Ginnie Mae mortgage-backed securities are popular, but these government backed bonds aren’t risk-free. For less prepayment risk and superior total return potential, investors may be better served by turning to Fannie and Freddie.

Government National Mortgage Association mortgage-backed securities (Ginnie Mae MBS) are direct obligations of the federal government — meaning the full and timely payment of principal and interest is guaranteed. But Ginnie Mae MBS are vulnerable to the biggest risk an MBS portfolio faces in a low interest rate environment — prepayments. Investors may not realize that Ginnie Mae mortgages tend to prepay at faster speeds than conventional mortgage-backed securities. In fact, conventional MBS — issued and guaranteed by the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac) — offer less prepayment risk and more attractive total return opportunities.

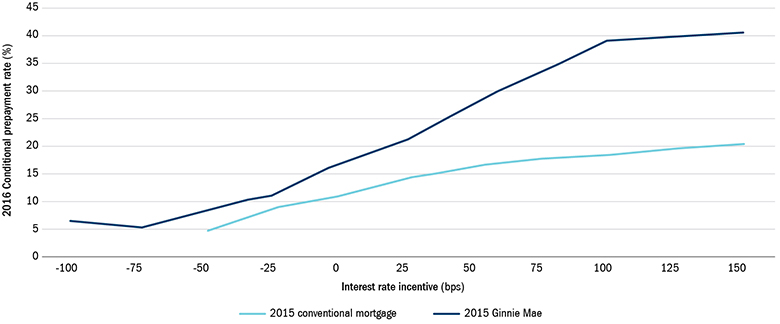

Prepayment risk: faster and higher with Ginnie Mae

Ginnie Mae mortgages are prepaid more frequently because they have lower up-front costs and are part of an efficient, streamlined refinancing program. Also, borrowers can easily roll their closing costs into a Ginnie Mae mortgage, which lowers the effective mortgage rate. The problem with prepayment activity is that investors in the underlying pool of MBS receive their principal back sooner than expected and must reinvest at lower current interest rates.

The graph below depicts the speed with which loans prepay in both Ginnie Mae MBS and conventional MBS. As rates move lower and the incentive to refinance initially increases, the conditional prepayment rate — prepayments represented as a percent of current outstanding loan balance — accelerates more rapidly among Ginnie Mae mortgages than conventional mortgages. As a result, Ginnie Mae MBS are more sensitive to interest rate changes than conventional MBS.

Lower interest rates expose Ginnie Mae prepayment risk

Source: Citigroup. 03/16-05/16 conditional prepayment rate for mortgage pools issued 03/15-08/15.

Higher prices, lower yields: a double whammy

Faster prepayments in the current environment reduce the theoretical valuation (fair market value) of MBS because investors are receiving cash flows earlier than expected and forced to reinvest at lower yields. Given today’s prepayment risk, Ginnie Mae MBS should actually be priced 1 point ($1.00) lower than conventional MBS. In fact, Ginnie Maes are priced $0.75higher. The net result is a market value that is, in our estimation, 1.75 points ($1.75) overpriced. But that’s not all. Faster prepayment speeds and higher prices result in lower yields compared to conventional MBS with similar maturity and coupon profiles — to the tune of 35 basis points (bps), or 0.35% lower.

Given this unflattering profile, what is driving demand for Ginnie Mae MBS to keep these high prices afloat? The answer is regulation. After the 2008 financial crisis, regulations and bank capital rules were enacted that impose rigid investment restrictions on certain market participants such as U.S. and Asian banks. These rules provide favorable treatment of Ginnie Mae MBS on bank balance sheets, giving these banks a non-economic incentive to invest in Ginnie Mae MBS over conventional MBS.

Ginnie Mae prepayment risk could go even higher

Based on conversations with housing regulators and legislators, we believe there could be meaningful changes ahead for Ginnie Mae MBS. As Tom Heuer, Senior Portfolio Manager on the Structured Assets Team explains, those changes could reduce the risk premium for credit-impaired borrowers and increase prepayment activity in Ginnie Mae MBS. Mortgage insurance premiums (MIPs) for less qualified homebuyers had been increasing from 2008 to 2013 as a way to help the Federal Housing Authority (FHA) meet its 2% statutory reserve requirement. According to the FHA’s 2015 annual report, the 2% requirement has been met, which means that MIPs, which were cut by 50 bps in 2013, could be reduced again. Another cut would incentivize current Ginnie Mae mortgagors to refinance at lower MIPs, thereby lowering the available mortgage rate and raising prepayment risk for Ginnie Mae MBS investors.

The bottom line

Conventional MBS offer an effective government guarantee, less prepayment risk and higher yields at lower prices than Ginnie Mae MBS. In addition, future housing regulatory changes could further elevate prepayment risk in Ginnie Mae MBS. For investors concerned about relative value in agency MBS, consider rotating out of Ginnie Mae MBS and into conventional MBS for a more attractive total return profile.

© Columbia Threadneedle Investments

© Columbia Threadneedle Investments