Fed: Almost Half of US Households Have Under $400 Saved

IN THIS ISSUE:

1. Fed Report: “Economic Well-Being of U.S. Households in 2015”

2. Americans Making $100,000+ Pay 80% of Federal Income Taxes

3. Be Sure to Read Today’s SPECIAL ARTICLES at the End

Overview

We begin today by looking at the recently released Federal Reserve study on the economic conditions of 50,000 randomly-selected US households. This annual survey attempts to capture a snapshot of the financial and economic well-being (or not well-being) of US households. Let me warn you upfront that some of the findings are really bad.

Following that discussion, I will reprint a recent study by FORBES which concludes that Americans who make over $100,000 pay almost 80% of all federal income taxes. That’s right. According to IRS data, Americans earning over $100,000 paid 79.5% of federal income taxes for 2014. This proves that top income earners pay more in income taxes than those who earn less.

Finally, I have two great opinion pieces in SPECIAL ARTICLES at the end that everyone should read, regardless of who you will be voting for in November.

Fed Report: “Economic Well-Being of U.S. Households in 2015”

Last week the Federal Reserve Bank released the findings of its third annual report on the economic and financial conditions of American households. The report is based on a comprehensive survey of over 50,000 individuals representing randomly selected US households.

The survey’s goal is to capture a snapshot of the financial and economic well-being of US households, as well as to monitor their recovery from the recent recession and identify any risks to their financial stability. It collects information on household finances that is not readily available from other sources.

The 2015 household survey focused on a range of topics, including:

- the personal finances of US adults;

- income and spending;

- economic preparedness and emergency savings;

- banking, credit access and credit usage;

- housing and living arrangements;

- auto lending;

- education and student debt; and

- retirement issues.

The findings of the 2015 household survey include some positive developments last year, as well as some very disappointing results. I will summarize them for you below.

Overall, individuals and their families continued to express mild improvements in their general well-being relative to that seen in 2013 and 2014. However, a number of adults still indicate that they are experiencing financial challenges, and optimism about the future declined modestly in 2015. For example:

- 69% of adults reported that they are either “living comfortably” or “doing okay,” compared to 65% in 2014 and 62% in 2013. However, 31%, or apprx. 76 million adults, are either “struggling to get by” or are “just getting by.”

- Individuals were 9 percentage points more likely to say that their financial well-being improved during 2015 than to say that their financial well-being declined.

- 22% of employed adults indicated that they were either working multiple jobs or doing informal work for pay in addition to their main job, or both.

- Only 23% of respondents expected their income to be higher in 2016, down from 29% who expected income growth in 2015 in the previous survey.

Over two-thirds (69%) said they are ‘living comfortably’ or ‘doing okay.’ I find that number very dubious. No other survey I know of puts the number remotely that high. It probably has to do with how the Fed asked the question.

Next, the Fed survey gets to a different round of questions, and the responses go downhill in a major way. For example, the survey asked how prepared for an emergency expense were the respondents. This is really bad:

- Nearly half (46%) said they did not have enough saved to cover an emergency expense costing $400, and would have to cover it by selling something or borrowing money.

- 22% of respondents experienced a major unexpected medical expense that they had to pay out of pocket in the prior year, and 46% of those said that they still owe debt from that expense.

The survey also asked respondents about several specific aspects of their financial lives, including their income and savings. Most respondents reported that they saved at least some of their income in the prior year. Income volatility/uncertainty, however, represented a major concern for many lower-income families.

- 68% of non-retired respondents said they saved at least a portion of their income in the prior year.

- 32% of adults reported that their income varies to some degree from month to month, and 43% reported that their monthly expenses vary to some degree. 42% of those with volatile incomes or expenses said that they have struggled to pay their bills at times because of this volatility.

