Mid-cap Dividend Growth Stocks by Sector - Part 2C: REITs and Real Estate Management

Introduction

This is the final installment in my series of articles on fairly valued mid-cap selections. My inspiration to produce these articles was at the request and suggestion from regular readers who were frustrated at the lack of coverage and/or articles on mid-caps. To accommodate those requests, I screened through the S&P 400 mid-cap index with the assumption that it represented a credible universe of high-quality mid-caps. The fact that I was only reviewing the S&P 400 index was missed based on many comments received on my previous articles in this series. In other words, I only included fairly valued research candidates that are members of the S&P 400 index in this series.

As I was reviewing this universe of mid-cap stocks, it became quite clear that there were more differences between individual mid-cap companies than there were similarities. Therefore, I organized the mid-cap research candidates into a series based on various industries and sectors. In part 1, I focused primarily on mid-cap stocks for growth. In part 2 I turned my focus towards dividend paying mid-caps. However, I broke part 2 into parts 2A and part 2B where I covered regional banks and Consumer Discretionary dividend growth stocks. In this final part 2C in this article series, I am presenting REITs and real estate oriented mid-caps.

Furthermore, it’s important to point out that my primary objective was to present a group of apparently fairly valued mid-caps based on a cursory screen. Therefore, I left it up to the reader to conduct their own comprehensive research and due diligence on any of these research candidates that appeal to them. To clarify further, throughout this series I am not suggesting that these are the best mid-cap stocks to invest in. Instead, I endeavor to present mid-cap selections from the S&P 400 index that currently appear attractively valued.

To summarize, just as it is with every other equity class, there are many different types of mid-size companies with each possessing different features and characteristics. For example, the mid-cap universe contains many intriguing growth opportunities. On the other hand, the mid-cap universe also contains dividend-paying companies of all categories. Investors can find high-yielding mid-caps, moderate-yielding above-average growing mid-caps, and everything in between. Simply stated, not all mid-caps are the same. The real estate oriented research candidates presented below come in all the flavors mentioned above.

Real Estate Investments and the Liquidity Factor

The two most dominant forms or choices for equity investors are stocks and real estate. Equity investing is also referred to as ownership versus investing in debt instruments often referred to as loaner-ship. In other words, equity investors position themselves as owners of the asset they are investing in. In contrast, investing in debt instruments is mostly associated with a guaranteed or consistent income stream in the form of interest payments. However, debt instruments typically do not afford the opportunity to participate in growth or gain in excess of your original investment. On the other hand, although equity investing implies participating in potential gains, it is also more exposed to participating in potential losses. These factors represent the primary difference between equity investing versus debt investing.

In regards to the two major equity classes, real estate or stocks, the primary differentiator has traditionally been liquidity. Common stocks are publicly traded on stock exchanges and therefore readily liquid. In contrast, real estate typically requires a significant effort and time in order to complete a sale. In other words, real estate is generally not considered a liquid investment class.

Furthermore, liquidity can be either a positive or negative attribute. On the positive side, if you need to raise cash for any reason, the liquidity provided with stock ownership easily facilitates that need. Moreover, depending on how much cash you need, you might only be required to sell a small portion of your holdings. However, if for example you are invested in a rental property such as a house, you cannot simply sell the kitchen and keep the rest of the house. If you need cash out of an investment, you are forced to sell the entire asset. Under these circumstances, liquidity is a positive for stocks and a negative with real estate.

On the other hand, liquidity can also be a significant negative. With the liquidity provided with stocks, you might need cash during a bear market and consequently be forced to sell your asset for less than it’s worth. Or worse yet, a bear market can incite panic in the investor’s mind causing them to sell their asset at a loss simply because they have become frightened. In contrast, the time and effort required to sell a piece of real estate may save the investor from making such a mistake. In that case, real estate’s lack of liquidity can be a real benefit.

