“The Fed has borrowed from future consumption more than ever before. It is the least data dependent Fed in history. This is the longest deviation from historical norms in terms of Fed dovishness than I have ever seen in my career… This kind of myopia causes reckless behavior.”

-Stanley Drunkenmiller (source)

At the beginning of each month, I like to look at equity market valuations. The stock market moved higher in April, yet for the fourth quarter in a row, corporate earnings were down. The good news about market valuations is that they can tell us a great deal about the annualized returns we are likely to get over the coming 10 years. The bad news is they tell us little about returns over the coming two years.

Buy low — sell high, they say. Pretty simple actually, but not many can actually do it. This is where valuations can help us get centered. Below I provide examples from several periods – low valuations in February 2009 and the great gains since.

Valuations were high in 2000 and 2007 and, as you will see, the subsequent returns from those starting points were not good. There were some better entry points, like in early 2009 but, really, who do we know that bought back into stocks then? It was pure panic, margin calls and forced liquidations. I wrote a piece that prior December entitled, “It’s So Bad It’s Good.” I didn’t get many positive responses.

Yet, here we are today — valuations are now higher than they were in 2007. As you will see on the coming chart, they are higher than every other period in time with the exception of time surrounding the great tech bubble.

We are getting more than a few “you didn’t beat the market” phone calls like I’m sure you are getting as well. The reality today is much like 1999 and 2007, far too many investors with false confidence in hand are buyers – not sellers. Cited are the returns of the market over the last handful of years. Behaviorally, this feels hauntingly similar to those prior cyclical peaks. Lessons not learned.

I have been writing about the global overcapacity glut in the last several letters. Let’s pass on that, let’s pass on the debt mess, let’s pass on underfunded pensions and let’s pass on the Fed. Valuations do matter, so let’s go there.

Before we do, I want to weave in a few recent comments that crossed my desk this week – and likely yours – from Stanley Druckenmiller. Stan spoke this past week at the Ira Sohn Investment Conference. The CliffsNotes version of his presentation follow:

- He is negative on China’s economy going forward

- He believes further stimulus in the Asian country will not work as it has “aggravated the overcapacity in the economy” (SB here – to which I add globally aggravated along with the other central banks)

- “Get out of the stock market and own gold.”

And here is the big point as it relates to today’s overpriced stocks:

- Stan added, “U.S. corporations have not used debt in productive investments, but instead relied on financial engineering with over $2 trillion in acquisitions and stock buybacks in the last year.”

- “Corporate books show that operating cash flow growth in U.S. companies has gone negative year-over-year, while net debt has gone up.” (SB again – big buyers of U.S. stocks have been the corporations themselves. I believe they are near the end of that runway due to negative operating cash flow.)

- “Higher valuations, limits to further easing… the bull market is exhausting itself.”

Druckenmiller is the Babe Ruth of investing. One of the all-time greats. His performance record, I believe, may be unmatched. “Get out of stocks”… “Buy gold”… Try explaining that one to your clients.

Yet, like all of us, he is far from perfect (as he’ll tell you); however, we should pause and give consideration to what he is saying. Now, on to valuations.

Median P/E

Valuations can tell us a great deal about what the forward annualized returns over the coming 10 years are likely to be. My favorite metric is a price-to-earnings ratio measure called median P/E. I believe it to be a fair and consistent way to look at current valuations and compare on the same basis to historical valuations (email me if you want a deeper explanation). In this way, we can see what forward returns might likely be.

The rules remain simple. If the price is excessively high relative to earnings, then you are not getting a good bargain and won’t make as much money. If price is low relative to earnings, you get really good bang for your buck.

