Retired Investors Should Give This Blue-Chip Technology Stalwart a Close Look

I believe that building and managing a successful stock portfolio is simple and straightforward, but not necessarily easy. Building and successfully managing a portfolio of individual stocks requires work, a disciplined philosophy and a reasonable commitment of time. But perhaps most importantly, it’s critical to start out with a precise understanding and acceptance of how you approach the investing process.

You can either behave as a prudent long-term investor or as an active trader. The differences between these two approaches are not subtle - they are vast. Unfortunately, at least in my personal experience, there are many well-intentioned people that feel they would be most comfortable with the prudent long-term investor approach, but cannot resist the seduction of stock price volatility. No matter how hard these investors try, they cannot ignore the daily ups-and-downs of stock price movements.

As one Morningstar writer I once read so aptly put it: “Given the proclivity of Mr. Market to plead temporary insanity at the drop of a hat, we strongly believe that it’s not worth devoting any time to predicting its actions.” Stated more directly, in the short run, stock price movements are often irrational and consequently unpredictable. Later I will provide a clear example supporting the veracity of that statement. Nevertheless, there are many active traders that believe they have an edge; however, I’ve yet to have anyone convince me that they in truth and fact do.

This brings me to the primary difference between the mindsets and perspectives of active traders versus long-term investors. Active traders tend to primarily be stock price focused. In their world, everything is about whether the price of the stock is rising or falling. A stock with a falling stock price is a bad stock, where a stock with a rising stock price is a good stock. Active traders possess more of a casino-like mentality and as such have little or no regard or concern about fundamentals or business values.

Ironically, the active trading approach requires more time, energy and effort than does a more prudent long-term approach. In other words, active trading essentially turns investing into a full-time job. Consequently, I contend that this approach is not appropriate for most people. Most of us have more important things to do with our lives and time than sitting in front of a computer screen obsessively tracking stock prices.

In contrast, long-term investing implies focusing more on the business you are invested in with little or even no concern about short-term price volatility. Instead of focusing on price movements, the focus is on the company’s financial performance and fundamental strengths. Prudent long-term investors understand that in the long run it’s the success of the business that truly matters most. These investors recognize and understand that buying a stock represents becoming a part owner in a business.

Personally, when I invest in a stock as a passive shareholder/owner, I am not interested in running the business. I leave that work to the management team. The only work I’m interested in is having my money working for me. As a minority shareholder, I am keenly interested in how the company is doing and only mildly interested in its short-term stock price movements. This is especially relevant when I have a clear understanding of what the business is worth. Therefore, if or when short-term market price drops below that level, I never assume I’m losing money. Especially if the business I own is continuing to perform as expected. Instead, I simply consider the business temporarily illiquid.

Therefore, if I did need to raise money, for example, in an emergency, I would look to other stocks I might own that the market was either valuing correctly or overvaluing. My point is that I don’t consider it intelligent to sell an asset for less than I believe it is worth. This type of business owner’s mindset goes a long way towards keeping emotion out of the investing equation. I draw my confidence from the strength and health of the business I own which keeps me from panicking during periods of high market volatility.

I have chosen the business below because I believe it is attractively valued and because it offers a high-yield in today’s low interest rate environment. However, this particular business also offers important insights and represents a quintessential example of the principles I have been discussing in this introduction. In other words, not only do I consider it an excellent investment at this time, I also feel it offers vitally important investing lessons. I intend to elaborate on both as I review Cisco Systems, Inc. (CSCO) below.

