“Let yourself be silently drawn by the strange pull of what you really love. It will not lead you astray.”

-Rumi

Sometimes it is good to sit back, reflect, recharge and then, once again, drive forward. I pulled open a drawer and found, tucked at the bottom of a pile, a few notes I wrote down many years ago. Notes from Mom… I wanted to remember her.

She would tell me, “Act as if all you wish to create has already occurred. See the end result. Close your eyes and feel what it feels like celebrating that result. Know it to be true – then let it go, be patient and watch the miracles line up. Chance meetings. A call from a friend. Walk forward in knowing and trust that you will create great things.”

She’d say, “Quiet your mind and listen to your thoughts. Identify what you intend to create. Speak it out loud. Write it down.” Then she’d gaze intensely with her gray blue eyes and say, “Now go out and pursue it with a pit bull-like determination. Steve, you’ve got to do the work to make it happen.”

Sounds like sage advice for our politicians. Where is that candidate? I think I’m voting for my mom for president. And yours too.

Ok, I feel a bit more inspired. Recharged, energy high, what to create next. Thanks, Mom. Needed that!

What I do know is we humans will find our way forward. Let’s do it with great joy for ourselves, our families and collectively for each other. But we’ll need to think big and do the hard work. We have borrowed too much and saved too little.

As for the markets, I believe forward 10-year returns will be in the low single digits and the ride will be bumpy.

Speaking of looking forward. Here is Bill Gross from his recent post titled “Culture Clash”:

“Prepare for renewed QE from the Fed. Interest rates will stay low for longer, asset prices will continue to be artificially high. At some point, monetary policy will create inflation and markets will be at risk. Not yet, but be careful in the interim. Be content with low single digit returns.”

On my worry list is the China debt mess (far larger than the subprime bomb that exploded in 2008), a sovereign debt crisis in Europe, political inaction, geopolitical event risk, a coming pension crisis (overpromised, underestimated and significantly underfunded) and negative interest rates across much of the developed world.

On the plus side, the U.S. looks comparatively strong – that favors international capital flows. Picture investors fleeing negative interest rates in Europe and Japan as policy moves, negative interest rates and a probable debt crisis drives capital to U.S. stocks and bonds. A kind of an international flight to safety. More buyers than sellers the story goes. This means that what is overvalued can grow to be even more overvalued. Yet, on the other hand, international panic, despite the positive flows, may not be good for U.S. stocks; though such an event will likely be bullish for U.S. government bonds. Risks… all investing involves risk.”

With that said, there is an interesting statistic out about Japan. You may recall that part of their stimulus (QE) program involves buying ETFs. In April, the Bank of Japan bought $2.7 billion in ETFs. Brace yourself. This brings their ownership up to 59% of all of the ETFs available in Japan. That takes “whatever-it-takes” to a whole new level. Not sure if I feel safe (with Central Bank’s setting a possible downside risk floor) or scared out of my mind.

I think back to Leon Cooperman’s quote, “bull markets are born on pessimism, grow in optimism and die in euphoria.” No clear euphoria just yet. We advisors are told we should know which bet to make. This is an economic experiment of unprecedented proportion. Diversify your set of bets.

Goldman says sell stocks. Druckenmiller says sell stocks and buy gold. El-Erian says put 25% in cash. I find myself in the risk is high camp but we could go 20% higher before we go 50% lower. Thus, I believe it is prudent to own equities but hedged. Reduce exposure. Find non-correlating diversifiers. It’s time to play defense so you can be in the favorable position (with capital largely preserved) to play offense when the getting gets good. And it will get good again.

Why? It is in times of dislocation that leverage (pay attention to the current record high margin debt) quickly unwinds. At such times, “stocks for the long haul” turns quickly into “get me the hell out” and it is that behavior we must mentally prepare for and protect against. It is that behavior that will create our next great buying opportunity. Stay patient until then.

I wrote about and knew that it was going to be bad in 2008. The problem is I started writing about it in 2006. There is a lot that can go wrong on the way to being right and getting the wrong right is not so easy to do. I knew it would be bad, but I never imagined we’d reach the near collapse of our entire financial system.

China’s debt problem is that bad, but will that take down the system? I don’t think so. Mario Draghi’s “whatever it takes.” Politicians stepping up and doing right. Needed structural reform? Not just yet, I’m afraid, so I think recession is likely within the next 18 months and it is recession that the equity markets hate the most. Expect a -30 to -60 percent decline if the past is any guide. The implications, at least to me: Risk management is important, especially when the market is so richly priced.

So I think of what we learned from our moms. Now may be the time to, “Quiet our minds and listen to our thoughts. Identify what we intend to create. Say it out loud. Write it down. And, importantly, let’s “go out and pursue it with pit bull-like determination.”