Legendary investor Warren Buffett explains the liquidity factor far better and in a much more entertaining fashion than I. Warren is comparing two illiquid real estate investments he made in the early 1990s to his experience in owning stocks. The following excerpt from his 2013 letter to shareholders summarizes and clarifies what I said above:

“There is one major difference between my two small investments and an investment in stocks. Stocks provide you minute-to-minute valuations for your holdings whereas I have yet to see a quotation for either my farm or the New York real estate. It should be an enormous advantage for investors in stocks to have those wildly fluctuating valuations placed on their holdings – and for some investors, it is.

After all, if a moody fellow with a farm bordering my property yelled out a price every day to me at which he would either buy my farm or sell me his – and those prices varied widely over short periods of time depending on his mental state – how in the world could I be other than benefited by his erratic behavior? If his daily shout-out was ridiculously low, and I had some spare cash, I would buy his farm. If the number he yelled was absurdly high, I could either sell to him or just go on farming.

Owners of stocks, however, too often let the capricious and often irrational behavior of their fellow owners cause them to behave irrationally as well. Because there is so much chatter about markets, the economy, interest rates, price behavior of stocks, etc., some investors believe it is important to listen to pundits – and, worse yet, important to consider acting upon their comments.

Those people who can sit quietly for decades when they own a farm or apartment house too often become frenetic when they are exposed to a stream of stock quotations and accompanying commentators delivering an implied message of “Don’t just sit there, do something.” For these investors, liquidity is transformed from the unqualified benefit it should be to a curse.

A “flash crash” or some other extreme market fluctuation can’t hurt an investor any more than an erratic and mouthy neighbor can hurt my farm investment. Indeed, tumbling markets can be helpful to the true investor if he has cash available when prices get far out of line with values. A climate of fear is your friend when investing; a euphoric world is your enemy.

During the extraordinary financial panic that occurred late in 2008, I never gave a thought to selling my farm or New York real estate, even though a severe recession was clearly brewing. And, if I had owned 100% of a solid business with good long-term prospects, it would have been foolish for me to even consider dumping it. So why would I have sold my stocks that were small participations in wonderful businesses? True, any one of them might eventually disappoint, but as a group they were certain to do well. Could anyone really believe the earth was going to swallow up the incredible productive assets and unlimited human ingenuity existing in America?”

REITs: Real Estate in Liquid Form

According to NAREIT (the National Association of Real Estate Investment Trusts):

“A REIT, or Real Estate Investment Trust, is a company that owns or finances income-producing real estate. Modeled after mutual funds, REITs provide investors of all types regular income streams, diversification and long-term capital appreciation. REITs typically pay out all of their taxable income as dividends to shareholders. In turn, shareholders pay the income taxes on those dividends.

REITs allow anyone to invest in portfolios of large-scale properties the same way they invest in other industries – through the purchase of stock. In the same way shareholders benefit by owning stocks in other corporations, the stockholders of a REIT earn a share of the income produced through real estate investment – without actually having to go out and buy or finance property.”

Definitionally speaking, NAREIT also explains the REIT structure as follows:

“To qualify as a REIT a company must:

- Invest at least 75 percent of its total assets in real estate

- Derive at least 75 percent of its gross income from rents from real property, interest on mortgages financing real property or from sales of real estate

- Pay at least 90 percent of its taxable income in the form of shareholder dividends each year

- Be an entity that is taxable as a corporation

- Be managed by a board of directors or trustees

- Have a minimum of 100 shareholders

- Have no more than 50 percent of its shares held by five or fewer individuals”

3 Attractively Valued S&P 400 Mid-Cap REITs and One Real Estate Management Company

The following F.A.S.T. Graphs™ portfolio review summarizes the three fairly valued mid-cap dividend growth stocks in the REIT sector and the real estate management company. The portfolio review lists them by ticker, name, credit rating, sector, price to FFO/cash flow, dividend yield, market cap and long-term debt to capital. The companies are listed in order of highest dividend yield to lowest.