Quintessential Lessons in Long-Term Investing

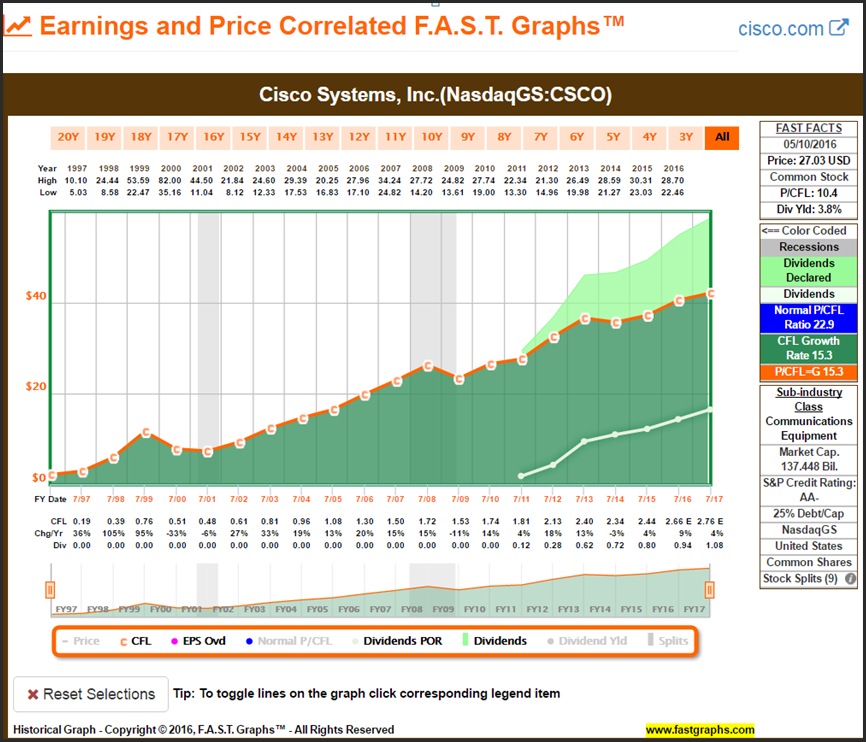

It is a commonly-held view that technology companies are cyclical stocks. To a great extent, this is true. However, just because a business operates in the Technology Sector does not simultaneously suggest that it is a highly cyclical business. Cisco is a case in point. A quick review of the following earnings and dividends only F.A.S.T. Graphs™ on Cisco suggests that this technology bellwether looks more like a growth stock than a cyclical stock. Business did falter a little bit during our last two recessions, but neither case suggests deep cyclicality.

On the other hand, since fiscal 1997 earnings growth has averaged over 13% per annum and the company initiated a dividend at the beginning of fiscal year 2011. The honeydew green line (white) plots the company’s dividends per share, and the area below the line represents the portion of earnings they paid out, commonly known as the dividend payout ratio. The light green shaded area shows the same dividends after they have been paid out. This graph illustrates our first look at Cisco the business.

When looked at from this business perspective, I see very consistent and strong long-term business performance. Additionally, a review of the FAST FACTS boxes to the right provides additional initial insights into the quality of this business. I like the low debt to capital ratio of 25%, I like the AA- S&P credit rating and I like the dividend yield of 3.9%. I also like the growth of the company’s dividend since they started paying one in 2011. From what I see here, Cisco represents exactly the kind of business that I would like to be the owner of. Importantly, there are no stock prices to contaminate my thinking or engender emotional responses.

When I am initially examining a business for prospective investment, I start out by reviewing its long-term earnings performance as I did with Cisco above. Next, I like to also look at its historical cash flow generating performance. Examining cash flows is even more relevant when I am evaluating a dividend paying stock. Clearly Cisco is more than adequately covering its current dividends with strong cash flows.

Investing in the Business

At this point, I consider Cisco a further research-worthy candidate because I like what I see regarding my first look at the business behind Cisco’s stock.

(Note: before I would actually consider a stock “research worthy” it would also have to be available to me at an attractive valuation. Cisco currently meets my valuation criteria. However, this can only be determined by including stock price into the equation. In the context of this article’s secondary objective of presenting time-tested lessons in investing, I have chosen to save stock price inclusion for later when I delve deeper into valuation principles.)

Nevertheless, Cisco’s consistent and impressive long-term operating record motivates me to want to look deeper under the hood. Of course, this implies diving into the company’s financial statements.

