5 Attractive Biotechnology Stocks for Healthy Long-term Returns

Introduction

I am a fervent believer that investors are best served by investing towards a specific investment objective that suits their own unique goals, objectives and risk tolerance. In other words, investing is not always trying to get the highest possible total returns. If that were true, no one would have ever invested in bonds, CDs or other fixed income instruments.

Personally, my primary current investment objective is focused on achieving a reliable and growing dividend income stream. That doesn’t mean that I don’t expect capital appreciation to go along with my dividends, because I do. However, capital appreciation is secondary to what I need right now. Therefore, I am content to allow it to happen over the long run. This means being willing to accept the ups-and-downs of short-term market volatility that is sure to occur, as long as my dividend income keeps increasing.

On the other hand, I also have discretionary assets that I can invest in/or utilize outside of my core portfolio. So even though I favor dependable dividend paying stocks, I still am attracted to examining exciting growth investments with money I am both willing to and can afford to lose. However, even though I’m willing to lose with these discretionary assets, I don’t expect to. Instead, my objective is to generate significantly higher total returns than my prudent dividend growth portfolio is realistically capable of achieving.

More simply stated, I still appreciate powerful and exciting growth stocks because I understand they are capable of generating significantly higher returns. However, I am also cognizant of the fact that the risk associated with achieving those returns is also significantly higher. Consequently, I am just as adamantly (or even more so) focused on valuation when investing in growth stocks as I am with prudent blue-chip dividend paying stocks.

One of the most difficult things for the value-oriented investor to accept and embrace is the reality that the best value comes from stocks that are temporarily out-of-favor. In this regard, the value investor must also recognize that hitting the perfect bottom can only be accomplished with luck. Therefore, the intelligent value investor is willing to assume some short-term pain in order to achieve long-term gain.

The biotechnology sector contains many exciting growth stocks. But most importantly, as it relates to this article, the sector has recently been out-of-favor, which I believe has created bargain investment opportunities. Consequently, I offer the following 5 biotechnology stocks as attractive looking research candidates primarily for growth or long-term total return. However, 2 of these 5 biotech stocks offer attractive dividends in conjunction with above-average growth and attractive value.

3 Research-Worthy Biotechnology Growth Stock Candidates

These first 3 biotechnology research candidates are offered as pure growth stocks. None of them pay a dividend, and I don’t expect any of them to initiate one anytime soon. However, I believe all 3 appeared attractive relative to their long-term growth potential.

On each candidate, I present a short business description courtesy of S&P Capital IQ, followed by a series of F.A.S.T. Graphs™ and FUN Graphs highlighting some important fundamental metrics. Importantly, what I am presenting here is the recommendation that these stocks are worthy of further scrutiny if growth for high total return is your objective.

Biogen Inc (BIIB)

“Biogen Inc. discovers, develops, manufactures, and delivers therapies for the treatment of neurodegenerative diseases, hematologic conditions, and autoimmune disorders. It offers TECFIDERA, AVONEX, and PLEGRIDY to treat relapsing forms of multiple sclerosis (MS); TYSABRI to treat relapsing forms of MS and Crohn’s disease; and FAMPYRA to improve walking ability for patients with MS.

The company also provides ELOCTATE to treat adults and children with hemophilia A for control of bleeding episodes; ALPROLIX to treat adults and children with hemophilia B for control of bleeding episodes; RITUXAN for treating non-Hodgkin's lymphoma, rheumatoid arthritis, and chronic lymphocytic leukemia (CLL), as well as two forms of ANCA-associated vasculitis; GAZYVA for the treatment of patients with previously untreated CLL; and FUMADERM to treat plaque psoriasis.

The company’s products in Phase III development stage comprise ZINBRYTA, a monoclonal antibody for the treatment of relapsing-remitting MS; Aducanumab for Alzheimer’s disease; and ISIS-SMNRx for spinal muscular atrophy. Its Phase II clinical trial products include Anti-LINGO for optic neuritis and MS; Amiselimod for multiple autoimmune indications; BAN2401 and E2609 for Alzheimer's disease; Raxatrigine for trigeminal neuralgia; rAAV-XLRS for X-linked juvenile retinoschisis; and BG00011 for idiopathic pulmonary fibrosis. Its Phase I clinical trial products comprise Dapirolizumab pegol for systemic lupus erythematosus (SLE); ISIS – DMPK for myotonic dystrophy; Anti-BDCA2 for SLE; Anti-alpha-synuclein for Parkinson’s disease; and BIIB063 for sjogren’s syndrome.

The company has a strategic research collaboration with Ionis Pharmaceuticals, Inc. It offers products primarily through its own sales force, marketing groups, and third parties worldwide. The company was formerly known as Biogen Idec Inc. and changed its name to Biogen Inc. in March 2015.

Biogen Inc. was founded in 1978 and is headquartered in Cambridge, Massachusetts.”

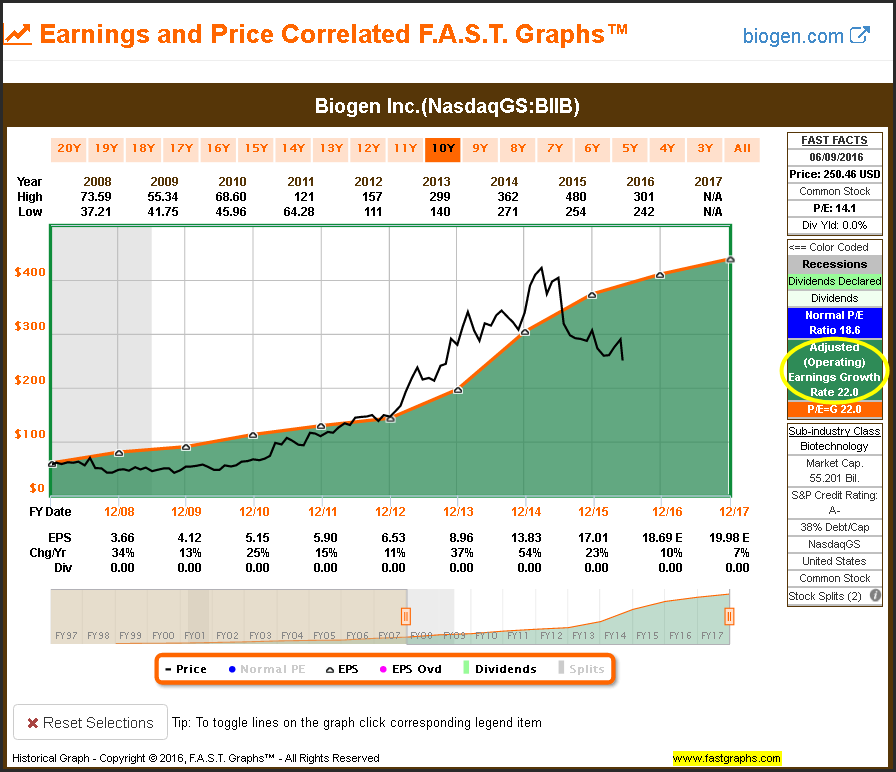

Biogen has produced an impressive record of earnings growth since fiscal year 2008. However, it should be noted that growth expectations for 2016 and 2017 are below historical norms.

