“Nearly all men can stand adversity, but if you want to test a man’s character, give him power.”

– Abraham Lincoln

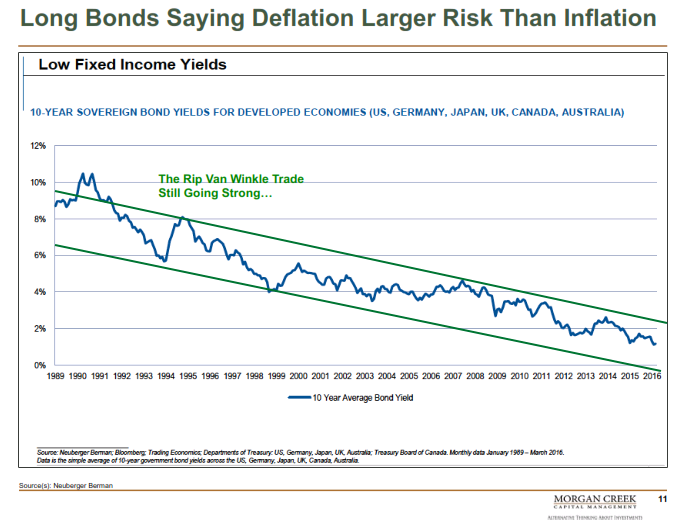

Do you remember back in the early 80s when interest rates peaked at 15.25% and most everyone felt rates were moving higher, certainly not lower? The fact is, it was the single best time in history to get bullish on bonds.

Solomon Brothers’ head of research Henry Kaufman went from bond bear to bond bull and that call, unpopular as it was, later earned him “guru” status. The thing is, at that time, most people thought he was nuts.

Recall too that inflation was in the mid-teens and both stocks and bonds had burned investors over the prior decade. Fed Chairman Paul Volker stood tall in his fight to rein in inflation. Kaufman’s bullish call went on deaf ears. Few seized the opportunity.

I remember my mentor, John Ray (then a portfolio manager at Delaware Funds) telling me a story about an investment committee meeting where he stood before his colleagues and said we should put 100% of our money in long-term Treasury bonds and call it a day (or maybe call it 32 years as that investment beat stocks by a large margin). John’s bullish call went on deaf ears.

Let’s pause and look at the current situation from 35,000 feet. Back then we were trying to defeat inflation by driving ultra-high interest rates even higher. Today, we are trying to create inflation by driving ultra-low interest rates even lower. Who wanted to buy bonds in the early 80s? The past 1, 3, 5 and 10 years of performance were abysmal. It was the right thing to do. Everyone wants to buy bonds today. Just look at the fund flows.

Investors look at recent performance and project it forward. This has to stop!

