IN THIS ISSUE:

1. US Economy Grows by Weakest Pace in Two Years

2. 90% of Americans Worse Off Today Than in 1970s

3. 24% of Voters May Not Vote For Trump or Clinton

Overview

Today we will focus on a recent study from the Levy Economics Institute which found that 90% of Americans were worse off financially in 2015 than at any time since the early 1970s. Furthermore, for the vast majority of Americans, the nation’s economy is in a prolonged period of stagnation, worse even than that of Japan.

So are we really worse off today than Japan? This latest study concludes that the answer is YES, when it comes to real income – that is, income adjusted for inflation. According to their findings, 90% of Americans earn roughly the same real income today as the average American earned back in the early 1970s. It’s an eye-opening look at how the vast majority of Americans are struggling to make ends meet.

Before we get to that discussion, let’s take a look at last Thursday’s disappointing report on 1Q Gross Domestic Product. We will round-out today’s E-Letter with some interesting polling data from Rasmussen, which suggests that up to 24% of American voters may not vote for Donald Trump or Hillary Clinton and may just stay home on Election Day if they are the nominees. Wow!

US Economy Grows by Weakest Pace in Two Years

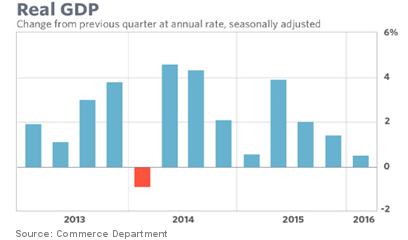

Last Thursday’s initial 1Q GDP report came in below expectations and deserves some additional analysis. The US economy expanded in the 1Q at the slowest pace in two years as American consumers reined-in spending and companies tightened their belts in response to weak global financial conditions and the plunge in oil prices.

1Q Gross Domestic Product rose at a 0.5% annualized rate after a 1.4% 4Q advance, the Commerce Department reported. The increase was well below the 0.9% pre-report consensus and marked the third straight disappointing start to a new year. This advance report will be revised two more times at the end of May and June.

As you can see above, US GDP has been trending lower each quarter since the 2Q of 2015. Weaker global economies and oil’s tumble resulted in the biggest business-investment slump in almost seven years in the 1Q, and household purchases climbed the least since early 2015, the GDP data showed.

While Federal Reserve officials acknowledged the 1Q softness in their policy statement last Wednesday, they also suggested that strong hiring and recent tepid income gains have the potential to reignite consumer spending and propel economic growth stronger later this year... but they almost always point to something positive.

The fact that personal consumption growth slowed in the 1Q is a disappointment, especially in light of much lower gasoline and energy prices from a year ago. Household purchases, which account for almost 70% of the economy, rose at a 1.9% annual pace last quarter, compared with 2.4% in the final three months of last year.

Consumer spending, while slightly better than the 1.7% median forecast, was a disappointment in light of the consumer-friendly fundamentals including low gasoline prices, cheap borrowing costs, increased hiring and warmer-than-usual winter weather.

Thursday’s GDP report showed disposable income adjusted for inflation climbed 2.9% in the 1Q, an improvement from the 2.3% gain in the final three months of 2015. The savings rate ticked up to 5.2% in the 1Q from 5.0% in the 4Q of last year. Government spending rose at a 1.2% pace, led by states and municipalities. That’s about it for the good news.

The biggest negative factor weighing on the economy last quarter came from companies. Nonresidential fixed investment, or spending on equipment, structures and intellectual property, dropped at a 5.9% annualized pace, the biggest decline since the 2Q of 2009. This was much worse than expected.

Investment is also languishing as corporations struggle to boost profits against a backdrop of weak overseas demand and restrained domestic purchases. Consumers in the US scaled back purchases, and companies continued to trim inventories to bring them more in line with sales.

Inventories subtracted 0.33% from GDP growth after a 0.22 percentage-point drag in the 4Q of 2015. Progress in trimming inventories, along with receding headwinds from abroad and the latest comeback in the prices of oil and other commodities, may keep investment from deteriorating further. Weaker demand from overseas customers led to a drop in exports in the 1Q. Trade subtracted 0.34% from GDP growth, the most in a year.

Stripping out unsold goods and trade, the two most volatile components of GDP, as well as government expenditures, so-called final sales to private domestic purchasers increased at a 1.2% rate, the weakest advance since the third quarter of 2012.

Several forecasters suggested that the 1Q will be the worst quarter for consumption and the economy for all of 2016, as has been the case the last couple of years. In 2015, GDP rose 0.6% in the 1Q before rebounding to a 3.9% pace in the 2Q. In 2014, the economy shrank at a 0.9% rate in the 1Q and jumped by a 4.6% rate in the April-June period.

Remember, the weak starts in 2014 and 2015 were attributed to severe winter weather, which was not the case this year when we had a very mild winter in most parts of the country. So it remains to be seen if we will see a similar rebound just ahead.

Now let’s get on to our main topic for today.

