|

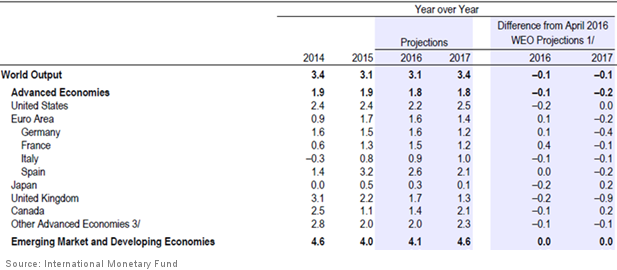

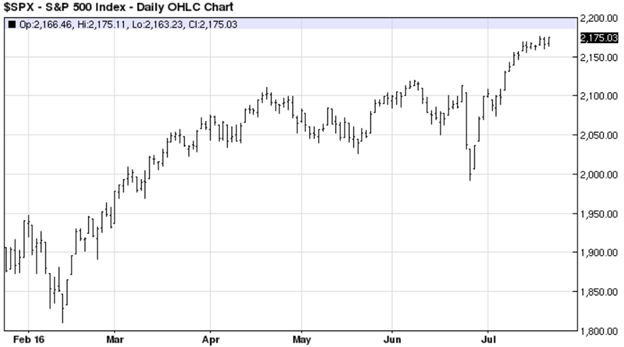

IN THIS ISSUE: 1. IMF Cuts 2016/2017 World Growth Forecast, But Not Much 2. More Highlights From the IMF’s Global Growth Forecasts 3. Foreign Investors Flock to US Securities Amid Global Uncertainties IMF Cuts 2016/2017 World Growth Forecast, But Not Much Last Tuesday, the International Monetary Fund (IMF) released its latest quarterly “Global Growth Forecasts” which I will summarize below. Before we get into those, I should note that the IMF had been one of the most outspoken critics of “Brexit” ahead of the surprising UK vote on June 23. Specifically, the IMF warned that a Brexit vote would lead to “severe regional and global damage.” In light of this and other repeated dire warnings ahead of the vote, most analysts expected a significant downward revision to the IMF’s latest forecast for global growth. That didn’t happen. The IMF’s latest forecast puts global growth in 2016 at 3.1%, down only 0.1% from its April estimate of 3.2%. For 2017, the IMF again reduced its previous forecast by only 0.1% to 3.4% from 3.5% in April. The IMF did revise downward its growth forecast for the United Kingdom, but again not as much as was widely expected. The latest forecast puts UK growth in 2016 at 1.7%, down only 0.2% from its April estimate. For 2017 the IMF forecasts growth of 1.3%, down 0.9% from its April estimate of 2.2%. Despite its alarming rhetoric ahead of the Brexit vote, the IMF now does not expect a recession in the UK this year or next. This came as quite a surprise to many. The IMF emphasized that the above forecasts are based on the UK striking a deal with the EU that avoids a large increase in economic barriers, as well as no further major financial market disruption and limited political fallout. However, in a worst-case scenario, the IMF warned that many European-based companies that also have operations in the UK could close or relocate to other EU countries from the UK. This would hurt consumption and investment – possibly leading to a UK recession by early 2017. But the IMF was clear that this is not the most likely outcome as a result of Brexit. The IMF’s new forecasts for continental Europe were also not nearly as dire as expected. The IMF had warned that Brexit would be very negative for the European Union (EU) countries, yet the latest forecasts were actually better than expected in some cases. The latest IMF forecast has Germany growing by 1.6% in 2016, an increase of 0.1% from its April forecast, and 1.2% in 2017, down 0.4%. The latest forecast has France growing by 1.5% in 2016, an increase of 0.4% from its April forecast, and 1.2% in 2017, down 0.1%. The new forecast for Italy is for growth of 0.9%in 2016, down 0.1%, and 1.0% in 2017, down 0.1% from April’s forecast. For the 19-country Euro Area as a whole, the IMF predicts growth of 1.6% in 2016, up 0.1% from its April reading, and 1.4% in 2017, down 0.2% from the previous estimate. The IMF left its latest estimates for Emerging Market and Developing Economies unchanged at 4.1% for 2016 and 4.6% for 2017. The point is, the latest forecasts from the International Monetary Fund were not nearly as bad as most analysts had expected, and some were actually increased from the April report.

