Emerson Electric: High-yield, Sound Valuation and 59 Consecutive Years of Dividend Increases, Part 2

Introduction

When I’m looking for a stock to add to my portfolio, there’s nothing more frustrating than spending a significant amount of time and effort on research - only to discover that the company in question is significantly overvalued. Consequently, my first step always starts out with an assessment of the relative valuation of the company I am considering. No matter how much I admire the company, its management team and its financial health and strength, I simply refuse to pay more for a stock than I believe it is worth. The most commonly accepted investing principle is to buy low and sell high.

In Part 1 of this two-part series. I ran the blue-chip Dividend Aristocrat and Champion Emerson Electric Company (EMR) through many variations of time-honored fair valuation measurements. My general conclusion was that Emerson Electric was reasonably valued, and therefore, worthy of conducting a more comprehensive research effort on.

Since the time that Part 1 was written, Emerson Electric’s stock price has increased approximately a couple of dollars per share. Nevertheless, I still consider it comfortably within a fair value range, but obviously not as attractive as it was last week. As a result, investors might want to wait for a better entry point. However, there’s no guarantee that that would happen.

Sidebar on Emerson Electric’s Valuation Calculations

After posting part 1 of this 2-part series, I received several questions regarding how I calculated the fair value multiple that I applied to the earnings and cash flow metrics that I presented. Here is what I wrote in part 1:

“With these 10-year average calculations in hand, I can run what I consider conservative fair valuation levels for each of these metrics measured against Emerson Electric's current market price of approximately $50.75.

For cash flow, I apply a historical normal cash flow value multiple of 9.5 which gives me a fair value price of $49.00. This is approximately $2 below Emerson Electric's current price. This valuation method suggests that Emerson Electric is mildly overvalued based on cash flows, which is important from a dividend perspective.

For operating cash flow, I apply a normal price to operating cash flow multiple of 12.4, which gives me a fair value price of $50.22. This valuation method indicates that Emerson Electric is fully valued based on the market's historical operating cash flow multiple.

For operating earnings I apply Emerson Electric's normal P/E ratio for this timeframe of 16.9, which gives the fair value price of $50.70. This valuation method indicates that Emerson Electric is fairly valued based on the market's historical operating earnings multiple.

For free cash flow I apply Emerson Electric's 10-year historical normal price to free cash flow multiple of 15, which gives me the fair value price of $50.10. This valuation method indicates that Emerson Electric is fairly valued based on a reasonable price to free cash flow.”

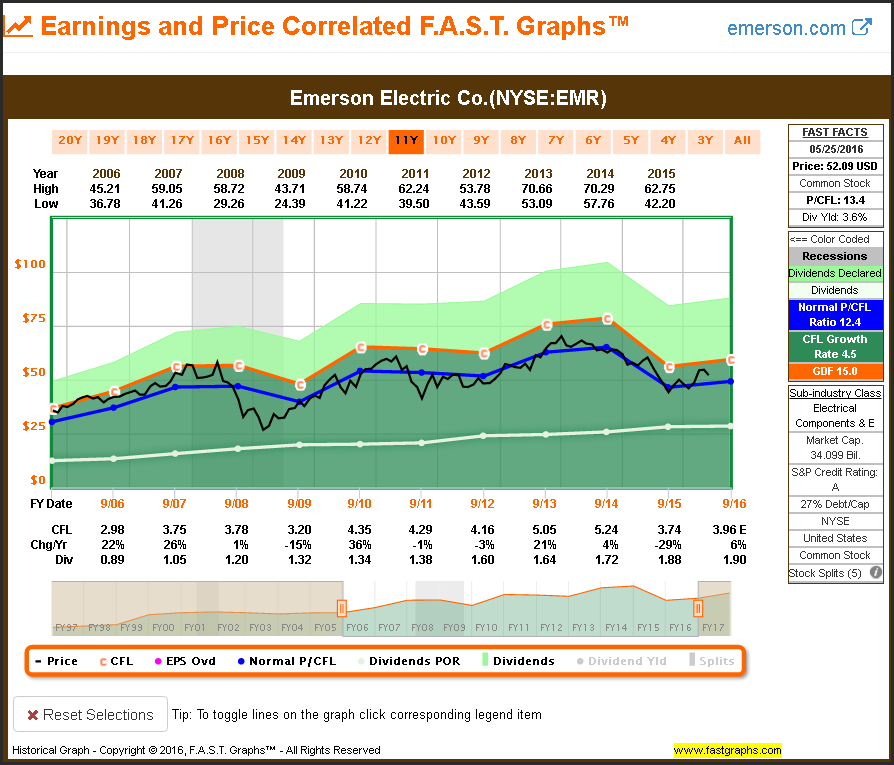

In order to come up with these calculations, I utilized F.A.S.T. Graphs™ which automatically ran these calculations for me. For example, the following 10-year operating cash flow and price correlated graph on Emerson Electric reflects the normal 12.4 multiple I referenced. I offer this example to provide an opportunity to elaborate on statistical references such as a historical normal valuation metric.