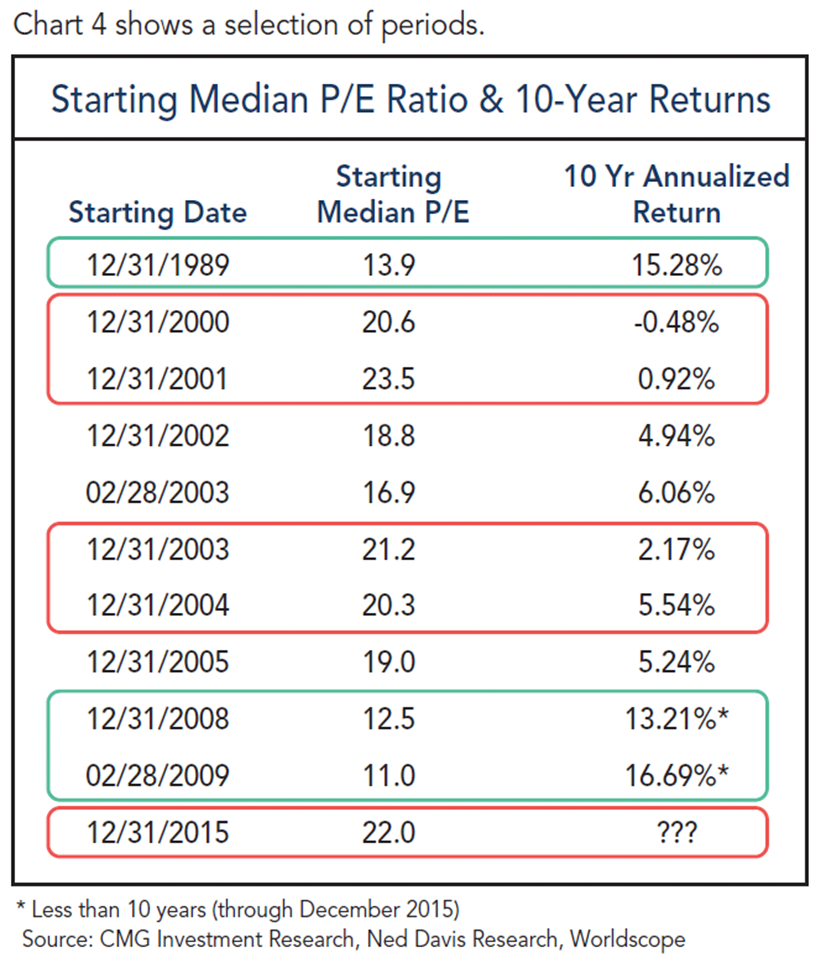

Here is a look at a few sample periods in history (you may have seen this chart from me before):

Take a look at the median P/E of 11.0 the month the market made its low in February 2009. Did most clients get 16.69% annualized return since then? Well, for those of you that had little money in the market or were in high school or college back then, here is what happened: MOST PEOPLE PANICKED AND GOT OUT at the LOW. The single biggest month of outflows on record occurred that month.

Show me the brave few who bought then. I don’t recall getting any calls asking why they did so much better than “the market” back then. I can show you the many who are buying in today. Makes no sense, but it might be best for me to jump off my soap box and get back to valuations.

Now, if you invested at the market top in the fall of 2007, the median P/E was at 19 and the S&P 500 peaked at 1549.38. The S&P 500 closed at 2065.30 at the end of April 2016. That’s about a 33% gain over eight years and seven months or an annualized total return of 5.86% per year.

Ok, so where are we today?

Median P/E reached 22.7 at the end of April. That is higher than any point looking at median P/E data from 1964 to present with the exception of the crazed pre- and post-tech bubble period.

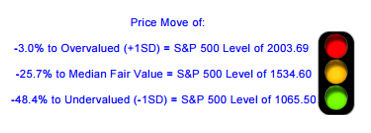

The next clip is courtesy of Ned Davis Research. The traffic light and arrows are my notations as I attempt to simplify the chart. What I like about this chart is that it does a good job estimating overvalued, fair value and undervalued levels on the S&P 500 Index. Kind of an investor reality road map.

With the S&P 500 Index at 2065.30, it (by this measure) means that the market is overvalued by 3% (red light) by historical measures. In the chart, NDR uses a 1SD (standard deviation) move above fair value (it uses the 52.2 year median P/E of 16.9 to determine fair value) to identify the market as overvalued at 2003.69.

In English, a one standard deviation move is a movement away from a historical trend – it is something that doesn’t happen very often. In the case of median P/E, a 1SD move has happened about 10% of the time since 1964. Two SD moves happened about 2% of the time since 1964 (tech bubble). The point is they mark periods of extreme.

Fair value is determined to be 1534.60 (yellow light). Most of us would be happy with adding more to equities at that level and we’d be ecstatic to get really aggressive should the S&P 500 correct to 1065.50 (the green light).

