“The best thing we can do is get back to pricing risk.

Getting to that point should be and will be painful.”

— PJ Grzywacz, President, CMG Capital Management Group“Central banks don’t like being the only game in town,

but they don’t know how to get out of it.”

— Mohamed A. El-Erian, Chief Economic Adviser, Allianz“If I had gone to people four years ago and said, ‘Forty percent of the world’s sovereign bonds would be at negative rates (even 40 percent of corporate bonds now in Europe are coming out at negative rates), central banks would expand their balance sheets $10 trillion, and that the world would somewhat look normal, with all of the geopolitical risks that we have with ISIS, etc.,’ people would have said, ‘John, what are you thinking?’ And yet all of those unthinkable things have come about.”

— John Mauldin, Chairman, Mauldin Economics“Suffering comes from having an argument with reality.”

— Buddhist proverb

Our team spends a great deal of time debating the economic outlook and to say PJ Grzywacz is bright would be an understatement. Sometimes our discussions get passionate and I think it is a good thing. To wit, passion in everything is a good thing. PJ challenges all things that might lead to “groupthink” biases. Something we think about a lot.

Over the last several weeks, I’ve been sharing my notes from Mauldin’s Strategic Investment Conference held in Dallas in late May. In groupthink terms, the overall tone was bearish. Debt, deflation and demographics remain a challenge. Rosenberg, Grant, Shilling, Hunt, Yusko, Friedman, Fisher and Mauldin are all in the bear camp.

Geopolitical strategist George Friedman titled his presentation, “The World is Going to Hell…But We’re OK.” Relatively speaking, North America is in good shape. I share with you my notes from his presentation in fast-paced bullet point form. Former Dallas Fed President, Richard Fisher said that most of the people he knows have a sizable portion of their assets in cash. Asked what position his portfolio is in, he responded, “The fetal position.”

Perhaps this is what his friends are seeing:

“The artificially high asset prices caused by zero interest rates and central bank purchases have created what El-Erian calls liquidity delusion. Investors, he warns, should be prepared for increased volatility as a result of the divergence in policy between the Federal Reserve and the European Central Bank, the Bank of Japan and the People’s Bank of China. Volatility will lead to patches of illiquidity that will accentuate volatility.

But all is not lost, El-Erian says. The key for investors is to remain very nimble and take advantage of volatility when asset prices overshoot. He suggests treating cash as part of the strategic allocation of a diversified portfolio — advice the long-time investor has put into practice for himself. El-Erian has had the bulk of his money in cash since last spring.” From Michael Peltz, Editor, InstitutionalInvestors.com (January 2016).

Today, I share the last of my notes from the conference. Keep the concept of “groupthink” in the back of your mind. Not all were bearish. Though it seems our collective hope rests on coordinated central bank policy at the same time our fiscal authorities get their acts together. Wishful? I’m not holding my breath.

Fisher was critical of Yellen yet clear that the Fed knows what it needs to do. I found his presentation particularly interesting. Finally, let’s conclude today’s piece by taking a look at the most recent valuation metrics. You’ll see they are higher than in 2007 and pretty much any period of time with the exception of the late 1990’s and early 2000’s.

Grab that coffee, find your favorite seat and dive in.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- George Friedman – Geopolitical Strategist

- Richard Fisher – Former Dallas Fed President

- Concluding Thoughts – Pippa, Mauldin and Ferguson

- A Quick Look at Valuations (They Remain High)

- Trade Signals – Nearing an All-Time High

- What You Can Do

George Friedman – Geopolitical Strategist

George Friedman is an internationally recognized geopolitical forecaster and strategist on international affairs. Following are my notes from the Strategic Investment Conference in bullet point format. Friedman’s presentation is entitled, “The World Is Going to Hell…But We’re OK” (I know… what a start).

- Eurasia – 5 billion of the 7 billion people alive today live in this area.

- They are going through a period of massive destabilization.

- He sees a coming crisis in Germany and believes an Italian banking crisis is up next.