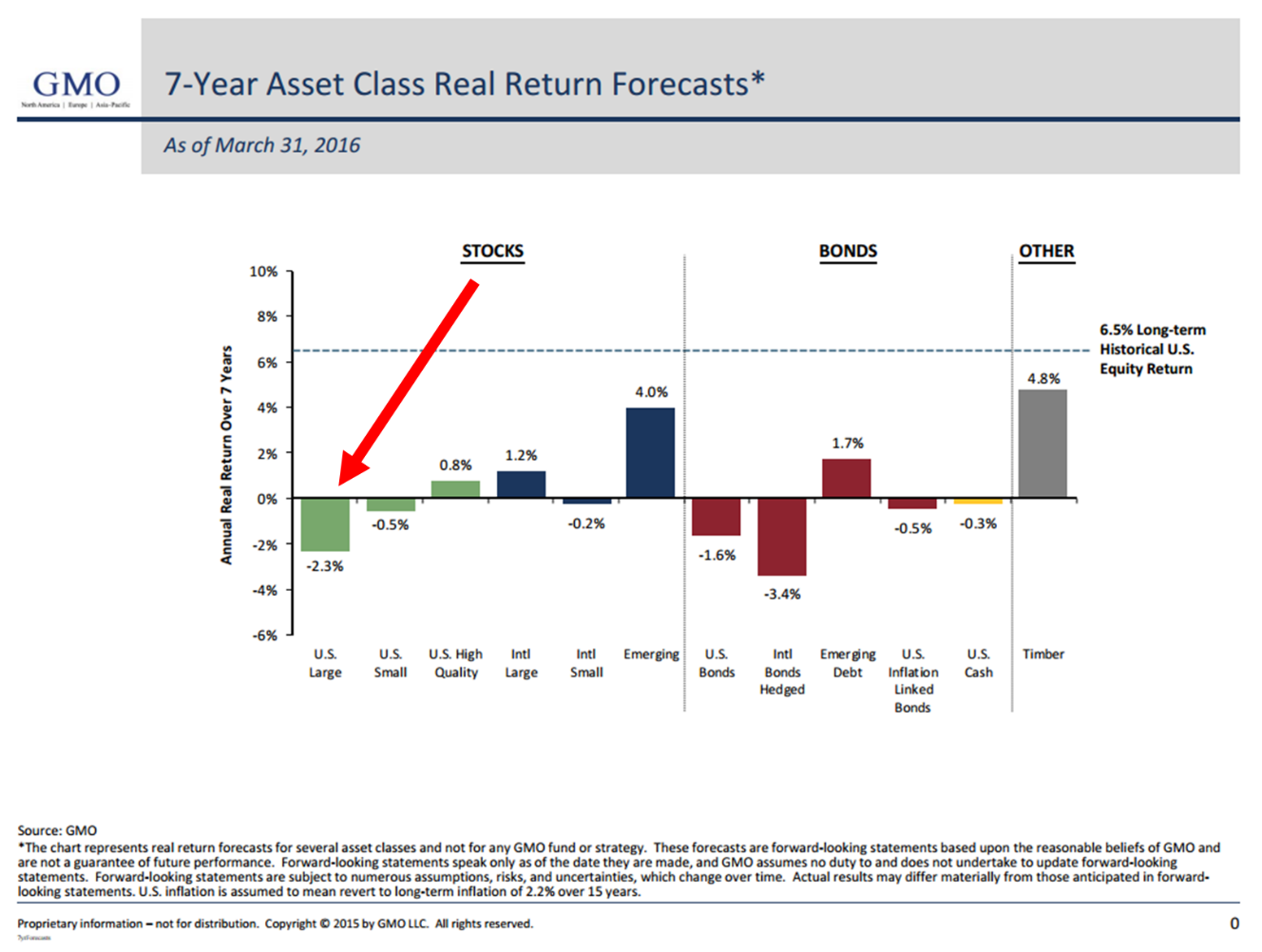

It’s a fine mess we find ourselves in. So here is the skinny. The bond market has little juice left to provide your portfolio with the help it provided you in the past. The same is true for the equity market as you can see next in GMO’s 7-Year Real Asset Return Forecast:

For the S&P 500 Total Return Index, that’s -2.3% per year for seven years. And, as you see, there is a lot of below 0% numbers across categories in the chart. Show this to everyone you know (especially your clients).

By the way, over the last decade, GMO’s forecasts had a 93.6% correlation to what they predicted and what actually happened. In non-geek terms, that’s pretty spot-on. No guarantees, of course, but we should take note.

All of this perhaps more eloquently expressed by Bill Gross in his latest missive entitled, “Bon Appetit!”

With interest rates near zero and now negative in many developed economies, near double-digit annual returns for stocks and 7%+ for bonds approach a 5 or 6 Sigma event, as nerdish market technocrats might describe it. You have a better chance of observing another era like the previous 40-year one on the planet Mars than you do here on good old Earth.

We are in the late stages of an economic game of musical chairs. Not many open chairs remain. We circle around and when the music stops, we race quickly to find an open chair. At the end of the game, there are few winners yet we all think we can play it and act quickly when the music stops. The Fed is in control of the music.

Many will lose but the game will be reset (higher interest rates and lower stock prices) and on we will go and play again. Let’s not lose the game. For now, be smart, play defense, be patient and know that there are many ways to make money. I share a few ideas in the conclusion below.