The Fed survey also asked questions about household levels of education debt/student loans. Over half of adults under age 30 who attended college took on at least some debt (student loans, credit card debt and/or other forms of borrowing) while pursuing their education. The likelihood of falling behind on student loan payments varied depending on the type of institution attended and the level of education completed.

- In addition to any student loans, 21% of adults have education-related credit card debt. The median outstanding education-related credit card debt for those under 30 was $3,000. [This is lower than any other similar survey I have seen.]

- 21% of those who borrowed to attend a for-profit institution are behind on their student loan payments. Among those who borrowed to attend a public or not-for-profit institution, 7% and 5% are behind on their payments, respectively.

The Fed survey also asked questions regarding housing and living arrangements. Most respondents said they are satisfied with the quality of their house and neighborhood, although this varies based on the income level of the community. Additionally, most homeowners feel that their house appreciated in value in the prior year.

- 70% of all adults surveyed said they are ‘mostly or completely satisfied’ with the overall quality of their neighborhood, although only 35% of those in high-poverty areas report this level of satisfaction. [Here, too, I find this result dubious.]

- 51% of homeowners believe that their home value increased in the 12 months prior to the survey. 43% expect that home values in their neighborhood will increase in the next 12 months.

The survey also asked questions about retirement planning. Many individuals reported that they have no retirement savings, and – among those who are saving – a large number of respondents indicated that they lack confidence in their ability to manage their retirement investments.

- 31% of non-retired respondents reported that they have no retirement savings or pension at all, including 27% of non-retired respondents age 60 or older.

- 49% of adults with self-directed retirement accounts are either ‘not confident’ or only ‘slightly confident’ in their ability to make the right investment decisions.

- Just over 25% of adults with self-directed retirement accounts do not seek out any financial advice when investing these funds. 52% of those who do not seek out advice say they either cannot afford assistance or would like help but do not know where to get it.

These annual Fed surveys often raise more questions than they answer. The bottom line is that most US households are living on the edge financially. The fact that almost half of households do not have enough saved to cover a $400 surprise expense tells it all.

Now let’s move on to our second topic for today, a surprising new report from FORBES.

Americans Who Make More Than $100,000

Pay 80% Of Federal Income Taxes

by Kelly Phillips Erb May 18, 2016Here’s the dirty little secret that we don’t like to talk about: when it comes to income tax, top earners really do pay more in federal income taxes. According to recent Internal Revenue Service (IRS) data, Americans earning over $100,000 paid 79.5% of federal income taxes in 2014.

The preliminary data… indicates that 148,686,586 Americans filed individual income tax returns in 2014. Of those, only about 112,831,339 taxpayers reported taxable income (adjusted gross income less deductions). Of those, 96,612,233 taxpayers filed individual income tax returns showing $1.358 trillion in total income tax due. Total income tax is the sum of income tax after credits plus the infamous Net Investment Income Tax (NIIT). It does not include any of the other taxes that make up total tax liability including uncollected FICA (or Social Security) tax on tips, additional tax on income from nonqualified deferred compensation, and repayment of advance payments of the health coverage tax credit; those additional taxes would bump up the number of taxpayers to 101,021,848 owing $1.419 trillion in total tax.

The data shows that 23,745,195 Americans filed individual income tax returns reflecting adjusted gross income (AGI) of $100,000 or more in 2014, representing 16% of all returns. Of those, most (23,626,332) reported tax due (yes, it’s possible not to owe tax at those income levels). Those 16% of taxpayers paid $1.079 trillion in taxes or 79.5% of the total income tax paid.

I know what you’re thinking: what about all of those supposed tax breaks for the rich? What about Warren Buffett? The self-made billionaire Warren Buffett has attracted a great deal of interest for making comments suggesting that most wealthy Americans pay a lower tax rate than those who work for him, saying in 2007:

“I’m willing to bet anyone in this room $1 million that those rates are less than the secretary has to pay.”