We need to do the wind sprints. It is hard work but we’ll then find ourselves in far better shape. Let’s do it and we’ll create something great.

I enjoyed Bill Gross’s piece “Culture Clash” which I share with you via a link below. That, along with a few charts of interest, and I did promise you a quick summary of the Sam Zell / T. Boone Pickens session from the SALT Conference. The two reflected on their careers, discussed opportunity in America, and argued about the need for political change in America. Some notes:

- Zell: “We live in an environment where there is unending opportunity. Anyone who says there is no opportunity, just talk to Mark Zuckerberg.”

- Zell: “The biggest issue is the regulation of our businesses has become so repressive that the ability to achieve has been brought down by regulatory burdens.”

- Does it matter who is President? Zell says absolutely. “Building a business is like building a wall of bricks.”

- “Businesses are built on the confidence of their owners… that they believe in tomorrow, that they believe in new markets. [The owner] isn’t always right, but it’s that belief. You have to have confidence in leadership and your country. How can you make commitments when the rules change [regularly].”

- “I’ve never thought about what a President would do for me,” said Zell. “Only what a President won’t do to me.”

- On Pickens: He was challenged by an Oklahoma Congressman who said that Pickens was in the office the previous day asking for the Congressman to do something for him. Pickens replied, “You’re misunderstanding. I wasn’t asking you to do something for me. I was asking you to not do something to me.”

- On the election, Zell said that Americans are looking at the execution of the policies when making a decision for President. He said, “I believe that the Trump phenomenon is about the revulsion regarding the government’s inability to execute.”

- Pickens and Zell also argued that the government has failed to incentivize work and has increased the cost of employment in the nation, while increasing dependency on government.

I am racing to catch a train to New York. I will be a guest on Liz Claman’s “Closing Bell” on Fox Business News today. You’ll see what a middle-aged dude looks like in bad makeup by clicking to see the interview here. I’ll then be racing back home to catch tonight’s Philadelphia Union vs. DC United game. Susan and the boys will meet me there. Peanuts and a cold IPA await.

On Tuesday, I’m heading to Dallas for Mauldin’s Strategic Investment Conference in Dallas. I’m going to arrive early to meet with John and several other ETF strategists prior to the conference kick-off. An impressive lineup of speakers, including: Richard Fisher, James Grant, Lacy Hunt, David Rosenberg, Gary Shilling to name just a few.

I’ll share some of my high level notes with you next week. Here is a look at the agenda. (This takes you to the home page and click on Agenda at the top.)

Ok – Grab that coffee and dive in.

Included in this week’s On My Radar:

- Culture Clash – Bill Gross

- A Couple of Charts I Found of Interest

- Trade Signals – Fed Minutes: Odds of a Rate Hike…Up

Culture Clash by Bill Gross

Michael Bloomberg hit on an important topic at the SALT Conference – the robotization of industry. Frankly, it is coming to the financial industry both in terms of automated investment platforms or the robo advisor, but also to how we might interact with clients online. Bloomberg noted that robots might replace humans in up to 40% of jobs. You see it now in manufacturing plants. It is coming folks and we need to think about the implications.

Bill writes about the generational divide between Boomers vs. X-ers and Millennials but this is the part that jumped out at me:

“But here’s the thing. No one in 2016 is really addressing the future as we are likely to experience it, and while that future has significant structural headwinds influenced by too much debt and an aging demographic, another heavy gust merits little attention on the political stump. I speak in this Outlook to information technology and the robotization of our future global economy. Virtually every industry in existence is likely to become less labor-intensive in future years as new technology is assimilated into existing business models. Transportation is a visible example as computer driven vehicles soon will displace many truckers and bus/taxi drivers. Millions of jobs will be lost over the next 10-15 years. But medicine, manufacturing and even service intensive jobs are at risk. Investment managers too! Not only blue collar but now white collar professionals are being threatened by technological change.” (Emphasis mine.)