Today, let’s quickly take about the Fed (a behind the curtain view) and their probable course of action and then, in bullet point form, share with you my notes from Mark Yusko’s outstanding presentation at the recent Strategic Investment Conference (hosted by my good friend simply now known as Mauldin). By the way, I’ve ordered the audio recordings and will see if I can get permission to share a link to Yusko’s presentation with you. It was outstanding and, overall, I believe it is well captured in this next quote from Bill Gross.

The “fact of the matter” – to use a politician’s phrase – is that “carry” in any form appears to be very low relative to risk. The same thing goes with stocks and real estate or any asset that has a P/E, cap rate, or is tied to present value by the discounting of future cash flows. To occupy the investment market’s future “penthouse,” today’s portfolio managers – as well as their clients, must begin to look in another direction. Returns will be low, risk will be high and at some point the “Intelligent Investor” must decide that we are in a new era with conditions that demand a different approach. (Emphasis mine.)

With that, let’s get started. Grab a coffee or maybe two – I share a number of “what do we do” ideas.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Fed Up

- Mark Yusko’s Presentation – There Goes The Boom

- Trade Signals – Global Recession Probability High, No U.S. Recession Yet

Fed Up

I had dinner with Danielle DeMartino Booth last week in Dallas. Danielle is a former senior analyst for Richard Fisher and worked with him during his time as the Dallas Fed president.

Danielle co-hosted a private dinner and I was fortunate to be seated next to her. I have been reading Danielle’s weekly blog since I saw her last June on CNBC (via ZeroHedge.com). The piece was titled, “Another Fed ‘Insider’ Quits, Tells The Truth.” Read her blog, she’s really smart.

In a few short months, Danielle is coming out with a book titled, Fed Up. Our dinner discussion was honest, direct and candid. A bit of a peek behind the great curtain.

Honestly, I can’t tell you I feel any better and, in fact, I feel worse. Much of what I believe was confirmed.

Smart people were at the conference, like former Dallas Fed president Richard Fisher, and have tried to stress the business behavioral reactions to policy but, to be clear, there is not much hope in a change of monetary religion. Their hope to unleash animal spirits is not the outcome they are getting. They are guessing with blind faith in a flawed model.

Janet Yellen and her team of 750 plus PhDs are being tested. “… But if you want to test a man’s character, give him power,” said Lincoln. Of course, man is defined to be woman or man. Her character and her leadership, like Volker’s in the early 80’s, is at test.

Richard Fisher

The bottom line, in my view, is that the Fed lacks real world business experience. Banks are sitting on $2 trillion of the Fed created QE money and earning 50 bps. Free money… not getting into the system (i.e. loans). Zero (or near zero) bond interest rates have incentivized corporations to borrow for nothing and use the money to buy back stock and M&A. What future opportunity costs are being missed? What unintended behaviors have been created?

I was surprised to learn that there are over 750 PhDs on staff at the Fed. Academics educated in a Keynesian ideology. Expect helicopter money to come next and the direct buying of stocks.

Fisher has business common sense. And so does Danielle. Thus, Danielle has titled her soon-to-be-released book, Fed Up. Not sure if you feel any better. In fact, I don’t! I’m going to buy the book.

With thoughts on the Fed out of the way. Next is a summary of Yusko’s presentation in bullet point form. Short and to the point. So please email me if something is unclear.

Mark Yusko’s Presentation – There Goes The Boom

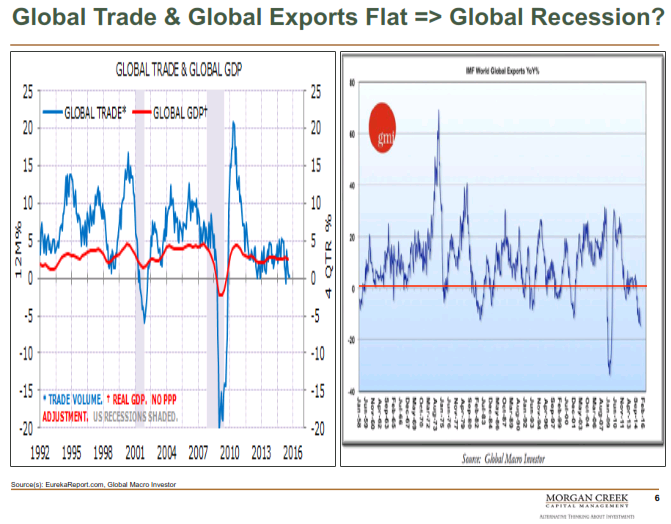

- Global trade has gone negative – it has never happened without a recession.