When monthly closing stock prices are brought into the equation we initially see a very high correlation between price and earnings over the long run. However, we also see a significant disconnect where price became significantly ahead of earnings justified valuation for most of 2013, 2014, and the first half of 2015. However, it appears that expectations for slower growth took the wind out of the price sails.

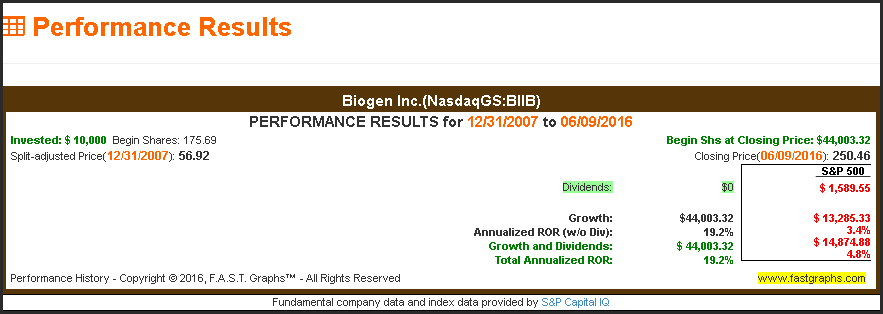

Nevertheless, in spite of the drastic correction in stock price, the long-term returns that Biogen generated for shareholders has significantly outperformed the average company.

Biogen has produced excellent gross and net profit margins over the last 10 years. Even though growth is expected to slow somewhat, I find it comforting that net profit margins are strong and improving.

I also like the fact that Biogen’s return on equity has been increasing at a rapid rate.

Consensus long-term earnings estimates and growth rates are currently forecast to be below historical norms. However, Biogen does have an exciting pipeline of potential future blockbuster drugs, but, there is high risk as to whether they will generate future profits or not.

Celgene Corporation (CELG)

“Celgene Corporation discovers, develops, and commercializes therapies to treat cancer and inflammatory diseases worldwide. It markets REVLIMID, an oral immunomodulatory drug for multiple myeloma, myelodysplastic syndromes (MDS), and mantle cell lymphoma; ABRAXANE, a solvent-free chemotherapy product to treat breast, non-small cell lung, pancreatic, and gastric cancers; POMALYST/IMNOVID to treat multiple myeloma; and OTEZLA, a small-molecule inhibitor of phosphodiesterase 4 for psoriatic arthritis, psoriasis, ankylosing spondylitis, Behçet's disease, atopic dermatitis, and ulcerative colitis.

The company’s products also include VIDAZA, a pyrimidine nucleoside analog to treat intermediate-2 and high-risk MDS, and chronic myelomonocytic leukemia, as well as acute myeloid leukemia (AML); THALOMID for the patients with multiple myeloma and erythema nodosum leprosum; ISTODAX to treat cutaneous and peripheral T-cell lymphoma; and FOCALIN, FOCALIN XR, and RITALIN products. Its clinical stage products include OTEZLA for the treatment of various immune-inflammatory diseases; sotatercept for the treatment of renal anemia, beta-thalassemia and MDS; luspatercept for beta-thalassemia and MDS; CC-486 to treat MDS, AML, and solid tumors; CC-122 and CC-220 to treat hematological and solid tumor cancers, and inflammation and immunology diseases; PDA-002 for the treat diabetic foot ulcers and peripheral neuropathy; and PNK-007 for hematological malignancies treatment.

The company has collaborative agreements with Novartis Pharma AG; Acceleron Pharma; Agios Pharmaceuticals, Inc.; Epizyme Inc.; Sutro Biopharma, Inc.; bluebird bio, Inc.; FORMA Therapeutics Holdings, LLC; Acetylon Pharmaceuticals, Inc.; OncoMed Pharmaceuticals, Inc.; NantBioScience, Inc.; AstraZeneca PLC; Lycera Corp.; Juno Therapeutics, Inc.; TriNetX, Inc.; Triphase Accelerator Corporation; and Nurix, Inc.

The company was founded in 1980 and is headquartered in Summit, New Jersey.”

