Headline consumer confidence was a bit softer in April. The Consumer Confidence Index fell to 94.2 from 96.2 in March. This was below expectations of 95.8. The weakness in the report came from the expectations component as it fell by 4.3. The present situation component actually rose by 1.6.

For just the second month since the financial crisis, jobs are perceived to be more plentiful than they are perceived to be hard to get. The only other month since 2008 that this occurred was in September 2015. This is a positive sign for further declines in the unemployment rate. History over the past 30 years suggests that if expectations that jobs are more plentiful continue to increase compared to expectations that jobs are hard to find, the overall unemployment rate should fall further.

Since 2014, more consumers have expected to receive a raise than those who expected to see their income decrease. Prior to the financial crisis, this was usually a positive signal that the employment cost index (ECI) would be growing at around a 3% year-over-year rate. However, as has been widely reported, in the past two years the ECI has only been growing at about 2% year-over-year rate. Only time will tell if this a new structural level for wage growth or if the ECI will eventually accelerate to previous historic levels.

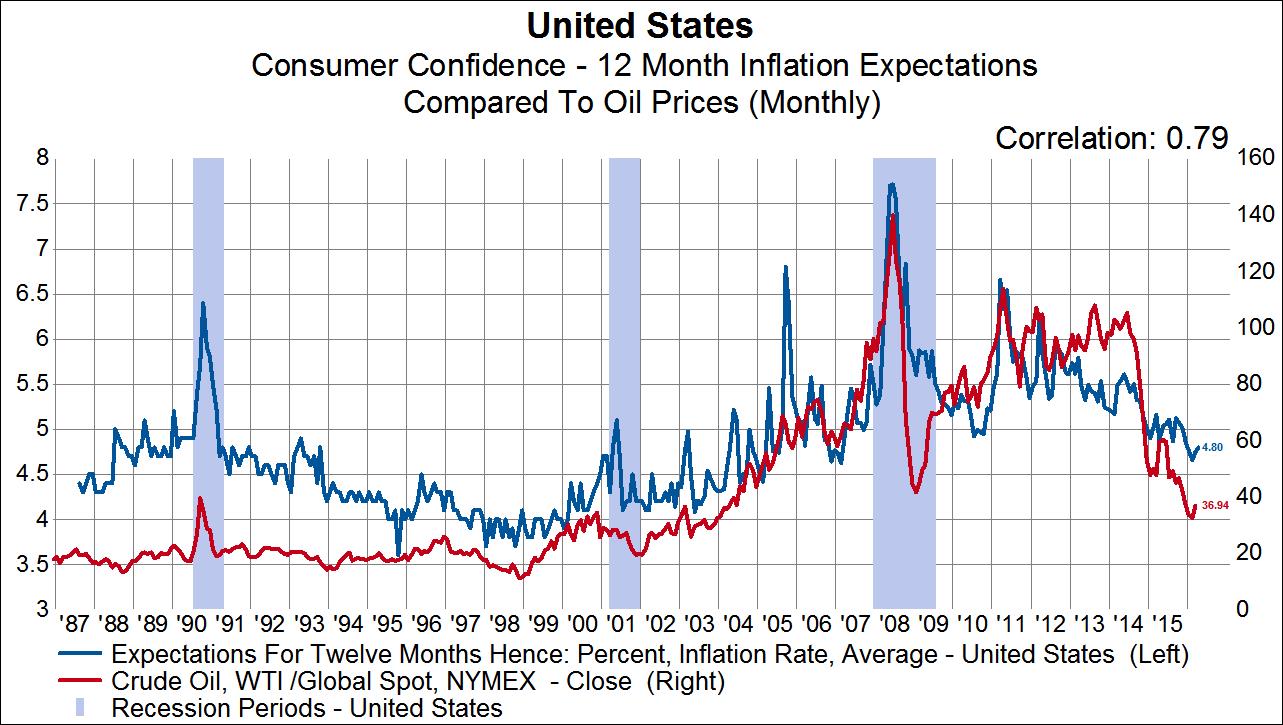

Given how important inflation expectations are to the Fed, we are sure they are keeping tabs on the series below. 12-month inflation expectations have steadily fallen since making a cyclical high in 2011 at 6.66%. The latest reading provided a slight bounce but outside of 2016, at just 4.80, its at the lowest level since 2007. As the chart below shows consumer’s inflation expectations are highly correlated with oil prices. If lower oil prices are here to stay, then embedded inflation expectations may continue to fall (at the detriment of the Fed’s dual mandate).