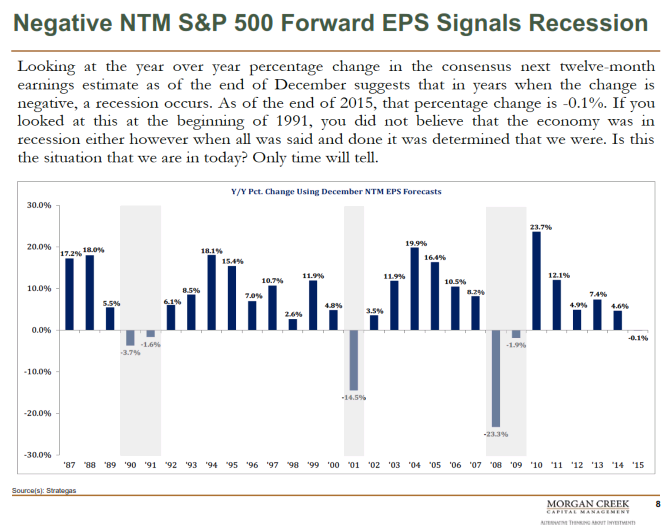

- Corporate earnings – six quarters of year-over-year decline: A leading economic indicator… it is probable that recession is coming.

- Bad companies are supposed to go out of business. Chesapeake Energy should not be able to borrow $4 billion.

- QE has kept too many poor quality companies in business.

- Interest rates are not going up. 2023 will be the secular low in interest rates.

- Yusko sees recession next year; however, if oil spikes higher, then recession will come sooner.

- Yellen will not raise rates this year. (SB here: to that end, we’ll find out in June or July. Christine Lagarde at the IMF and China have her by the short hairs – no rate increase or dollar will rise and China will respond in true currency war fashion and devalue the yuan).

- In February, Christine Lagarde put them all in a room (The Shanghai Accord) and said, “This ends now.” (Speaking about the currency truce and the plan to coordinate QE together.)

- Immediately following that February meeting, you saw a massive spike in futures buying activity. Yusko said, “Pretty amazing.” Here is a picture:

- On inflation – he said there isn’t any… there is no inflation. Everything is deflating.

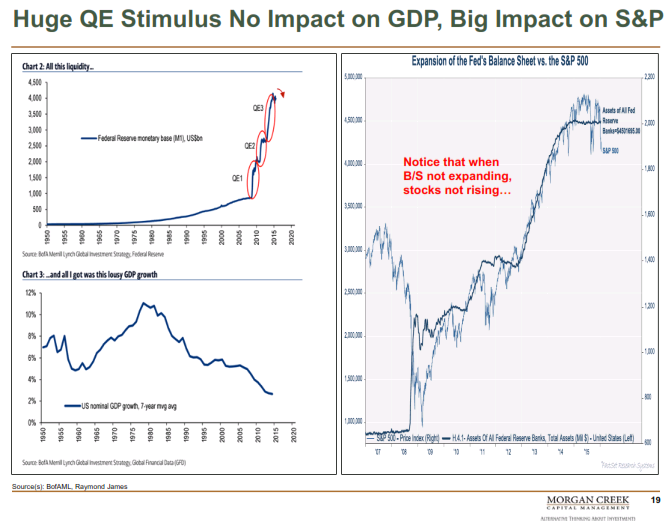

- The Fed will be talking about QE4 by the third quarter. This slide was cute:

- The huge QE stimulus has had no impact on GDP but a big impact on the S&P. Notice that every time they end QE, stocks do not go up.

- QE ended in 2014. The stock market is not up since then.

- Regarding Japan: Wherever the yen goes, Japanese stocks go. Yen goes down, then stocks go up and vice versa.

