The economic data arriving this week and next will help to solidify the near-term outlook for growth and monetary policy. There are almost certainly going to be surprises along the way and the financial markets have a tendency to over-react. However, it’s likely that the figures will remain consistent with moderate economic growth.

GDP is a quarterly figure, but every month has a GDP estimate. First comes the advance estimate, with is based on incomplete information, followed by the 2ndestimate a month later and the 3rd estimate a month after that. Data on foreign trade and inventories has been missing in the advance estimate, a major uncertainty for those trying to forecast the growth figure -- but that changes this week. The Bureau of Census will release June import and export data (goods only) and estimates of June wholesale and retail inventories. These figures are subject to later revisions, but they should get us a step closer to the initial estimate. Still, many uncertainties remain.

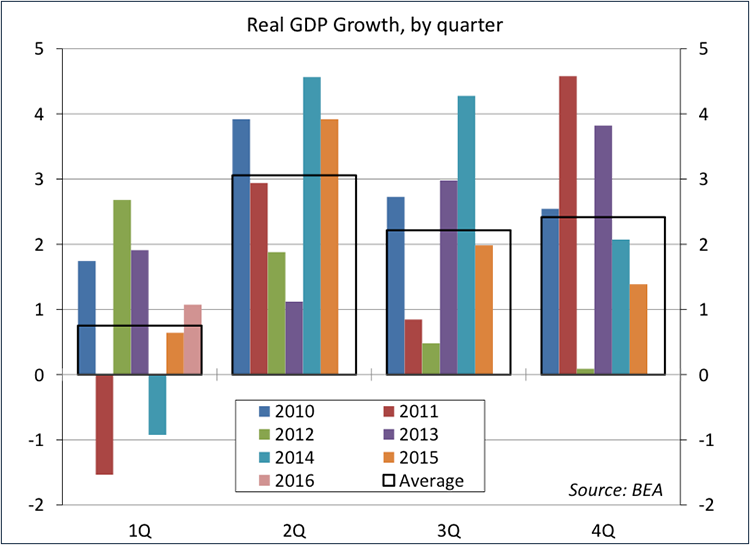

Once a year, almost always in late July, the Bureau of Economic Analysis releases benchmark revisions. This year, that is a “garden-variety” benchmark, based on updated component data, with no major changes to the methodology. In recent years, first quarter GDP growth figures have tended to be a lot lower than in the rest of the year, suggesting that something may be wrong with the seasonal adjustment (this is called “residual seasonality”). Problems with the seasonal adjustment will eventually take care of themselves. That is, over time, a change in the seasonal pattern will become incorporated in the seasonal adjustment. We can expect to see a reduced seasonal pattern in adjusted benchmark data this week, but some residual seasonality is likely to remain. The BEA is working to address seasonal adjustment issues and will begin publishing unadjusted GDP figures for the first time beginning in mid-2018.

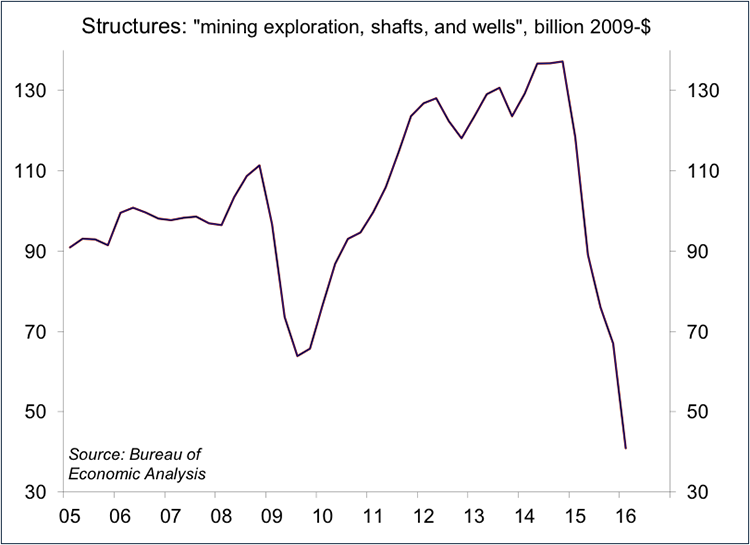

A large drop in oil prices, as occurred in the 1980s has often provided a boost to GDP growth. Spending less to fill their gas tanks, consumers have more money to spend on other things. However, following the rise of domestic oil production, a drop in oil prices also has a negative impact. The loss of well-paying energy-related jobs is a serious setback for many areas of the country. Yet, at its peak, oil and gas well drilling accounted for only a small portion of total nonfarm payrolls. The greater impact (in terms of GDP growth) has been in business fixed investment. Energy exploration is capital-intensive. In nominal terms, business fixed investment rose 0.5% from 4Q14 to 1Q16, but would have risen 5.5% if not for the contraction in “mining equipment, shafts, and wells.” Importantly, the contraction in energy-related capital spending won’t last forever, and we shouldn’t see an ongoing drag on business fixed investment (and overall growth) in the coming quarters.

Outside of the energy sector, business fixed investment has been soft. Benchmark revisions are expected to show slower capital spending than was reported earlier, but this is more consistent with a slow patch rather than an outright recession.

Despite choppiness in May and June, job growth remains moderately strong, albeit at a slower trend than in the last two years. Employment gains should continue to support consumer spending growth through the remainder of the year. In the early stages of an economic recovery one normally sees rebounds in construction and manufacturing jobs (higher paying), but that was never going to happen this time. Retail and leisure jobs (lower paying) typically get hit hard in the downturn and snap back quickly. In recent years, job gains have been broader based, with strength in professional and business services. Business formation was hit hard in the downturn, but is picking up. Consumer spending growth should therefore remain at a moderately strong pace in the near term.