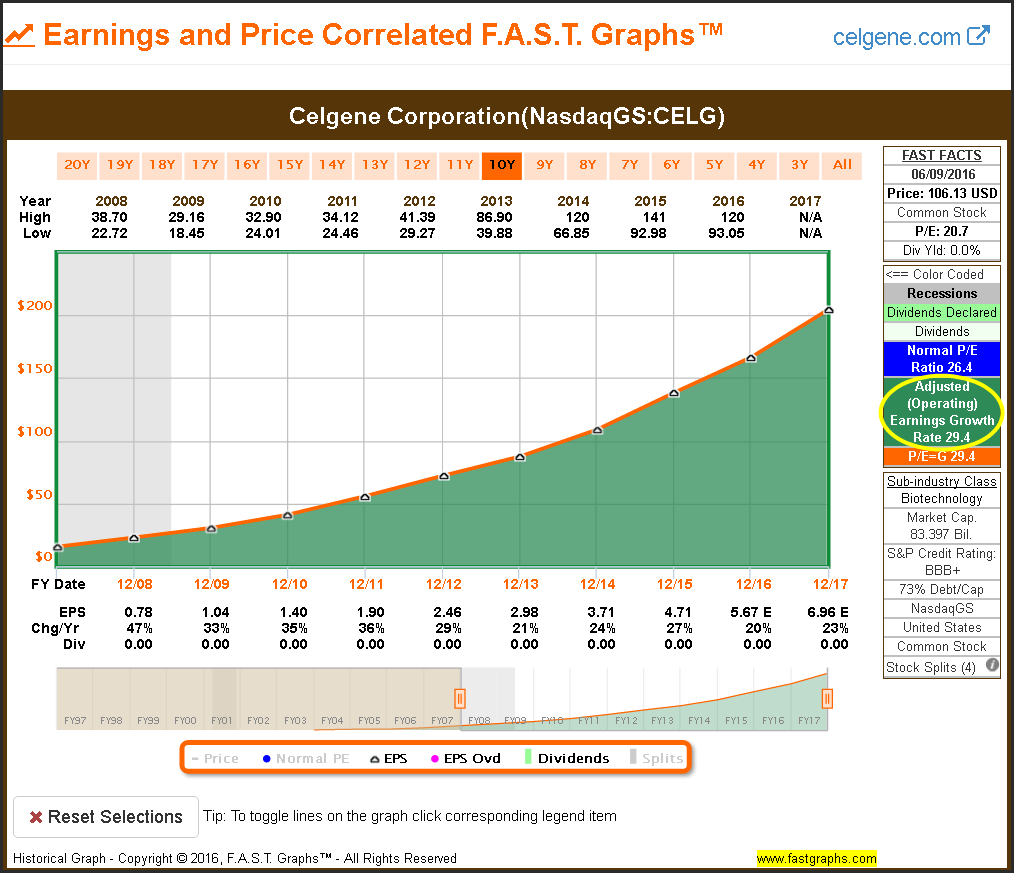

Of the research candidates presented in this article, Celgene, represents my personal favorite. Historical earnings growth has been extremely strong and very consistent since 2008. The only real negative is the company’s high debt to capital.

Once again, we see a clear correlation between monthly closing stock prices and earnings over the long run. But most importantly, it is clear that the best times historically to invest in Celgene has been when its price has been below its earnings justified level as it is today.

Celgene represents another example of significant long-term performance in spite of its current undervaluation, and the fact that it was moderately overvalued at the beginning of 2008. This clearly illustrates the power of compounding earnings growth at high levels.

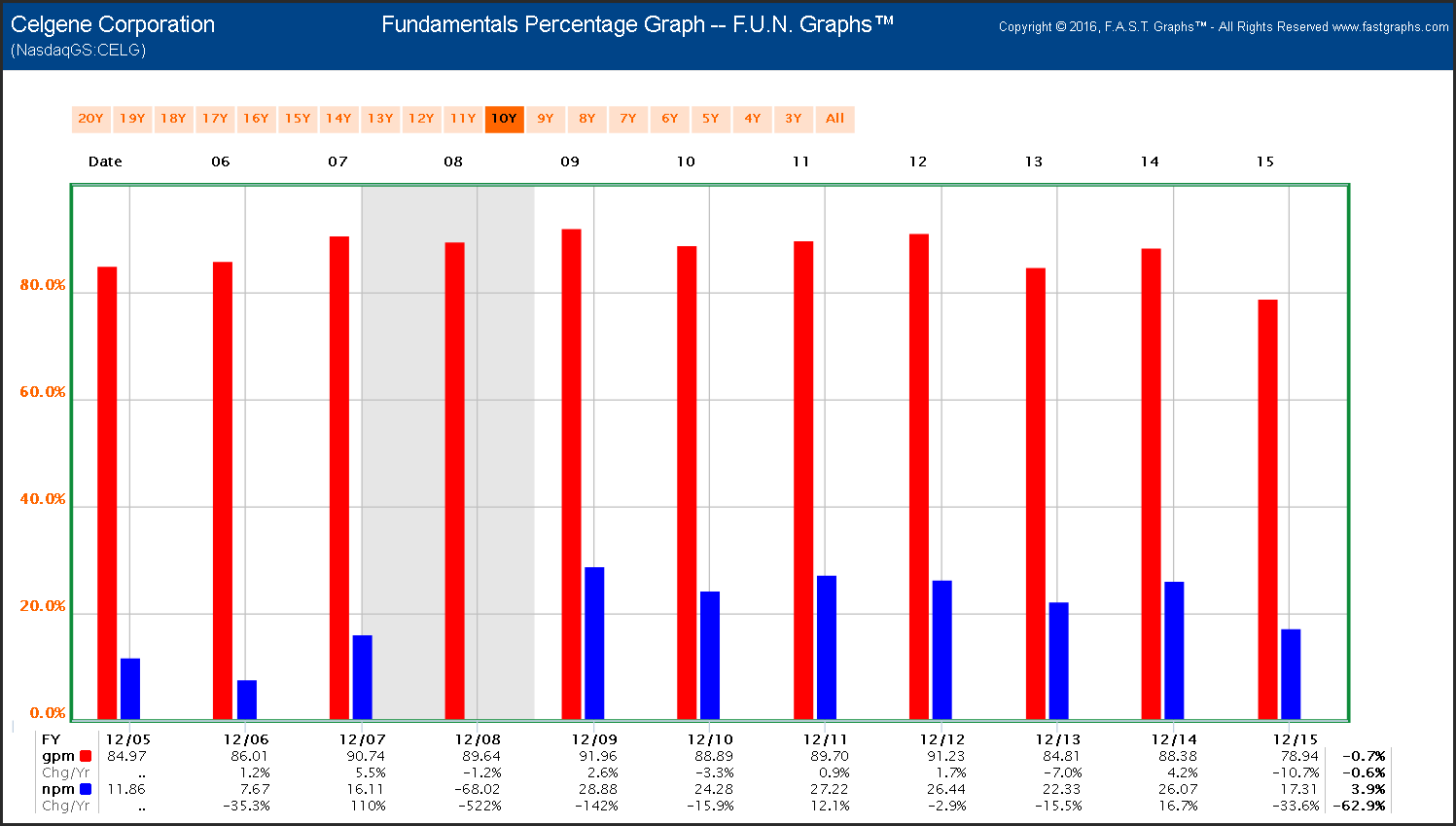

Celgene has produced strong gross and net margins historically. However, net profit margins weaken somewhat in 2015, but remain high relative to the average company. On the other hand, net profit margin has improved to almost 32% through the March quarter of 2016 (not shown on the graph).

Celgene also produces high returns on equity.