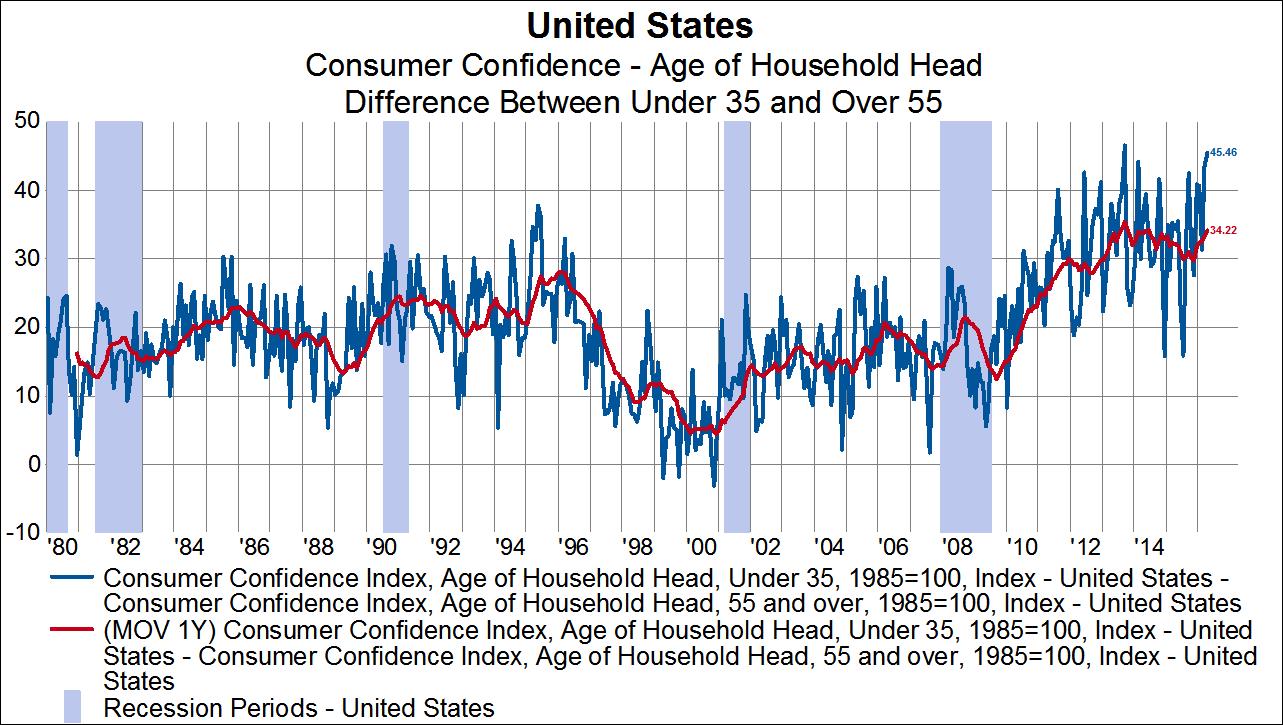

On the heels of the news that the millennial generation is officially larger than the baby boom generation, the difference in the consumer confidence between the two generations is at its second highest level since 1980. Millennials are much more confident than baby boomers. There is a 45.5 point spread between the consumer confidence levels of those under 35 compared to those over 55. The only point that this spread was higher was in September 2013. As the below chart shows, there has been a structural shift in this relationship since the financial crisis. The 1-year moving average has been above 28.5 since September 2011. The one-year moving average never hit that level from 1980-2011.