Who are you going to believe, me or your lying eyes?

– Groucho Marx

Economic data reports are subject to measurement error, statistical noise, and seasonal adjustment difficulties. They should always be taken with a grain of salt. However, that’s not to say that the figures are useless. Rather, they are subject to interpretation. What then do we make of the situation when the hard data conflicts with the anecdotal information?

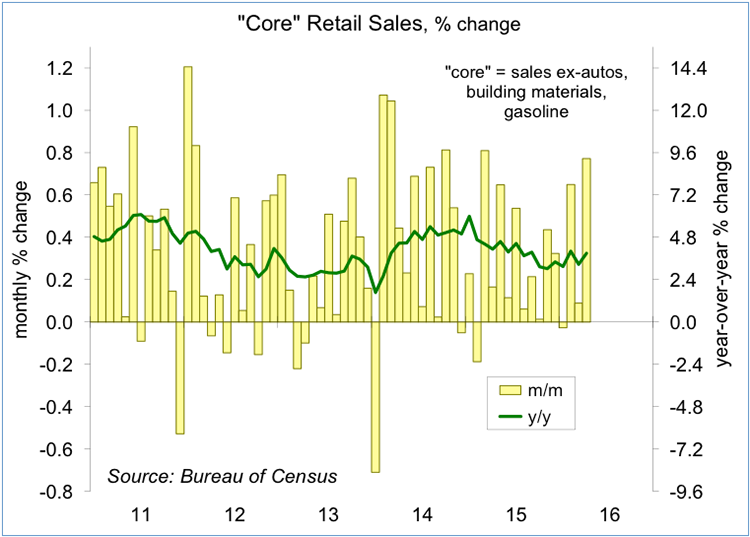

Last week, a number of retailers reported disappointing results for April. Yet, the Bureau of Census reported strong sales, with upward revisions to the figures for February and March. What gives? The BoC figures are subject to revision, but that’s not it. Rather, the government’s retail sales data are more comprehensive; they cover a wider range of spending than a few specific retailers. Sales do bounce around from month to month. Adjusted data have to account for seasonal variation, the number of weekends in the month, and floating holidays.

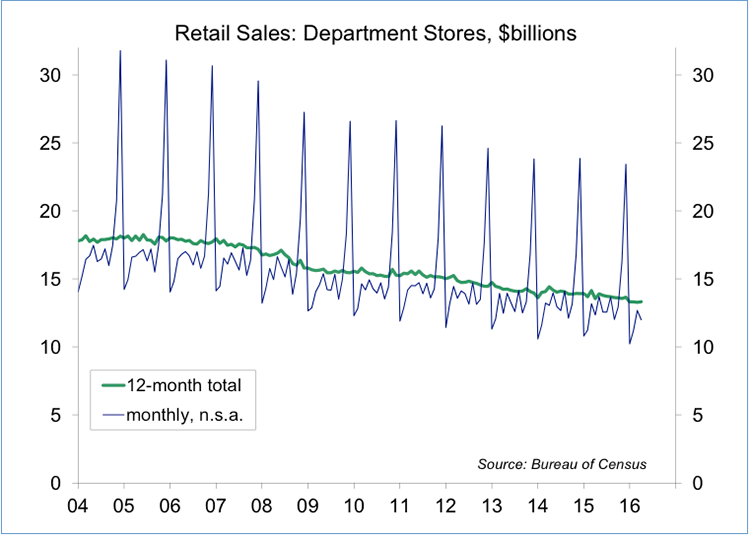

First quarter figures were generally soft. Usually, that’s due to bad weather, but weather wasn’t much of a factor in 1Q16. In fact, temperatures were generally warmer than average, which is usually supportive for consumer spending growth. In the absence of adverse weather, it’s easier to get to the malls, or so the thinking goes. Yet, consumers have become less enamored with bricks and mortar shopping. Department store sales fell 1.7% y/y in April, continuing a downward trend.

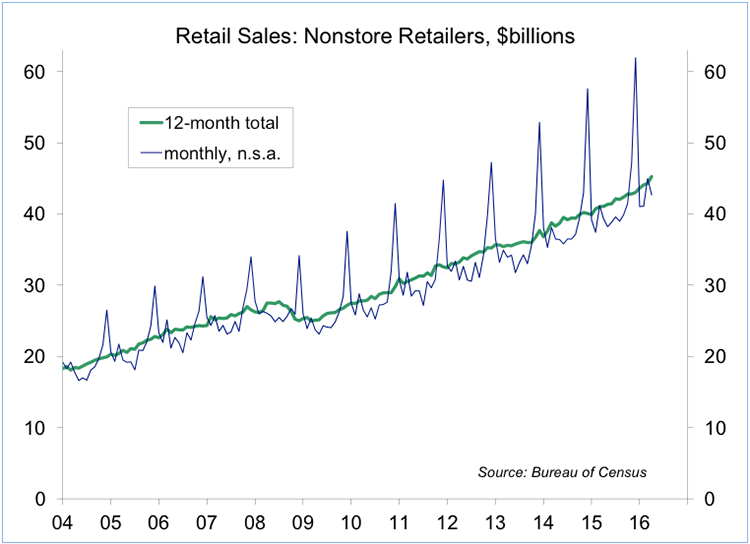

Nonstore sales, which include mail order and internet retailers (such as Amazon), rose 10.2% y/y in April, continuing a strong upward trend. There’s a lot to be said for convenience. We’re also seeing strong sales gains at restaurants and bars, supported by the drop in gasoline prices, but also reflecting the long-standing trend of households taking more meals outside the home (again, there’s a lot to be said for convenience). Consumers are also paying more for their medical prescriptions. Sales at pharmaceutical and drug stores are reported with a lag, but they were up 7.9% for the 12 months ending in March.

Many of the economic reports for March appear to have been distorted by the early Easter. Figures are adjusted for the timing of Easter, but it’s difficult to get it right (as there are interactions between the holiday and weather). Softer March figures should then be followed by a rebound in April. That was the case with unit auto sales and the retail sales numbers, and we should see a similar pattern in other economic data reports. Given this noise, how do we gauge the underlying strength of the consumer? We can take the average of March and April, but figures for May will help to confirm whether the economy is strengthening or simply trending at a moderate pace.

Beyond the numbers, it’s clear that there is economic angst out there (reflecting dissatisfaction with the Washington establishment). While the economy is improving in aggregate, it’s not necessarily advancing for the average citizen.