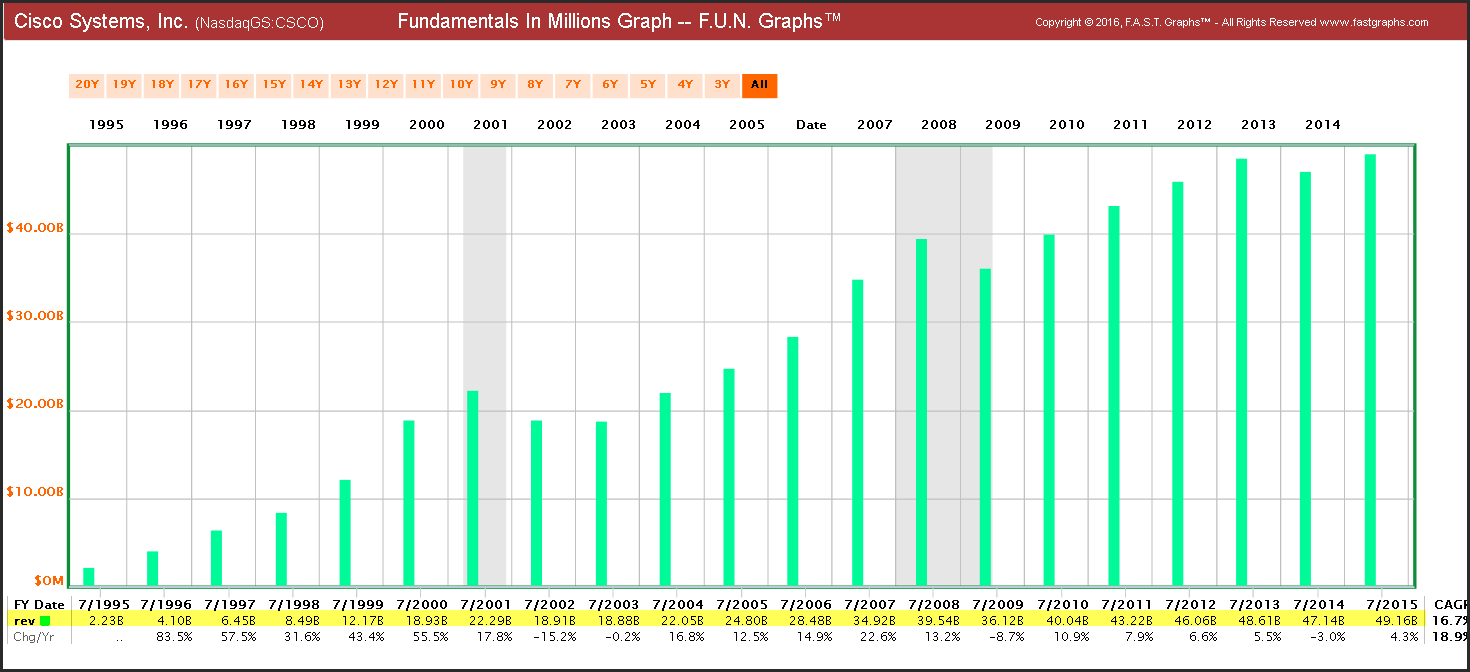

The first metric I like to examine in the financial statements are revenues. Bottom line results like earnings must start and come from the top line. Additionally, accounting conventions coupled with financial engineering could possibly paint a rosier earnings picture than is deserved, whereas top line results clearly illustrate whether a business is truly growing or not. I like to look at revenues from two perspectives. First I examine gross revenues in dollars. Cisco’s long-term revenue growth has been impressive as depicted below.

However, since I am also a passive shareholder, I also like to look at revenues per share. Revenues per share can be impacted by what some call financial engineering in the form of share buybacks. On the other hand, as I will later illustrate, share buybacks can be a positive or a negative depending on the company’s stock valuation at the time and/or whether or not the company has a good use or need of its cash to fund future growth. Cisco’s revenue per share record is just as impressive as its gross revenues.