The blue line on the following graph represents a normal price to cash flow multiple of 12.4. Therefore, anywhere the price of the stock (the black line) touches the blue line it is trading at a price to cash flow multiple of 12.4. Obviously, when the price is above that line the multiple is higher, and when the price is below that line the multiple is lower. Consequently, the blue line serves as a valuation reference that can be analyzed over this entire timeframe. In other words, it is a valuation that the market has most commonly applied to Emerson Electric based on cash flows over the time period being measured.

On the other hand, it is not perfectly precise across the whole time period. There are times when the market valued Emerson Electric higher, and times when it valued Emerson Electric lower. Nevertheless, it clearly represents a reasonable valuation reference within a reasonable range of accuracy. Currently, Emerson Electric is trading at a price to cash flow multiple of 13.4 which is modestly above the 12.4 average. Therefore, I believe it is logical to state that Emerson Electric might be fully valued based on this metric today, but not significantly overvalued. Stated differently, Emerson Electric appears prudent based on its operating cash flow valuation, but not necessarily cheap.

Emerson Electric: Researching the Business behind the Stock

My approach is to position myself as a long-term shareholder of the business rather than speculating in the stock. Consequently, once I have determined that fair valuation is present, my next step is to dig deeper into the business that I am considering investing in. Therefore, I like to remove the distraction of stock price from my analysis at this stage in the process and focus solely on how the business has historically performed.

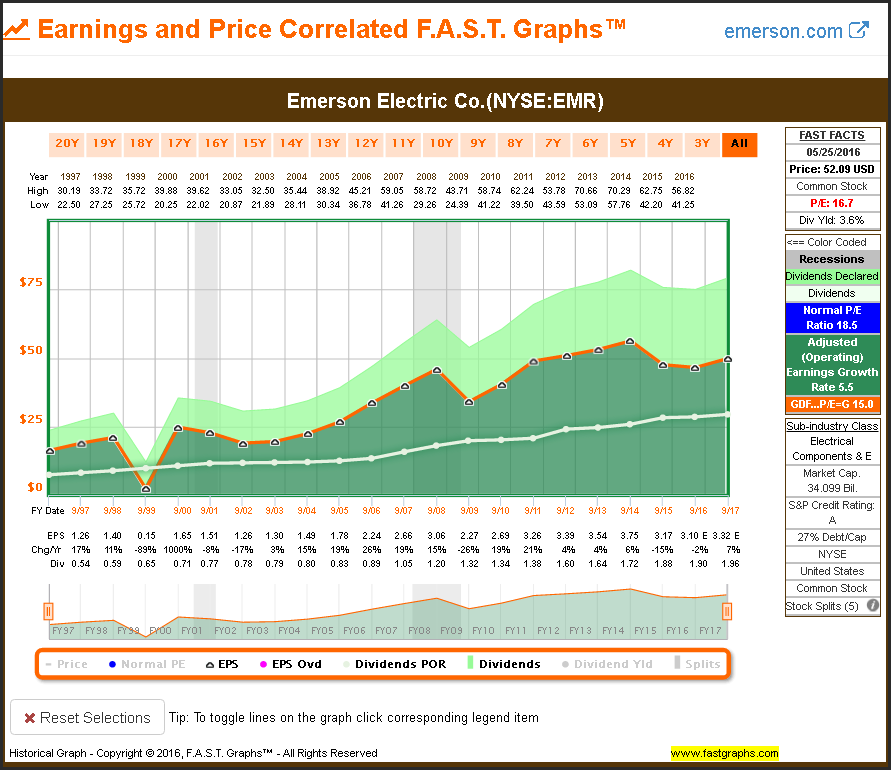

Additionally, my focus is also placed upon how the company satisfies the primary investment objective that I am seeking by investing in the business. In the case of Emerson Electric, my primary investment objective is for achieving an above-average and growing current dividend yield. Therefore, the dividend line (the honeydew green or white colored line) represents my primary focal point. Emerson Electric is a Dividend Aristocrat and Champion that has increased its dividend for 59 consecutive years. My graph only goes back to 1997; however, it is clear that Emerson Electric has steadily increased its dividend each and every year.

On the other hand, as indicated in part 1 of this series, a review of Emerson Electric’s historical operating earnings (the orange line on the graph) clearly indicates periods of cyclicality. This simply means that Emerson Electric has not historically grown their earnings each and every single year. This is simply what is meant by referring to Emerson Electric as a cyclical stock.

Nevertheless, this does not mean that the company produces losses from time to time. A review of the operating earnings below illustrates that Emerson Electric has been a profitable enterprise even during cycles when earnings were falling from the previous year. More simply stated, Emerson Electric is a profitable business even during down cycles which partially explains why they have been able to continue to grow their dividend over so many decades.