- Russia is building military forces as rapidly as it can.

- 50% of the Russian budget relies on oil.

- We have a country with 2,000 nuclear missiles that is destabilizing now.

- China is like Japan in 1989 (economically).

- Middle East – in a word “disintegrating.”

- The entire Eurasia land mass is in a state of failure. Money is surging out of this area.

- The heartland of humanity is destabilized.

- Yet at the same time, North America is in good shape.

- Mexico has emerged as the world’s 11th largest economy.

- On the U.S. he noted the following – Lehman Brothers collapse was the 4th devastating crisis since 1972.

- We’ve had the S&L crisis (early 1990s), muni crisis, foreign debt crisis and Lehman (SB here: though I’d put Long-Term Capital Management in the mix).

- Noting when crisis happens in the U.S., “we get all the players in one room and we fix it.”

- “We wipe out a bunch of investors. We’ve invented things before to bail us out and we’ll do it again.”

- “That doesn’t happen in Europe. There is no structure in Europe. They are not set up to deal with crisis.”

- So Europe poses a large geopolitical risk.

- Then there is Russia. When Russia invaded Georgia, they announced to the world, “We are back.” With several “lines in the sand” since crossed, he believes the U.S. has effectively said to many of its allies “we do not have your back.” He added, “We are not in the business of being the world’s nanny anymore.”

- When Europeans ask him, doesn’t Obama understand our problems? George answers, “Yes… he just doesn’t care.” (SB here: Ugh on that quote).

- He believes our current financial crisis is manageable as the U.S. is rich in assets and largely self-sufficient (especially with growing energy independence); this, despite our debt and entitlement problems.

- On China – China was purposefully built as an export model. The future of an exporting country depends on the willingness for its customers to buy. When the world broke, the Chinese exporters failed.

- If you live in a country earning $2 per day, you cannot buy an iPad. China has to have exports to pay the loans that the banks have made. When your exports go south – expect bad loans (defaults).

- By 2011, it was much cheaper to produce in Mexico, Vietnam and Singapore. China lost its competitive edge. It was evident then that China was not in good shape.

- China recently arrested 300 people that work in the government’s statistics department – they have now admitted that the numbers they report have been false.

- It is now evident the “Chinese miracle” has popped. The engine that drove much of the global commodity growth tanked. As we’ve seen in commodity prices like oil, copper, etc.

- We have not seen such a universal pattern since 1942. This is not the 1970s and not the 1990s.

- SB here: scary thought, yet Friedman added, “To be clear, I do not see a World War III.” Speaking geopolitically, he added, “But we are not in the global model we were in prior to 2008.”

- Five of seven billion people are living in zones in crisis.

- Globally, we have a very real export crisis fueled by a lack of customers willing to buy.

- On Italian banking crisis – he said, “18% of the loans are reported as non-performing.” He is pretty certain that it is worse than 18%. Germany owns a lot of that debt. There is nothing that indicates the Italians can re-right themselves.

- Most of the Italian debt is corporate debt. Most of the debt is owned by EU investors. Portugal has entered the picture.

- The crisis is not over. It has been put on hold. He sees a coming banking failure that will destabilize Europe. (SB here: not sure how the U.S. won’t experience some degree of collateral damage due to the interwoven web of counterparty risk.)

- The German banking system is hardly in a position to bail out the European banks.

- (SB again: think back to how the U.S. has been able to “put everyone together in one room and find a solution. Friedman doesn’t believe Europe can get the players from France, Italy, Germany, etc. to get in one room and find a solution. Never tested. Look at how Germany feels about the southern countries. Hope they’ll pass the coming test.)

- Overall, there is large unemployment and a massive depression in Southern Europe.

- That is a problem for Germany because 50% of their exports go to the southern countries. He added, “The fourth largest economy in the world is in trouble.”

- USA

- 13% of our GDP comes from NAFTA (the North American Free Trade Agreement)

- We are our own customers.