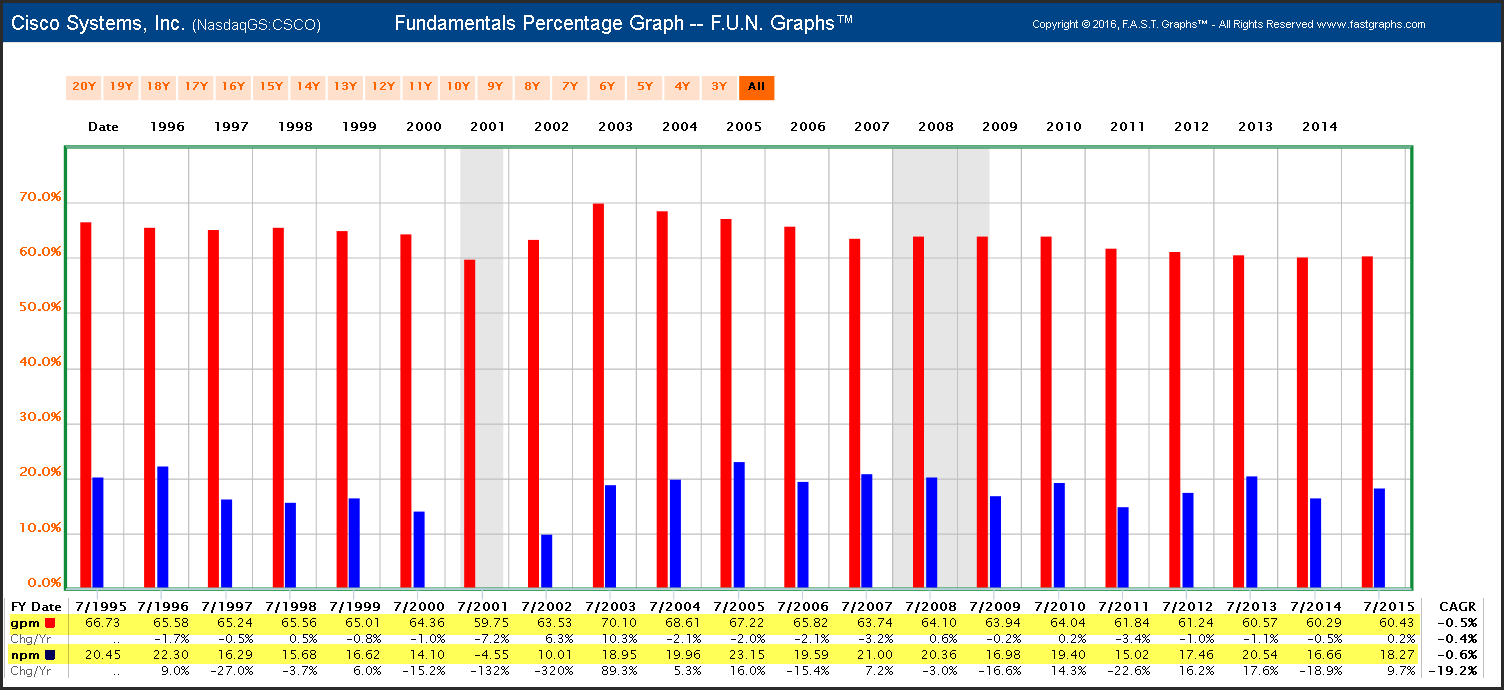

After reviewing a company’s top line, I like to turn my attention to profitability. At this point I am interested in determining how much profitability the company generates per dollar of sales. To evaluate this, I look at gross profit margins compared to net profit margins. Cisco generates very high gross profit margins which I consider a plus. My personal benchmark for net profit margin is 15% or better. Cisco has consistently produced net profit margins exceeding that benchmark. I like businesses with high net profit margins.

After I have reviewed profit margins, I typically turn to analyzing return on equity. As a shareholder, I consider this metric important because it essentially measures the return the company is earning on shareholder money. I am quite comfortable when I see a return on equity of 10% or better. Cisco earns returns on equity above this threshold. One caveat regarding return on equity is that companies can boost it by taking on more debt. Consequently, I put more weight on this metric when debt levels are reasonable - as is the case with Cisco.