When I am initially examining a business for prospective investment, I start out by reviewing its long-term earnings performance as I did with Emerson Electric above. Next, I like to also look at its historical cash flow generating performance. Examining cash flows is even more relevant when I am evaluating a dividend-paying stock. Clearly, Emerson Electric is more than adequately covering its current dividends with strong cash flows, even during down cycles.

In spite of Emerson Electric’s moderate level of cyclicality, the company’s dividend record has been impressive and I really like its current yield considering today’s low interest rate environment. Therefore, I am motivated to take a deeper look at the financial health and vigor of this cyclical business. Of course, this implies diving into the company's financial statements.

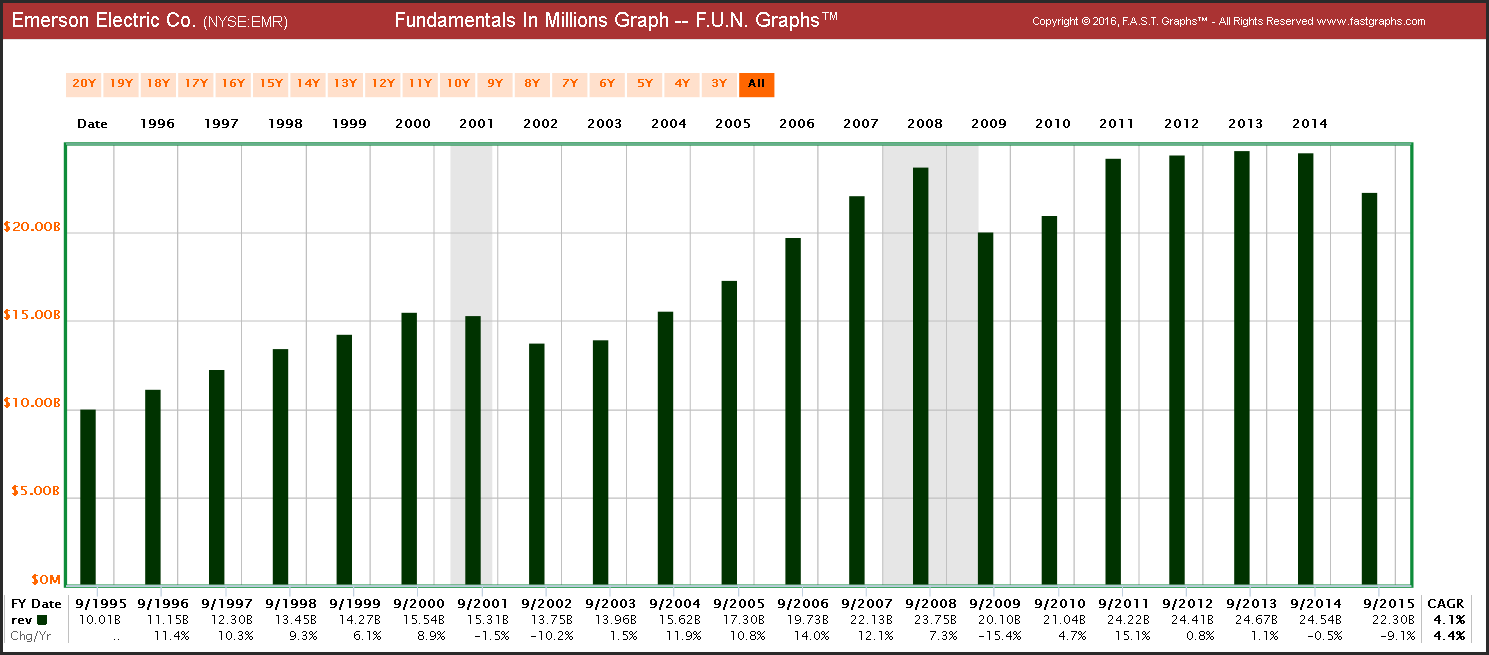

The first metric I like to examine in the financial statements is revenues. Bottom-line results like earnings must start and come from the top line. Additionally, accounting conventions coupled with financial engineering could possibly paint a rosier earnings picture than is deserved, whereas top-line results clearly illustrate whether a business is truly solid or not. I like to look at revenues from two perspectives. First, I examine gross revenues in dollars. Emerson Electric’s long-term revenue growth has been generally strong with only moderate periods of cyclicality as depicted below:

However, since I am also a passive shareholder, I also like to look at revenues per share. Revenues per share can be impacted by what some call financial engineering in the form of share buybacks. On the other hand, as I will later illustrate, share buybacks can be a positive or a negative depending on the company's stock valuation at the time and/or whether or not the company has a good use or need of its cash to fund future growth. Emerson Electric’s revenue per share record is consistent with its gross revenues.