- The Bank of Japan owns one-third of JPY bonds and 60% of all ETFs (SB here: I recently showed they own 59%. Think about how crazy this is…).

- He said, “Yellen will buy stocks just like the Japanese.”

- Regarding oil, Yusko predicted $26 per barrel of oil and that happened. He then predicted $50 per barrel of oil by year end. He didn’t think it would happen as fast as it did (we are near $50 today).

- Adding: Oil takes 10 years to recover. You get a spike, then back down, spike, then back down.

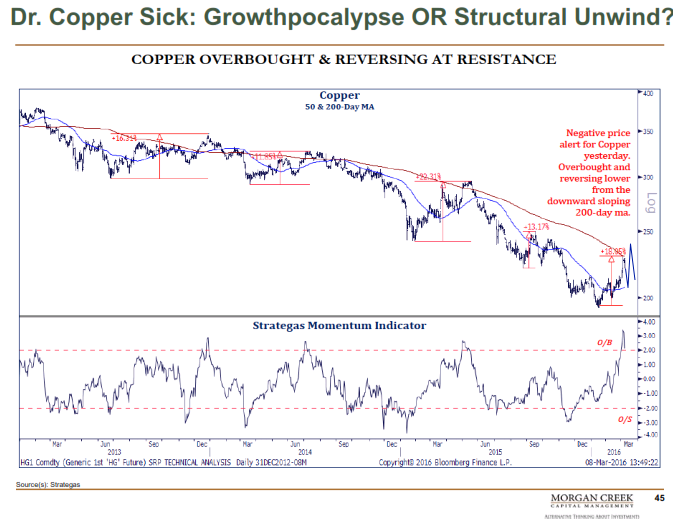

- He noted that “Doctor Copper” is telling us the world economy is in trouble.

- On the business cycle:

- Debt maturity calendar is large in the next few years – expect defaults.

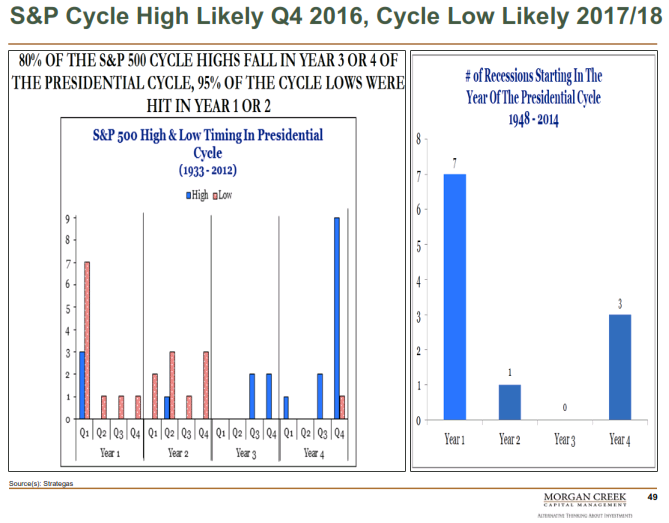

- Election year market tendencies:

- The S&P 500 market high typically occurs in the fourth quarter prior to a new president taking office.

- Recessions almost always start in the first year of a new president.

- This is an interesting fact he noted: the compounded annual return on the S&P 500, December 1999 to present, is just 3.5% (nominal – or before inflation).

- GMO is predicting negative real returns for the first time since 1999. (SB here: I shared his story with you last week… In 1999, when he told his UNC endowment board of directors that equity returns would be a negative 1.9% annualized for the next seven years, he was scolded by a board member. Then, like today, he recommends a shift away from equities.)

- GMO is predicting -2.3% for the next seven years (that is an annualized loss per year so think of it as a loss of approximately 20% compounded. Try telling that one to your retirement board or brother-in-law).

- He noted margin debt is at a record high. (SB: something we have been talking about for months.)

- Adding, “Stocks go down 6.5 times faster than they go up.”

- He thinks we are looking at a 2000 to 2002-like period all over again.

