How to Determine the Value of a Cyclical Stock like Emerson Electric: Part 1

Identifying the intrinsic value of a cyclical stock is more difficult than valuing a company with a steady history of growing earnings. However, there are many Dividend Aristocrats and Dividend Champions that are, in fact, cyclical companies. In spite of this cyclicality, they have been able to steadily increase their dividends for over 25 consecutive years in order to make these prestigious dividend growth stock lists. Therefore, since growth of dividend income is important to the dividend growth investor (especially for those in retirement) it only makes sense to include certain cyclical stocks with long histories of growing their dividends in our research activities.

However, it is also important for investors to have a clear perspective of what a cyclical stock is and what it is capable of offering in terms of both capital appreciation and dividend income. As a general statement (and there are exceptions to the rule) cyclical stocks are not fast growers over the long run. Consequently, they are not always the best choice for generating maximum long-term capital appreciation.

Nevertheless, if purchased at sound or attractive valuations, they are often capable of generating strong intermediate-term returns. These strong intermediate returns generally occur when a cyclical stock is purchased at or near the bottom of its cycle. As cyclical stocks move through one cycle to the next, operating results (earnings and cash flows) often achieve periods of explosive growth followed by periods of declining growth. This cyclicality, and the associated extended periods of price volatility, present challenges to the long-term investor. It’s often very hard for many long-term investors to find the fortitude to ride out the cycles.

On the other hand, for the investor looking for a steadily increasing level of dividend income, investing in cyclical stocks at attractive valuations can be quite rewarding. I base this position on two additional general characteristics that many best-of-breed cyclical stocks possess. First of all, is an above-average dividend yield. In order to attract investors, cyclical companies are often more generous with their dividend payouts. I believe they do this to compensate for their lack of consistent or fast growth.

Second, many of the best-of-breed cyclical stocks have conservative financial structures. Competent management teams of best-of-breed cyclical companies understand the need to be conservative with their finances. The most experienced management teams of cyclical companies are keenly aware that a future down cycle is inevitable. Consequently, the best managed cyclical companies tend to be conservative with the management of their cash flows.

Rational Methods for Determining the Intrinsic Value of Cyclical Stocks

When all of the above is considered, I contend that it is imperative to be careful about the valuation you pay when investing in cyclical stocks, even when it is a Dividend Aristocrat. However, as previously stated, determining the intrinsic value of a cyclical stock is difficult. Nevertheless, we need to look for some of the best or most rational methods for determining the intrinsic value of a cyclical stock, because getting valuation right on a cyclical is even more important than it is on a steady grower.

However, we should simultaneously remember that valuing any business is part art and part science, and there is no absolute or perfect way to value any business. Moreover, we should also recognize and understand that there are many faces to valuation. Therefore, we should also be prepared to examine and consider valuation based on numerous perspectives and metrics.

Additionally, certain valuation methods only apply to certain companies. Furthermore, we should also accept the fact that it would be rare to find a company with a perfect score. The best that we can rationally expect is to identify a company where there is a preponderance of evidence supporting attractive valuation.

With the remainder of this article, I’m going to share my approach to researching and assessing the fair valuation of the blue-chip Dividend Aristocrat cyclical stock Emerson Electric Company.

Emerson Electric Co. (EMR)

Emerson Electric is a Dividend Aristocrat and Champion that has increased its dividend for 59 consecutive years. However, it is also a cyclical stock. As a result, I will apply a slightly different approach to assessing its relative valuation than I would with a more consistently growing company. With the more consistent grower, I would normally evaluate recent historical growth and consider looking at consensus analyst estimates for the next one or two years’ worth of earnings.

However, with companies with more cyclical histories of earnings and cash flow growth, I like to utilize the method that Ben Graham recommended many years ago. In his heyday, Ben Graham was primarily evaluating industrial companies that tended to have cyclical histories. Therefore, he recommended assessing fair valuation based upon the average earnings of a cyclical business over the past 10 years.

Ben’s general idea was that a 10-year timeframe would cover an entire business cycle, and therefore, the 10-year average evened out the highs and lows. I’d like to go a little farther and apply the same calculations to include the 10-year average of both operating cash flows and free cash flows.