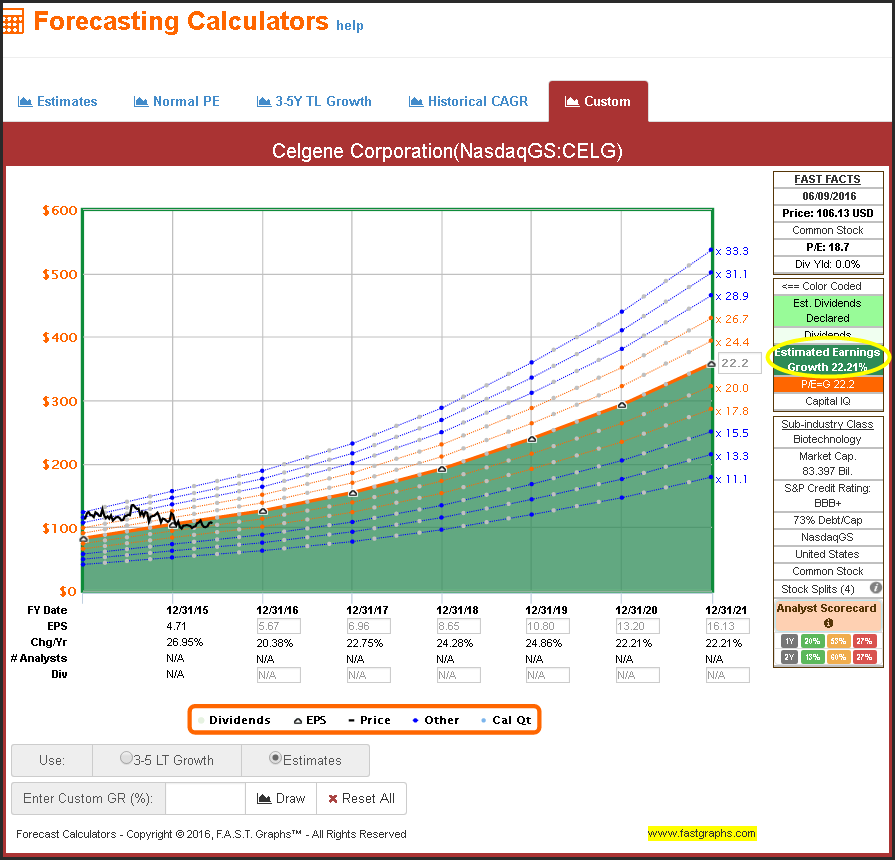

Analysts continue to expect Celgene to grow future long-term earnings in excess of 20% per annum.

Jazz Pharmaceuticals (JAZZ)

“Jazz Pharmaceuticals Public Limited Company, a biopharmaceutical company, identifies, develops, and commercializes pharmaceutical products for various medical needs in the United States, Europe, and internationally.

The company has a portfolio of products and product candidates with a focus in the areas of sleep and hematology/oncology. It markets Xyrem, an oral solution for the treatment of cataplexy and excessive daytime sleepiness (EDS) in patients with narcolepsy; Erwinaze to treat acute lymphoblastic leukemia (ALL); Defitelio for the treatment and prevention of severe hepatic veno-occlusive disease, a potentially life-threatening complication of hematopoietic stem cell transplantation; and Prialt, an intrathecally administered infusion of ziconotide for the management of severe chronic pain.

The company also develops JZP-110, a late-stage investigational compound, which is in phase III clinical trail for the treatment of EDS in narcolepsy and obstructive sleep apnea; and JZP-386, a deuterium-modified analog of sodium oxybate that is completed phase I clinical trail for use in patients with narcolepsy. In addition, it sells psychiatry and other products.

The company is headquartered in Dublin, Ireland.”

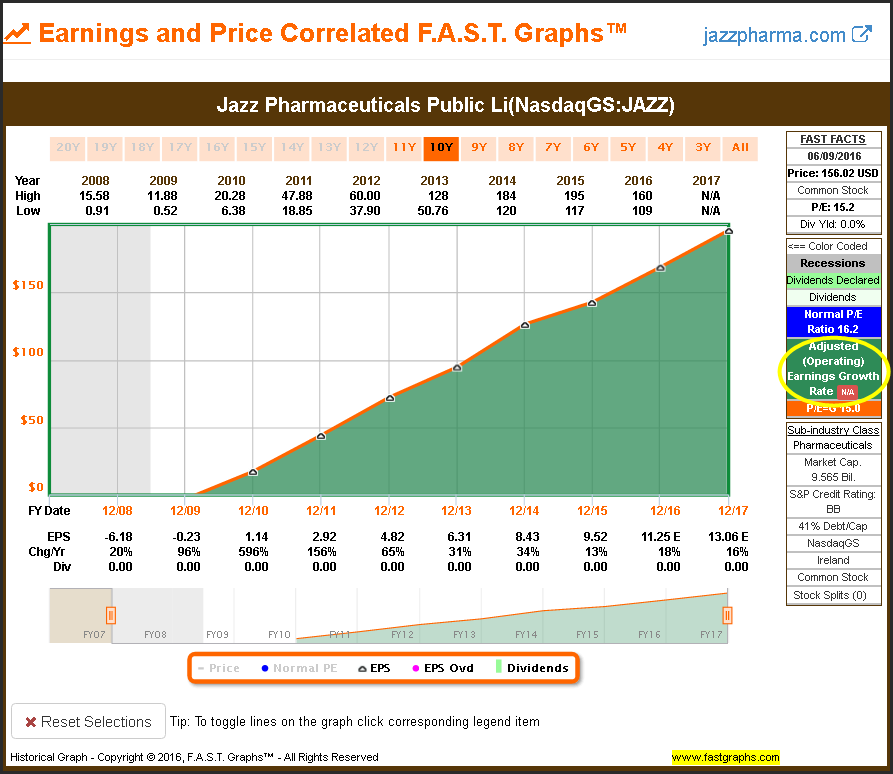

Jazz Pharmaceuticals went from negative earnings in 2009 to positive earnings in 2010. Consequently, long-term earnings growth rate has been distorted by aberrantly high earnings growth in 2010 and 2011. Nevertheless, historical earnings growth since 2013 has exceeded 20% per annum.

When monthly stock prices are included, we once again see a high correlation between earnings growth and stock price over the long term. However, in this case, the orange earnings justified valuation line is drawn at a market average P/E ratio of only 15.