- We are relatively immune to the rest of the globe because of this.

- We are not dependent on other countries. We are far less export dependent.

- We have a $339 trillion dollar net worth. We can manage our debt.

- South America is enormously attractive:

- Mexico is the most impressive. Low wages, less regulatory red tape. Airplane and car manufacturers have shifted away from China.

- India has shifted manufacturing out of China to parts of Latin America and Africa.

- No wall needed as most of the migration is the illegal immigrants heading back to Mexico. More people are heading south across the border than north.

- “The world may be going to hell but we are ok.” The U.S. is so well positioned that it will take generations to change this fact.

- It is really possible that the dollar gets really, really strong. (SB: I’ll be sure to share that one with our currency manager – who is largely long the U.S. dollar and has had that trade move against him since mid-February.)

- SB final thought – can someone please get me a pill?

Richard Fisher – Former Dallas Fed President

- North America is the growth engine of the world.

- Innovative – people like George P. Mitchell who invented horizontal drilling. One man changed the oil industry.

- Mexico and Canada have the best rule of law in the world.

- Businesses are relocating to Mexico. Costs are lower.

- “If you want an example of how to get things done – be Mexico.”

- “What are the trip wires?” he asked. Answering his own question, he said, “We know that our markets are levitating but the trip wires are rarely seen.”

- “When you combine ignorance and leverage you get bad results,” implying that is where we find ourselves today.

- The U.S. has $19 trillion in debt. That is $11 trillion more than it was in 2008.

- The Fed’s balance sheet is more than $5 trillion. There is little opportunity for the Fed to expand its balance sheet.

- The Fed is trying to raise interest rates as they know there is only 25 bps to work with today if they need to lower.

- What other tool is left? They can talk and that is what they are doing. Fed statements have gone from 250 words to 950 words today.

- He thinks the central banks are losing their currency (meaning credibility)

- Speaking about trip wires: he said to pay attention to the rollover of the Fed’s existing portfolio. Adding, $2.6 billion rolls in 2016 and $1.6 trillion rolls between 2016 and 2019. He said to watch very closely as to where they invest. “Uber important!”

- Other trip wires:

- Our government has to borrow to pay interest rates.

- There was $1.3 trillion in subprime. There is $7 trillion in sovereign debt.

- Banks are being hampered by Dodd-Frank. Both market making and overall market liquidity.

- He said to keep in mind a quote from Churchill, “In finance, everything that is agreeable is unsound.”

- He recommended that the only book every investor should ever read is Charles Mackay’s book, Memoirs of Extraordinary Popular Delusions. (SB: I’m putting that one on my summer reading list.)

- There is a big bubble in commercial real estate.

- Monetary policy is killing the insurance industry, regional banks and pension plans.

- Insurance companies are living in a 1% return world but they are pushing forward a cart that has liabilities at 5%.

- Pensions are plowing into private equity. That trade is too crowded. He said, “To me, it will end in tears.”

- In regards to expunging the debt. A topic that you’ll see more about below. He said, “Debt can’t be expunged under the current laws.”

- “We have job and income destruction on the people that are the back bone of our country.” He is not surprised to see the rise of Trump and Sanders.

- On Janet Yellen: “She knows her job, she knows what she has to do but she is afraid to do it. The Fed knows they have to do everything they can do to get rates higher.”

- We are at the lowest rates in 239 years – think about that,” he added. (SB here: Bill Gross stated this week that yields are the lowest in 5000 years.) See: Bill Gross Follows Soros, Other “Market Masters” In Warning Of “Supernova”.

- He was asked if June 15 is the last stand for Fed credibility. He answered, “All central banks have lost credibility.” (SB: wow!) He said, “The Fed did a good job with QE1 and QE2. But we began to lose credibility with QE3… where you made the rich richer.”

- Asked what position he is taking with his own portfolio? He answered, “the fetal position. Most of the smart money I know is heavy in cash.”