After reviewing a company's top line, I like to turn my attention to profitability. At this point, I am interested in determining how much profitability the company generates per dollar of sales. To evaluate this, I look at gross profit margins compared to net profit margins. Emerson Electric generates very high gross profit margins, which I consider a plus.

My personal benchmark for net profit margin on a growth stock is 15% or better. However, that is too high a standard to apply to cyclical stocks with significant manufacturing components. Therefore, I prefer to measure cyclical stocks net profit margins relative to its sector norms. The NYU Stern School of Business produced a review as of January 2016 that shows net margins for Emerson Electric’s subsectors average between 6% to 8%. Emerson Electric’s net margins have typically been above that range, and have been increasing over the last few years. Therefore, relative to many of its peers, Emerson Electric generates strong net profit margins.

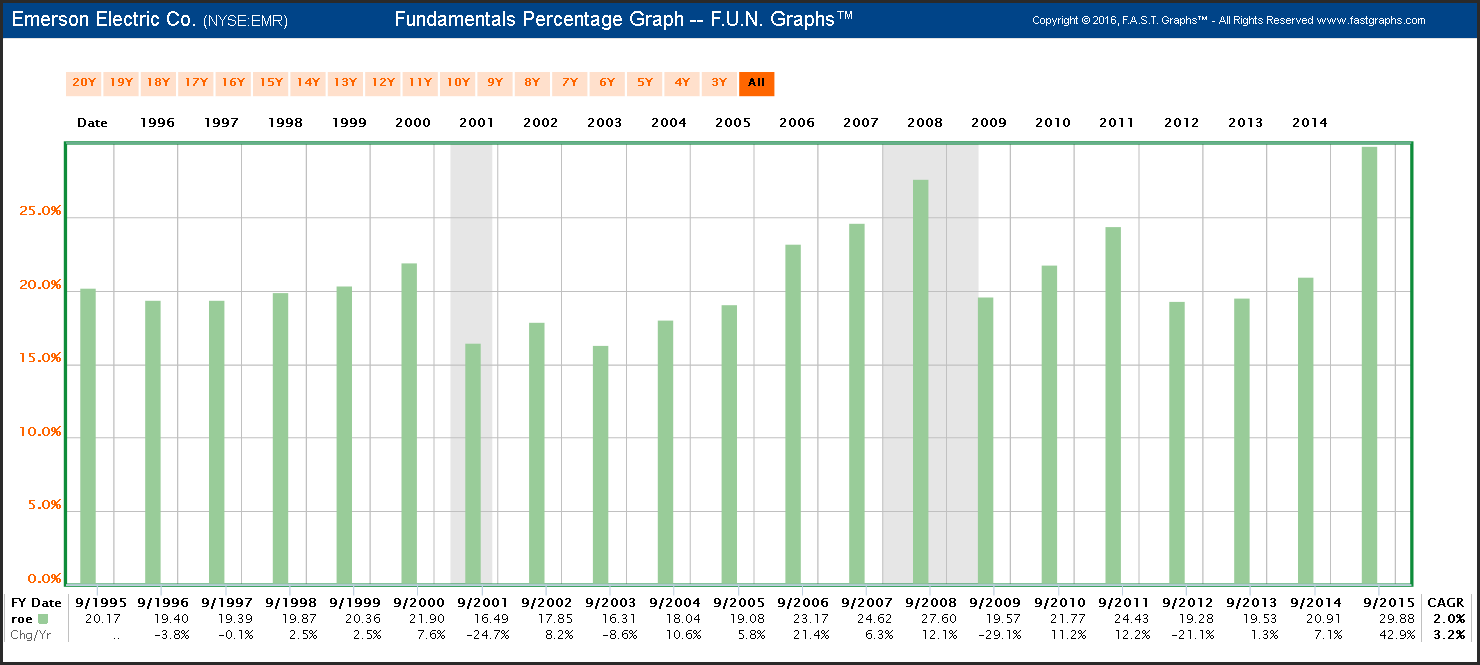

After I have reviewed profit margins, I typically turn to analyzing return on equity. As a shareholder, I consider this metric important because it essentially measures the return the company is earning on shareholder money. I am quite comfortable when I see a return on equity of 10% or better. Emerson Electric earns returns on equity significantly above this threshold. One caveat regarding return on equity is that companies can boost it by taking on more debt. Consequently, I put more weight on this metric when debt levels are reasonable - as is the case with Emerson Electric.

Thus far, I've illustrated some of the go-to metrics that I like to look at when evaluating the strength and health of a business I might be interested in investing in. However, I don't stop here. Additionally, I thoroughly examine the company's balance sheet, cash flow statement and income statement. These financial items are available from numerous sources. Personally, I utilize F.A.S.T. Graphs™ and FUN Graphs (fundamental underlying numbers) to facilitate a deeper look into the company's financials.