- “The problem with human beings is we sell what we need and we buy what recently worked.” (SB: If you are an advisor, I bet you are nodding your head along with me in agreement with this quote. Imagine telling your parents that you want to go into a business that plays games on human behavior – one where you need to convince your clients to buy the investment strategies that haven’t worked recently and get your clients out of the ones that have worked. This goes for stocks, bonds and any type of investment.

- Put 80% of your money in a well thought-out, disciplined, long-term investment plan. Don’t give money to your friend’s business – “but you will” and “you will lose.” Don’t give money to a strange new idea – but you will and you will lose. So set aside at least 80% into diverse assets (he likes index funds) but he recommends 100% to a diversified “endowment like, investment plan. (SB: he was funny in explaining this. I did those things and I lost and I learned.)

- On debt: “there is too much debt everywhere.”

- On emotions, he commented, “Do not make investments that feel good, you will lose your money.”

- All of the money that went into the market in January, February, March and April of 2000 went into tech stocks. Cisco was at $100 per share. It went to $8 and is now $24. It is never going back to $100.

- Most investors say to themselves, “I’ll get out when I get back to even.” Don’t do that…

- Advice on manager selection, he said, “Never buy a manager with a good three-year track record, buy a good manager with a long-term record and a crappy three-year record… you will do better.” (SB: good advice.)

A selection of slides from his presentation along with a few comments from me:

- I’ve been noting for some time (like the subprime time bomb we discussed in 2006) that one of the large systemic risks is a sovereign debt crisis in Europe. To that end, I found this next slide from Yusko’s presentation interesting:

- Here is the chart on the presidential election cycle:

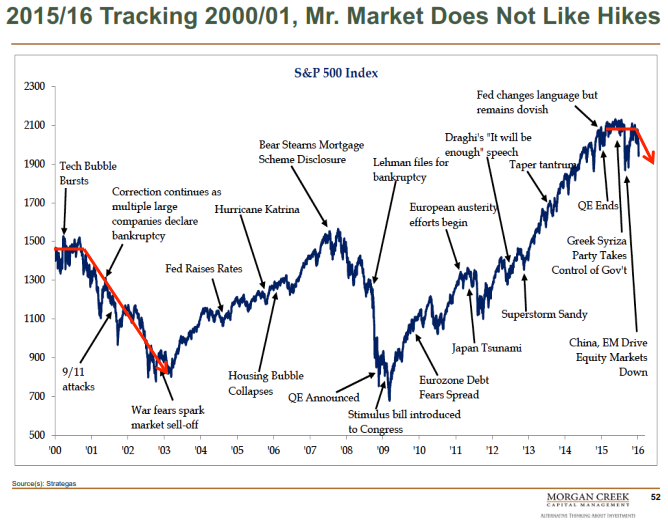

- Market doesn’t like rate hikes:

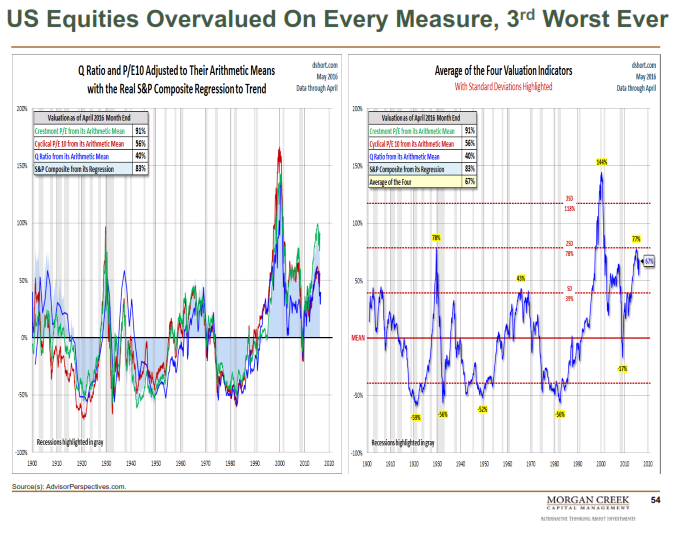

- On valuations (SB: this is data I share with you monthly)