In 2010, Buffett continued the conversation when he announced that he paid an effective tax rate of just 11.06%. Today, Buffett is the third wealthiest person in the world with a current net worth of $67.2 billion…

And here’s where the math can get funny. While the top 16% of Americans paid nearly 80% of taxes by dollars, that doesn’t mean that they paid an 80% tax rate. Don’t conflate percentage of all taxes paid with tax rates. Remember, we have a progressive income tax. With a progressive income tax, the rate of tax increases as taxable income increases but – and it’s a big but – everyone pays the same rate for the same income.

Here’s an example: Let’s assume you have taxable income of $100,001 as an individual. You might look at a tax table and assume your tax rate is 28%. But that’s your marginal tax rate or more simply, your top rate. For federal income tax purposes, every dollar that you make over $100,000 will be taxed at 28% until you hit the threshold for the next rate. But every dollar that you made from the first dollar was not taxed at 28%.

That’s because every dollar of taxable income (income figured after deductions, exemptions, exclusions and other adjustments) from zero dollars to $9,225 is taxed at 10% for every person filing as single. Every dollar of taxable income from $9,226 to $37,450 is taxed at 15% for every person filing as single. Every dollar of taxable income from $37,451 to $90,750 is taxed at 25% for every person filing as single. Every dollar of taxable income from $90,751 to $189,300 is taxed at 28% for every person filing as single. In other words, all taxpayers in the same filing status are taxed at the same rate for the same income.

(Those are numbers figured using the tax rates for 2015…)

It’s typically more helpful to look at the effective tax rate. The effective tax rate has different meanings depending on the context but at its most simple, it’s calculated by dividing your total tax by your taxable income.

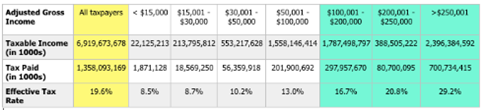

Using that math, the effective tax rate for all taxpayers in 2014 is 19.6%. The effective tax rate for taxpayers making more than $100,000 in 2014 is just a bit higher: 23.6%. Here’s how it breaks down:

Huh? That doesn’t seem to jive with what I said earlier about 16% of taxpayers paying 80% of tax. Why not? You have to look at all of the numbers in context. While it’s true that taxpayers reporting over $100,000 pay most of the total taxes, it’s also true that they generate most of the income. The top 16% of taxpayers reported $5.574 trillion in adjusted gross income (AGI): that’s 57.7% of the total adjusted gross income for all taxpayers.

The numbers are even more stark when you look at taxable income: the same 16% of taxpayers were responsible for generating 66% of all taxable income. When you think about it in those terms, the numbers begin to make a little more sense: those that generate the most taxable income pay the most in total tax by dollars. Whether that’s “fair” or not is another story.

Keep in mind this is preliminary data which means that it represents estimates of income and tax items based on a sample of individual income tax returns for 2014 filed between January and late September 2015. Returns are weighted to represent a full year of taxpayer reporting. That means some data gets left out – in this case, it’s mostly data for those filing last minute tax returns on extensions. Those tend to be – though not always – higher income taxpayers.

You can get a better handle on figures by using the IRS’ complete year data, but the problem with that is that it tends to be a bit old and doesn’t reflect contemporaneous data or changes in the tax laws. In our case, preliminary data (what I used) is available for 2014, but the last set of complete data available dates back to 2011.

It’s also important to remember that this data focuses on income tax rates, not other taxes such as Social Security and Medicare taxes. If you factor those in, the rates look very different. Medicare taxes are flat (all taxpayers pay the same 1.45%) as are Social Security taxes (all taxpayers pay the same 6.2%), but they are capped so that taxpayers who make over $118,500 do not pay Social Security tax on the amount over $118,500. Additionally, under a law that kicked in beginning in 2013, an employer must withhold additional Medicare tax of .9% from wages paid to an individual earning more than $200,000, regardless of filing status or wages paid by another employer.

END QUOTE

All the best,

Gary D. Halbert