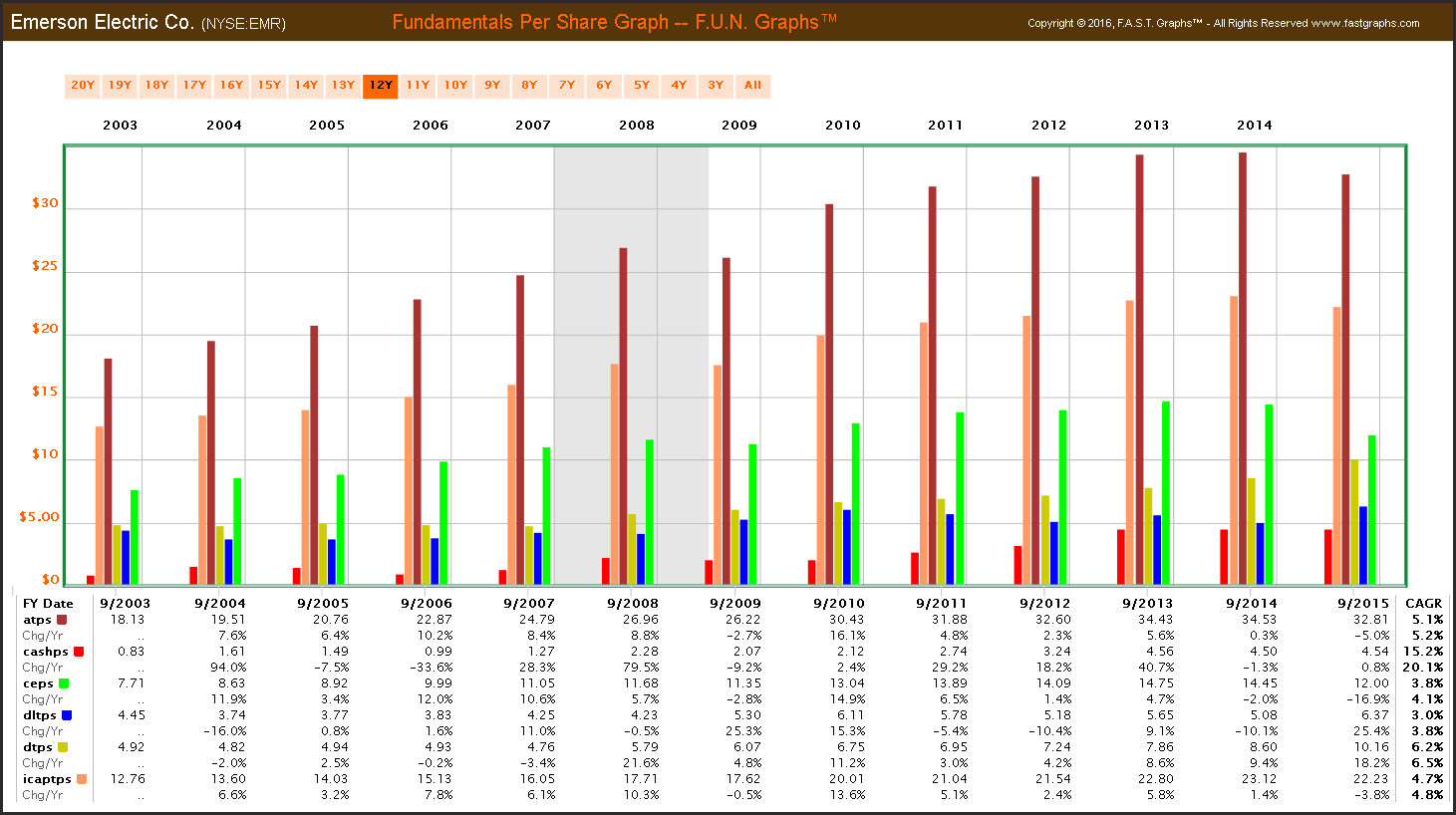

I typically start out by examining all of the metrics together on the company's balance sheet, cash flow statement and income statement. Here is a sample of Emerson Electric’s balance sheet, which includes assets per share (atps), cash per share (cashps), common equity per share (ceps) - also known as book value, debt long-term per share (dltps), debt to total per share (dtps) and invested capital per share (icaptps).

