Just when you thought all the fear-mongering had subsided, the national debt has resurfaced as a topic in this year’s presidential race. Yes, the deficit is large. No, it is not a problem. However, there some concerns about the longer run.

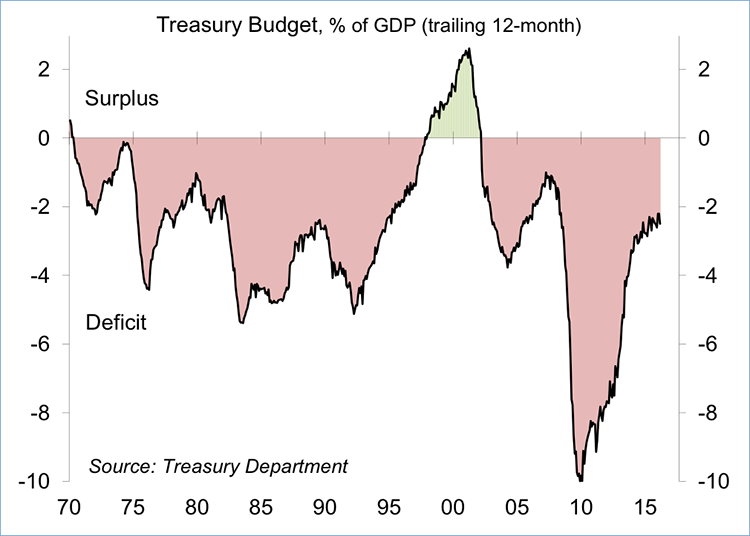

The federal budget deficit hit $1.4 trillion in FY09, or about 10% of nominal GDP. That is enormous, but it simply reflected the magnitude of the Great Recession. Revenues fell. Recession-related spending (unemployment insurance, fiscal stimulus) rose. As the economy recovered, recession-related spending went away and tax receipts improved. The deficit is now down to 2.5% of GDP, which is sustainable.

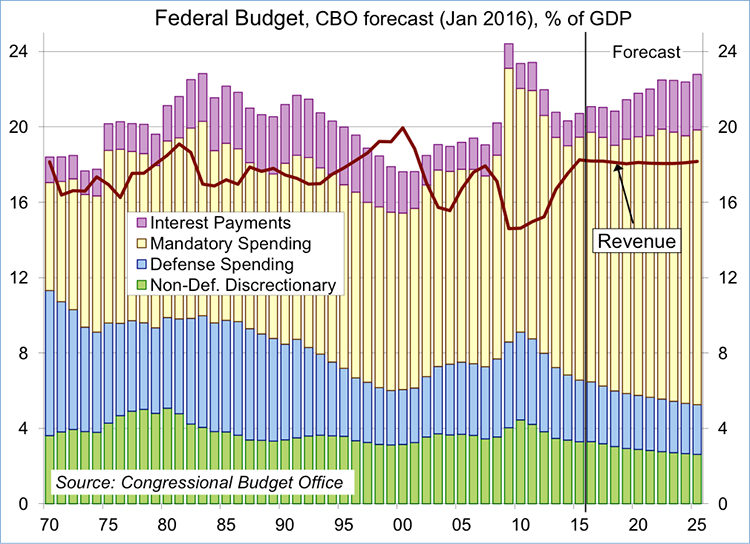

Some politicians talk as if cutting the deficit were simply a matter of “trimming the fat.” However, if one excludes social Security, Medicare, interest payments, and defense outlays, there’s not a whole lot left to cut. If you cut nondefense discretionary spending to zero over the next 10 years, you would still be running a budget deficit.

While the deficit (as a percentage of GDP) is currently manageable, it is expected to rise in the years ahead as the baby-boom generation continues to move into retirement. The Congressional Budget Office projects that the deficit will approach 5% of GDP by FY26. So, something’s going to have to give at some point. We can reduce the deficit (or limit its growth) by scaling back entitlements or by raising revenues. Some now argue (I kid you not) that we have to cut entitlements now so that we don’t have to cut them later (which makes no sense if you think about it for more than a second). Raising revenues is tricky. Republicans aren’t going to go along with increases in tax rates (even if called “revenue enhancements,” as they were during the Reagan years). Broadening the tax base, as part of overall tax reform, could get bipartisan support, but that means giving up certain tax breaks that some will object to (that is, those benefiting from those tax breaks). It’s true that the U.S. has one of the highest corporate tax rates in the world, but the effective rate (what corporations actually pay) is among the lowest. If you started from scratch, you could certainly come up with a better, more efficient tax system, but the problem is you can’t start from scratch.

The national debt, the sum of past budget deficits, is now over 100% of GDP. However, marketable debt is about 76% of GDP (the difference is the money that the government owes itself, mostly the Social Security and Medicare trust funds). There is no magic level of debt that gets an economy in trouble. Research arguing that view has been discredited. The federal government currently has no problem borrowing, nor is there any evidence that it is crowding out private investment.

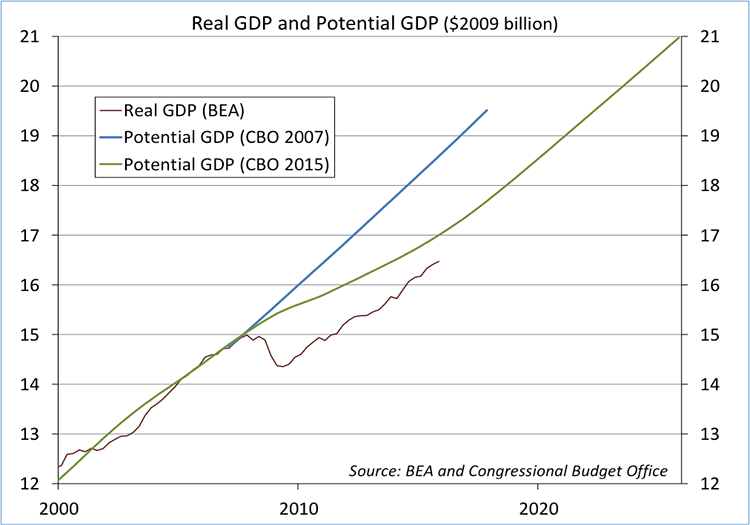

Here is something to worry about. The Great Recession has put potential GDP on a lower, slower track. This makes future budget strains more of a problem than if we had remained on the pre-recession trajectory. More unsettling, that assumes that the economy does not stumble into a recession along the way.