90% of Americans Worse Off Financially Today Than in 1970s

A recent study in March from the Levy Economics Institute found that 90% of Americans were worse off financially in 2015 than at any time since the early 1970s. Furthermore, for the vast majority of Americans, the nation’s economy is in a prolonged stagnation, far worse than that of Japan. Worse than Japan?

When we think of the Japanese economy, we think of the “Lost Decades.” Japan’s economy was the envy of the world in the 1980s, but starting in 1991, it fell into a prolonged recession and deflation which lasted from then to 2010. Japan’s GDP fell from $5.33 trillion to $4.36 trillion during that period, which saw wages fall by apprx. 5%.

So are we really worse off today than Japan? The Levy Economics Institute at Bard College thinks the answer isYES, when it comes to real income – that is, income adjusted for inflation. According to their findings, 90% of Americans earn roughly the same real income today as the average American earned back in the early 1970s.

As a result of this stagnation in incomes and the plunge in housing values during the Great Recession, 99% of American households have seen their net worth fall since 2007 according to the study. Economic stagnation hasn’t reached the remaining 1% of the US population, which has seen a recovery in their real incomes over the same period to near new highs.

The chart above has not been updated to include results for 2015, but the trends are clear. The bottom 99% of US income-earning households have seen their net worth decline since the financial crisis of 2007-2009.

Once upon a time, the American economy worked for nearly everybody, and even the middle class got richer. Things were quite different in the decades preceding the 70s, a period that stretches back to the late 1940s, when real incomes rose for both groups.

Simply put, for the vast majority of Americans, the dream of a steady increase in income was lost back in the early 1970s. What can explain this big shift in the income distribution in the last four decades?

One clue is in the timeframe of the shift, which coincides with the growing openness of the American economy to international trade and investments. Many believe that globalization is largely to blame.

An open economy pitted American entrepreneurs and workers against overseas peers. For the top 10% of the population, those with the right skills, an open American economy was a good thing, a source of efficiency and opportunity that translated into higher real incomes.

Yet for the remaining 90% of the population, those with the wrong skills or little skills, the openness of the US economy was a bad thing, a source of job losses and lower incomes.

Another contributing factor, as I wrote in my blog last Thursday, is out-of-control federal regulations, especially during the Obama administration. The Code of Federal Regulations is now more than 81,000 pages long.

A new study from George Mason University found that the US economy would have been $4 trillion -- or 25% -- bigger than it was in 2012 had federal regulations been capped at 1980 levels. This is astonishing!

Getting back to our topic, there is yet another clue why 90% of Americans are worse off today than in the 1970s. The shift in income distribution became worse in the aftermath of the Great Recession, which brings up yet another reason for the decline: the ultra-low interest rate monetary policy, which boosted the prices of stocks and bonds, mostly benefiting the top 10%, which were very likely to own these assets.

On a political note, maybe this explains why so many people are rallying behind Donald Trump and Bernie Sanders who blame both globalization and Wall Street for depriving many Americans of the dream for a better life.

This topic deserves more attention which I will provide in the weeks ahead.

24% of Voters May Not Vote For Trump or Clinton

I have not commented on the politics surrounding the presidential primaries this year. Yet this is an election season like none other we have seen in decades. According to Rasmussen Reports, this year is shaping up to be a historic election.

Specifically, nearly one-in-four voters say they will stay home or vote for a third party candidate if Hillary Clinton and Donald Trump are the major party presidential candidates, so said Rasmussen last week. Its latest survey was conducted April 25-26.

The latest Rasmussen Reports national telephone survey of “Likely US Voters” found Trump and Clinton tied at 38% each. But 16% say they would vote for some other candidate if the presidential election comes down to those two, while 6% would simply stay home, with another 2% undecided.

Still, the picture appears to be improving for both candidates. In early March, 49% of voters told Rasmussen they would definitely vote against Trump if he is the presidential nominee of the Republican Party. Yet nearly as many (42%) said they would definitely vote against Clinton if she is the Democratic Party’s nominee.

Trump is more toxic within his own party than Clinton is in hers. If Trump is the Republican nominee, 16% of GOP voters say they would choose a third-party candidate, while 5% would stay home. Two-thirds of Republicans (66%) now say they would vote for Trump, but 10% would vote for Clinton instead.

If Clinton is the Democratic nominee, 11% of Democrats would vote third-party, while just 3% would stay home. Three-fourths (75%) would support the nominee, but 11% say they would vote for Trump.

Among voters not affiliated with either major party, nearly one-third say they would opt out: 21% would choose a candidate other than Trump or Clinton, and 10% would stay home. Trump leads Clinton 38% to 27% among unaffiliated voters, according to Rasmussen.

Obviously, both Trump and Clinton are unpopular with many Americans. The latest poll above shows Trump with higher negatives than Clinton. However, Trump may have a better chance of improving his negatives with voters than Clinton. Why?

Hillary Clinton has been in or around national politics since her husband became president in 1993. Everyone knows her. Trump on the other hand is a relative newcomer to politics. Voters may be more likely to change their opinion of Trump than of Hillary. Of course, it’s impossible to know if voters’ opinions of Trump will change for the better or the worse. We’ll see.

All the best,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.