Investment Thesis

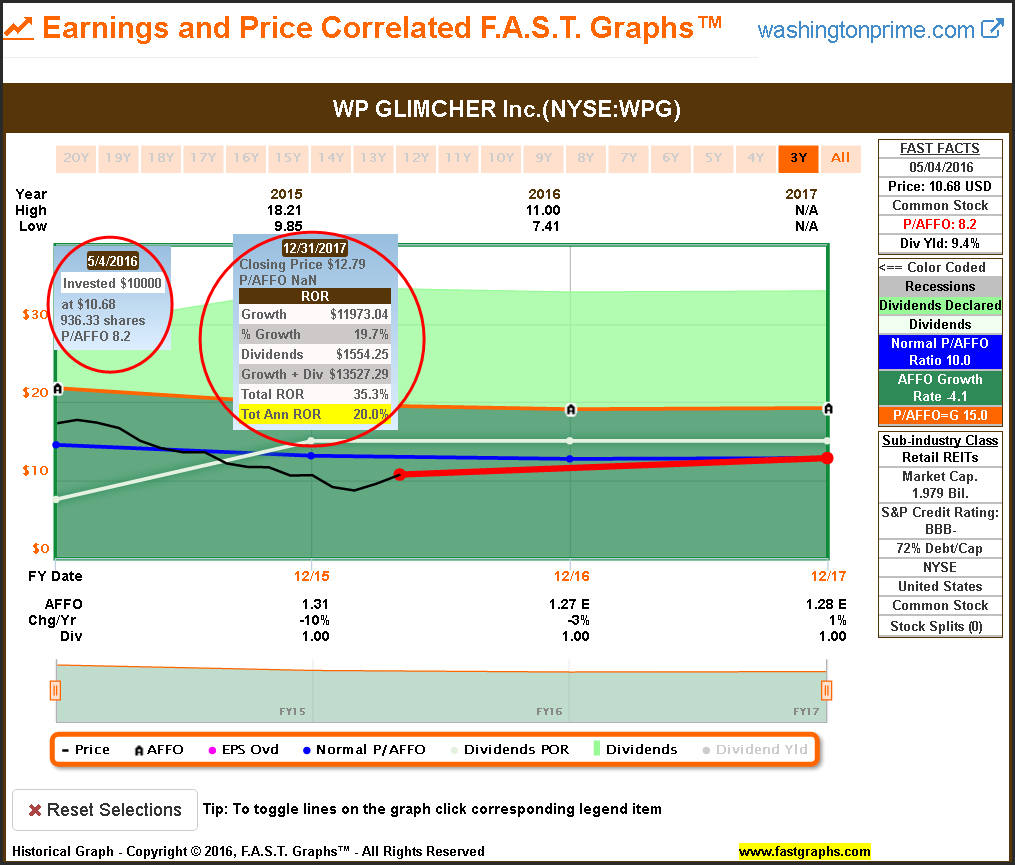

Although WP Glimcher is a relatively new entity with little history, I included it in this article because of its high current yield and extreme low valuation. Therefore, I believe a significant portion of the risk is already included in its price (low valuation). However, as is the case with many spinoffs, the company’s high debt to capital ratio is a concern.

Company description:

“WP Glimcher Inc (NYSE: WPG) is a multi-faceted retail real estate investment trust (REIT) with a portfolio of 118 shopping centers, including enclosed regional malls, open-air lifestyle centers and community centers. The company specializes in the ownership, management and development of retail shopping centers throughout the U.S.

WP Glimcher was formed following Washington Prime Group’s (NYSE: WPG) acquisition of Glimcher Realty Trust (NYSE: GRT) in January 2015. Washington Prime Group was formed in May 2014 following a spin-off from Simon Property Group. Today the company operates out of our headquarters in Columbus, Ohio, and we have an additional office in Indianapolis, Indiana.

As a premier retail real estate company, WP Glimcher is focused on the experience we create at each of our centers. By providing a mix of things to do and things to buy, WP Glimcher delivers the right combination of tenants, activities and events to keep shoppers engaged and returning to our properties. The company also offers more than 66 million square feet of space for retailers looking to grow in the U.S. We pride ourselves on creating meaningful relationships with our partners.