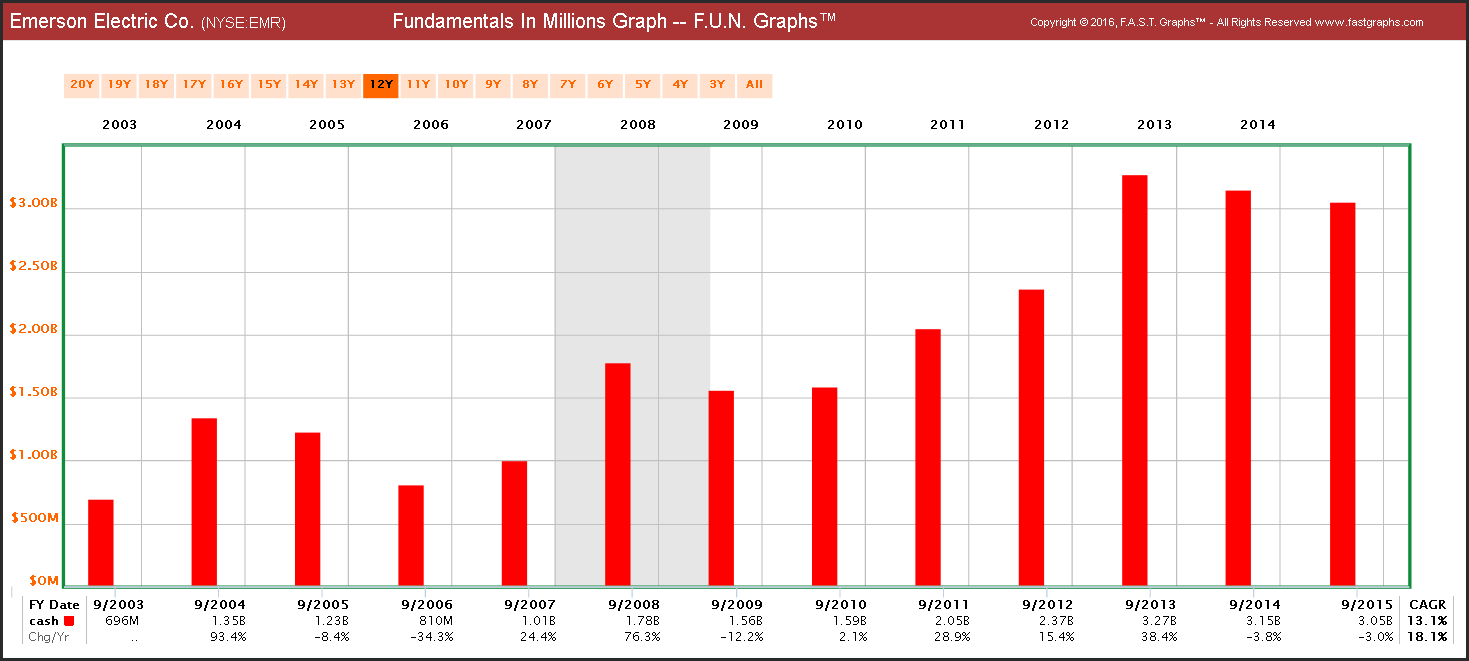

Additionally, I will look at each metric on the balance sheet one at a time in order to focus more clearly on each metric. Here's an example of Emerson Electric’s cash. Clearly, Emerson Electric possesses significant financial resources and flexibility.

Learning About The Business

Once I have thoroughly examined a company's financial results, health and strength, I typically turn my attention to learning as much as I can about what the company does and how it makes its money. The easiest way to do that is to simply follow the link on my F.A.S.T. Graphs to the company's website. Although I recognize that much of what I will find will be company propaganda spun as positively as they can, I can also learn a lot about the company's products and various business enterprises. Here is a snapshot from Emerson Electric’s website illustrating key product areas with specific links to each. If I'm seriously interested in investing in the company, I will peruse each of those links. Emerson Electric could currently be described as a conglomerate operating in several diverse industry segments.

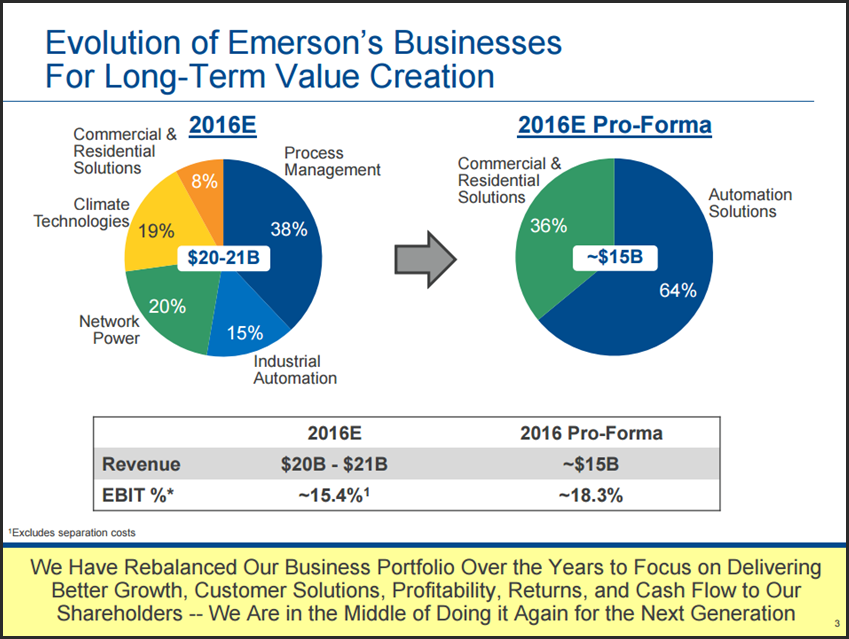

However, Emerson Electric has a legacy of transforming and evolving their business to stay current. The following slide from their 2016 Investor Conference reveals their transformation from 1990 to 2000.