- He concluded by saying, “Keep your head about you. We live in the sweet spot (North America). We will be ok if we get some Fiscal Policy and the Fed gets off the zero bound.”

Concluding Thoughts – Pippa, Mauldin and Ferguson

As investors, I think what we want to do is look for the opportunities that will come from the breakup in the Euro.

Dr. Pippa Malmgren, founder or the DRPM Group, summed up some of the challenges Europe faces citing an EU politician who said, “We know exactly what to do, we just don’t know how to get reelected after we do it.” She believes the Euro will likely fail. “This is not holding together internally,” she said and added, referring the June 23 Brexit vote, “Britain will have nothing to exit.”

Mauldin’s presentation was outstanding and it can be summed up in the quote I opened with in today’s OMR. Here it is again: “If I had gone to people four years ago and said, ‘Forty percent of the world’s sovereign bonds would be at negative rates (even 40 percent of corporate bonds now in Europe are coming out at negative rates), central banks would expand their balance sheets $10 trillion, and that the world would somewhat look normal, with all of the geopolitical risks that we have with ISIS, etc.,’ people would have said, ‘John, what are you thinking?’ And yet all of those unthinkable things have come about.”

On debt, Mauldin believes “the unthinkable” is that we join hands together (China, Japan, Europe and the U.S.) and monetize the debt at the same time… a global jubilee. One country can’t do it without everyone else doing it, otherwise you’ll have currency wars that will make the 1930s look like a spring picnic.

On the Fed, John asked, “WWTFD?” — What Would The Fed Do? They have been all schooled with Keynes’ book, The General Theory of Employment, Interest and Money. They believe that consumption is the key driver of the economy. As a quick aside, David Rosenberg said that, “Income is the drive, not consumption,” to which I agree. Anyway, the Fed believes that deflation is the worst thing in the world. The belief means you swear on the “Fed bible” that you will not let deflation happen. So the Fed will keep printing. BTW, Fisher agrees they will likely keep printing (though he strongly disagrees with that course of action).

And this is the same for every central bank in the world. John said, “So the likely outcome is a currency war between the major players.” Something we’ve both been writing about for the last several years.

Asked from the audience how we should invest, John answered, “The only thing to do is invest in the global markets. Find managers with flexible strategies that trade the global markets and diversify between a handful of them. You’ve got to be able to get to the other side of what is coming (yes, we’ll get another recession). You have to figure out how to get from here to there with your capital intact.”

Now, let’s go back to that “groupthink” thought. You can see how easy it is to get captured by well thought-out research from a group of bright individuals. Not everyone at the conference was bearish, like Niall Ferguson, MA, D.Phil., historian and Harvard University professor.

Ferguson said, “We avoided the great depression. That is why monetary policy works.” He sees the Shanghai Accord as a possible inflection point that may lead us to a global coordinated monetary policy. I just couldn’t find myself in his camp.

If valuations were low (which they are not), I’d feel much better about letting the noise be noise. But that is not the case. So I find it hard to get me out of this bearish “groupthink” loop and feel that maybe the group is right. The loan optimist at the conference, and he’s a bright one, sees the potential for a global jubilee. Hope he’s right. But either way, valuations are too high and the next recession-driven correction will reset the deck.

Therefore, stay nimble. Risk remains high. Play defense so that you can switch back to offense (e.g. long equities) when the getting gets good again. Unless you have the guts of Druckenmiller (“sell stocks and buy gold”) or Soros now that he has apparently re-entered the investment game and is reportedly going heavily into gold.