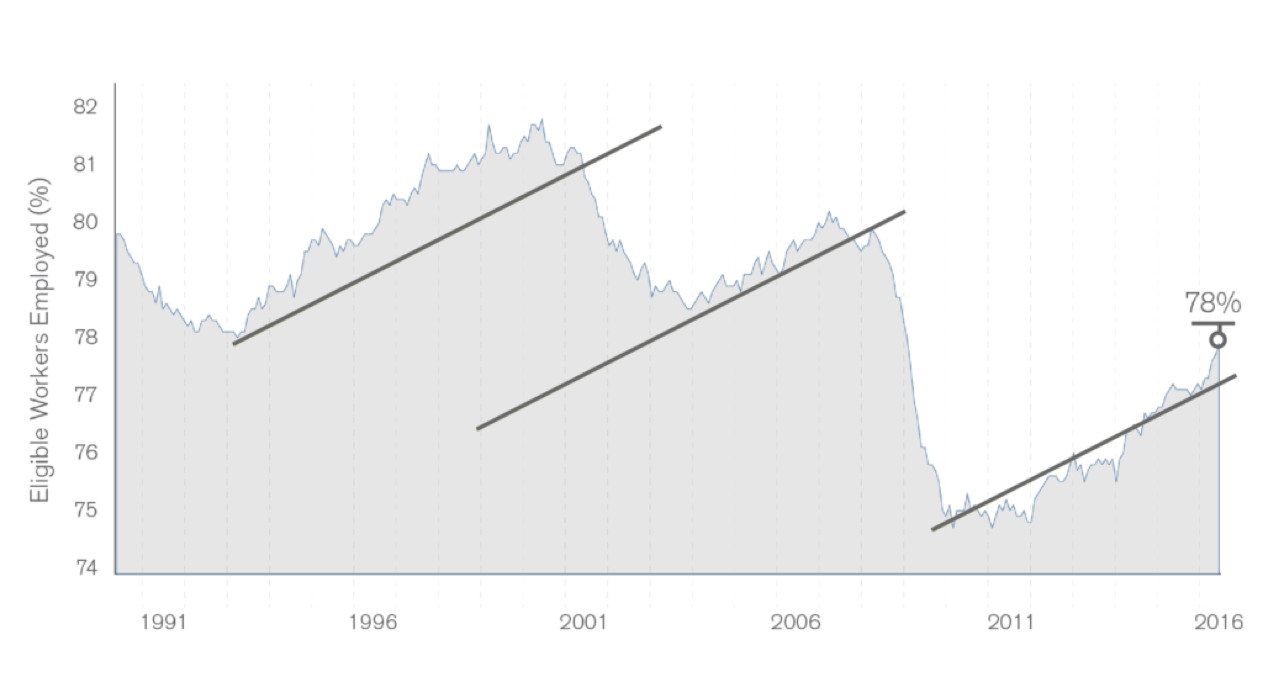

Nobel Prize winning economist Michael Spence wrote in 2014 that “should the digital revolution continue…The structure of the modern economy and the role of work itself may need to be rethought.” The role of work? Sounds like code for fewer jobs to me. And if so, as author Andy Stern writes in Raising the Floor, a policymaker – a future President or Prime Minister – must recognize that existing government policies have “built a whole social infrastructure based on the concept of a job, and that concept does not work anymore.” In other words, if income goes to technological robots whatever the form, instead of human beings, our culture will change and policies must adapt to those changes. As visual proof of this structural change, look at Chart I showing U.S. employment/population ratios over the past several decades. See a trend there? 78% of the eligible workforce between 25 and 54 years old is now working as opposed to 82% at the peak in 2000. That seems small but it’s really huge. We’re talking 6 million fewer jobs. Do you think it’s because Millennials just like to live with their parents and play video games all day? I think not. Technology and robotization are changing the world for the better but those trends are not creating many quality jobs. Our new age economy – especially that of developed nations with aging demographics – is gradually putting more and more people out of work.

Chart I: Advance of the Robots, Retreat of Labor

Source: U.S. Bureau of Labor Statistics

Source: U.S. Bureau of Labor Statistics

What should the policy response be?

Bill Gross goes on to talk about a “UBI” or “Universal Basis Income.” He notes, “If more and more workers are going to be displaced by robots, then they will need money to live on, will they not? And if that strikes you as a form of socialism, I would suggest we get used to it.”

Yikes! What kind of wind sprints are we going to need to do? Add another one to the worry list. But hey, let’s say we drop our working hours by 25% and let the bots do the heavy lifting. Take that robot! Kidding, of course. What I do know is we are endlessly creative and we’ll find our way. Let’s celebrate life, I think my mom would say.

Bill suggests some UBI solutions as well. I need to spend some quiet time thinking about this. A bit more from Bill:

- “Oh, this sounds too good to be true. Just print the money! Well, to be honest, a politician – and a central banker – should admit that increasing joblessness must be paid for somehow.

- Raising taxes (not lowering them, Donald) is one way.

- Issuing more and more debt via the private market is another (not a good idea either in this highly levered economy).

- A third way is to sell debt to central banks and have them finance it perpetually at low interest rates that are then remitted back to their treasuries.