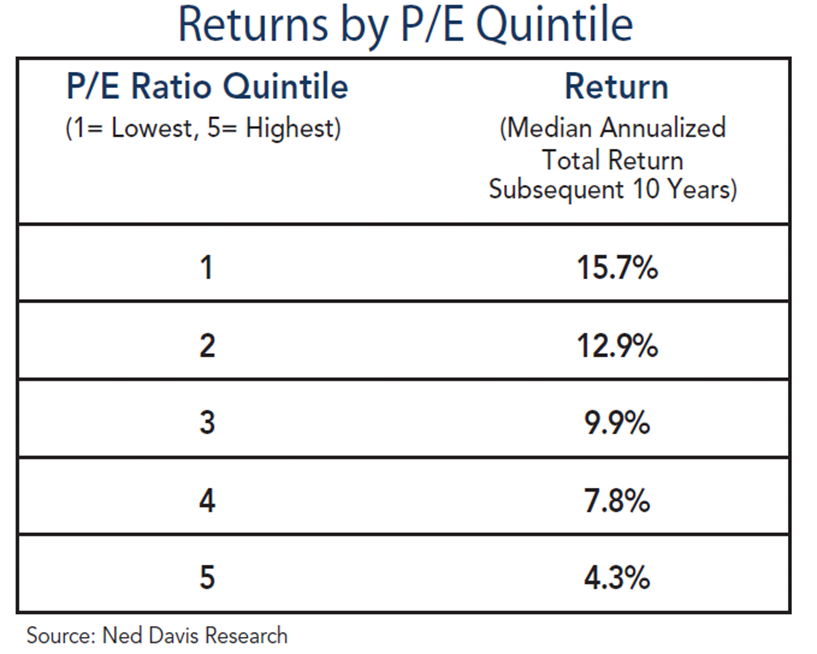

Here is what the current high valuations are telling us about probable coming 10-year annualized returns. A median P/E of 22.7 puts us in the most expensive quintile (quintile 5) of all month-end median P/E readings dating back to 1926. The highest returns occurred when the market was inexpensively priced (quintile 1) and the lowest returns occurred when the market was expensively priced (quintile 5).

This week’s piece is solely focused on valuations (very high) and forward 10-year annualized return probabilities (very low). Share it with your clients; especially when they feel it is time to put more money into stocks. Hold up the stop sign and tell them “Stan Says Sell.”

Steve says reduce equity exposure, stay long bonds for now, overweight to tactical and liquid alternatives and hedge the equity exposure you may have. I know it will be hard for you to keep your clients on board with you if the market moves 10% or 15% higher before Stan is ultimately proven right.

Stan is well known for placing large amounts of money on a small number of bets. He is a speculator extraordinaire. He is quoted as saying “there are bulls, bears and pigs.” Further adding that he considers himself “a pig” – going “all in” on just a few targeted bets. Hard for most of us humans to do.

I’m a big Stan fan. He may or may not be right on this one but the hair on our arms should stand straight up when he issues such a clear and present danger warning. High valuations are flashing the same warning.

This week begins what I hope will be a shorter and more concise letter. During the week, I tweet out links to articles, charts or research that I find important. If you are interested, you can follow me on Twitter here.

Hey, if you find On My Radar helpful, please share it with a friend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Summing up the current state of valuations:

- Median P/E, Price to GAAP Earnings, Price to Shiller Earnings, Price to Operating Earnings, Price to Forward Earnings, Price to Sales, Operating Earnings, Price to Book = Extreme Overvaluation.

- Part of the problem is that corporate earnings peaked in the second quarter of 2015. Another part is that debt financed equity buybacks have helped drive equity market prices higher.

- Lower earnings and higher prices mean we get a higher P/E ratio – or expensive hamburgers!

One last area that causes me concern is the high level of margin debt. I don’t know if it is from individuals borrowing from their stock brokerage accounts similar to how they used home equity lines of credit at the peak of the housing bubble or if they are aggressively invested in stocks but high margin debt – high any debt can be problematic.

When you combine overvalued markets with declining profit margins, high margin debt and questionable liquidity, markets have the tendency to unwind quickly. Declines trigger margins calls and, in many cases, this causes forced selling to meet those calls. Forced selling may trigger additional margin calls, which triggers more forced selling. More sellers than buyers… other buyers step out of the way and thus waterfall-like declines occur.

Conclusion: Reduce and hedge that equity exposure. Weave in other non-correlating diversifiers.