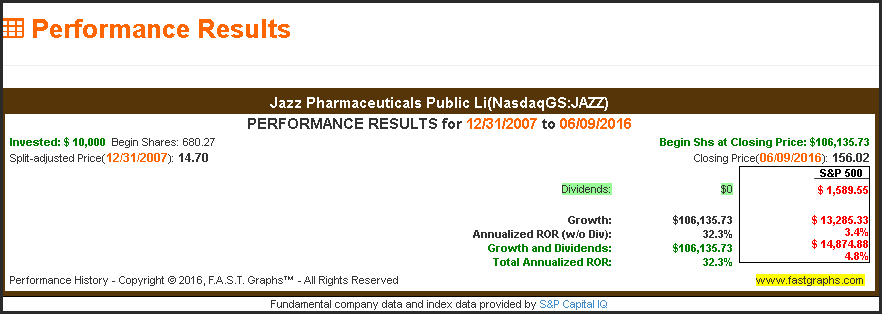

Nevertheless, Jazz has produced exciting long-term returns for its shareholders.

Jazz has produced exceptional gross margins since 2007. However, net profit margins have been a little more erratic. Nevertheless, I consider this an intriguing research candidate at its current valuation.

The return on equity for Jazz is troubling. Therefore, I consider this my least favorite of the 5 research candidates presented. However, it’s hard to argue with its past performance.

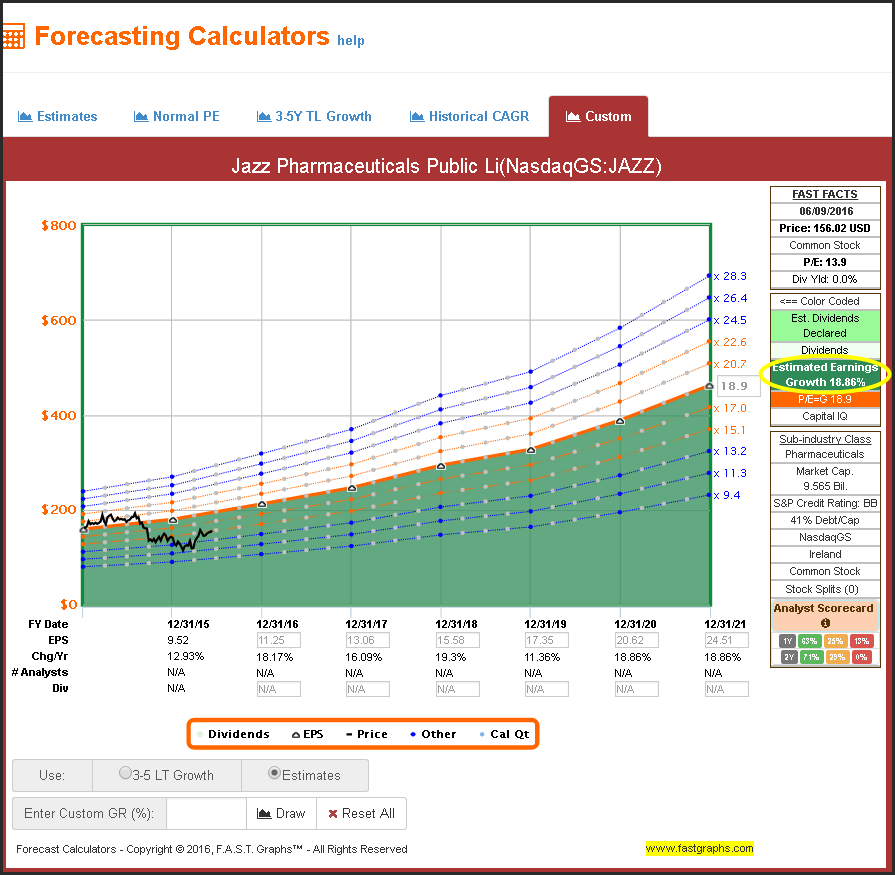

Consensus estimates for future growth are very strong - approaching 19% per annum. However, there is scant history available to analyze on this company, and analysts don’t have a great record of forecasting earnings over the last couple of years.

2 Research Worthy Biotechnology Dividend Growth Stock Candidates

These next 2 biotechnology research candidates offer both above-average growth and above-average current dividend yield and dividend growth potential. Consequently, I consider both attractive long-term total return opportunities with the benefit of a solid and growing dividend yield.

AbbVie Inc (ABBV)

“AbbVie Inc. discovers, develops, manufactures, and sells pharmaceutical products worldwide. The company offers HUMIRA, a biologic therapy administered as a subcutaneous injection to treat autoimmune diseases; IMBRUVICA an oral therapy for the treatment of chronic lymphocytic leukemia; and VIEKIRA PAK, an interferon-free therapy, with or without ribavirin, for adults with genotype 1 chronic hepatitis, including those with compensated cirrhosis.

It also provides Kaletra, an anti-HIV-1 medicine used with other anti-HIV-1 medications as a treatment that maintains viral suppression in HIV-1 patients; Norvir, a protease inhibitor indicated in combination with other antiretroviral agents to treat HIV-1; and Synagis to prevent respiratory syncytial virus infection in high risk infants.

In addition, the company offers AndroGel, a testosterone replacement therapy for males diagnosed with symptomatic low testosterone; Creon, a pancreatic enzyme therapy for exocrine pancreatic insufficiency; Synthroid to treat hypothyroidism; and Lupron, a product for the palliative treatment of prostate cancer, and endometriosis and central precocious puberty, as well as for the treatment of patients with anemia.

Further, it provides Duopa and Duodopa, a levodopa-carbidopa intestinal gel to treat Parkinson’s disease; Sevoflurane, an anesthesia product for human use; TriCor, Trilipix, and Niaspan treat metabolic conditions characterized by high cholesterol and/or high triglycerides; and Zemplar to treat secondary hyperparathyroidism.

The company sells its products to wholesalers, distributors, government agencies, health care facilities, specialty pharmacies, and independent retailers from its distribution centers and public warehouses. AbbVie Inc. has strategic collaboration with C2N Diagnostics, Calico Life Sciences LLC, Infinity Pharmaceuticals, Inc., Ablynx NV, Galapagos NV, and Alvine Pharmaceuticals, Inc.

The company was incorporated in 2012 and is based in North Chicago, Illinois.”

AbbVie has a short history after being spun off of Abbott Labs. However, the company has produced consistent above-average earnings growth and its dividend has been increased and grown each year since it was an independent company.