Money for free! Well, not exactly. The piper that has to be paid will likely be paid for in the form of higher inflation, but that, of course, is what the central banks claim they want. What they don’t want is to be messed with and to become a government agency by proxy, but that may just be the price they will pay for a civilized society that is quickly becoming less civilized due to robotization. There is a rude end to flying helicopters, but the alternative is an immediate visit to austerity rehab and an extended recession. I suspect politicians and central bankers will choose to fly, instead of die.”

He concludes, “Private banks can fail but a central bank that can print money acceptable to global commerce cannot. I have long argued that this is a Ponzi scheme and it is, yet we are approaching a point of no return with negative interest rates and QE purchases of corporate bonds and stock. Still, I believe that for now central banks will print more helicopter money via QE (perhaps even the U.S. in a year or so) and reluctantly accept their increasingly dependent role in fiscal policy. That would allow governments to focus on infrastructure, health care, and introduce Universal Basic Income for displaced workers amongst other increasing needs. It will also lead to a less independent central bank, and a more permanent mingling of fiscal and monetary policy that stealthily has been in effect for over 6 years now. Chair Yellen and others will be disheartened by this change in culture. Too bad. If there is an answer, the answer is that it’s just that way.

Investment implications: Prepare for renewed QE from the Fed. Interest rates will stay low for longer, asset prices will continue to be artificially high. At some point, monetary policy will create inflation and markets will be at risk. Not yet, but be careful in the interim. Be content with low single digit returns.”

Bill Gross is lead fixed income portfolio manager at Janus Capital Group. You can find his full piece here.

“The big problem is how do we create jobs?” “We need to give people the dignity of the job and the right pay to take care of their families.” – Michael Bloomberg (2016 SALT Conference)

Amen brother Mike!

Bloomberg said that if you really want to worry about America, roughly 40% of all jobs can be automated over the next 10 years. Robots – add that one to the list.

I can’t see UBI or maybe it can exist in some helpful form. I believe such programs repress vs. uplift. Yes, we have a responsibility to help those that can’t help themselves but there should be a limit. But what does that look like? I don’t know. However, we can create many jobs! Come on people (leaders) – we can do this!!!

A Couple of Charts I Found of Interest

Fund Flows January 2016 to May 2016

In the next two charts, note the comparisons between the first five months of 2015 and 2016. You’ll see continued net outflows from equity MFs and ETFs (selling equities). Also, note the reduction in “net announced corporate actions.” M&A and corporations buying back their stock had been a big source of market buying demand. It is slowing.

Source: CNBC

Source: CNBC

January 2015 to May 2015

Company stock buybacks are down. Cash takeover announcements down even more. M&A is down. A year ago it was a strong start to the year with buybacks and M&A. Not so this year. Source: TrimTabs and CNBC.

Hey, if we follow Japan, TrimTabs is going to need to add a new line to the chart: “Fed ETF Purchases.”

Wages Are Down.

Source: TrimTabs Investment Research CEO Charles Biderman on equity outflows, the job market and the slowdown in corporate buying. His advice:

Source: TrimTabs Investment Research CEO Charles Biderman on equity outflows, the job market and the slowdown in corporate buying. His advice:

- “Wage and salary growth has slowed – and is evidenced by the economy.”

- “Stay patient until the Fed recognizes the dire state and launches its next batch of helicopter money.”

Maybe Biderman needs to add Central Bank’s buying ETFs to his charts. BoJ owning 59% of all of the ETFs available in Japan? Just saying.

Federal Government Deficit Increasing Again

Another interesting chart to me shows that the Federal Government deficit is growing again. Note the gray shaded area (middle section, far right of chart). Also note the economic gain or pain per annum when the deficit is “worsening.”

The data tells us to continue to expect slower economic growth and slower wage growth (see non-farm payrolls – right-hand box, upper section of chart).

Trade Signals – Fed Minutes: Odds of a Rate Hike…Up

Here is a link to the Trade Signals blog page.

SPECIAL NOTE ABOUT GMAIL: [As a quick aside, if you are subscribed to this newsletter via your Gmail email address, Gmail filters emails into three mailboxes: a main inbox, a social inbox and a promotions inbox. If you are like me, I totally ignore the social and promotions inboxes. Google is virtually flawless at filtering incoming mail so that users see only what they want to see, without asking us! It’s pretty amazing, actually. We believe On My Radar may get relegated to the promotions box. To make all future OMRs go to the main inbox, find an old OMR message in the promotions box and drag-and-drop it into the main inbox. At that moment, a little message will appear above the inbox tab asking, “Do this for future messages from [email protected]?” Then click “Yes.”]

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Have a wonderful weekend!

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History:

Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Following are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Tactical All Asset Strategy FundTM, CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group

© CMG Capital Management Group