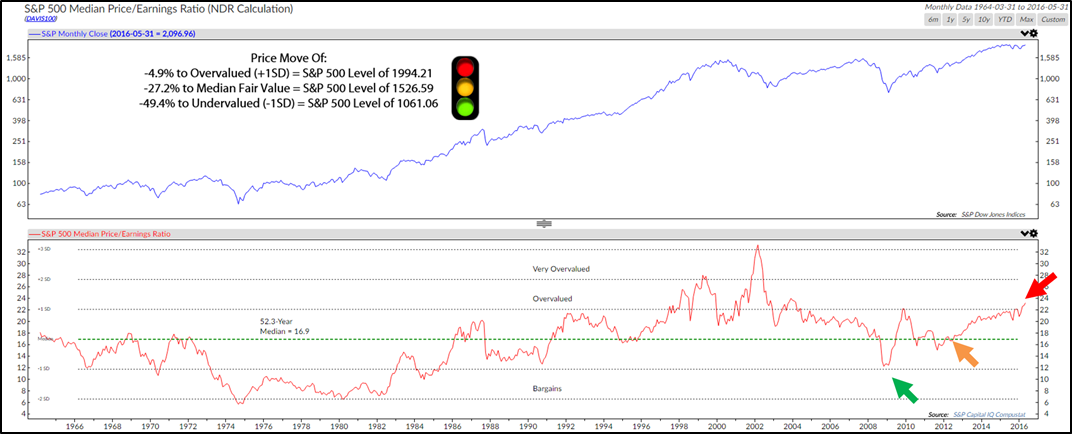

A Quick Look at Valuations

S&P 500 Index – Median PE

Median PE was at 23 at May 2016 month-end. That is higher than it was in 2007. The notable exception was in the late 1990s and early 2000s following the tech bubble. While PE is a poor timing measure, it is a very good estimate of forward returns.

This chart shows the S&P 500 Index to be -27.2% away from fair value. It also looks at standard deviation moves. A 1SD move happens but not often as you can see in the history dating back to 1966 (red line in the lower section of the chart). Given the May close in the S&P 500 Index at 2,096.96, this chart shows the market to be 4.9% overvalued.

Note the red, yellow and green light icon. I put that in to simply identify the risk rewards. The arrows in the bottom section highlight “overvalued, fair value and bargains.”

