The Employment Report is by far the most important data release for the financial markets. However, investors aren’t always aware that the figures are statistics, reported with a fairly large degree of uncertainty. That raises the possibility of overreactions to what may just be noise. That said, the broad range of job market data is consistent with further improvement in labor conditions. At the same time, we can expect the pace of job growth to slow over time, simply because it has to.

Prior to seasonal adjustment, the economy added over one million jobs in April (seems a little silly to worry about the nearest 40,000 or 50,000 in the adjusted figure). Payrolls were reported to have risen by 160,000 after adjustment. That figure is subject to revision, of course, and is reported accurate to ±115,000 (this represents a 90% confidence interval for those of you who remember that class in statistics). We can be 90% confident that the true monthly change was between +45,000 and +275,000. The bottom line is that one should take the monthly figures with a grain of salt. One can reduce the impact of noise in the payroll data by taking the three-month average. Payrolls averaged a 200,000 gain over the last three months – still fairly strong (+192,000 for private-sector payrolls).

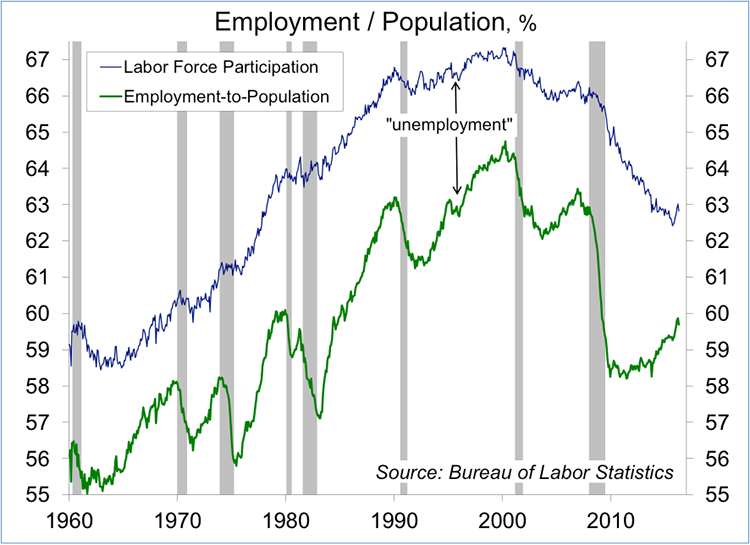

The household survey data are based on a sample of about 60,000 households. That may seem small, and it doesn’t provide good estimates of employment (reported accurate to ±300,000), but it’s large enough to yield reasonably accurate estimates of ratios, such as labor force participation or the unemployment rate (reported accurate to ±0.2%). The unemployment rate held steady at 5.0% in April, but labor force participation fell from 63.0% in March to 62.8%, and the employment/population ratio fell to 59.7% from 59.9%. Those declines are well within the usual amount of statistical noise. We would need further data to confirm a change in trend.

It’s a presidential election year, so that means we will hear various claims about the strength or weakness of the economy. One assertion is that growth has been substantially lower in this recovery than in past recoveries. That is true. Another claim is that GDP growth can easily be boosted to 4% per year. Demographics played a big part in the past and will also play a big part in future economic growth, but this also brings us back to the topic of productivity growth.

Labor force participation rose significantly from the 1960s to the 1990s, reflecting women entering the workforce in greater numbers. That trend has played itself out – so jobs should rise more or less in line with the growth in the working-age population. In the 1990s, we also started to see a trend of lower participation (beginning first with men). It’s estimated that a half to three-quarters of the drop in participation since 2007 has been due to the aging population. Looking ahead, the Bureau of Labor Statistics expects the labor force to rise about 0.5% per year over the next 10 years. Hence, this is largely a story of faster labor force growth in the past, and slower labor force growth in the future.

Economic growth is also dependent on productivity (output per worker). The preliminary estimate of 1Q16 productivity growth was terrible. These data can be quirky, but the year-over-year trend remained soft, in line with the weak pace that has prevailed over the last five years. Since the demographic outlook is set (save for immigration), political candidates should then focus on what they will do to boost productivity growth. Efforts to lift capital spending make sense, but borrowing costs are already low. This doesn’t appear to be a problem with supply. Rather, firms won’t want to expand unless they are confident that the demand will be there for the goods and services they produce. The whittling away of the middle class likely plays a part in that moderate demand outlook.