Thus far I’ve illustrated some of the go-to metrics that I like to look at when evaluating the strength and health of a business I might be interested in investing in. However, I don’t stop here. Additionally, I thoroughly examine the company’s balance sheet, cash flow statement and income statement. These financial items are available from numerous sources. Personally, I utilize F.A.S.T. Graphs™ and FUN Graphs (fundamental underlying numbers) to facilitate a deeper look into the company’s financials.

I typically start out by examining all of the metrics together on the company’s balance sheet, cash flow statement and income statement. Here is a sample of Cisco Systems’ balance sheet which includes assets per share (atps), cash per share (cashps), common equity per share (ceps)-also known as book value, debt long-term per share (dltps), debt to total per share (dtps) and invested capital per share (icaptps).

Additionally, I will look at each metric on the balance sheet one at a time in order to focus more clearly on each metric. Here’s an example of Cisco’s cash. Clearly, Cisco possesses significant financial resources and flexibility.

Learning About The Business

Once I have thoroughly examined a company’s financial results, health and strength, I typically turn my attention to learning as much as I can about what the company does and how they make their money. The easiest way to do that is to simply follow the link on my F.A.S.T. Graphs™ to the company’s website. Although I recognize that much of what I will find will be company propaganda spun as positively as they can, I can also learn a lot about the company’s products and various business enterprises. Here is a snapshot from Cisco’s website illustrating key product areas with specific links to each. If I’m seriously interested in investing in the company, I will peruse each of those links.

I will usually then go to the company’s investor services sections and look for presentations that the company has recently presented. Here is an example of an informative slide from Cisco’s Q2 Fiscal Year 2016 Conference Call:

But, my favorite places to learn about the company’s businesses are by reading the compay’s 10-Ks and 10-Qs. As I previously stated, researching a stock is simple and straightforward. However, I also stated that it requires time and effort. Consequently, I will usually not go to this extent with my research process unless I am very confident that I am examining an attractive potential investment.