© Copyright 2016 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/

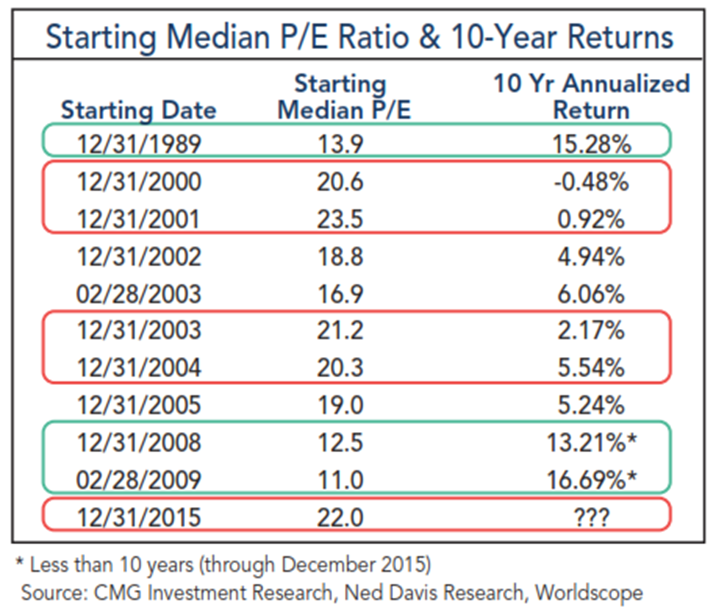

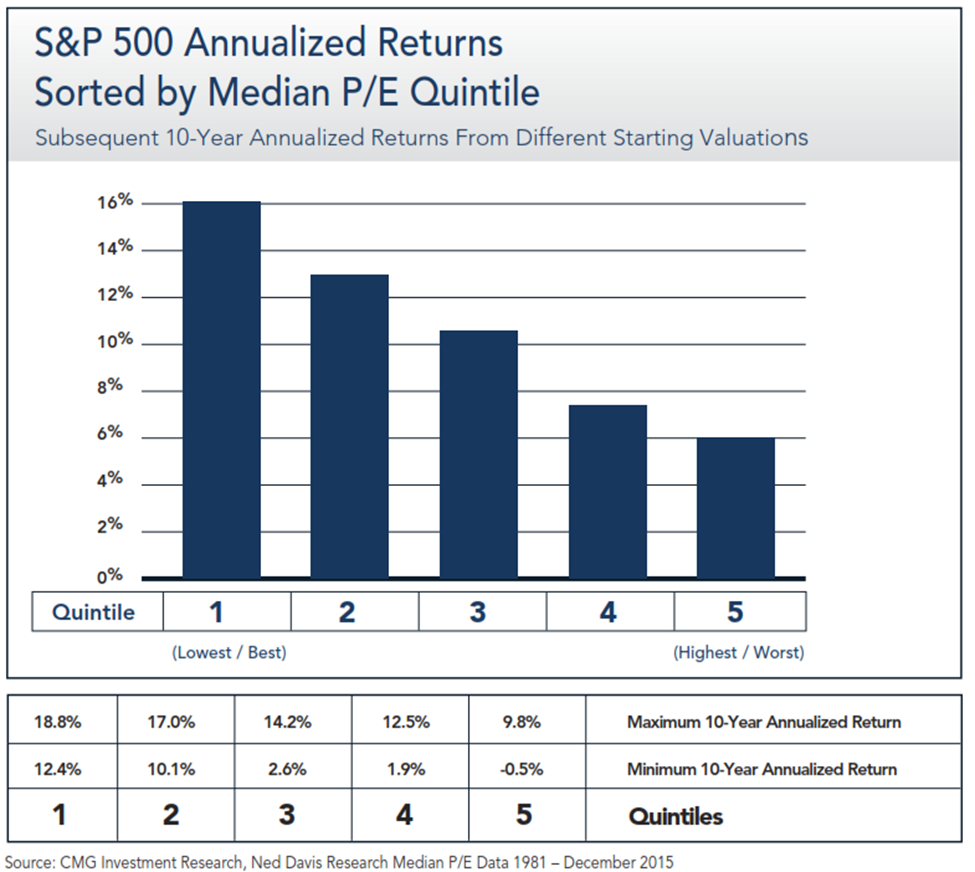

This next chart selects several dates in history. It looks at what Median PE was at a particular month- end and then shows what the subsequent 10-year annualized return turned out to be.

At a current Median PE of 23, we are at the highest level since the early 2000s and higher than the 12-31-2015 number. The next chart shows the average data 1981 through December 2015. Same message. Expect low forward returns when valuations are high.

