tactical and liquid alternatives.

The plan this week was to talk about China’s recent currency devaluation. Here is a quick note: Their move seems to have gone unnoticed. Recall the last two times China devalued, U.S. stocks fell over 10%. Worth watching.

China is struggling under the weight of too much debt, poor demographics and competition from lower priced suppliers in Vietnam, Indonesia and the Philippines. China needs economic relief. So does Europe and Japan for that matter. The easiest way to give the Chinese economy a boost is to cheapen its currency, the yuan, to make its exports more competitive. Currency Wars remain in play. Keep this on your radar.

As a quick aside: I share a number of views on the markets and the global economy each week in On My Radar. If you are a CMG client, you may find that our current allocations may be invested in ETFs that may seem contrary to our macro view. For that reason, I wrote a piece called, “What On My Radar Means as it Relates to Our Investment Strategies and Your Clients’ Portfolios.” I hope you find it helpful.

Trade Signals – Strength in Health Care, Telecom & Fixed Income

Click through to find the most recent Trade Signals. My favorite weight of evidence indicator, the CMG NDR Large Cap Momentum Index, remains in a sell signal. Trade Signals is posted each Wednesday. Here is a link to the Trade Signals blog page.

Personal Note – Lake George

I’m in Lake George, New York with Susan and our children at her brother Jim and his wife Maureen’s home. As you can see next, what a place!

Brianna is taking the train up from NYC and we’ll pick her up later this afternoon. Time with family – priceless! Fun time on the lake remains ahead. I’m a lucky man.

Some needed downtime is planned for mid-August. We’ve rented a house in Stone Harbor, New Jersey. I’ll be speaking on portfolio construction using ETFs at the Morningstar ETF Conference on September 7-9 in Chicago. Please let me know if you will be attending. I’d love to grab a coffee. Denver follows on September 13-15 where I’ll be attending the S&P Indexing Conference.

Wishing you and your family the very best!

If you find the On My Radar weekly research letter helpful, please tell a friend … they can sign up for the letter by clicking the “subscribe here” link that follows:

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal Chairman & CEO CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History:

Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Following are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group

© CMG Capital Management Group