Cisco Systems, Inc.: Quintessential Lessons on Valuation

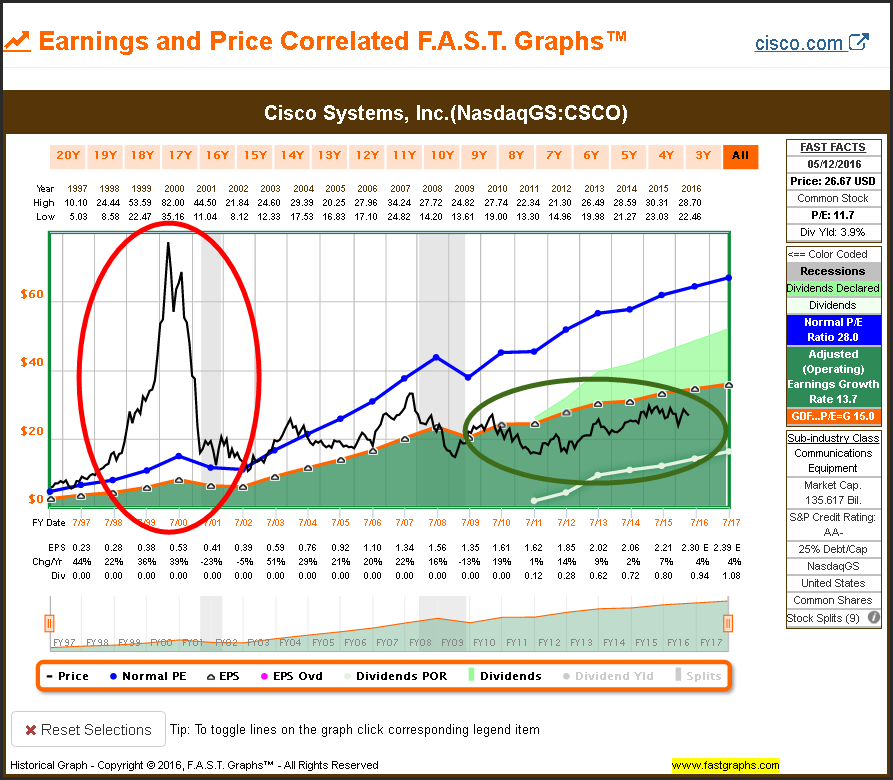

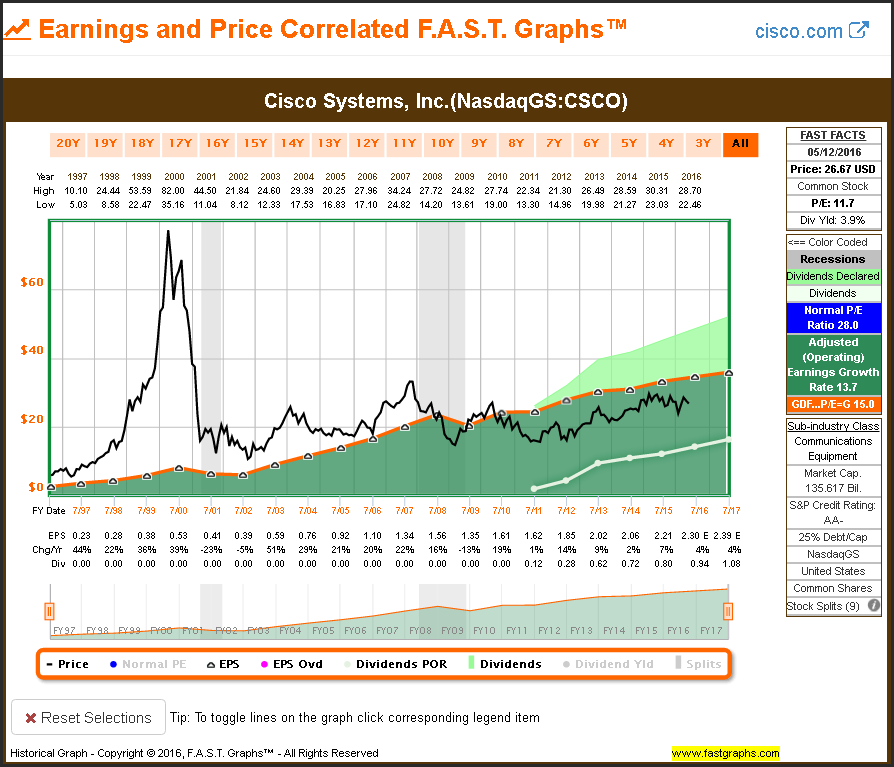

In the introduction to this article I suggested that stock price movements are often irrational and consequently unpredictable. Furthermore, I promised that I would present a clear example supporting the veracity of that statement. The stock market’s long-term valuation history on Cisco Systems provides compelling evidence supporting just how irrational the stock market can be at times.

In the late 1990s Cisco Systems, along with several other bellwether technology stocks, were being valued at ridiculous valuations (see the red circle on the graph). At its peak, Cisco was being valued at over 160 times earnings and for a time had one of the largest market caps of any company on the earth. However, this was an irrational valuation because Cisco’s fundamentals clearly did not support such a ridiculously high level. In other words, Cisco’s business was worth nowhere near what the market was valuing it at.

Remember, I also earlier stated that it’s the value of the business that truly matters in the long run. Therefore, the subsequent fall from grace of Cisco’s stock price in calendar years 2000 and 2001 presents striking evidence of that reality. But we must also recognize that just as the market can irrationally overvalue a business; it can also be just as irrational with undervaluing a business.