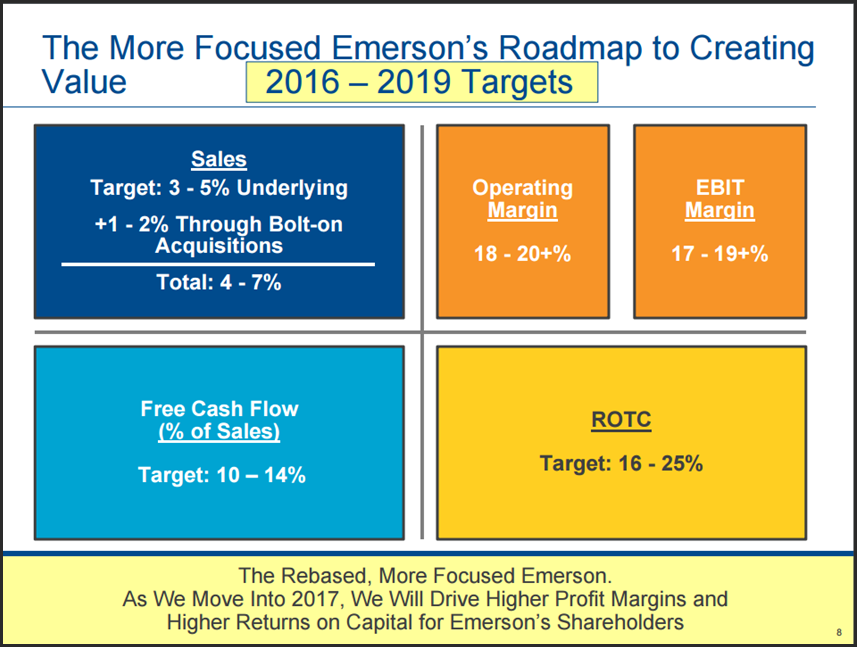

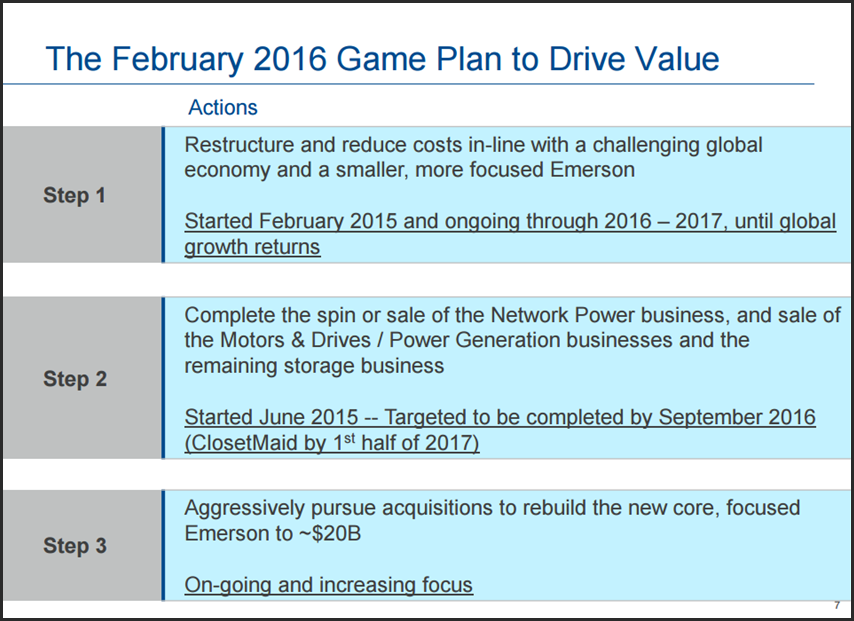

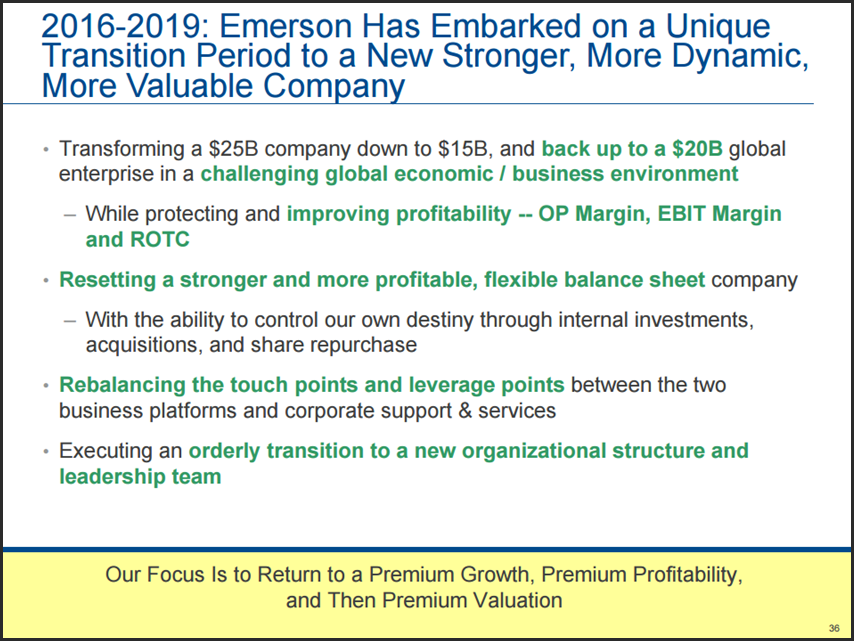

These next slides reveal that Emerson Electric’s management expects to be very active in transforming the company for 2016 and beyond.

Emerson Electric’s strategic transformation is designed to create a more focused Emerson Electric. Their ultimate goal is focused on increased profitability and strong cash flow generation.

An integral aspect of their strategic transformation includes both divestitures and strategic acquisitions. Management is contemplating either spinoffs or direct sales of certain business segments. Although the exact form that these divestitures will take is still under consideration, I believe either strategy will directly benefit existing shareholders. However, the precise benefit is only conjecture at this point.

Emerson Electric’s endgame is to create a better balanced and more focused business model designed to enhance profitability and future growth. Although Emerson’s transformation is an ambitious undertaking, the company has a long history of evolving and adapting. Nevertheless, in addition to the historical cyclical nature of their operating history, this transition does create a level of uncertainty. On the other hand, as indicated above, Emerson Electric has the financial health and strength to execute, and a management team that has the experience to get the job done.

ZACKS Research Reasons to Buy Emerson Electric

In addition to learning as much as I can about a company via its website, I also like to check other resources to see what they have to say. This would include searching for articles on financial blogs such as Seeking Alpha or Gurufocus, prominent financial newspapers such as the Wall Street Journal as well as research services that I subscribe to. My objective is to learn as much about the business and its future potential as I can.

For example, ZACKS Research will typically provide reasons to buy a company and reasons to sell. I like this balanced approach because it provides both the positives and the negatives regarding the company I am researching.

Currently ZACKS presents several positives on Emerson Electric. They site improving trends in US construction and Emerson’s historical approach to mergers and acquisitions. They also favor Emerson’s cost cutting and restructuring initiatives. And they feel confident regarding Emerson’s transformation and streamlining efforts.