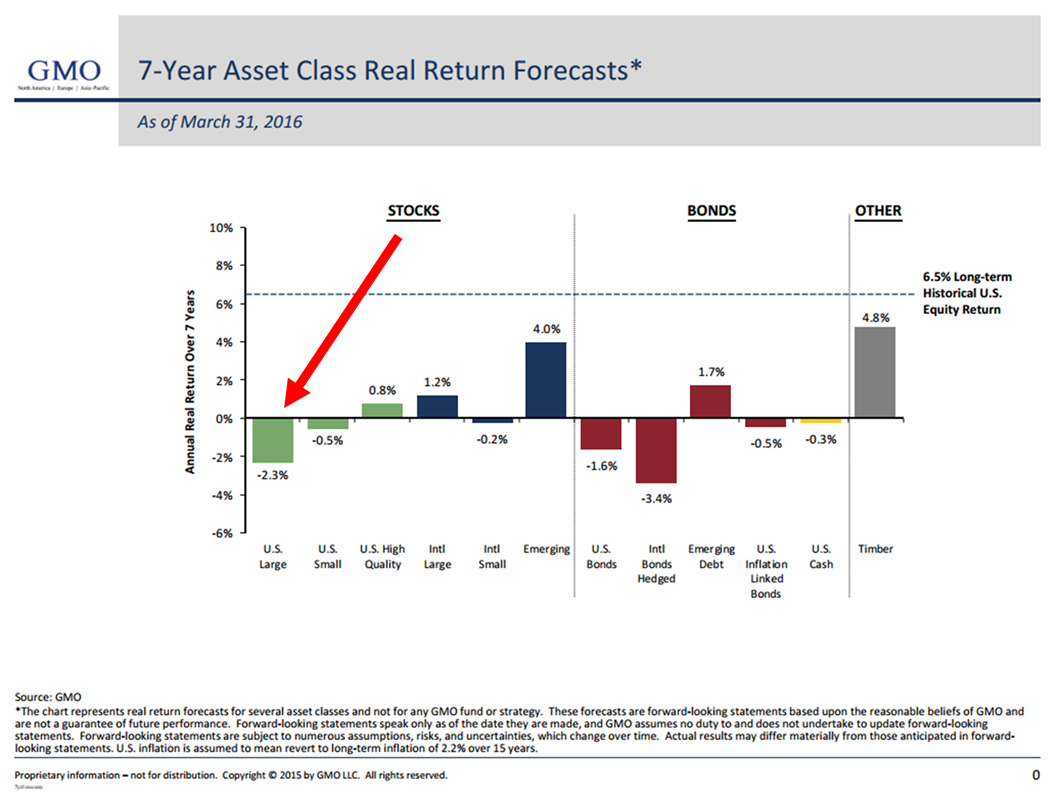

I’ve shared this next chart with you recently. Here is what GMO is saying about returns over the next seven years:

Whether we look at price to sales, price to operating earnings, price to Shiller earnings, price to forward earnings, price to book and most other measures, we find the same conclusion. The market is richly priced. That doesn’t mean it can’t go higher short term; it does mean that 10-year forward returns are likely to be low and downside risk is high.

If “suffering comes from having an argument with reality,” let’s not argue with reality.

Trade Signals – Nearing an All-Time High

Click through to find the most recent trade signals. You can see how we are positioned in our CMG Opportunistic Tactical All Asset ETF Strategy. High yield remains in a buy signal as does the Zweig Bond Model (favors long-term bond exposure). Equity market trend evidence is neutral at best. Our CMG Ned Davis Research Large Cap Indicator remains in a “sell”. Here is a link to the Trade Signals blog page.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

What You Can Do

Last week, I shared a few portfolio ideas with you. If you missed that post I’m going to include them again today. Skip forward if you read this section last week.

With all the gloom due to the current state we find ourselves in, it is only gloomy if we are hoping for 8% returns in a 2% return world. The 8% or better opportunity is coming. Just not from this starting place. A sizable correction is in front of us so let’s play defense now so we can put our offense back on the field at the right time.

In the optimistic “what you can do” category, I share the following, but please understand that they are not a specific recommendation for you to buy or sell any security. I do not know your personal needs, time horizon, risk tolerance or goals. Past performance is no guarantee of future results. Speak with your investment advisor and craft a well-considered investment game plan. Ok, here I go:

First, the path to success is discipline and diversification. How you size the risks (all investments involve risk, including CDs and cash) in your portfolio matters. Here are a few ideas:

- Consider managed futures, global macro and tactical strategies. They have been largely out of favor over the last three years – find good managers and consider overweighting to these categories. I favor a 40% to 50% weighting. I like a mix of currency strategies (due to non-correlation or diversification benefits) and approaches that can go directionally long or short equity and fixed income exposure.

- Find ETF strategies that have the flexibility to invest globally. Blend together a few (3 to 5) experienced ETF strategists that have disciplined processes with the flexibility to move to fixed income, cash, sectors, internationally and even cash. Make sure they don’t have the same process and make sure their strategies can position to defensive asset classes.

- For your equity exposure, hedge your individual positions with out-of-the-money put options and consider writing covered calls to increase your yield and reduce the cost of the put options (think of it as “stock catastrophe insurance”).