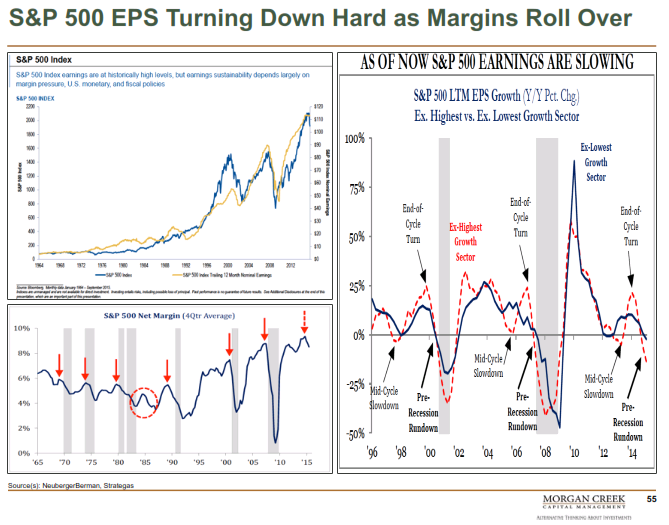

- If share prices stay high and earnings decline, you get an even higher overvalued market:

- Finally, because I’ve tortured you with enough slides and I’m pretty sure my edit team wants to shoot me right now, I’ll conclude this section with one last chart.

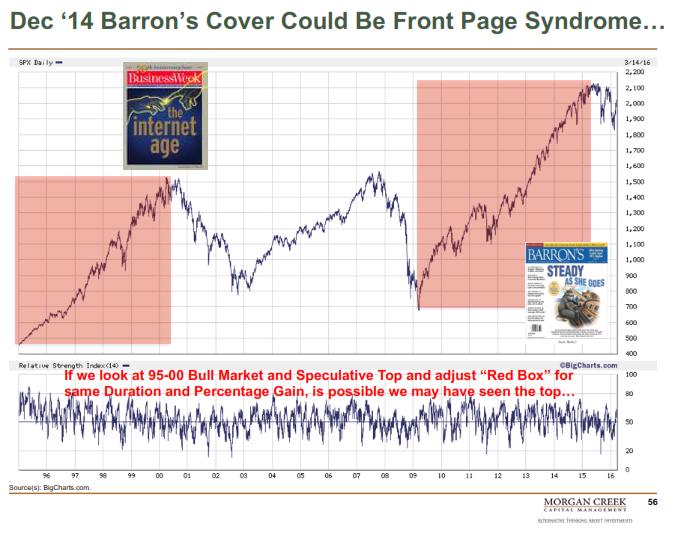

Do you remember the “front page” theory? When it becomes consensus that the market will forever go higher, you end up with some bullish print on the front page of a popular magazine and when bottoms are reached, you see something along the lines of this bear market will never end. To that end, Yusko shared this next chart:

Trade Signals – Global Recession Probability High, No U.S. Recession Yet

Click through to find the most recent trade signals. You can see how we are positioned in our CMG Opportunistic Tactical All Asset ETF Strategy. High yield remains in a buy signal as does the Zweig Bond Model (favors long-term bond exposure). Equity market trend evidence is neutral at best. Our CMG Ned Davis Research Large Cap Indicator remains in a “sell”. Here is a link to the Trade Signals blog page.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Concluding Thoughts – Portfolio Ideas

I’m going to share a few portfolio ideas with you, but please understand that the following is not a recommendation for you to buy or sell any security as I do not know your personal needs, time horizon, risk tolerance, goals or assessed suitability. Past performance is no guarantee of future results. Speak with your investment advisor and craft a well thought-out investment game plan. Ok, here I go:

First, the path to success is discipline and diversification. How you size the risks (all investments involve risk, including CDs and cash) in your portfolio matters. Here are a few ideas:

- Consider managed futures, global macro and tactical strategies. They have been largely out of favor over the last three years – find good managers and consider overweighting to these categories. I favor a 40% to 50% weighting. I like a mix of currency strategies (due to non-correlation or diversification benefits) and approaches that can go directionally long or short equity and fixed income exposure.