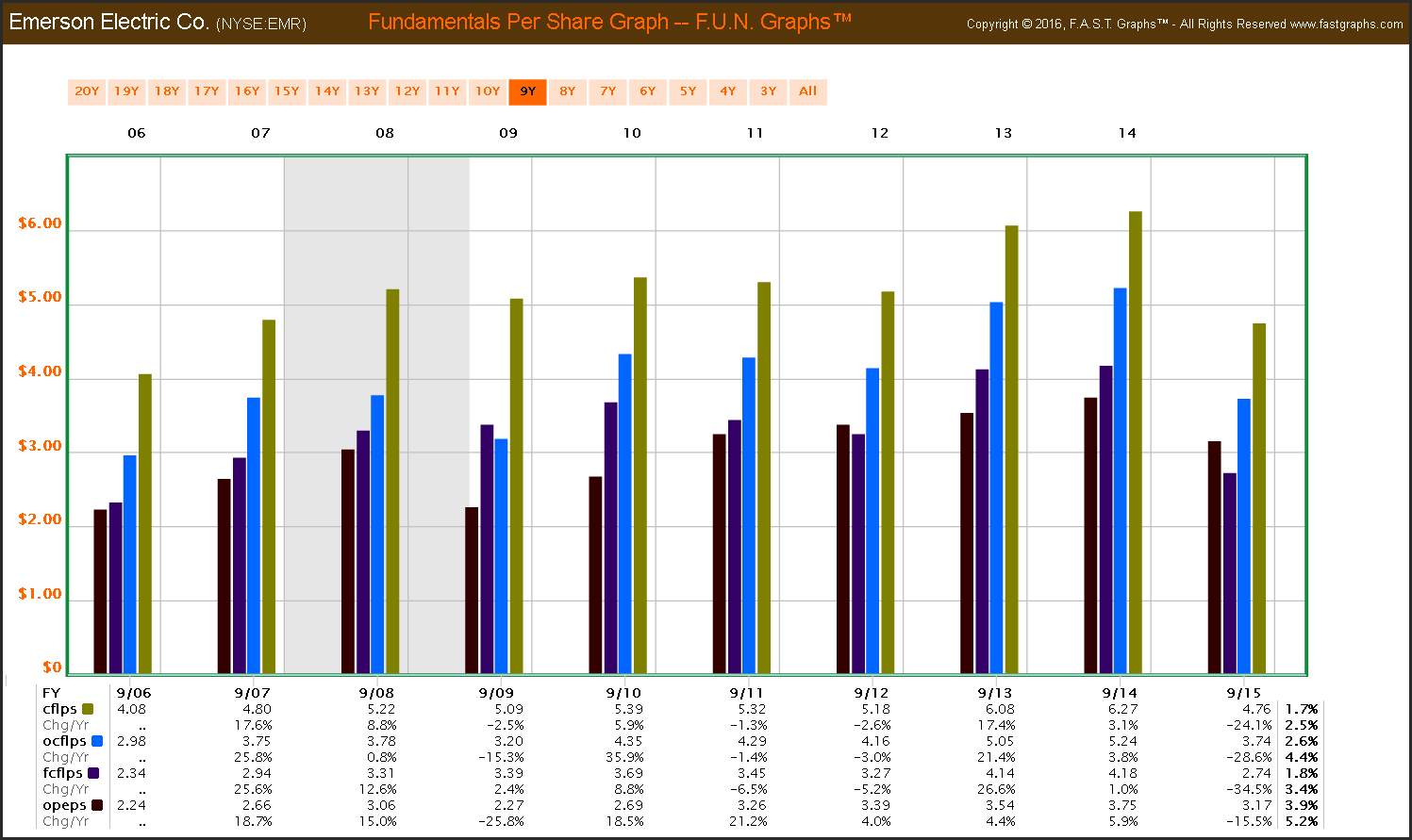

The following FUN Graph reports cash flow per share (cflps), operating cash flow per share (ocflps), free cash flow per share (fcflps) and operating earnings per share (opeps) for Emerson Electric over the past 10 years. When calculating the 10-year average on each I get the following:

10-year average cash flow per share $5.21

10-year average operating cash flow per share $4.05

10-year average free cash flow per share $3.34

10-year average operating earnings per share $3.00

With these 10-year average calculations in hand, I can run what I consider conservative fair valuation levels for each of these metrics measured against Emerson Electric’s current market price of approximately $50.75.

For cash flow, I apply a historical normal cash flow value multiple of 9.5 which gives me a fair value price of $49.00. This is approximately $2 below Emerson Electric’s current price. This valuation method suggests that Emerson Electric is mildly overvalued based on cash flows, which is important from a dividend perspective.

For operating cash flow, I apply a normal price to operating cash flow multiple of 12.4, which gives me a fair value price of $50.22. This valuation method indicates that Emerson Electric is fully valued based on the market’s historical operating cash flow multiple.