- Incorporate a disciplined way to go flat with some of your equity exposure. Internally, we use the CMG Ned Davis Research Large Cap Momentum Index. We go long a low-fee large cap stock ETF on buy signals and we buy a Treasury bill ETF on neutral signals. To us, cash or BIL gives us an option to buy at a bargain sometime in the future. It also reduces our risk exposure. Find a disciplined way to do the same.

- There are also mutual funds that can give you equity market exposure but also have hedging processes built in.

- As for individual targeted risks (single position speculative plays), I am bullish on India and Mexico. I like using ETFs to gain exposure. I am bearish on Italy and France (consider buying put options on ETFs that give exposure to those countries).

- I am short-term neutral but long-term bullish on gold. A 5% to 10% portfolio max weighting.

- Hedge funds are not going away, but many will not survive. Fees will likely continue to come down. It may not feel like we need hedged strategies, but we do. Personally, I favor liquid access to hedge fund managers available within mutual fund 40 Act structures. (You are going to pay up for talent – I’d focus on net returns.)

- Think in terms of how much you are going to allocate to your three asset buckets: stocks, bonds and liquid alternatives. I favor 30-30-40 today and will switch to as much as 70-10-20 when equity market valuations become attractive again. That will happen in the next recession. Margin debt will unwind, selling pressure will be quick so a portfolio designed for defense today will be able to take advantage of the opportunity that will present. Patience is required today as will be the strong stomach required to take action when the time is right. Like the market lows in 2002 and 2009, it was hard to buy, but valuations were best and potential returns the greatest. My best guess is 2017… tied to recession, default cycle, etc. Much depends on the Fed and our fiscal authorities.

For now, participate but protect. And as Yusko concluded in his presentation (click here), adopt the endowment approach.

To that end, I recently wrote a paper titled, “The Total Portfolio Solution.” You can simply reply, “TPS”, to this email to receive your free copy.

Personal Note – “The Greatest”

“I hated every minute of training, but I said, ‘don’t quit.’ Suffer now and live the rest of your life as a champion.”

“He who is not courageous enough to take risks will accomplish nothing in life.”

“I’m the greatest thing that ever lived! I’m the king of the world! I’m a bad man. I’m the prettiest thing that ever lived.”

“I am an ordinary man who worked hard to develop the talent I was given. I believed in myself and I believe in the goodness of others.”

I think that is how most of us will remember him most (click on the link below for a short ESPN “30 for 30” on Muhammad Ali – The Greatest.

Muhammad Ali

I’m going to make plenty of popcorn and watch the hour long special with my kids. Click here to view the 30 for 30 I’m going to watch with my kids.

Our hero… “God works through people, it is not me,” he told the Iraqi hostages he helped free. A great and humble leader. May you continue to “float like a butterfly and sting like a bee.”

Lots of soccer is in our weekend plans. Susan’s team competes in New Jersey as does her youngest son, Kieran. My youngest, Kyle, is heading to Seville, Spain for a two-week class trip and tomorrow night our gang of six (absent Kyle and Brianna) are heading to watch the U.S. Men’s National Team play at Lincoln Financial Field in South Philadelphia.

The plan is to head into the city in the early afternoon, grab some cheesesteaks and then take the subway to the stadium. All dressed in red, white and blue. It’s a big game for the U.S. I hope we sting like a bee.

I’m in NYC for several meetings on the 23rd and then Susan and I are flying to Dana Point, California. I’ll be speaking at the 21stAnnual Global Indexing & ETFs Conference. My team and I believe all investors have benefited greatly by the growth and innovation from the ETF industry. Looking forward to learning much more at the conference.

Chicago follows on June 20-22. Team CMG will be attending a conference hosted by the fastest growing advisory firm at TD Ameritrade. We’ve watched them grow from several hundred million to approximately $1.5 billion under management over the last five years. A great success story. Avi is joining me and we’ll both be presenting. If you are in town, we hope to see you.

Wishing you a fun filled weekend!

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History:

Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Following are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group, Inc.

© CMG Capital Management Group