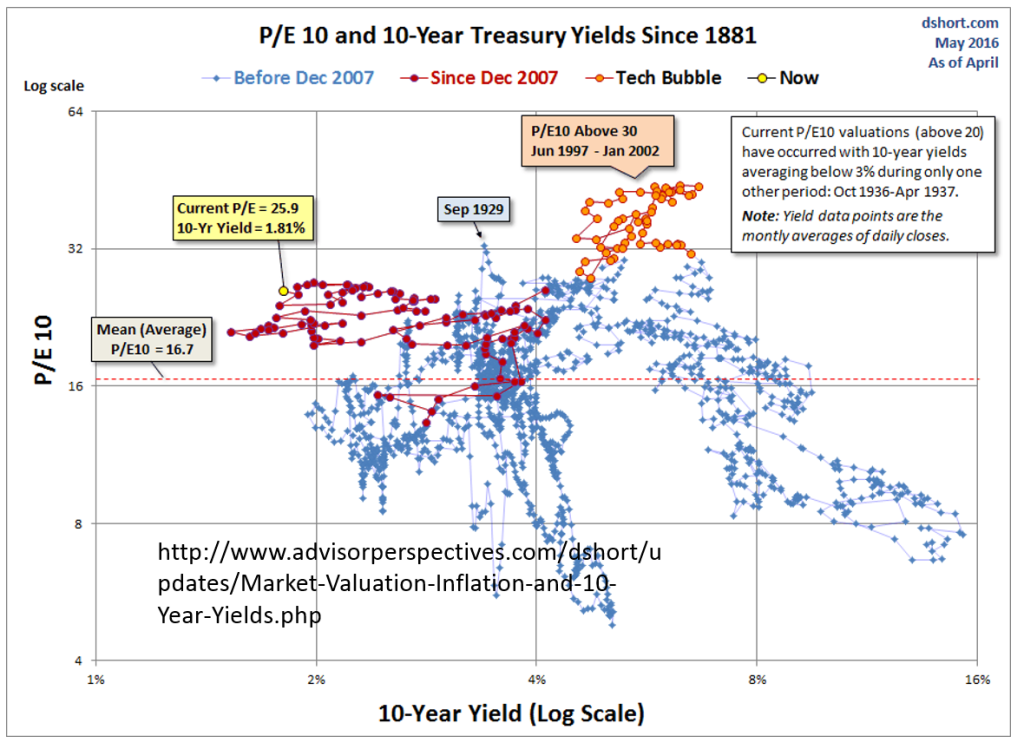

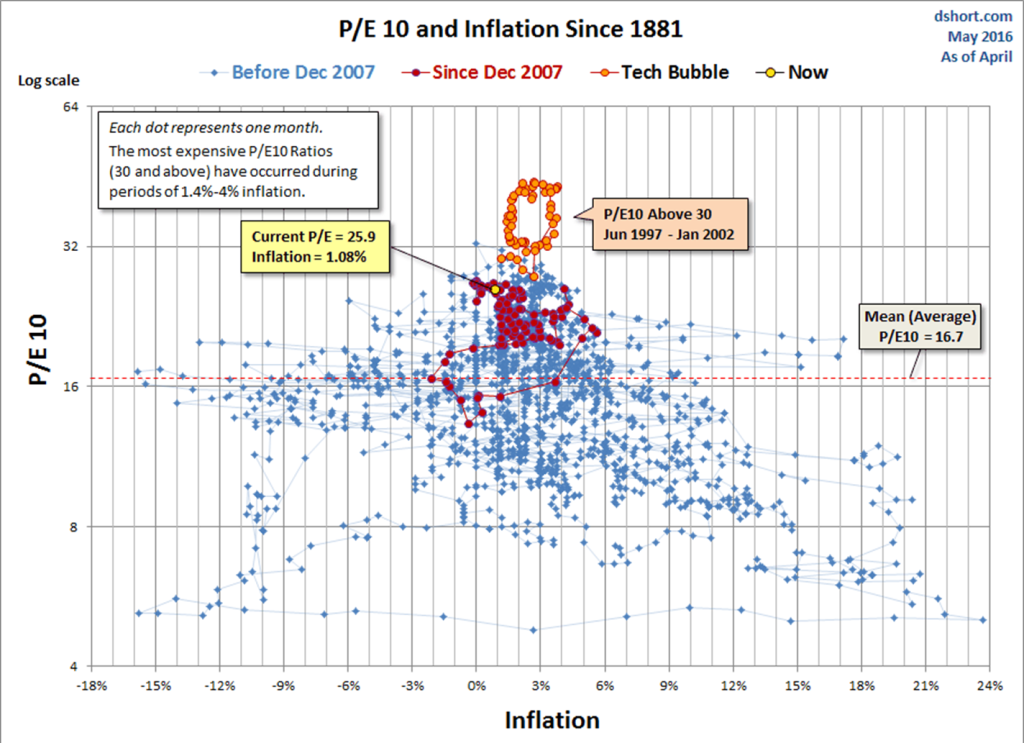

Finally, for fun (quant geek joke) take a look at these next two (way cool) charts courtesy of dShort.com.

Market Valuation, Inflation and Treasury Yields: Clues from the Past – dshort.com

I really like Doug Short’s Advisor Perspectives blog. You can find more information here.