For operating earnings I apply Emerson Electric’s normal P/E ratio for this timeframe of 16.9, which gives the fair value price of $50.70. This valuation method indicates that Emerson Electric is fairly valued based on the market’s historical operating earnings multiple.

For free cash flow I apply Emerson Electric’s 10-year historical normal price to free cash flow multiple of 15, which gives me the fair value price of $50.10. This valuation method indicates that Emerson Electric is fairly valued based on a reasonable price to free cash flow.

At this point, Emerson Electric calculates to be at or near fair value within a reasonable range based on applying practical valuation multiples to each of these four important operating metrics. As previously stated, the score is not perfect, but there is a preponderance of evidence supporting Emerson to be at a reasonable current valuation.

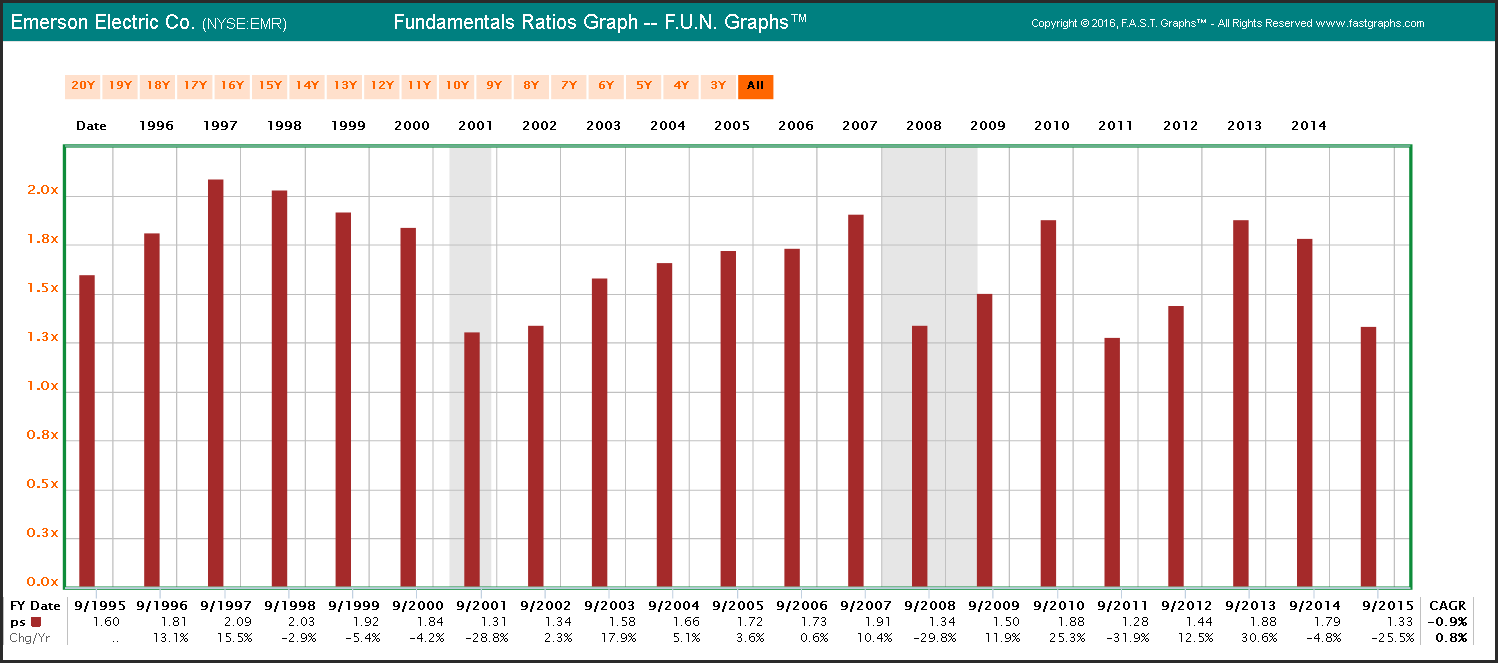

However, these are but four of the many faces of valuation referenced above. So far so good, but it’s now time to evaluate many of the other faces of valuation on Emerson. This next graph reveals the longer-term historical price to sales ratio for Emerson Electric. A quick review of this graph indicates that Emerson is currently trading at the lower end of its historical price to sales ratio. A low price to sales ratio is a solid indicator of fair value.