Even though the history is short, AbbVie’s stock price has moved in tandem with earnings over the long run. Moreover, periods of both overvaluation and undervaluation are vividly revealed. Currently, I consider this high-quality biotechnology company currently undervalued. My only reservation is the company’s high debt to capital ratio.

Even though AbbVie’s performance history is short, the company has outperformed the S&P 500 on both capital appreciation and dividend income. I think this is noteworthy considering how strong the performance of the average company was during this timeframe.

AbbVie has produced strong and attractive gross and net margins since it was an independent company. However, it’s also important to recognize that Humira is their flagship drug and it has produced more than 50% of sales and 70% of profits. However, the company’s pipeline is interesting, and Humira is expected to be a solid contributor for years to come.

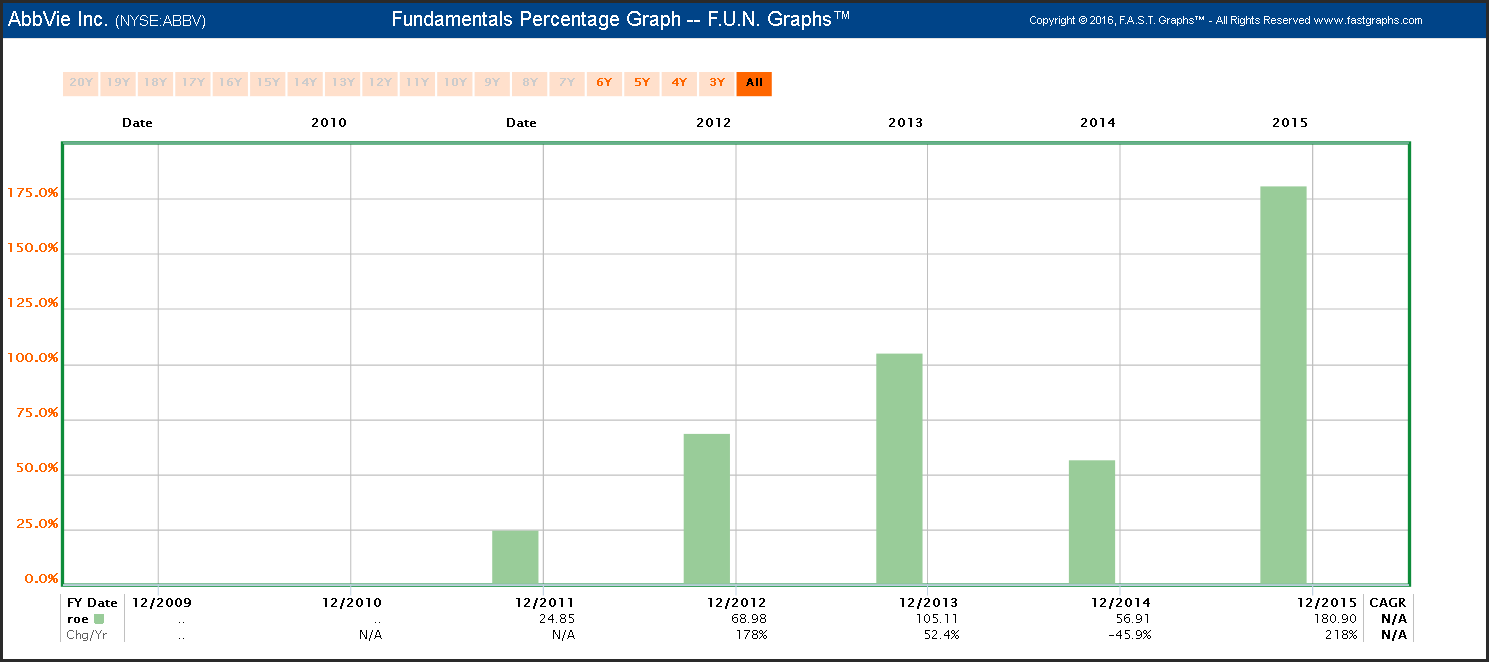

AbbVie’s return on equity has been very high stakes in most part due to Humira.

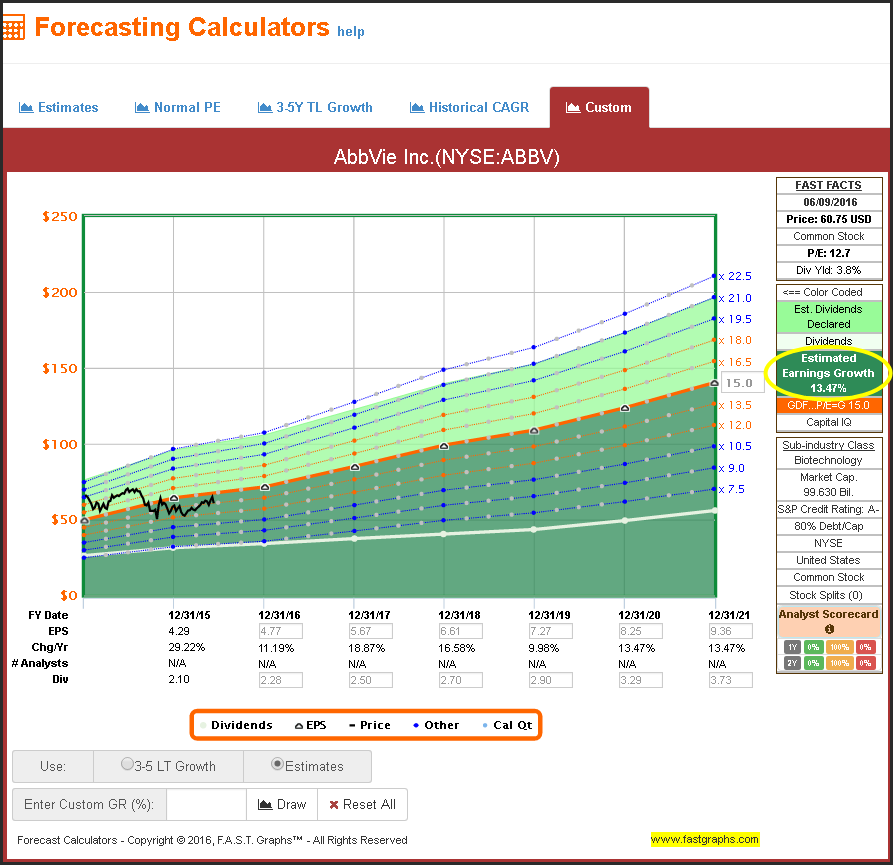

Consensus estimates for AbbVie’s future earnings growth is significantly above average. Couple this with an extremely attractive current dividend yield and AbbVie appears to be a very solid investment.