Concluding Thought

Why should valuations be on our radar right now? It is because 75% of the investable money will be controlled by pre-retirees and retirees by 2020 (according to Blackrock).

Even if we assume that they have saved enough, and that is mostly an inaccurate assumption, this age group (which I find myself in), dare I say, may not have the runway or stomach for the seven or so years that may be required to get back to even from the minus 30%, 40% or 50% stock market hit the next recession will bring. And recession will come.

If you can’t follow Stan’s advice and decide to just hold on tight in the next market storm, then know that you will be ok over the next 10 years. That is if 0% to 2% after inflation is ok with you (and you don’t need to touch the money).

Rather, my two cents is to play it smart today and get prepared to be a great big buyer when the next correction creates the next great big investment opportunity. Until then, play solid defense.

The great Sir John Templeton once told me that the secret to his success is that he “buys when everyone else is selling and sells when everyone else is buying.” It is ringing in my head today. He also added, “It sounds easy but it will be one of the most difficult things for you to do.” Amen, Sir John.

Let the historical math and common sense of median P/E valuations help show the way.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kindest regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

Trade Signals History:

Trade Signals started after a colleague asked me if I could share my thoughts (Trade Signals) with him. A number of years ago, I found that putting pen to paper has really helped me in my investment management process and I hope that this research is of value to you in your investment process.

Following are several links to learn more about the use of options:

For hedging, I favor a collared option approach (writing out-of-the-money covered calls and buying out-of-the-money put options) as a relatively inexpensive way to risk protect your long-term focused equity portfolio exposure. Also, consider buying deep out-of-the-money put options for risk protection.

Please note the comments at the bottom of Trade Signals discussing a collared option strategy to hedge equity exposure using investor sentiment extremes is a guide to entry and exit. Go to www.CBOE.com to learn more. Hire an experienced advisor to help you. Never write naked option positions. We do not offer options strategies at CMG.

Several other links:

http://www.theoptionsguide.com/the-collar-strategy.aspx

IMPORTANT DISCLOSURE INFORMATION

Past performance is no guarantee of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. (or any of its related entities, together “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods. Mutual funds involve risk including possible loss of principal. An investor should consider the fund’s investment objective, risks, charges, and expenses carefully before investing. This and other information about the CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM is contained in each fund’s prospectus, which can be obtained by calling 1-866-CMG-9456 (1-866-264-9456). Please read the prospectus carefully before investing. The CMG Global Equity FundTM, CMG Tactical Bond FundTM, CMG Global Macro Strategy FundTM and the CMG Long/Short FundTM are distributed by Northern Lights Distributors, LLC, Member FINRA.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Hypothetical Presentations: To the extent that any portion of the content reflects hypothetical results that were achieved by means of the retroactive application of a back-tested model, such results have inherent limitations, including: (1) the model results do not reflect the results of actual trading using client assets, but were achieved by means of the retroactive application of the referenced models, certain aspects of which may have been designed with the benefit of hindsight; (2) back-tested performance may not reflect the impact that any material market or economic factors might have had on the adviser’s use of the model if the model had been used during the period to actually manage client assets; and (3) CMG’s clients may have experienced investment results during the corresponding time periods that were materially different from those portrayed in the model. Please Also Note: Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that future performance will be profitable, or equal to any corresponding historical index. (e.g., S&P 500® Total Return or Dow Jones Wilshire U.S. 5000 Total Market Index) is also disclosed. For example, the S&P 500® Total Return Index (the “S&P 500®”) is a market capitalization-weighted index of 500 widely held stocks often used as a proxy for the stock market. S&P Dow Jones chooses the member companies for the S&P 500® based on market size, liquidity, and industry group representation. Included are the common stocks of industrial, financial, utility, and transportation companies. The historical performance results of the S&P 500® (and those of or all indices) and the model results do not reflect the deduction of transaction and custodial charges, nor the deduction of an investment management fee, the incurrence of which would have the effect of decreasing indicated historical performance results. For example, the deduction combined annual advisory and transaction fees of 1.00% over a 10-year period would decrease a 10% gross return to an 8.9% net return. The S&P 500® is not an index into which an investor can directly invest. The historical S&P 500® performance results (and those of all other indices) are provided exclusively for comparison purposes only, so as to provide general comparative information to assist an individual in determining whether the performance of a specific portfolio or model meets, or continues to meet, his/her investment objective(s). A corresponding description of the other comparative indices, are available from CMG upon request. It should not be assumed that any CMG holdings will correspond directly to any such comparative index. The model and indices performance results do not reflect the impact of taxes. CMG portfolios may be more or less volatile than the reflective indices and/or models.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group

© CMG Capital Management Group