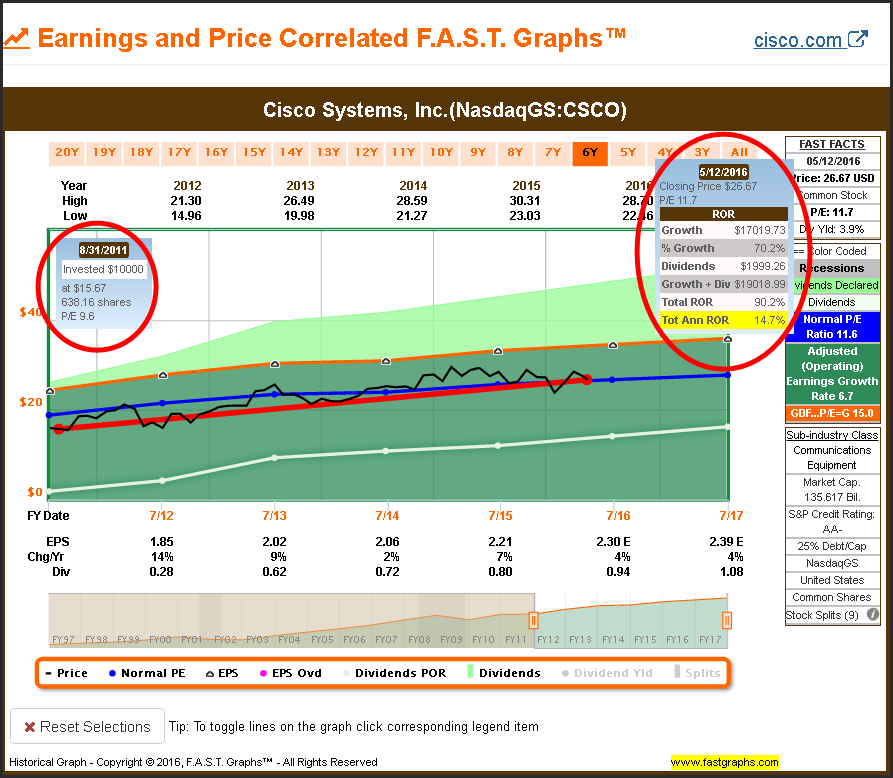

It is my contention that this is precisely what has been happening with Cisco’s stock price since the beginning of 2010 (see the green circle on the graph). Consequently, my primary investment thesis for suggesting Cisco is based on what I consider to be significant current undervaluation by the market. A blended P/E ratio below 12 and a dividend yield of approximately 3.9% with the opportunity to grow seems compelling to me considering Cisco’s quality and financial health as described above. However, prudence might dictate waiting until the company reports 3rd quarter results on May 18.

One additional comment regarding Cisco, its recent performance and valuation, is to point out that in spite of this, the company has outperformed the S&P 500 since it initiated its first dividend in fiscal 2011. The following earnings and price correlated graph with performance calculations illustrates how attractive Cisco has been over this timeframe.