Amgen Inc (AMGN)

“Amgen Inc., a biotechnology company, engages in discovering, developing, manufacturing, and delivering human therapeutics worldwide. It offers products for the treatment of illness in the areas of oncology/hematology, cardiovascular, inflammation, bone health, nephrology, and neuroscience.

The company’s principal products include Neulasta, a pegylated protein to decrease the incidence of infection associated with chemotherapy-induced febrile neutropenia in cancer patients; NEUPOGEN, a recombinant-methionyl human granulocyte colony-stimulating factor for reducing the incidence of infection for patients with non-myeloid malignancies; and Enbrel to treat rheumatoid arthritis, plaque psoriasis, and psoriatic arthritis.

Its principal products also comprise EPOGEN to treat a lower-than-normal number of red blood cells caused by chronic kidney disease (CKD) in patients on dialysis; Aranesp for treating anemia; XGEVA for the prevention of skeletal-related events; Prolia to treat postmenopausal women with osteoporosis; Repatha for the treatment of high cholesterol; and Sensipar/Mimpara products for use in the treatment of secondary hyperparathyroidism in CKD patients on dialysis.

The company’s other marketed products include Kyprolis, a proteasome inhibitor to treat patients with multiple myeloma and small-cell lung cancer; Nplate, a thrombopoietic compound; Vectibix, a human monoclonal antibody; and BLINCYTO for the treatment of patients with Philadelphia chromosome-negative relapsed or refractory B-cell precursor acute lymphoblastic leukemia. It also develops various products that are in various clinical trials.

The company serves pharmaceutical wholesale distributors; and physicians or their clinics, dialysis centers, hospitals, and pharmacies, as well as consumers. It has collaborative agreements with Xencor, Inc.; UCB; Novartis AG; and Bayer HealthCare Pharmaceuticals Inc.

Amgen Inc. was founded in 1980 and is headquartered in Thousand Oaks, California.”

Amgen is widely considered as the mother of all biotechnology companies. This biotech giant has produced strong and steady earnings growth over its entire history, and the initiation of a dividend in 2011 that has grown significantly is also a plus.

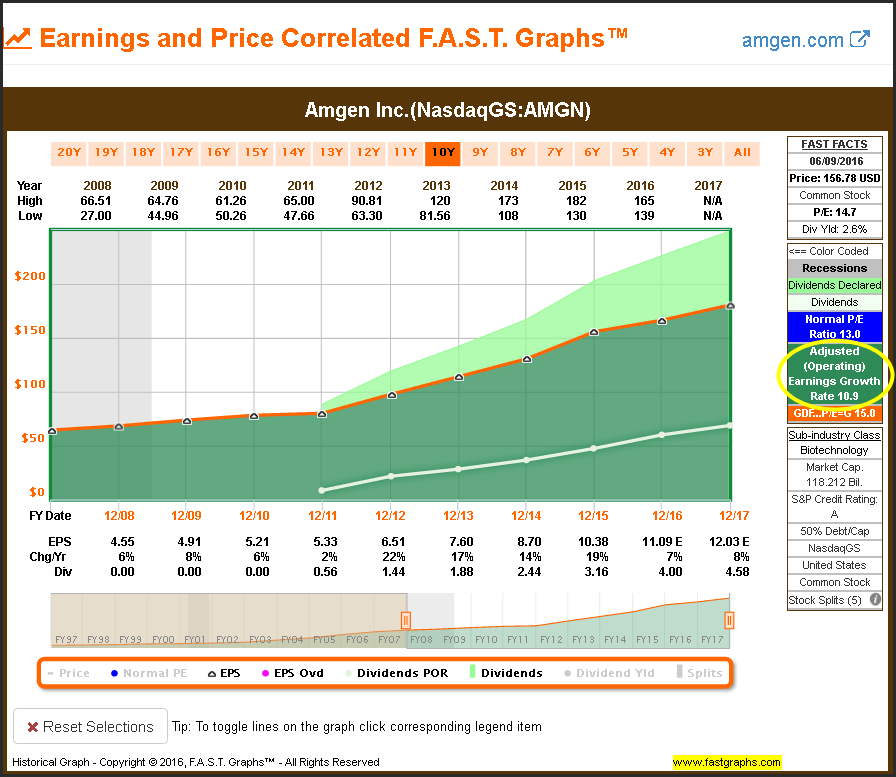

Clearly, Amgen’s stock price has closely tracked its earnings achievement. After becoming moderately overvalued in 2015, the recent negativity towards biotechnology in general appears to have brought the stock to attractive valuations again.

Amgen has been a solid performer that has generated higher returns than the S&P 500 and a higher level of cumulative dividend income even though it’s only paid a dividend since 2011.