On the negative side, they reference the current turmoil and volatility in the oil and gas market and weak economic conditions in the industrial markets. They also point out headwinds in China and other markets potentially weighing on underlying future sales growth.

The ZACKS Research is only available to subscribers. However, there are numerous other sources that prospective investors can examine that are not subscription based.

Emerson Electric: Investment Thesis

From the perspective of capital appreciation, I believe the best time to consider investing in a cyclical stock is during a down cycle. However, that does not mean having the insight to purchase at the absolute bottom. This is impossible, but identifying a down cycle is certainly possible. I believe Emerson Electric is currently in a down cycle, and I believe the company is taking the necessary steps to propel the business to their next up cycle. On the other hand, cyclical stocks are not typically your best choice for maximum capital gain.

Even so, my interest in Emerson Electric is not maximum total return. Instead, I am looking for a predictable long-term dividend income stream and growth thereof. Emerson Electric is not only a Dividend Aristocrat and Champion; it is also a member of a more elite list known as Dividend Kings that only contains 18 companies that consecutively increased their dividend for 50 years or more. I’m not absolutely certain who created this list, but I came across it from the website Sure Dividend.

What I found most interesting about this list is that many of the companies on this list are cyclical stocks. As a result, they don’t have the highest long-term growth rates, however, their historical records of increasing their dividends each year are virtually second to none. Although this is pure speculation on my part, it might suggest that the management teams of these Dividend Kings recognize that in order to attract and retain shareholders, they need to compensate with an impeccable dividend policy.

Summary and Conclusions

I offer Emerson Electric as an attractive high quality dividend growth stock currently available at attractive valuation. The company offers a high current yield, has an A S&P credit rating, and a debt to capital ratio of only 27%. The company is currently in transition, but this is nothing new for this company that has been in business since 1890. If high current income with the opportunity to see that income grow is your objective, then I suggest taking a close look at Emerson Electric.

Disclosure: Long EMR

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.