Many analysts concluded in late June that the IMF had been “bluffing” about the dire consequences of a Brexit vote. In its own defense, the IMF claimed that it was prepared to increase its Global Growth Forecasts slightly as of June 22 (the day before the Brexit vote). The IMF said:

So if the IMF is to be believed, the revision in global growth from 3.2% to 3.1% for 2016 is actually worse than it looks, since they had planned to increase the number prior to the Brexit vote. I’m not sure I’m buying that story. More Highlights From the IMF’s Global Growth Forecasts The IMF forecasts US economic growth of only 2.2% in 2016, down 0.2% from the April estimate, with growth of 2.5% in 2017, unchanged from its previous estimate. The IMF cited weaker than expected growth in the 1Q as the basis for the 2016 downgrade. China’s forecast remained almost unchanged, with growth of 6.6% (+0.1%) in 2016 and 6.2% (unchanged) in 2017. The IMF noted that Brexit fallout is likely to be muted for China, the world’s second-largest economy, because of its limited trade and financial links with the UK. However, should growth in the European Union be affected significantly, the adverse effect on China could be material, the IMF cautioned. The IMF upgraded its forecast for Russia and Brazil, both of which are in recession again this year. The IMF projects the Russian economy will contract by 1.2% in 2016 versus its April estimate of -1.7%, following -3.7% in 2015. Brazil is expected to contract by 3.3% in 2016 as compared to -3.8% in the earlier estimate, and move out of recession in 2017 at 0.5% growth. That remains to be seen. While the latest forecasts from the IMF were not as bad as many analysts expected, the Fund cautioned, as usual, that there are still global risks which could render their outlook off the mark. In addition to Brexit, the IMF cited serious ongoing problems in European banks, in particular Italy and Portugal. The IMF also cautioned that geopolitical tensions and terrorism are also taking a heavy toll on the outlook in several economies, especially in the Middle East, with further cross border ramifications. They also warned that protectionist policies are likely to arise in developed nations in response to the ongoing refugee crisis, which has no end in sight. The bottom line is that Brexit has so far not been as disruptive as the IMF imagined, and the latest revisions were not as negative as expected. Yet the IMF maintains that the world remains a dangerous place overall. I agree. Foreign Investors Flock to US Securities Amid Global Uncertainties While equity markets around the world reacted negatively in the first few days after the Brexit surprise on June 23, US stocks reversed higher in late June and cruised to new all-time record highs. Some are calling it a “market melt-up.”

In the wake of Brexit, foreign investors have been buying US Treasuries, and to a lesser degree US equities, with abandon. While the initial negative reaction to Brexit may have been overdone, the longer-term risks of Brexit remain. For one, it remains to be seen how quickly or slowly Britain’s new Prime Minister Theresa May will move forward in implementing Brexit, which is a huge uncertainty. Yet the biggest uncertainty is whether or not any other European nations will vote to exit the EU. Most of the sources I read agree that the answer is when, not if. There are several countries in Europe that are believed to be contemplating holding a national referendum on whether to remain in the EU. A leading candidate is France, which could be the death blow for the EU. The leading candidate to become France’s next leader, Marine Le Pen of the far-right National Front Party, vows to hold a national referendum if she becomes president in April. While fears of the UK’s exit from the EU may have been overblown, especially by those who wanted to “remain,” the thought of other countries leaving raises the possibility that the EU and the euro could cease to exist. If so, that will be very unsettling for global financial markets and volatility could rise to unprecedented levels. European banks are undergoing a real life stress-test in the wake of Britain’s vote to leave the European Union. Their share prices were already down 20% this year; since Brexit, they’ve doubled that decline. If the rout isn’t stopped soon, many European banks may shrink to the point they can no longer remain in business. UniCredit, Italy's biggest bank, has suffered particularly badly this year. It has a market capitalization of just 12 billion euros, dwarfed by its non-performing loans valued at 51 billion euros on paper. Italian banks as a whole have non-performing debts worth 198 billion euros. A full-blown banking crisis could erupt in Italy any day now. These are just a sampling of the global risks out there today, not to mention negative interest rates in many parts of the world. As a result, foreign investors are flocking to the safety of US dollar denominated securities including Treasury notes and bonds and US equities to a lesser extent. This is a big reason why US stock indexes are at new record highs. Investing in US stocks today, and for that matter Treasuries as well, is a high-risk decision. There is broad agreement that US stocks are over-valued. With Treasury yields hitting all-time record lows earlier this month, bond prices are similarly over-valued. So why are foreign investors flocking to buy these securities? Global investors are desperate for yield. So are US investors. Wishing you profits with lower risk, Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent. |

| © Halbert Wealth Management |