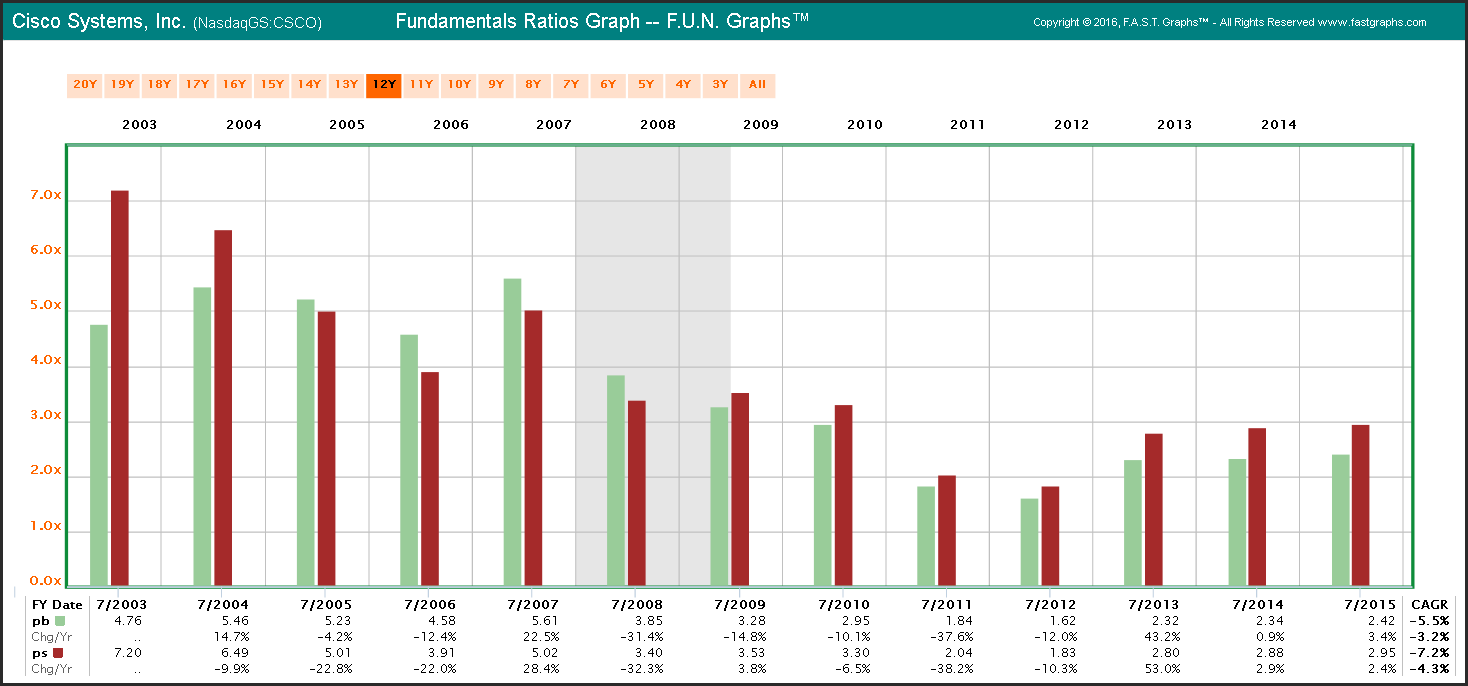

Earnings and price are not the only valuation metrics I like to examine. Cisco also looks very attractively valued based on its current price to book (pb) and price to sales (ps).

Management

One final but extremely important element involved in thoroughly researching a company is analyzing the company’s management team. In my personal opinion, the capability of Cisco’s management team has been historically much-maligned providing further evidence of irrational investor behavior. This especially relates to former CEO John Chambers. Over the years I have read many scathing criticisms of his lack of skills of running Cisco. Yet the very first graph I presented in this article clearly supports the undeniable fact that John Chambers did a great job running the business.

The company’s earnings growth under his reign has been nothing short of spectacular. On the other hand, the irrational way that the market has been pricing the stock was simply beyond management’s control. Management can grow the business, but they have no control over how the market will price the stock. John Chambers has recently stepped down as CEO but remains executive chairman.

I offer the following graphical comparison to illustrate the competency of Cisco’s management team and their stewardship since fiscal year 1997. Earlier I discussed the potential impact of financial engineering on earnings relating to share buybacks. The comparison of the following two graphs illustrate that Cisco’s management was prudently issuing shares when valuations were high (above the orange line) and excessive. In contrast, this also illustrates how management has been prudently buying back shares recently when valuation of the stock was low (on or below the orange line).

Summary and Conclusions

I am a firm believer and aligned with legendary investor Warren Buffett who said “investing is most intelligent when it is most businesslike.” Prudent long-term investors are most interested in positioning themselves as long-term shareholder owners or partners in excellent businesses. At the same time, they recognize that in the long run, business results matter most. When you are investing as an owner, you go in with the intention of owning the investment for a long period of time. Consequently, you spend most of your effort and energy focusing on business results and very little worrying about day-to-day price volatility.

I believe that most people intuitively understand and even embrace the time-tested principles of investing as business owners. However, I also recognize that the relentless siren song of stock price volatility in the short run can be very unnerving. Nevertheless, if long-term investing success is truly your goal, then I believe it’s imperative that you learn to trust business results more than short run price action.

Disclosure: Long CSCO

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.