Focused on our people and the areas our properties serve, WP Glimcher places great emphasis on fostering a positive and strong culture and giving back to the community. The company’s values are based on open communication, continuous feedback and fostering a positive work environment.”

WP Glimcher (WPG)

Investment Thesis

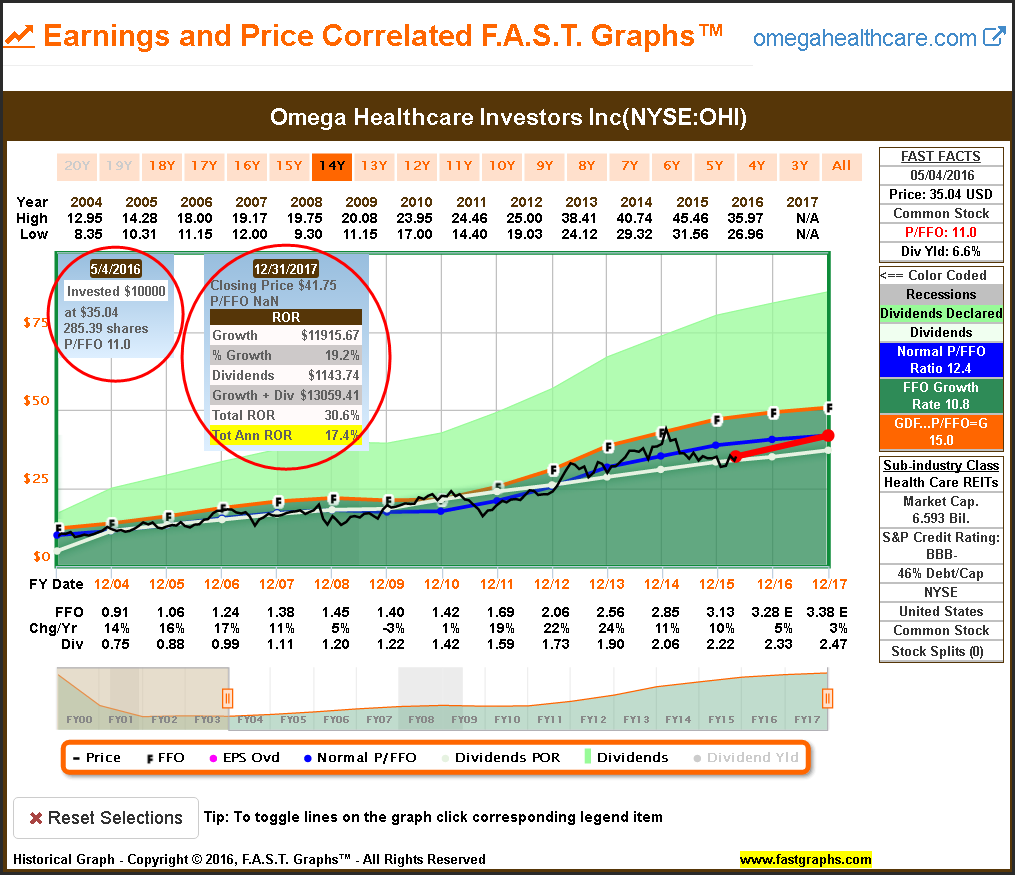

I included Omega Healthcare Investors based on its above-average yield, consistent historical FFO growth and low current valuation. For disclosure, I am currently long OHI, and I will refer to REIT expert Brad Thomas and his article found here to provide insights into this quality healthcare REIT.

Omega Healthcare Investors Inc (OHI)

Investment Thesis

I included EPR Properties as a fairly valued if not fully valued above-average yield REIT with a consistent operating history based on FFO growth. Additionally, I included this research candidate because of its monthly dividend payment schedule which I felt might appeal to many dividend income investors.