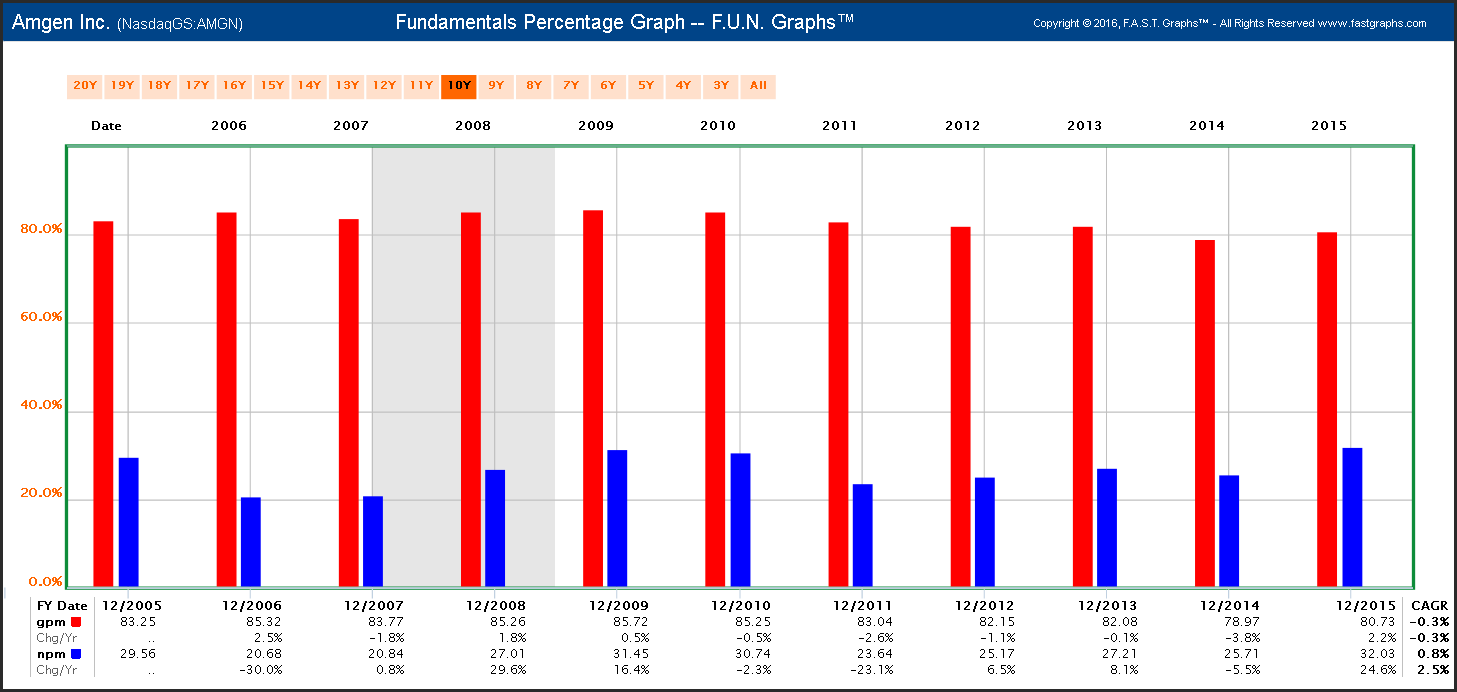

Not only have Amgen’s gross and net profit margins been high, they have also been very consistent.

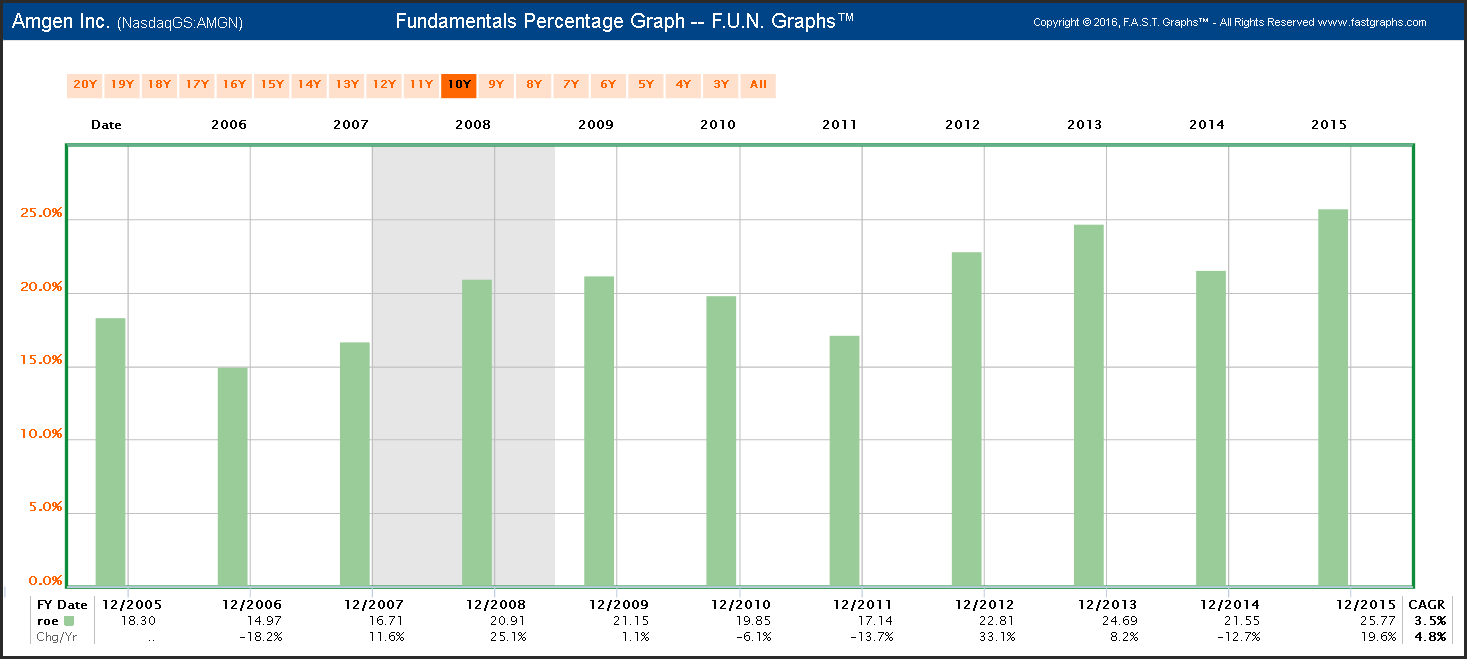

Likewise, Amgen has achieved a very attractive and consistently high return on equity historically.

Long-term estimates for Amgen’s future earnings growth are above average. Adding the additional opportunity of an above-average and growing dividend income makes Amgen look very solid at current valuations.

Summary and Conclusions

The best-of-breed companies in the biotechnology sector have a legacy of producing exceptional long-term shareholder returns. However, the sector has recently gone out-of-favor which I believe has created a significant long-term opportunity for investors willing to take the risk.

There are many that believe that biotechnology represents the future and promise of medicine. Some even believe that chemical-driven pharmaceuticals have run their course. The 5 research candidates presented in this article appear to be worthy of further research and due diligence for those interested in above-average long-term returns, and are willing to take the risk associated with investing in biotech.

Considering that the stock market in general appears rather frothy, attractively-valued biotechnology stocks appear to be worth a closer look considering the retrenchment in price most have experienced recently. But most importantly, biotechnology stocks today appear to offer something for everyone. If income is your objective, there are 2 here that are worth looking at. If growth is your objective, I believe all 5 of these candidates are worth a closer look.

Disclosure: Long ABBV

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.