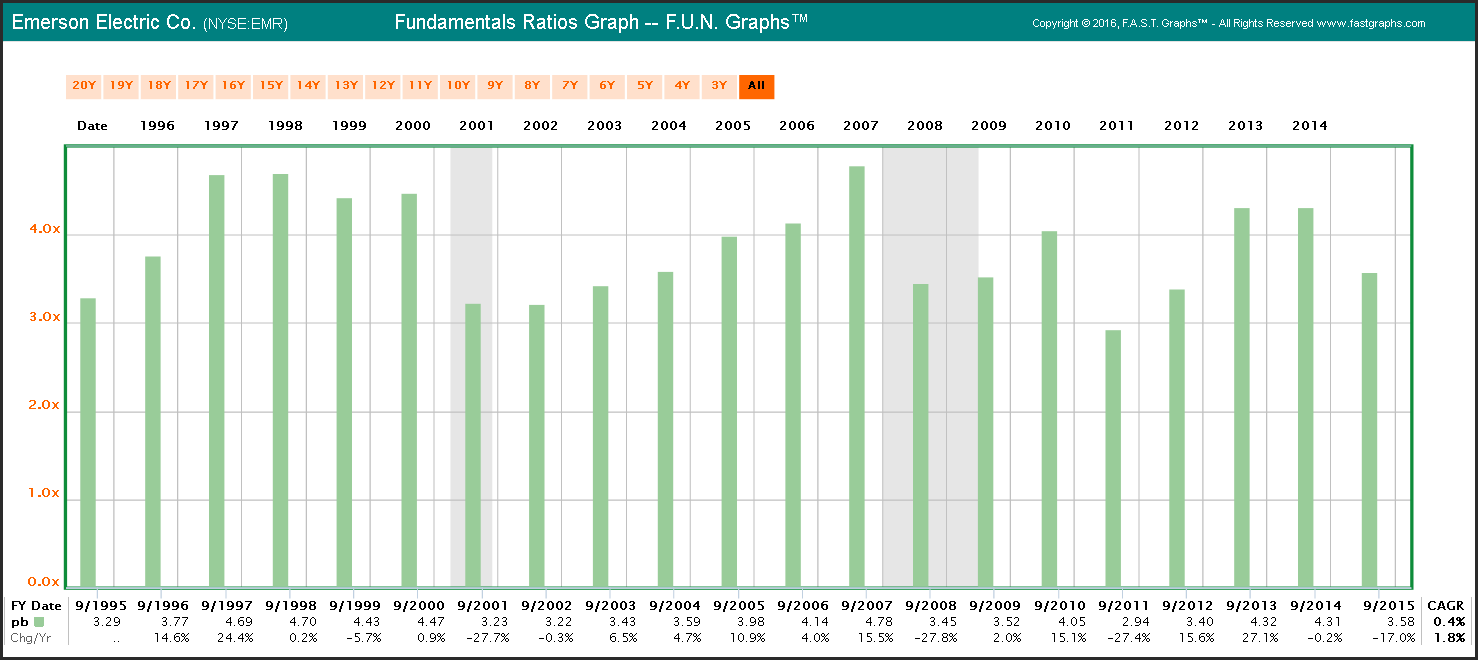

Since Emerson Electric is heavily involved in the manufacture of many of its products, book value is more relevant than it would be with service companies. Emerson Electric’s book value at fiscal year-end September, 2015 sits at the lower end of its historical norms. This provides an additional indication that Emerson Electric is currently available at a reasonable valuation.

Since Emerson Electric is a Dividend Aristocrat and Dividend Champion, a quick review of its historical year-end dividend yields provides an additional face of fair value. In this case, a higher dividend yield represents a better valuation because dividend yield is highest when valuation based on price is lowest. Emerson Electric currently offers close to one of its highest historical dividend yields.

Summary and Conclusions

Before I would even consider conducting a comprehensive research, due diligence and analysis effort on any company, I have to consider it attractively valued. Fair valuation is critical to long-term investment success and to controlling risk. Consequently, I see no benefit in spending a lot of time or effort researching a company that is overvalued. No matter how much I like the company, no matter how high quality it might be, I simply will not invest in a company and pay more than I believe it is worth. Therefore, assessing fair value is always my first step.

However, once I have determined that fair value is evident, as I have with Emerson Electric, then and only then does the real work begin. All I have accomplished thus far is the determination that cyclical Emerson Electric is worthy of a more comprehensive research effort. Once the valuation test has been passed, I will then move on to assessing quality and potential opportunity.

Additionally, I try to understand the business behind the stock and assess whether or not I’m interested in becoming a shareholder/owner for the long run. Although cyclical stocks like Emerson Electric are more challenging, they can be excellent sources of long-term dividend income and growth thereof. In part 2, I will turn my attention to a more comprehensive look at Emerson Electric for potential current investment.

Disclosure: Long EMR

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.