EPR Properties (EPR)

Investment Thesis

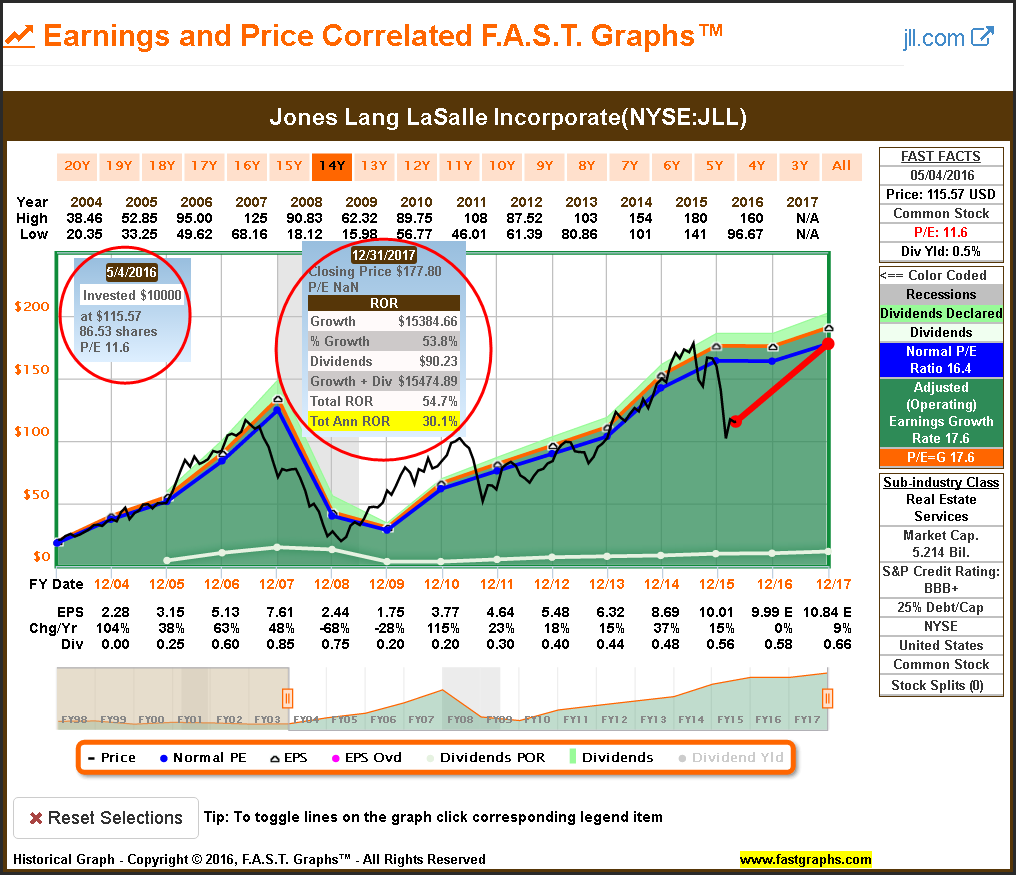

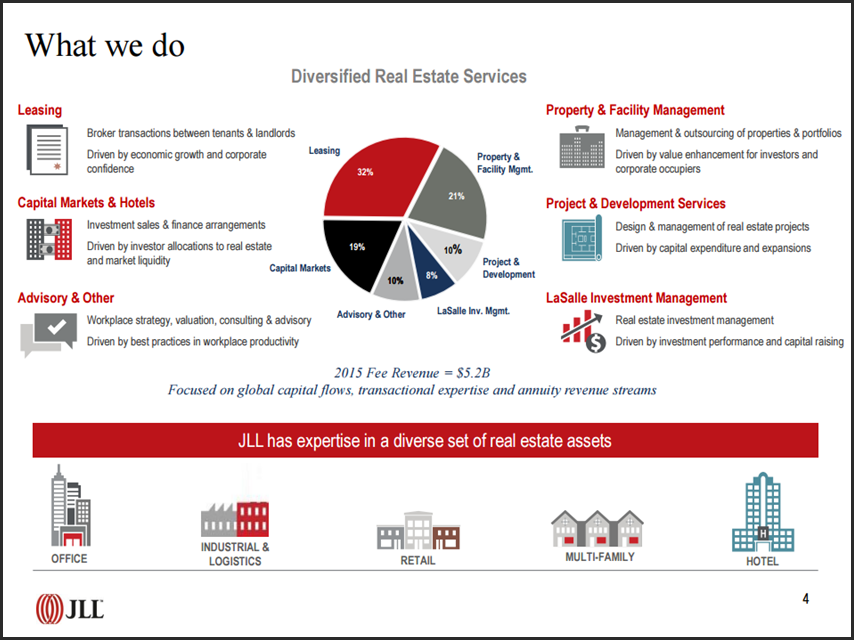

My fourth and final research candidate, Jones Lang LaSalle, operates in the real estate industry, however, it is not a REIT. My primary motivation for including it as a research candidate was its low valuation indicating the potential for significant capital gains. This real estate management company does pay a small dividend but not enough to attract the dividend investor. Consequently, it is offered purely as a capital gain based on potential price recovery candidate. With this in mind, I’ve included two F.A.S.T. Graphs™ with this example.

The first is a price and cash flow correlated valuation reference, and the second a price and earnings correlated valuation reference. Although the company looks attractive on both earnings and cash flows, Jones Lang LaSalle looks especially compelling relative to operating earnings.

Jones Lang LaSalle Inc (JLL)

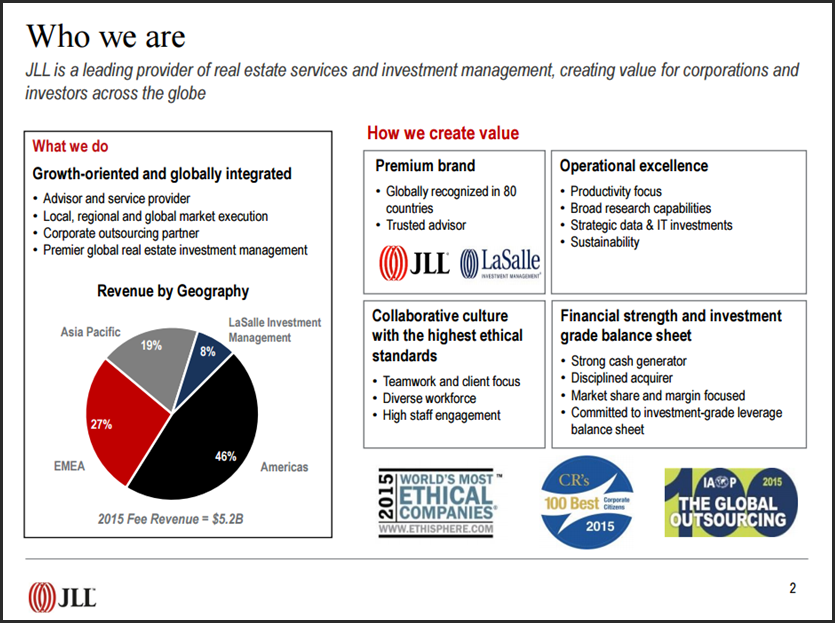

For those readers not familiar with this company, I have included a few slides from its most recent investor presentation.

Summary and Conclusions

This concludes my series on fairly valued mid-cap stocks. Not every investor may be willing to consider smaller size companies for their investment portfolios, especially those investors in retirement. However, smaller size companies generally have more room to grow than their larger counterparts. Consequently, there are those investors that prefer smaller companies on the belief that they are capable of growing faster - thereby generating larger gains.

On the other hand, my review of the S&P 400 mid-cap index found very few companies in the mid-cap class that I considered attractively valued enough currently to include as potential research candidates. Nevertheless, at the request of several readers, I choose this series of articles on mid-caps. Although I believe that the growth of a business represents one of the best sources of higher total returns, it only works when valuations are reasonable or attractive. Caveat emptor.

Disclosure: Long OHI

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.