- Find ETF strategies that have the flexibility to invest globally. Blend together a few (3 to 5) experienced ETF strategists that have disciplined processes with the flexibility to move to fixed income, cash, sectors, internationally and even cash. Make sure they don’t have the same process and make sure their strategies can position to defensive asset classes.

- For your equity exposure, hedge your individual positions with out-of-the-money put options and consider writing covered calls to increase your yield and reduce the cost of the put options (think of it as “stock catastrophe insurance”).

- Incorporate a disciplined way to go flat with some of your equity exposure. Internally, we use the CMG Ned Davis Research Large Cap Momentum Index. We go long a low-fee large cap stock ETF on buy signals and we buy a Treasury bill ETF on neutral signals (See Trade Signals section below). To us, cash or BIL gives us an option to buy at a bargain sometime in the future. It also reduces our risk exposure. Find a disciplined way to do the same.

- There are also mutual funds that can give you equity market exposure but also have hedging processes built in.

- As for individual targeted risks (single position speculative plays), I am bullish on India and Mexico. I like using ETFs to gain exposure. I am bearish on Italy and France (consider buying put options on ETFs that give exposure to those countries).

- I am short-term neutral but long-term bullish on gold. A 5% to 10% portfolio max weighting.

- Hedge funds are not going away, but many will not survive. Fees will likely continue to come down. It may not feel like we need hedged strategies, but we do. Personally, I favor liquid access to hedge fund managers available within mutual fund 40 Act structures. (You are going to pay up for talent – I’d focus on net returns.)

- Think in terms of how much you are going to allocate to your three asset buckets: stocks, bonds and liquid alternatives. I favor 30-30-40 today and will switch to as much as 70-10-20 when equity market valuations become attractive again. That will happen in the next recession. Margin debt will unwind, selling pressure will be quick so a portfolio designed for defense today will be able to take advantage of the opportunity that will present. Patience is required today as will be the strong stomach required to take action when the time is right. Like the market lows in 2002 and 2009, it was hard to buy, but valuations were best and potential returns the greatest. My best guess is 2017… tied to recession, default cycle, etc. Much depends on the Fed and our fiscal authorities.

For now, participate but protect. And as Yusko concluded in his presentation, adopt the endowment approach.

To that end, I recently wrote a paper titled, “The Total Portfolio Solution.” You can simply reply, “TPS”, to this email to receive your free copy.

Personal Note – “Team Marv”

I lost my father four years ago to prostate cancer (men – get that PSA checked). Last night I drove up to my childhood hometown, State College, Pennsylvania, to attend the 20th annual Coaches vs. Cancer Charity Golf event. I’ll be playing the Penn State Blue Course with one of my father’s best friends, former PSU basketball coach Bruce Parkhill. Bruce started Coaches vs. Cancer 20 years ago.

He and my father had a wonderful relationship. They’d golf together a few times each week. They were crazy about each other. It was great to watch over the years. Dad was also a basketball junkie. With free access to the University’s facilities (Rec Hall), Dad played into his late 50s. He had an old timer’s one-handed press shot (he’d shoot the ball from his chest instead of above his head and would always surprise the students he’d play with and against).

Maybe it was basketball or maybe golf that brought them together. But it was friendship that bound them together. Bruce’s wife Arlene is joining our foursome. Two of nicest people you could ever meet. I’ll be holding back some tears when I see them. Our team today is called “Team Marv.”

Coach Bruce Parkhill, Tim Sommers, Arlene Parkhill and Ted Oyler

Finally, more to come on the Mauldin Conference in next week’s post. I also want to share with you the May month-end valuation metrics so stay tuned for that as well.

I hope you find this missive helpful. It is a labor of love but I do find the process helps me to focus in on what I believe is most important in regards to our long-term financial health.

If you want to spend a few extra bucks, you can order an audio replay of the Mauldin Conference sessions by clicking here. I believe you’ll also get the presentations. You’ll need to set aside some time, but I believe you’ll find it important for your financial health.

Wishing you a fun-filled weekend!

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History:

Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Following are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group

© CMG Capital Management Group